PPRUF - Richemont: The Luxury Holding Is Increasingly Earning Its Premium Due To Strong Results

2023-05-26 18:20:27 ET

Summary

- Richemont is the 2nd largest luxury holding in Europe with a focus on luxury jewelry and watches.

- After some years, Richemont found its way back on the growth track and also achieved new highs of profitability and cash conversion.

- Regarding the EV/FCF ratio and the comparison to its peers, Richemont could offer an interesting opportunity for long-term investors.

Richemont ( CFRHF ) is the 2nd largest luxury holding in Europe and is often being compared to LVMH ( LVMHF ) and Kering ( PPRUF ). Although Richemont shares are up more than 30% YTD, the company has underperformed its often-cited peers over the long term. In the recent years, however, Richemont significantly increase its profitability and cash conversion. Also, the transformation of the individual distribution strategies seems to be paying off. As the underlying trend of growing demand for luxury goods continues, Richemont could be a compelling long-term investment. For now, though, investors should keep Richemont on their watchlists and wait for setbacks, as luxury companies have rallied over the past year.

Business Model

Since 1988, the Rupert family has been continuously building its luxury portfolio under the holding company "Compagnie Financière Richemont SA" ( CFRHF ), which today consists of 27 businesses. Richemont is often compared to its European peers: LVMH ( LVMHF ) and Kering ( PPRUF ), although their product offering is quite different.

Business Segments of Richemont (Own Illustration)

{kind=link}

Jewellery Maisons

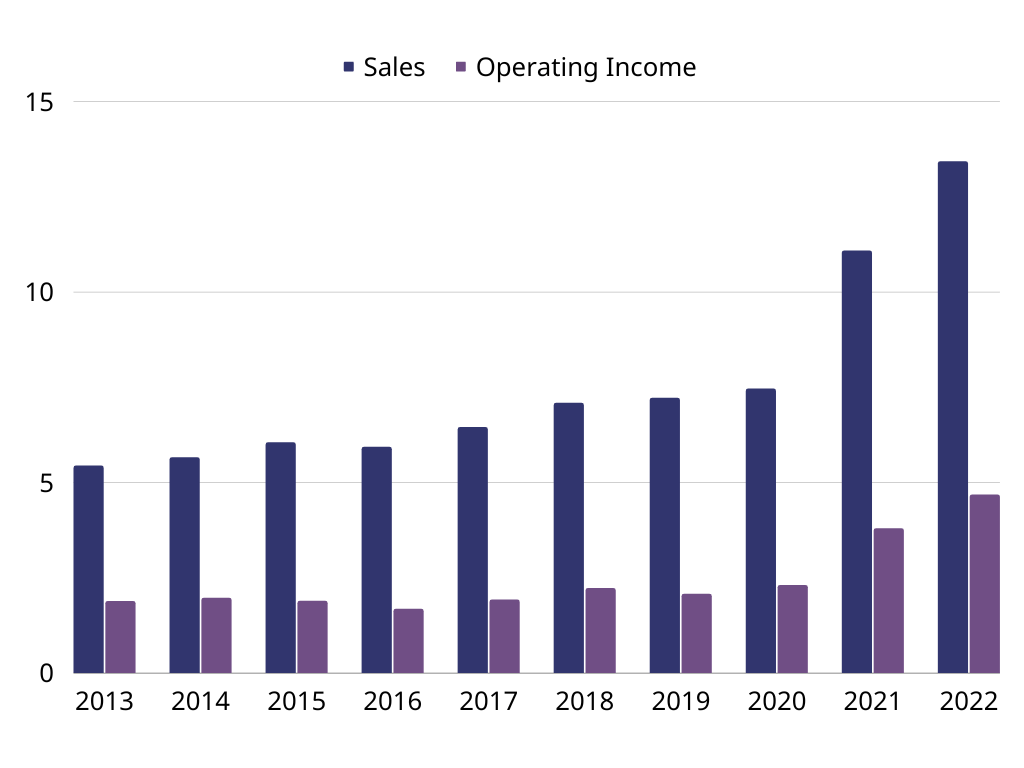

The most important business segment for Richemont combines its activities in luxury jewelry and accounts for about 70% of total sales. The main driver of this segment is mainly the iconic jeweler, Cartier, which was named as the 6th most valuable luxury brand in 2021. In addition, Van Cleef & Arpels and Buccellati are two other renowned jewelers who, together with Cartier, have contributed a total revenue of €13.4 billion, representing an increase of 21% compared to the previous year.

Jewellery Maisons, 2013-2022, in € billion (annual filings)

{kind=link}

Similar to the famous T-Bracelet or the Heart-Tag chain from Tiffany & Co, Cartier was able to reach an iconic status with several products, e.g. the Tank watch collection or the Love bracelet, leading to continuous demand and low price sensitivity. In its latest earnings call , CFO Burkhart Grund commented the current environment for the Jewellery Maisons as follows:

Our Maisons are increasing their manufacturing capacity, in order to support the strong demand they are experiencing, with the opening of a new manufacturing site in Italy for Cartier and the expansion of 2 ateliers in Italy for Buccellati. Van Cleef & Arpels is currently investing in a new manufacturing facility in Lyon, with additional manufacturing sites to be added over the coming years.

In addition to that, the brands also showed their ability to raise prices in order to offset the inflation of raw material prices. Because, unlike Louis Vuitton or Gucci, luxury jewelers are dependent on precious metals, diamonds and such more, which also faced incremental price increases. Therefore it's impressive that this segment ended 2022 with an operating margin of about 35%, underlining operative strength and high pricing power.

However, when asked by analysts about the pricing of Cartier and Van Clef & Arpels, Johann Rupert commented as follows:

I will answer that one, which is they didn't increase prices by as much as I wanted them to [...]. They felt that one has to look over the medium to long term; and that we shouldn't be using shortages, et cetera to raise prices. So we have generally not increased prices as much as our competitors. And Cartier, for instance, only took an increase in April, so don't look at Cartier and think price increases.

From my perspective, this highlighted an important aspect of luxury goods, which is the sustainable increase of brand equity. This is an advantage over competitors who, by constantly introducing new products and trends, make pricing incomprehensible to the customer. By focusing on long-term customer relationships, this segment is expected to maintain its role as a growth driver for Richemont.

Specialist Watchmakers

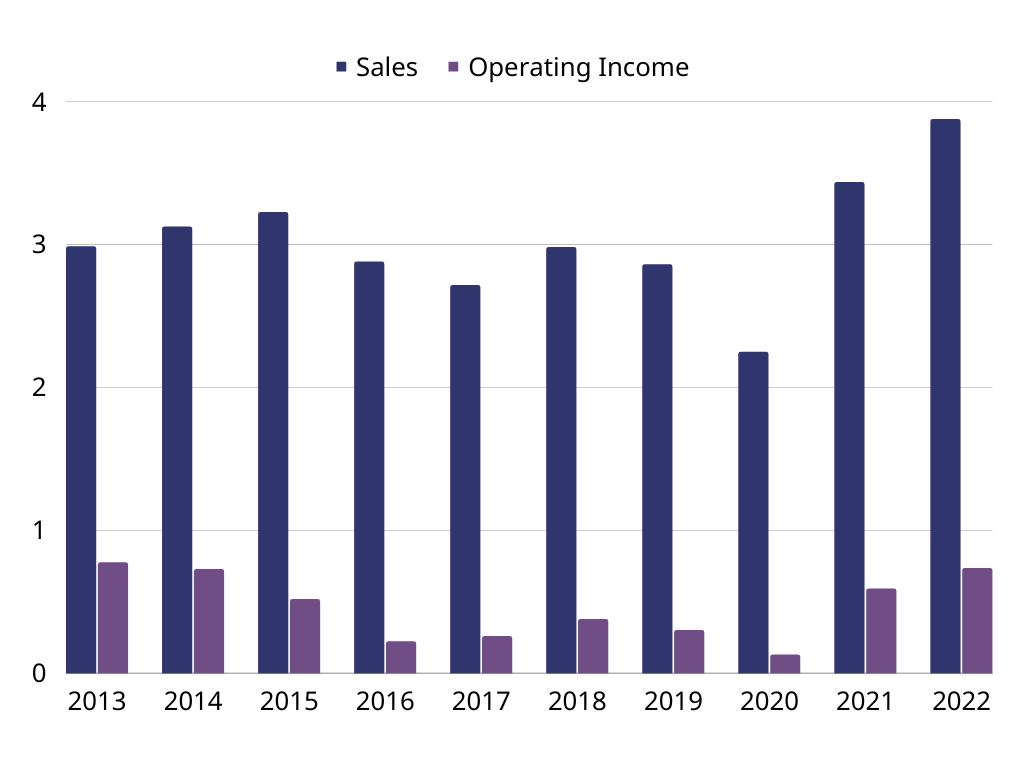

Moving on to the second business pillar, Specialist Watchmakers, which accumulates about 20% of total revenues. The emergence of this segment is essentially based on the acquisition of LMH-Holding ( Les Manufactures Horlogères ) in 2000, which included Swiss watchmakers like Jaeger-Lecoultre, IWC and A. Lange & Söhne. Next to Rolex, Patek Philippe and Audemar Piguet, Richemont owns some of the most popular and valuable watch brands in the world. Due to the high level of craftsmanship, operating margins are generally lower than fashion or jewelry, but the management was still able to increase the margins over the last years, resulting in 19% for the previous year.

Specialist Watchmakers, 2013-2022, in € billion (annual filings)

{kind=link}

This is partly possible, because of enhancing demand for luxury watches, leading to an increase in sales of 13% YoY, but also due to a transformation in the overall distribution strategy. The goal is to increase the direct-to-client business, while lowering the wholesale distribution, in order to improve the client experience. This is a development, we can see in many luxury businesses at the moment, but from my perspective, this is particularly reasonable for watch brands to compete with the brands on the upper end of luxury. In addition to that, this improves the companies ability to manipulate and monitor the customers experience and demand, which makes it also easier to identify trends.

Historical sales in this segment, however, show low growth rates of just 2.9% per year, as the hype around luxury watches is relatively young. The coming years will have to show whether the recent growth is a one-time effect or a long-term trend. Nevertheless, Richemont has several gems in its portfolio of watchmakers, each with its own heritage and iconic products that have the potential to be expanded in the future.

Other & Held for Sale

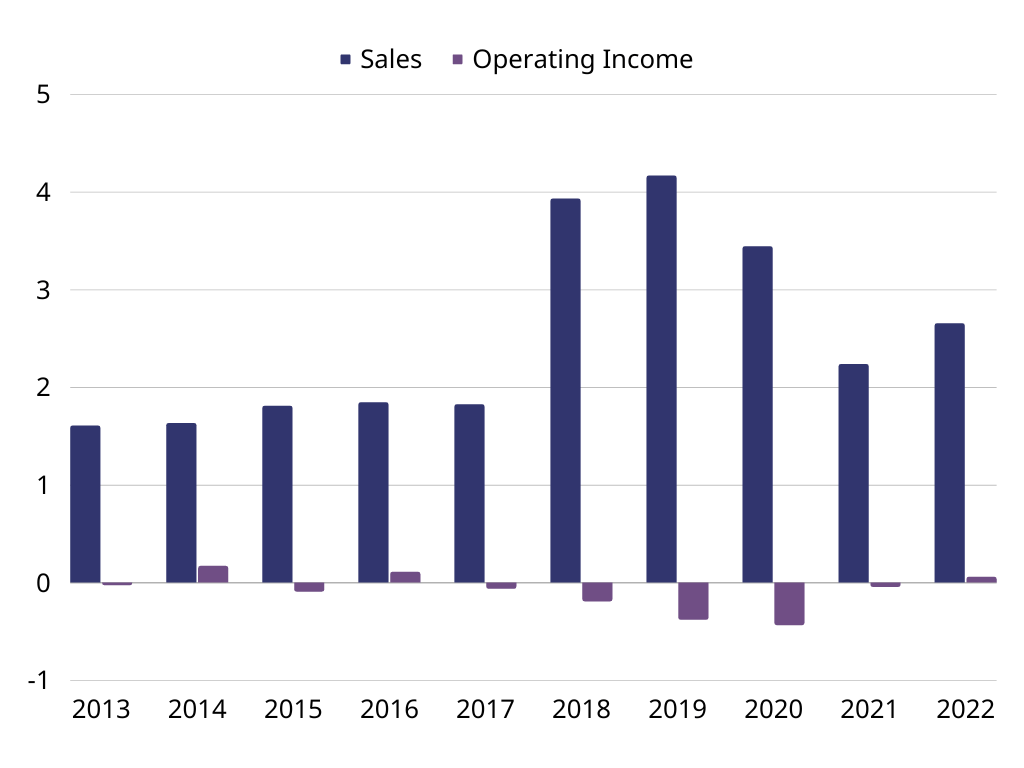

After having discussed the most important business segments of Richemont, we're coming to the remaining activities, which are being summarised as "Other" and contribute about 10% to the total sales. Looking back at the illustration above, the most recognisable brands include Mont Blanc, Chloé and Dunhill, which are mostly relatively early acquisitions of Richemont. In addition to that, Richemont included their e-commerce activities with YNAP and Watchfinder under this segment as well.

Other, 2013-2022, in € billion (annual filings)

{kind=link}

In August 2022, Richemont announced a transaction involving the sale of a majority stake in YNAP to Farfetch ( FTCH ) and Alabbar. Therefore, all related assets are now "held for sale" and the segment's revenues decrease.

While this segment never reached sustaining profitability, its not surprising that the deal delighted investors and it will be interesting to monitor, what Richemont can make out of the remaining activities.

Thoughts on the Businesses

Contrary to what one would expect from Richemont, the portfolio includes several first class assets, led by Cartier. Nevertheless, there has been no steady growth in the individual segments in the past, which explains the different share price developments. Now that the underlying market trend is stronger than ever, Richemont is also showing operational growth again. Moreover, the company seems to have recognized the trends and to have positioned the brands well for the future.

However, when compared to the other two European luxury houses, it is already apparent that its own brands are more difficult to expand and scale than fashion brands like Gucci or Louis Vuitton. The reason for this is the high level of craftsmanship and the more expensive raw materials.

That said, I think it's very interesting to take a look at how profitably Richemont can reinvest its money in the business.

Capital Allocation

Generally, a company has four ways of using its free cash flow, apart from filling the bank account:

- Reinvesting into the business

- Acquiring other businesses

- Repurchasing own shares

- Paying a dividend

In the following, I will focus on re-investments and acquisitions to see if Richemont has a competitive advantage over other luxury holdings.

Reinvesting into the Business

As already mentioned, Richemont focusses on enhancing its direct-to-client business by opening new flagship stores and upgrading existing ones. In 2022, directly operated stores contributed 68% to the total sales, especially driven by the Jewellery Maisons and new stores in Asia Pacific. The management seems to be confident about future prospects of the business and furthermore, sees opportunities to reinvest its capital.

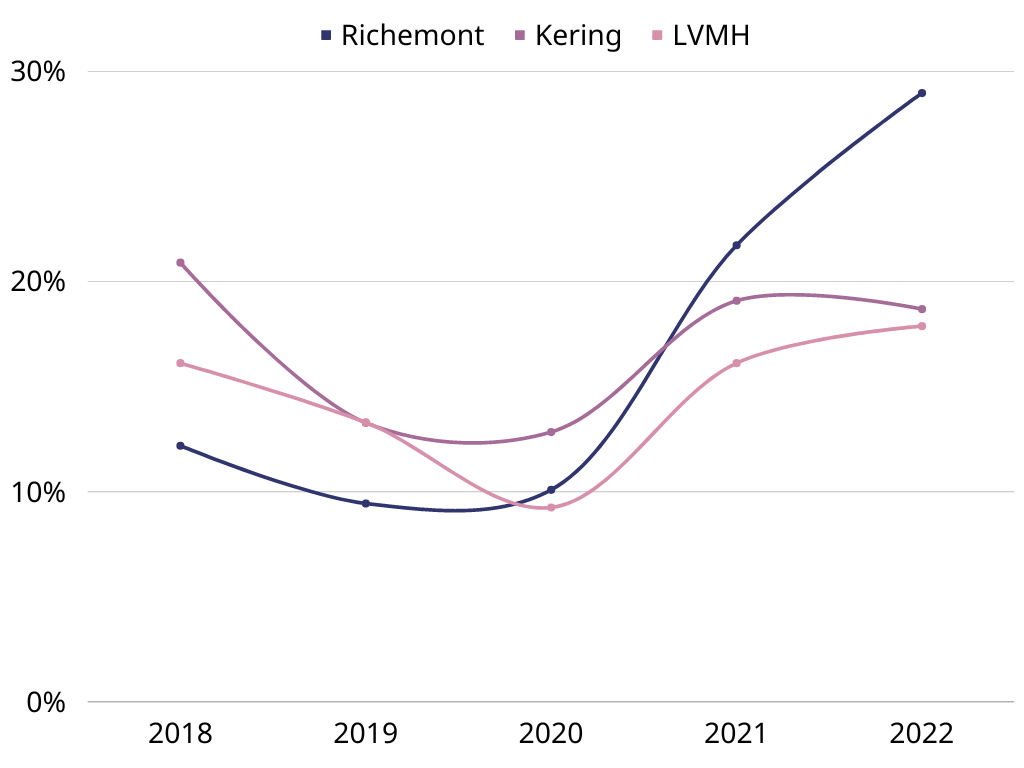

Overall, Richemont currently achieved a return on invested capital of 29% in 2022, representing a new high and the result of booming demand, which we already recognised above.

Unfortunately, investors should expect that these returns on capital will not be rolled over, as demand will normalise again.

ROIC by company, 2018-2022, in % (own calc.)

{kind=link}

However, I expect the underlying trend to maintain, because of the more profitable distribution strategy and lasting price increases. Richemont is likely to narrow the historical gap to its peers, although the gross of the businesses have a higher capital intensity, which should be kept in mind.

M&A

As Richemont is a holding of luxury businesses, it seems natural to assume that future growth will also derive from non-organic growth, besides the organic growth of already owned businesses. But, due to the fact that it takes several generations to build brands close to Cartier and others, there are less and less acquisition targets left.

YNAP

One idea of Richemont was to diversify their portfolio by adding e-commerce platforms that sell personal luxury goods. Therefore, Richemont spend about €5 billion in 2018, acquiring the YOOX NET-A-PORTER GROUP (YNAP), which is the company behind online luxury retailers "MR PORTER" and "NET A PORTER". As already mentioned above, while speaking of Richemont's "Other" businesses, the platform of luxury marketplaces was sold to the popular peer, Farfetch ( FTCH ), in 2021. According to Reuters and Vogue , the deal was mostly equity-based with Richemont, receiving about 50 million shares of Farfetch and €250 million in cash over the following 5 years.

Although, this was obviously a bad investment by Richemont, the company will still be able to benefit as almost all houses joined the Farfetch marketplace. In addition to that, Richemont is rid of the loss-making businesses through a final write-down of €2.7 billion and can therefore be more focused on the core business.

Future Expectations

Besides this recent transaction, Richemont was relatively cautious with M&A deals throughout the last years and focussed more on the operating strengthening of its core businesses, which was very successful so far, regarding the record margins and return on investment.

Now that the company build up a solid business with a rising cash position, it's relatable to me, why an analyst requested the probabilities of a new M&A deal in the latest earnings call . Johann Rupert directly responded as follows:

I tend to find in my past that the companies that are easy to buy, the companies that you buy, normally, there's a reason why they're very easy to buy. And you always underestimate the difficulty of fixing it, and the most difficult thing is inevitably the culture. That takes a lot longer that anything else. We have been more successful in buying even smaller companies with great culture, and then empowering them. If there's a financial meltdown, yes, maybe we'll look at bigger companies that are not performing because of exogenous factors, external factors. And yes, then we look. But at this stage, the terrible thing is the companies that are really nice are not for sale, okay? And that's across the board.

I personally like his comprehensive answer to this question, because it underlines the fact that acquiring and especially successfully integrating a new business into the existing organisational structures is a challenge and should be entered thoughtfully. Generally, Johann Rupert demonstrated in multiple instances that he intends to set Richemont up for long-term growth, instead of short-term profits, which is the advantage of owner-operated companies (although he has since stepped down from the position of CEO).

In addition to that, Rupert confirmed the assumption that it is becoming increasingly difficult to find companies that are already high quality and up for sale. Therefore, investors shouldn't expect the company to enter any larger acquisiton in the future. However, the strengthed balance sheet will equip Richemont with the ability to be opportunistic, once the market valuations deteriorate.

Final Thoughts on a Competitive Advantage

Regarding our starting point, namely the discussion of Richemont's competetive advantage through capital allocation, I would argue that Richemont succesfully set their core businesses up for future growth by reinvesting into the new distribution strategy and further increasing the awereness of its brands iconic offerings. In any case, this has enabled Richemont to close the gap with its peers in terms of capital allocation, resulting in the following final comparison:

| Revenues (in € million) |

| Gross Margin |

| EBIT Margin |

| Revenue CAGR (5 Years) |

| Revenue CAGR (2023-2025) |

| Richemont ( CFRHF ) |

| 19,953 |

| 68.74% |

| 25.21% |

| 12.62% |

| 8.76% |

| Kering ( PPRUF ) |

| 20,351 |

| 74.68% |

| 26.51% |

| 13.48% |

| 7.19% |

| LVMH ( LVMHF ) |

| 79,184 |

| 68.44% |

| 26.52% |

| 13.18% |

| 9.31% |

The table points out what we already assumed, namely the similiarity of all three businesses in terms of the key financial metrics. And it also stands out that analysts are expecting higher growth rates for Richemont in the coming years than for Kering, which I will recognize in the coming valuation.

But first, I would like to squeeze in a cash flow analysis that will be used for the valuation as well.

Cash Flows

In order to analyse a company's ability to generate cash from operations, I focus primarily on its free cash flow. Despite the usual calculation (OCF - CapEx = FCF), I adjust the operating cash flow for changes in net working capital and the expenses for stock-based compensation and off-balance sheet financing.

Using this approach, I try to get closer to the actual and sustainable cash generation of the business through the perspective of its owners.

For Richemont, the calculation (based on TTM) looks like this:

| in € million |

| Operating Cash Flow |

| 4,491 |

| - Stock-based Compensation |

| 94 |

| - Change in NWC |

| -1,167 |

| - Lease Liabilities |

| 688 |

| = Adjusted Operating Cash Flow |

| 4,876 |

| - Net CapEx |

| 962 |

| = Free Cash Flow |

| 3,914 |

A closer look at the adjustments above reveals that the usual free cash flow would be significantly lower due to increases of working capital. In its latest earnings call , the CFO of Richemont, Burkhart Grund, commented the cash flow development as follows:

Cash flow generated from operating [...] was robust at €4.5 billion, reflecting a strong operating profit from continuing operations offset by increased working capital requirements mainly due to higher inventories to support sales growth and our further retailization of the group's businesses.

As these effects will probably be compensated in the near future, it seems reasonable to adjust them now, in order to receive a sustainable cash flow.

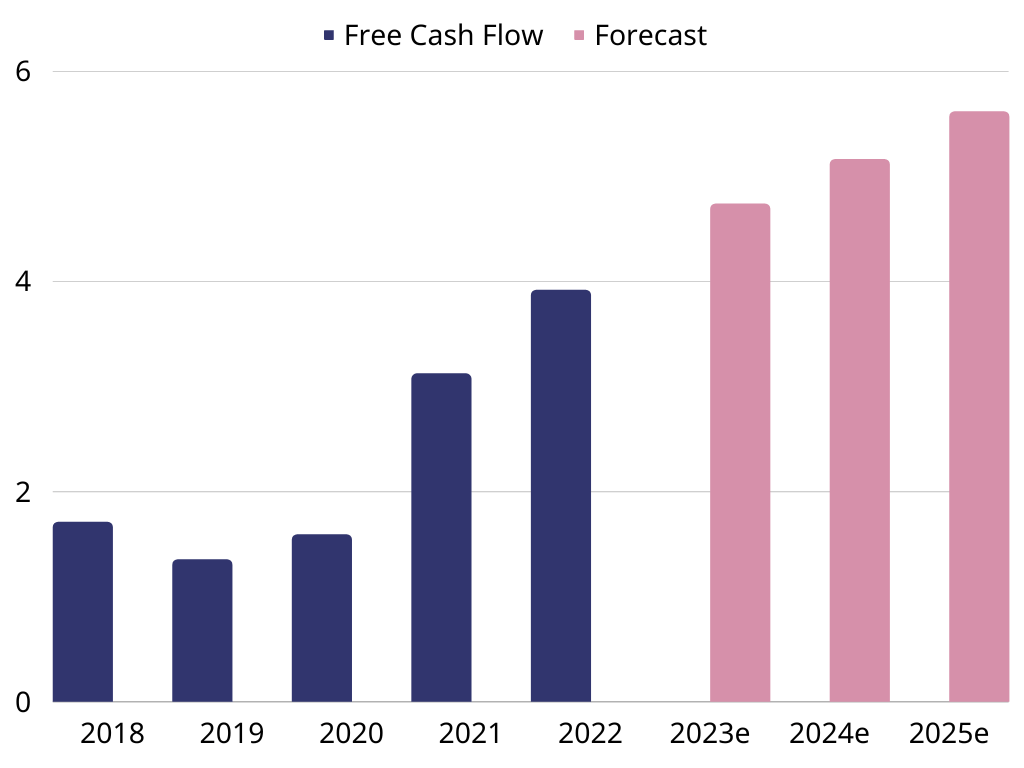

If we apply this to the last 5 years, we obtain a CAGR of 23% and an increasing FCF margin of previously 19.62%, demonstrating that Richemont became more profitable and cash-generating.

Free Cash Flow, 2018-2025e, in € billion (own illustration)

{kind=link}

To estimate future cash flows of the company, I used the average cash-conversion of 68% and the analysts estimates on EBITDA for 2023 to 2025. The result is even higher than the revenue estimates stated earlier, which indicates that analysts are expecting increasing operating margins. In general, investors should avoid projecting the historical growth rates and margins directly into the future, as the reopening-induced growth rates aren't likely to maintain. However, if Richemont remains their level of profitability and cash-conversion, it will probably do fine in the coming years and will also be able to benefit from possible opportunities and market trends.

Headwinds and Risks

Having said that, I would like to briefly outline current headwinds and risks that could impact my views on future cash flows.

China as a Cluster Risk

As those of you who are already invested in luxury businesses know, China, and in particular its reopening after the pandemic, is a key performance indicator for the coming years. Richemont's revenues are currently 40% dependent on the Asia-Pacific region, with China being the most important part. While Richemont has seen significant growth in most Asian regions, China has offset this growth, resulting in overall Asia Pacific sales growth of only 1% at constant exchange rates. Therefore, it seems reasonable to identify China as a potential constraint to future growth.

In its latest earnings call, Johann Rupert commented the current customer sentiment in China as follows:

We said that China will take longer to open, which was contrary to the popular belief, well, simply because we had more information and, I would say, better sources. [...] The Chinese saved an enormous amount of money during that period, but it was a traumatic experience. It was a total lockdown. And their first expenditure was just human going out for diving, traveling, so it was more spent on services. [...] Now we know, in terms of traveling, because of the prebooking and the airlines and the hotels, that we shouldn't expect a lot of Chinese tourists to come in groups to Europe before the end of summer. That's just data-driven.

I really liked the insight that Richemont seems to be very well networked in China, which allows this comprehensive review of the customer sentiment. As an investor and a potential shareholder of the company, this gives me a good feeling about China's dependence. In addition, Richemont has continued to expand its portfolio of DTC appearances in China and Asia in general, underlining its long-term expectations for these regions. The company could start to benefit from the ongoing reopening in the second half of this year, which is also the result of Bain & Company in their latest industry report .

In conclusion, I would classify China as an obstacle in the short term, but rather as an opportunity in the long term, from which Richemont and its shareholders could benefit.

Economic Downturn

Sales in China are not the only challenge. In Europe and North America, which account for 44% of total sales, recession fears and inflation rates remain high, leading to a cautious customer sentiment. But the luxury industry is better prepared for an economic down than in 2008/09, according to the industry report of Bain & Company . Therefore, the customer base of personal luxury goods is both larger and more concentrated on top customers, who are less sensitive to downturns. In addition, the industry experts are mentioning:

The customer centricity honed in recent years is another source of resilience for the industry, as is the multi-touchpoint ecosystem that luxury has developed.

Richemont's customer base, because of its high-end jewelry and watch offerings, is definitely based on both of these characteristics. In a recession, it's probably one of the best customer bases you can have, because it's mainly made up of the people who are least affected by a downturn. So I would say that the corresponding risk for Richemont is rather low.

Valuation

In order to value Richemont, I'll use the free cash flow, as calculated above, in relation to the total enterprise value. My assumption for this approach is that I probably won't be able to calculate a comprehensive DCF model as accurately as Wall Street, therefore I'm following Warren Buffett's approach :

It's far better to buy a wonderful company at a fair price than a fair company at a wonderful price.

So let's see, what CFRHF has to offer for us at the moment:

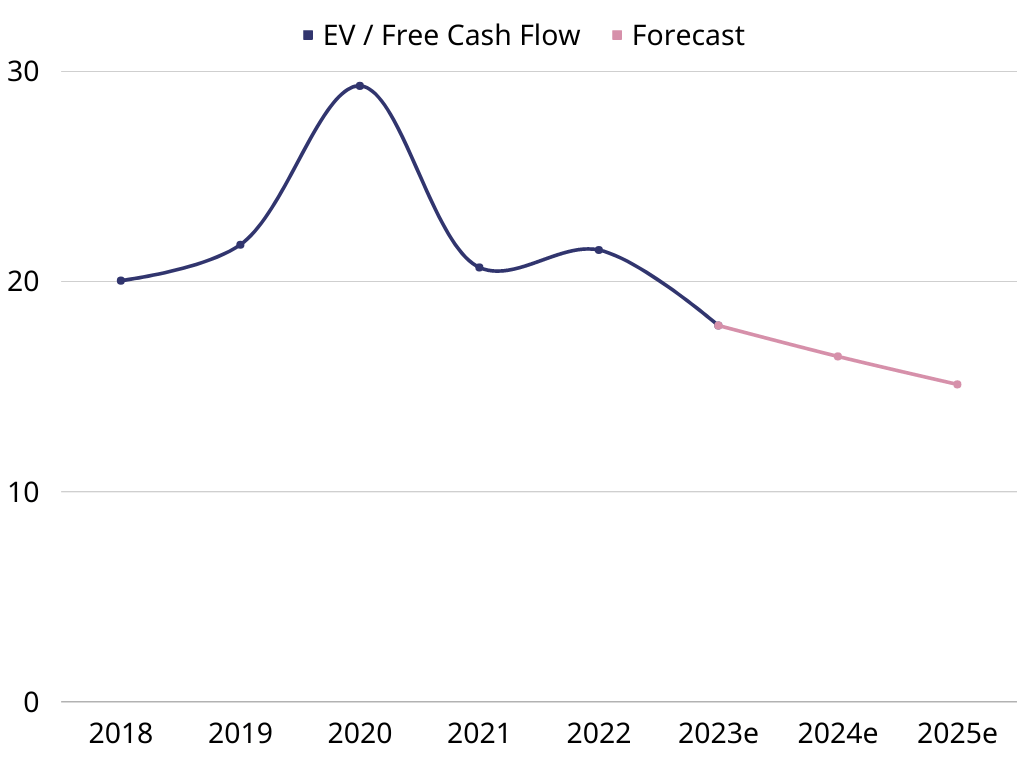

EV/FCF Ratios, 2018-2025e (own illustration)

{kind=link}

After Richemont rallied over the last year, the share price settled at about €149.22 (or $160), resulting in a current market cap and enterprise value of €86.06 billion and €83.46 billion, respectively. Therefore, using the calculated free cash flow of €3,914 million, investors are currently able to start a position at about 21.32x FCF. Interesting to see is that the multiple of Richemont stays relatively steady around the average of 22, although the share price nearly doubled from pre-pandemic levels. Therefore, the stock only followed the operating results of the business and maybe put a bit more optimism on top.

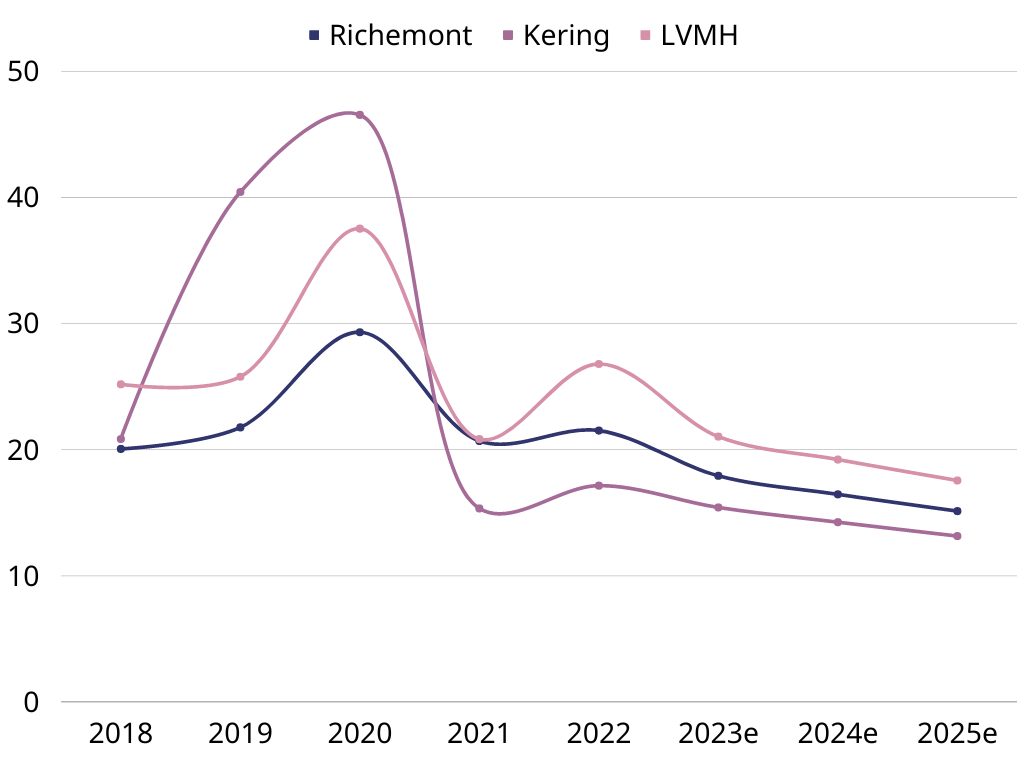

EV/FCF Ratios by Company, 2018-2025e (own illustration)

{kind=link}

Comparing this result to the peers of Richemont, we receive the result that the current valuation lies right in between Kering (17.14x FCF) and LVMH (26.79x FCF). The reason for this gap is probably the degree of diversification and future prospects of these companies, with Kering being the most concentrated and LVMH the most diversified. Richemont clearly narrowed this gap due to an improved operating model and increased focus on iconic products with higher margins.

In the coming years, Richemont should especially benefit from the faster growing jewelry segment and the reinforcement of the Chinese customer base, which we can also see being reflected in the forward multiples above. As for 2023 (or FY24), Richemont is trading at about 18x FCF, which looks pretty attractive to me for a quality company like Richemont, if they manage to meet my assumptions on appropriate cash flow conversion.

Conclusion

In conclusion, Richemont is one of the largest luxury holdings in Europe with an excellent portfolio of promising brands. Each of them has a unique and iconic heritage, which will continue to drive sales as demand for luxury jewelry and watches remains strong. In addition, the management has achieved new highs in profitability and demonstrated its long-term perspective on the business. As a result, Richemont should be able to overcome current challenges and be perfectly positioned for future growth.

However, as these levels of profitability and growth have only been in place for a relatively short period of time, Richemont does not yet enjoy the same high quality premium on valuation as LVMH ( LVMHF ).

In my view, Richemont has been under the radar of investors for a long time, but has now returned to the big stage as luxury jewelry and watches are in high demand. The recent rise in Richemont's share price confirms this and reflects the hype surrounding luxury companies.

Therefore, I would argue that investors who are interested in luxury companies should definitely put Richemont on their watchlist and can start building a position on setbacks.

For further details see:

Richemont: The Luxury Holding Is Increasingly Earning Its Premium Due To Strong Results