PPRUF - Richemont's Timeless Brands Offer An Attractive Investment Opportunity Following The Recent Sell-Off Across The Luxury Market

2023-11-24 05:17:34 ET

Summary

- Number 1 in hard luxury category.

- 27 luxury maisons with histories stretching back to 1755.

- P/E of 14x (historical average of 21x).

- No net debt.

Note: All figures are in EUR (€) unless stated otherwise.

Introduction

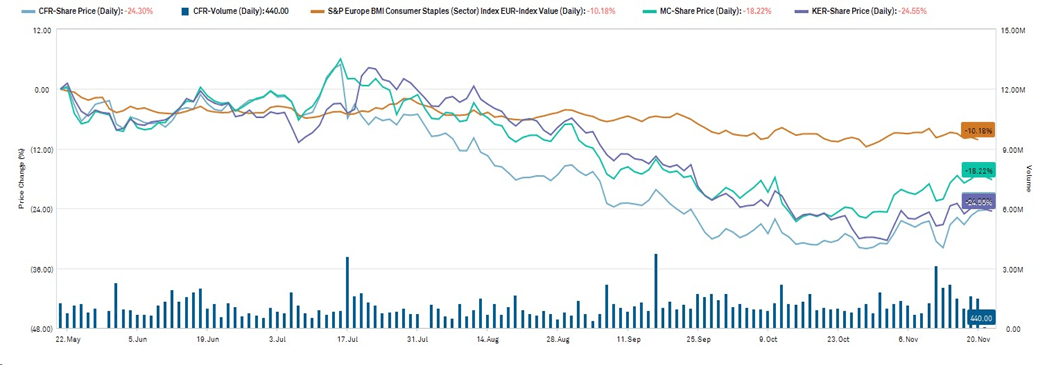

The share prices of the major luxury houses (LVMH (LVMHF), Kering (PPRUF), Richemont (CFRUY) (CFRHF)) have declined materially over the past six months due to fears of a global recession, a pullback on consumer spending, and a weaker Chinese economy.

{kind=link}

This pullback drew our attention to the sector, and as value investors, we were quickly attracted to Compagnie Financière Richemont SA ("Richemont") in particular. Richemont is a hard-luxury powerhouse that owns iconic brands whose heritages are measured in centuries. These brands are nearly impossible to recreate today. People outside of the investment world may not be familiar with Richemont, but we suspect that most consumers know their brands: Cartier, Van Cleef & Arpels, and Vacheron Constantin, to name a few.

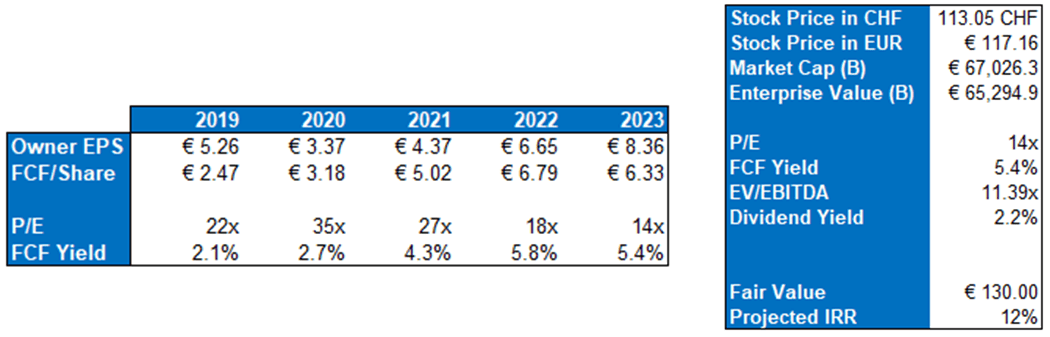

With the stock (CFR:SWX)(1) trading at CHF113, we believe that Richemont offers an appealing entry price, and we derive a fair value of CHF125 based on reasonable assumptions and expect a double-digit IRR on our investment over a five-year investment time horizon.

(1) Richemont reports its results in euros and the stock trades on the Six Swiss Stock Exchange (SWX:CFR). The company also has American Depository Receipts (ADRs) that trade over-the-counter in the United States ((CFRUY)).

Luxury Industry

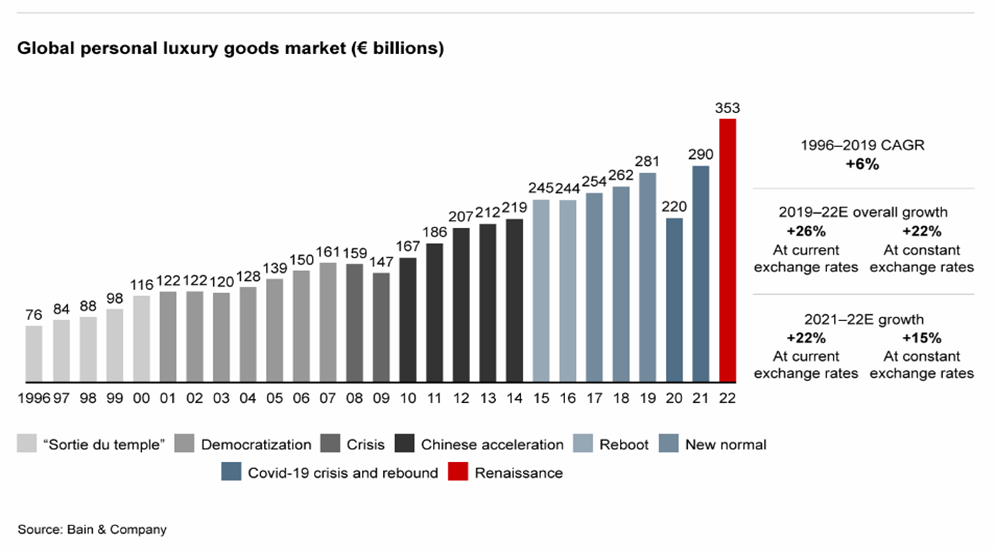

The luxury industry has benefitted from rising global wealth for decades and has remained resilient through various economic cycles. While there have been periods of slight contractions (2001 Dot-Com crash, 2008 GFC, 2020 Covid-19 epidemic), the luxury industry has always bounced back, often sharply driven by pent-up demand. We believe that this secular trend is set to continue.

{kind=link}

While the number of luxury consumers is expected to grow at a 2.7% CAGR as the world continues to get richer, very important customers (essentially, the top 1% of consumers) spend a disproportionate amount. As a result, the luxury market should continue to grow at a ~6% rate until at least 2030. Some of this growth will be driven by emerging markets like India and Southeast Asia due to their rapidly growing numbers of high-income consumers.

Despite different cultures having distinct values and traditions, throughout history, people have always had a desire to project their social status and wealth through jewelry. Scattered in museums worldwide today, you can find jewelry made from gold, silver, and gemstones from every region on the planet dating back thousands of years.

We believe this innate desire for hard-luxury items will remain unchanged, and Richemont will benefit as wealth continues to build worldwide, irrespective of which countries and regions grow the quickest.

Golden Necklace - circa 1400-1050 B.C

The Metropolitan Museum of Art

Company Overview

Richemont operates in three areas of the luxury market: Branded Jewelry, Specialist Watchmakers, and Fashion & Accessories:

{kind=link}

Luxury Jewelry

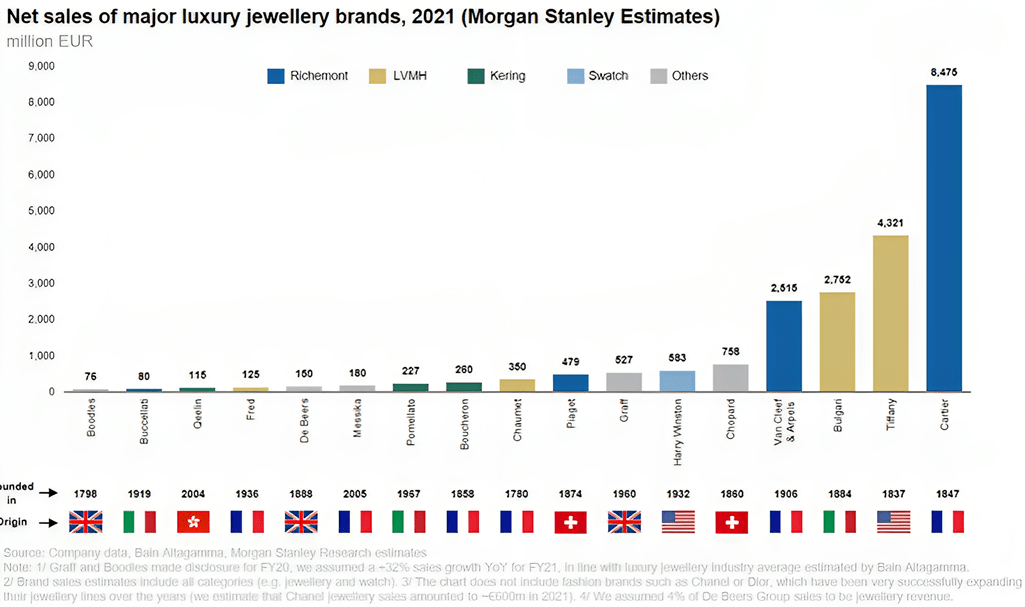

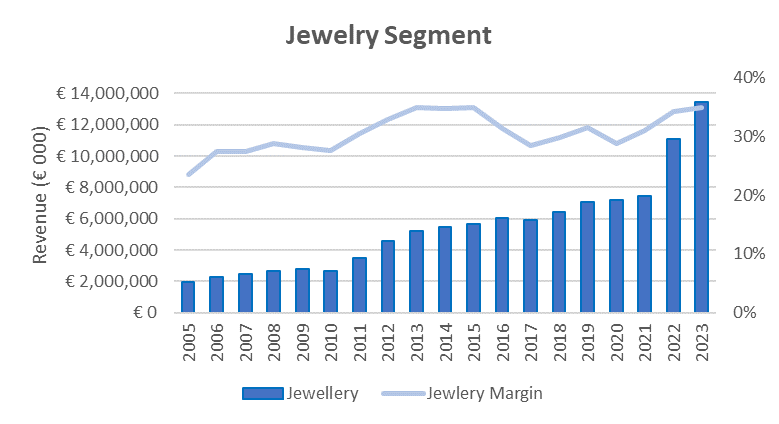

The Jewelry segment represents 67% of the company's sales and generates ~85% of its operating profits, making it the primary driver of the group's success. The segment is led by Cartier, which we believe is the largest and most valuable branded jewelry business in the world.

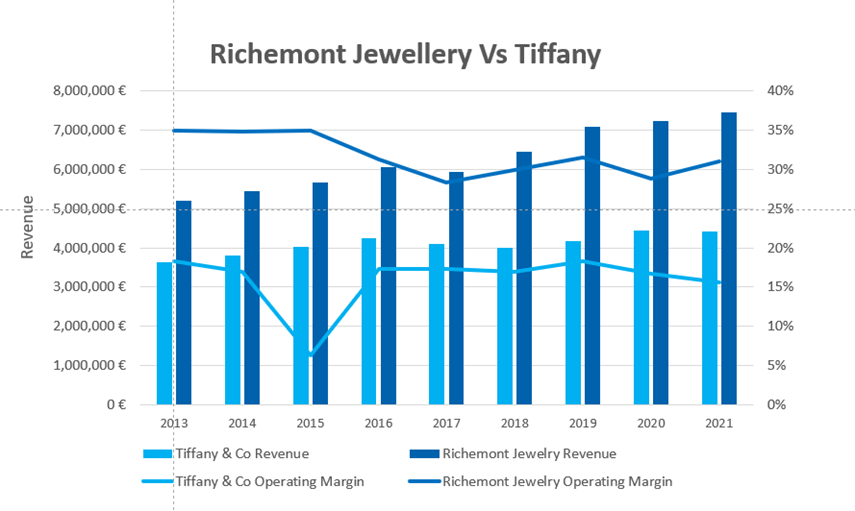

Cartier's iconic red box generates sales almost double that of the #2 competitor, Tiffany (owned by LVMH). In addition, Cartier delivers operating margins in the low 30% range (roughly 10-15% higher than Tiffany's historical average). Richemont's second-largest jewelry brand - Van Cleef & Arpels - is no laggard, producing sales comparable to LVMH's Bulgari to round out the top four spots on the global rankings.

{kind=link}

GreensKeeper & Company Reports

{kind=link}

Richemont's Jewelry segment has a decades-long track record of posting low double-digit growth throughout various economic cycles with remarkably consistent operating margins. Our analysis suggests that the bulk of this growth has been driven by Cartier's continuous strength, price increases and management's skill in building out smaller acquired brands.

CEO and Chairman Johann Rupert's family owns a 9.1% equity interest in the business and voting control via a dual-class share structure. He thinks and acts like an owner because he is one. When making acquisitions, Mr. Rupert has taken an unorthodox strategy to most luxury houses. For example, in 1999, Richemont paid €310m to acquire control of Van Cleef & Arpels from the founders' heirs (a business that was losing €60m a year at the time). It took time and patient long-term investment in the brand, but that business should generate over €1 billion of free cash flow ((FCF)) in 2023. Mr. Rupert believes that it is best to build - not buy - goodwill in the luxury space.

{kind=link}

While the luxury jewelry market has grown at a 7% CAGR from 2010-2022, the branded Jewelry market remains a small but faster-growing portion of the market. In 2019, branded jewelry represented ~18% of the total fine jewelry market. The remaining 82% of sales came from unbranded pieces often sold by local jewelers. As affluent consumers continue looking for ways to differentiate themselves and project their status, branded jewelry has increased its share. It is estimated that branded jewelry will continue to grow at 8-12% per annum and comprise 25-30% of the total market by 2025. As Cartier and Van Cleef & Arpels are synonymous with branded luxury jewelry, we expect Richemont to continue to benefit from this trend.

In addition to attractive volume trends in the jewelry business, Richemont possesses untapped pricing power. Like most luxury houses, Richemont has continually increased the price of its products over time. For example, a gold Chanel Love bracelet priced at €300 when introduced in the 1970s now fetches up to €7,000.

But despite its industry-leading position and considerable pricing power, Richemont has not instituted price increases as aggressively as its competitors. The rationale behind Richemont's strategy has been to protect and build their long-term equity with customers. To increase prices drastically when demand is high, only to lower prices following a subsequent slowdown in demand, alienates customers. The company recently admitted that it could double the price of many of its products and still sell out (products often resell at auctions for 2-3x the price of purchasing new). Instead, they take a measured approach to price increases (typically mid-single-digit) and are focused on building long-term trust with customers and keeping resale values high. This patient, long-term nurturing of its brands has allowed Cartier and Van Cleef & Arpels to blossom into the icons they are today.

The secular trends in the luxury Jewelry industry, combined with the timeless brands Richemont has built throughout its history, give us a high degree of confidence that investors willing to look past potentially soft short-term demand will be rewarded. Richemont's brands are poised to grow significantly faster than the economy over the foreseeable future.

We see limited fashion risk in Richemont's jewelry portfolio as many of their best-selling items, such as Cartier's Love bracelets and Van Cleef & Arpels' Alhambra collections, have remained popular since they were introduced many, many decades ago. These brands are timeless. And as Coco Channel herself so eloquently put it: "Style says, fashion goes."

Cartier

Specialty Watches

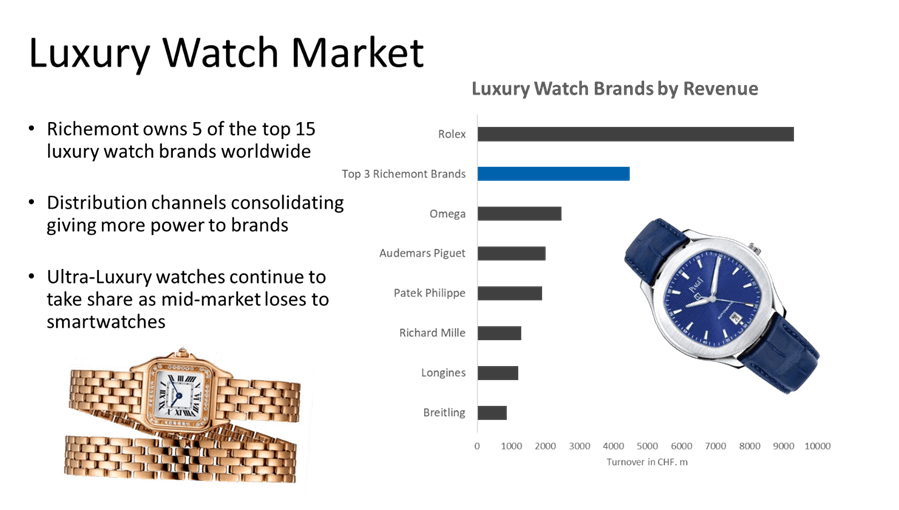

The Specialty Watches segment represents 20% of the company's revenues and generates 15% of its profits. Richemont owns a portfolio of seemingly timeless brands that command significant pricing power within the watch market. Perhaps the best example is Vacheron Constantin, the oldest watch manufacturer in continuous operation since it was founded over 265 years ago. Vacheron Constantin has survived multiple revolutions, pandemics, world wars, and recessions of every scale, all while maintaining its position as a top ten watchmaker across the globe today.

Morgan Stanley Swiss Watch Report & GreensKeeper

{kind=link}

Richemont's Specialty Watch segment has increased its sales at a 9% CAGR over the past 17 years but has experienced its fair share of volatility in operating margins. In 2015, the luxury watch market was flooded with inventory, leading Richemont to repurchase and destroy inventory from its distributors. While some media sources and shareholders criticized this action, we view it as a prudent long-term management decision to protect the longevity and health of its watch brands.

GreensKeeper, Company Reports

While this event plagued the segment's margins from 2016-2021, Richemont has learned from this episode and made several changes to avoid a repeat. In 2010, 54% of sales were made through wholesale partnerships, while only 46% of sales were sold directly through company-owned stores. Today, 74% of sales are generated from company-owned stores, giving Richemont increased control of its inventory in the market and a direct relationship with the consumer.

GreensKeeper, Company Reports

Richemont's remaining wholesale channel partners have also undergone a period of consolidation with leading companies such as Watches of Switzerland Group (WOSGF) (LSE:WSOG) gaining significant shares across Europe and North America. The Company's major distributors are incentivized to manage inventory shrewdly. Richemont grants wholesalers formal permission through selective distribution agreements to sell inventory on a store-by-store basis rather than allowing them to distribute across their entire business. Richemont has referred to this strategy as "fewer partners, more partnership." In a 2020 earnings call, CFO Burkhart Grund spoke to the issue:

We've managed to rebalance the relationship with our wholesale partners that the inventory that we sell into them is lean, is monitored and is really built and structured so that they can best serve their customers, which means our customers as well. And we have gone through considerable pain and considerable criticism for doing these buybacks…. It has to be accompanied going forward by a different way of running this business, with different management principles and KPIs. It's not for the sake of having a KPI, but it's for the sake of having a clean inventory position that will avoid, in the long run, brand equity impairment."

We believe that Richemont has learned its lesson, and these changes will lead to watch margins remaining in the high teens going forward.

Cartier

Fashion and Accessories

The Fashion and Accessories segment generates 13% of Richemont's revenues and a negligible amount of its profits as it often runs at a near-breakeven profit margin. The segment spans various product lines, including clothing, leather goods, footwear, and pens. While Richemont has struggled to gain much traction in this segment, they haven't invested much capital in it, with 80% of their capital expenditures going towards their Jewelry and Specialty Watches segments.

We view this segment as a collection of smaller, quality brands that management experiments with. Management remains hopeful that they will be able to drive higher profitability in this segment in the future. They have admitted that their leather segment has fallen behind as they dedicated most of their focus over the past decade to watches. However, they plan to shift some of their focus now that the Specialty Watch segment is in a stronger position. We have faith in management's execution abilities, given their track record, but don't assign any value to Richemont's Fashion and Accessories at this time. If they can turn one or two of their fashion brands into the next major Maison, it's a windfall from our perspective.

Valuation

We expect that the Jewelry and Specialty Watches segments will drive the bulk of the company's growth. We are comfortable that these segments can grow at least at the pace of the luxury market and believe that Jewelry will outperform as branded jewelry continues to take share. On the margin side, we believe Richemont can continue to hit its 30-35% Jewelry margin target, with the Specialty Watches segment preserving the high-teen margin levels of the past few years. While we acknowledge it is nearly impossible to predict the impact of a recession on near-term results with any precision, we believe that these medium-term growth and margin estimates are relatively conservative in light of the company's history, its latent pricing power, and the tailwinds driving the luxury industry.

{kind=link}

One of the benefits of a controlling family owning a meaningful stake is that the company is run conservatively and for the long term. Richemont has ample excess cash on the balance sheet and has consistently been operated with no net debt. Accordingly, the company can afford to invest in growing its smaller brands, such as Buccellati, while participating in M&A opportunistically. In addition, Richemont is a regular payer of dividends and has a history of paying special dividends to shareholders as cash builds up.

We derive our target price of CHF125 (€130) by applying a 20x EPS multiple to 2028 EPS of €8.69, a 40% dividend payout ratio, and a conservative discount rate of 10%. We would highlight that the company has historically traded at an average 21x earnings multiple. With the shares currently trading at CHF113, we derive a 12% IRR over that period. We believe these are reasonable assumptions for a company with a market-leading position in a growing industry with strong returns on capital.

Risks

Chinese Consumer Weakness

Over the past decade, an important driver of revenues for Richemont and the entire luxury market has been the growing cohort of wealthy Chinese consumers. Richemont's sales in the Greater China region rose from 11% of total revenues in 2005 to 25% of global revenues in 2023. While Richemont does not disclose sales by nationality, it is probable that sales from customers of Chinese nationality are greater than 25% of total revenues based on estimates of the broader luxury market itself.

{kind=link}

We believe an economic slowdown in China will have a greater effect on the entry-level luxury price range. In China, the top 2% of luxury customers accounted for 40% of the estimated total market spend in 2022. We believe the wealth effect has a larger impact on luxury consumers than an economic slowdown. Hence, the health of the equity and real estate markets is something that we monitor closely. However, past episodes of weaker demand have resulted in purchase deferment, not outright demand destruction.

Management Risk

Perhaps the most significant risk to any luxury company is mismanagement of its brands. More prevalent in the soft-luxury category, many brands have been impaired by management decisions such as over-saturation and alienating customers via risky advertisements, questionable brand extensions and oversupply. Richemont's management has shown themselves to be excellent stewards of their brands and we see little risk that they stray from the long-term focus that has gotten them where they are today. On a recent earnings call, Mr. Rupert discussed this topic:

Balenciaga would never ever have occurred at Richemont. And trust me, Bud Light would not have happened. It's not our role to be social adjudicators. We have colleagues, shareholders, commercial partners of all sexes, races, religious beliefs and as I said, I don't have a dog in that fight. We just want to stay true to the culture of Cartier, stay true to the culture for Van Cleef, Lange, all our products, and not get greedy. Don't pick low-hanging fruit, just grow within yourself and keep the brands' equity top of mind."

Mr. Rupert is 73 years old, and the company has an internal succession plan but has not named the next CEO other than to say that he/she will not be from the controlling family. Many of the company's top executives have been part of Richemont's Maisons for decades. Rupert's son Anton will remain on the board to preserve the culture and ensure that his colleagues will not have to wake up one day and find Richemont has a new owner with a short-term time horizon.

Other Risks

Richemont is subject to a wide variety of risks, including changing regulations, litigation, fraud, cybersecurity, and economic and geopolitical factors. Please review the company's latest Annual Report and other public filings for additional risk factors. Conduct your own research before making investment decisions.

Conclusion:

Despite the possibility of slowing demand and potentially even a global recession, we believe Richemont will remain the world leader in hard luxury for the foreseeable future. While we acknowledge that short-term profits may be affected if the economy softens, that possibility has been largely priced into the stock. Our bet is that Richemont's brands will continue to be desirable to luxury consumers, allowing Richemont to grow along with the world's rising number of wealthy individuals.

At a current price of CHF113, the stock trades at a forward P/E of 14x. We view Richemont as an attractive investment opportunity with a target price of CHF125 and expect an IRR of 12% over our five-year investment time horizon.

For further details see:

Richemont's Timeless Brands Offer An Attractive Investment Opportunity Following The Recent Sell-Off Across The Luxury Market