PAR - Richie Capital Group Q4 2022 Letter To Investors

Summary

- Richie Capital Group invests on behalf of clients using an established investment process leveraging decades of investment experience. Our investment goal is to provide superior returns over time through the active management of long-only investment strategies.

- When investors begin to move outside of their native risk habitats, strange things start to happen.

- Our outlook for equities remains positive.

| Portfolio Returns [1] |

| Q1 2022 |

| Q2 2022 |

| Q3 2022 |

| Q4 2022 |

| FY 2022 |

| FY 2021 |

| FY2020 |

| RCG Select Alpha [2] |

| (8.4%) |

| (14.0%) |

| (3.2%) |

| +9.6% |

| (16.4%) |

| +2.5% |

| +40.3% |

| RCG Long Short |

| (8.2%) |

| (1.9%) |

| +0.4% |

| +13.5% |

| +2.5% |

| (14.3%) |

| +10.0% |

| RCG Top 10 |

| (6.9%) |

| (14.0%) |

| (5.4%) |

| +7.3% |

| (18.8%) |

| +18.6% |

| +16.4% |

| Benchmark Returns |

| Russell 2500 Index |

| (5.8%) |

| (17.0%) |

| (2.8%) |

| +7.4% |

| (18.4%) |

| +18.2% |

| +20.0% |

| Equity Long/Short Index [3] |

| (0.9%) |

| (2.6%) |

| +0.3% |

| +3.2% |

| (0.03%) |

| +10.7% |

| +9.4% |

| S&P 500 (large cap) |

| (5.0%) |

| (16.4%) |

| (5.0%) |

| +7.4% |

| (19.0%) |

| +28.7% |

| +18.4% |

Dear Partner,

Since the Global Financial Crisis, we have operated in an environment where money has been “cheap”. When the Federal Reserve lowered the funds rate to a range of 0 to 0.25% during the heart of the pandemic, some might have even described money as “free”. Established companies could raise debt at historically low rates for any number of projects. Young startups could access venture capital to fund their operations as they searched for a path to profitability. And private equity firms had capital to lever up their portfolio companies to boost returns and de-risk their investments. Lower interest rates and over $14T in fiscal and monetary stimulus [4] worked together to stimulate the economy. With interest rates approaching near zero, governments, businesses, and consumers had ready access to money whenever they needed.

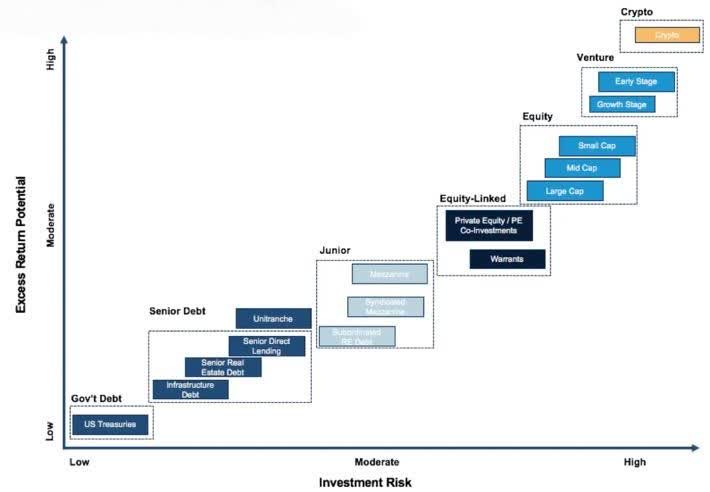

“Money” can be broadly defined as “a commodity accepted by general consent as a medium of economic exchange”. People use money to purchase value or they use money to create more money also referred to as “return” or “yield”. Where that money gets invested is based on the individual investor’s appetite for risk along their investment “risk curve”. The further out on the risk curve the investor ventures, the higher the potential, and expected, return. Most investors have a point on this curve where they feel most comfortable, a native habitat. This is the place where that investor feels that the level of reward they are seeking can be achieved at the level of risk they are comfortable with.

Example Risk Curve [5]

{kind=link}

U.S. Government debt in the form of 3-Month Treasuries is often considered “risk free”. The return an investor will receive is relatively low, but an investor can assume that the U.S. Government is unlikely to default on its debt within the next 3 months. This is the left side (starting point) of an investor’s risk curve. If an investor desires a higher return and is willing to take on more risk, they move up the curve in search of more return. From 3-month US Treasuries, an investor can take a short step to longer maturity government bonds which are riskier because there is more time for the government to default. And the options continue: corporate debt (public company bonds), public equities, hedge funds, private equity, and out to venture capital, real estate, and eventually more obscure moonshot opportunities in crypto and other ventures. The options along the risk curve are endless.

With interest rates as low as they were for so long, investors were no longer receiving their expected rate of return at their given risk appetite. And so, they were forced to move up the risk curve to achieve their desired return. Investors accustomed to receiving 3% interest on 10-year treasury notes had to move to corporate debt to achieve a 3% yield. Corporate debt investors had to “reach for yield” within lower sub tranches of debt and so on and so on. When investors begin to move outside of their native risk habitats, strange things start to happen. The investment landscape becomes unbalanced, and investors seemingly begin to behave against their own interests. Money begins to chase fewer and fewer opportunities, and investors become willing to accept lower returns for their money by paying higher valuations (on earnings or revenue multiples). Investors quickly forget that they are stretched further up the risk curve when other investors pile in after them boosting the returns of those who reached first. As investors observe others making loads of money, FOMO leads investors to ignore their typical due diligence standards and invest in companies that have no Board of Directors, no audited financials, and are incorporated in the Bahamas. “He’s an innovator.” “He attended MIT.”What could go wrong ?

From this behavior, we get meme stocks, moneycreated out of thin air, and venture like investments going publicwhen they have no business being publicly traded. During times of euphoria, frauds and scams proliferate . An investor’s vision gets blurry when it’s raining money, and it becomes challenging to differentiate real investment opportunities from deals that are truly “too good to be true”.

In a cycle as old as the market itself, these are all the standard signs of a market bubble. This is nothing new. Free money changes behavior and drives people further and further up the risk curve searching for returns. But free money is unsustainable. And during our recent cycle, the free flow of capital led to rampant inflation. The Federal Reserve’s response to inflation is what has finally broken the current cycle.

In our last letter , we discussed how the Federal Reserve is aggressively raising interest rates and unloading their balance sheet to beat back inflation. The free money is now drying up. And as the tide flows out, investors realize just how much risk they were taking in their search for returns.

“You don't find out who's been swimming naked until the tide goes out”

– Warren Buffett

As money dries up, frauds are uncovered, and investors flee to safety. As investors observe other investors getting burned, they remember the habits required to make good investments. I’m not sure what the opposite of FOMO is, but that is how investors behave, thereby pulling even more money out of the market, frequently in excess to the downside. Investors become more judicious in where they will invest their funds, and businesses with flawed business models atrophy and die as it becomes harder to raise fresh capital.

As interest rates rise, investors are now migrating back down the risk curve. Investors who had moved on from investing in risk free treasuries realize that 3-month treasuries are currently yielding 4.3% which is an attractive yield for them. And so, they move back downstream to their native habitat. And because all investors can now receive 4.3% interest on their money virtually “risk free”, the standards for additional risk are raised. To take risks up the risk curve, investors must be confident that they can receive a reward that is worth the additional risk. Meaning not just a higher return, but also a likelihood that such return will be realized. Sober decisions are made. Valuations for investments across the investment universe come down because investors demand a higher return.

That is where we find ourselves now. Markets have fallen over the past year, and we seem to be back to a more rational environment. Corporate management teams are becoming more disciplined as they cut costs and headcount to prepare for whatever market environment lies ahead.

What does this mean for our investments in equities? We believe that we are now entering a “stock picker’s market” where good investors have the opportunity to separate themselves. We may not see much movement in the indexes: high quality companies will shine, however, the indexes will continue to be burdened by underperforming “zombie” companieswith limited access to capital. Our expectation is that volatility will continue to be driven by market concerns around a recession and how deep it will be. Corporate earnings will be a key focus for investors in 2023.

There are reasons to be optimistic as there are numerous indicators pointing to a recession that will be mild: jobs continue to outpace workers available, businesses have built up solid cash cushions, the expected rise in unemployment could be modest, and household finances still have less debt and more savings built up from the pandemic.

There aremany studieshighlighting reasons to remain bullish for stocks in light of the current market environment. In previous inflationary periods, corporate earnings growth remained robust and the S&P 500 supported mid-teens earnings multiples when sustained inflation was kept below 6%. And in general, earnings growth remained strong in all but the highest inflationary periods. Finally, the valuation decline in 2022 should provide a buffer from future steep market declines.

Our outlook for equities remains positive. Welcome to the end of free money!

Selected portfolio discussion:

For the 4th quarter of 2022, the RCG Select Alpha strategy gained 9% and the RCG Long Short strategy gained 13% while their respective benchmarks the Russell 2500 Index gained 7% and the Equity Long Short Index gained 3%. For the full year, the RCG Select Alpha strategy declined 16% while the Long Short strategy gained 3% compared to declines of 18% and 0% for their respective benchmarks.

Our biggest contributors for the quarter:

Fair Isaac Corporation ( FICO up 45.3%) – The analytic software and data decision technology company continued to fire on all cylinders. FICO reported earnings growth across all metrics and raised guidance. The company is growing revenue faster than expenses, and their capital allocation strategy is focused on reducing share count to such an extent that EPS growth exceeds income growth. Additionally, in light of the slowing real estate market, the company has limited mortgage exposure. Mortgage origination accounts for only 11% of Scores revenue, 5% of total company revenue, and less than 20% of operating profit.

Perion Network ( PERI up +31.2%) – Our investment in the digital advertising solutions provider continues to deliver despite broader market turbulence and pessimism within the adtech industry. Perion’s strong performance during the quarter was driven by continued growth in the business as the company reported 31% revenue growth YoY and 141% growth in net income. Management pre-announced a further 30% growth in revenue for Q4. These are spectacular results, but what makes this an especially attractive investment is that the company is trading at a 7x EV to Cash Flow multiple. Pinpointing the source for the valuation discount leads us to a few possibilities:

- Their fundamental business is in the advertising market, which traditionally underperforms during times of economic slowdown as corporations cut advertising budgets.

- At $1.2B in market cap, the company is small and operates under the radar of most institutional investors. There are six analysts covering the company, but no coverage from any of the brand name investment banks.

- The company is headquartered in Israel.

Regardless of the valuation discrepancy, we believe Perion will continue to thrive due to the value they deliver to their customers and the support from the rapid growth of their niche segments within ad technology. Perion's iHub has proven a unique ability to match up the demand and supply within the market. The demand side is advertisers and the brand messages they want to communicate. These are then matched to the supply side which can include advertising spots supplied by search engines, social media, and video or Cable TV. Perion has targeted and captured the rapidly growing video and connected-TV market. PERI is growing this business segment at over 245% year-over-year. Another innovative Perion service is SORT. Perion's SORT allows brands to gather unique information about consumers without collecting cookies, thus creating privacy for consumers while providing customers with unique and actionable data. An important dynamic for advertisers who recognize that consumers increasingly favor brands that protect consumer privacy.

Our biggest detractors for the quarter:

Our biggest detractors for the quarter included The Trade Desk ( TTD down 25.0%), Par Technology ( PAR down 11.7%), and Waste Connections ( WCN down 1.7%) . We have discussed each of these in recent letters, and so we won’t rehash these this quarter.

We had a couple of new additions to the portfolio. One name of note was Richardson Electronics.

Richardson Electronics ( RELL up +41.6%) – Richardson Electronics is an engineered solutions services provider that is at the beginning of a meaningful transformation from a company that produces tubes and electrical components to a provider of green energy solutions. Richardson has multiple products in the green energy space, but their primary growth engine for the future is the designing and integration of ultracapacitor and lithium-ion batteries in niche products such as solar, wind, and power management applications. This shift in the business was validated in their most recent quarter as sales in their Green Energy Solutions segment more than tripled from the year prior. Management guidance confirmed continued future growth in this segment.

Despite the recent stock inflection, we believe Richardson is just scratching the surface in terms of its full potential. Richardson is working with large companies such as Siemens, Progress Rail (a division of Caterpillar), GE, AT&T, and turbine operator NextEra for several different power management solutions. This is the “who’s who” of corporations making large active investments into electrification and green energy, with any one of these many opportunities presenting an exponential growth opportunity for Richardson. We believe there is a long and profitable runway for RELL from a combination of existing products, products in the pipeline, and future opportunities on the horizon. You can find our more detailed report here .

Business Updates:

For the second consecutive quarter, we welcomed a new addition to the Richie Capital Group team.Eric Crownjoined our team in November as a Senior Investment Analyst. Eric has over five years of experience in the investment industry and will be involved in all aspects of our investments as we seek to continually improve our process and the performance and support we provide to our clients. We are excited to have him because Eric is truly a stock “junkie” who loves to immerse himself in all things investment related. That characteristic is a prerequisite for our investment team. He has made an immediate impact, and you can sample some of his work through his writeup on our new investment Richardson Electronics . Eric is a graduate of Siena College and he holds the Chartered Financial Analyst designation. Welcome to the team, Eric!

Our team remains positive as we continue to navigate the current market environment. These are the periods where we can provide the most value to our clients. We are up to the task and prepared. We believe we are doing some of our best work turning over many rocks to identify unique and niche investment opportunities. The investments we are making today will pay significant dividends in the future.

Khadir Richie, CIO, Richie Capital Group

Footnotes[1] All portfolio and index returns mentioned are presented net of expenses and maximum management fees paid by any account within the composite. All performance is estimated pending year-end performance audit. Completed audit numbers available upon request. [2] The RCG Long Only strategy has been rebranded the “RCG Select Alpha Strategy” as we continue to expand our client offerings. [3] BarclayHedge Equity L/S Index [4] $14T total for G20 economies ($5T from the US) and the largest stimulus as a percentage of GDP in world history. [5] Source: https://www.forbes.com/sites/rahulrai/2021/11/16/a - tale - of - two - cities - the - federal - reserves growing - influence - on - bitcoin/?sh=535d359e783b |

DISCLOSURESThe information contained herein reflects the opinions and projections of Richie Capital Group, LLC and its affiliates as of the date of publication, which are subject to change without notice at any time subsequent to the date of issue. Richie Capital Group does not represent that any opinion or projection will be realized. All information provided is for informational purposes only and should not be deemed as investment advice or a recommendation to purchase or sell any specific security. This shall not constitute an offer to sell or the solicitation of an offer to buy any interests in any fund managed by Richie Capital Group or any of its affiliates. Richie Capital Group has an economic interest in the price movement of the securities discussed in this presentation, but Richie Capital Group's economic interest is subject to change without notice. While the information presented herein is believed to be reliable, no representation or warranty is made concerning the accuracy of any data presented. This communication is confidential, and all content contained herein is protected by U.S. and international copyright laws. You may not copy, reproduce, distribute, transmit, modify, create derivative works, or in any way exploit any part of copyrighted material without the prior written permission from Richie Capital Group. Performance returns are estimated pending year-end audit. Past performance is not indicative of future results. Actual returns may differ from the returns presented. Factors that could result in a difference between composite returns and client account returns include, but are not limited to, account asset size, asset allocation, timing of transactions, commissions, management fees and specific client mandates relative to individual investment objectives. Estimated returns are presented net of expenses and maximum management fees. All dividends are assumed to be reinvested. References to market or composite indices, benchmarks or other measures of relative market performance over a specified period of time are provided for information only. Generally speaking, when you feel stupid it’s because you just got smarter. The composition of a benchmark index may not reflect the manner in which a Richie Capital Group portfolio is constructed in relation to expected or achieved returns, investment holdings, portfolio guidelines, restrictions, sectors, or concentrations, all of which are subject to change over time. Each client will receive individual returns from their respective custodian. Positions reflected in this letter do not represent all the positions held, purchased, or sold, and in the aggregate, the information may represent a small percentage of activity. The information presented is intended to provide insight into the noteworthy events affecting returns for clients. |

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Richie Capital Group Q4 2022 Letter To Investors