AES - Riding The Green Wave: Fluence Energy Is A Top Pick

2023-08-31 14:16:11 ET

Summary

- Fluence Energy, a leading player in the battery storage sector, is positioned for strong growth due to robust public investments in battery storage and two internal catalysts.

- The company operates in both hardware and software sides of energy storage, with advanced software products leveraging AI and machine learning.

- Public incentives for energy storage, such as tax credits and government funding, further support Fluence's growth prospects.

Over the past two decades, energy storage has evolved from a niche and relatively unknown technology to becoming the focal point of the entire utility sector. With an ever-increasing share of energy capacity coming from renewable sources, it's becoming increasingly important to support the electric grid with means to store and release energy based on demand and supply.

Fluence Energy ( FLNC ), a company formed in 2018 as a joint venture between AES Corporation ( AES ) and Siemens AG ( SMEGF ), stands as one of the global giants in the battery storage sector. Given the momentum of this megatrend, I felt it imperative to delve into this stock and evaluate the company's competitive position.

After a thorough analysis of the company's fundamentals, I'm convinced that it's a prime buy for three primary reasons:

- Robust public investments in battery storage, ensuring strong growth in the sector for the coming years.

- Two internal catalysts related to how Fluent Energy runs its operations.

- Extremely compelling financial data.

This also marks the beginning of my analytical journey, focusing predominantly on companies tied to sustainability and the energy transition.

Fluence's Business Model

Fluence Energy effectively runs two businesses: the design and sale of battery storage hardware and the software side of energy storage and grid management. While these two facets complement each other, they are distinct: their software is also sold to third parties and represents advanced products that hold significant value, not merely an extension of their energy storage offerings.

The two flagship software products from Fluence are Mosaic and Nispera. Mosaic is predominantly used for intelligent bidding, optimizing revenues by injecting stored energy into the electric grid at the most opportune moments. Nispera, on the other hand, is used for asset management, both for storage and energy production. These software products leverage AI and machine learning, constantly evolving to enhance operational efficiency, preempt faults, flag anomalies, and maximize energy arbitrage ROI.

On the hardware side, Fluence's offerings revolve around the Fluence Cube. This modular system is designed for scalability, allowing multiple Cubes to be combined based on the storage needs of the client. Currently, their lithium battery technology is sourced exclusively from China, with European supplies starting soon and the U.S., along with their contract manufacturing facility in Utah, set to begin in 2024.

Public Incentives for Energy Storage

Thanks to the Inflation Reduction Act, energy storage systems can now benefit from a 30% Investment Tax Provision. Furthermore, section 45X offers a $10 per KWh tax credit, based on the capacity of battery modules produced in the U.S., to boost domestic battery production. This is particularly significant for Fluence, as they are set to receive batteries from AESC in the U.S. by 2024 and will subsequently produce modules independently. The company has confirmed in their latest earnings call that both the batteries from AESC and those produced in-house will meet the requirements of section 45X.

Fluence can opt for a direct credit payment of $10/KWh, making this incentive particularly vital. The Utah facility, intended for their battery production, is expected to initially operate at an annual capacity of 6 GWh, as per management's projection. This translates to an annual $60 million in tax credits based on initial production rates. Even though this might seem like a minor contribution for a company projected to end 2023 with over $2 billion in revenue, it's crucial to understand that Fluence's business operates on thin margins at present, and these additional revenues are not linked to any marginal costs. Every percentage point of gross profit is pivotal right now.

Lastly, the Infrastructure And Jobs Act has allocated $505 million to the DOE to fund energy storage demonstration projects. While this is a lesser contribution, it underscores the government's intense focus on the sector in which Fluence operates.

To the present day, 12.000+ Fluent Cubes have been installed (Fluent Energy - Company Website)

SWOT Analysis

The energy storage market, according to Fortune Business Insights , is expected to grow at an annual CAGR of 19% until 2029; BloombergNEF even places the growth rate at 23%. It is undoubtedly a rapidly expanding market, yet it is also filled with uncertainties. This is why I find it crucial to critically analyze the opportunities and threats that Fluence faces in its sector.

Opportunities and Strengths

The primary opportunity comes from the rapidly expanding market, backed by all government policies directed towards ecological transition and the installation of renewable energy sources. The legislative wind is blowing in Fluence's direction, and this is always a good sign.

Speaking of internal opportunities, undoubtedly the initiation of their own battery production could lead to a reduction in COGS. Currently, Fluence's main challenge is to increase gross profit, so the production cost achieved in the Utah plant will be pivotal in determining the company's future.

Another opportunity is tied to Fluence establishing a strong presence in Germany and its plans to extend its projects to Northern Europe. Here, governments are also pushing for the installation of energy storage systems. The European Union aims to achieve net-zero by 2050, and several northern countries plan to get there sooner. Given that Fluence originated from a Siemens subsidiary, there's potential to secure significant orders in the European market.

Weaknesses and Threats

Fluence's primary weakness is related to battery procurement, which at the moment is not very diversified. The vast majority of their supplies come from China, and any further increase in tariffs - a possibility that cannot be excluded - could harm the margins compared to companies that produce or source exclusively in the US.

Additionally, there's technological uncertainty surrounding the battery storage market. As highlighted in my analysis of Solid Power, solid-state batteries will soon start to be mass-produced, and Fluence hasn't made any references to preparing for this eventuality. There are also other technologies vying to replace lithium batteries in the battery storage world, like sodium-ion batteries.

Lastly, there's a tangible concern about Tesla (TSLA) rapidly conquering the battery storage world, but that's a lengthy and intricate discussion that I'll reserve for an analysis dedicated solely to this aspect.

The Issue of Gross Profit Margin

As I mentioned earlier, Fluence's main issue is the gross profit margin. This becomes clear when examining the income statements of recent years (data in $ millions, provided by Seeking Alpha).

| 2019 |

| 2020 |

| 2021 |

| 2022 |

| TTM |

| Revenue |

| 92.2 |

| 561.3 |

| 680.8 |

| 1,198.60 |

| 1,987.00 |

| Gross profit |

| -7.9 |

| 7.9 |

| 15 |

| -11.4 |

| 79.8 |

| Gross profit margin |

| -8.57% |

| 1.41% |

| 2.20% |

| -0.95% |

| 4.02% |

| Operating expense |

| 41.7 |

| 48.7 |

| 89.3 |

| 221.2 |

| 252.1 |

| OpEx/Revenue |

| 45.23% |

| 8.68% |

| 13.12% |

| 18.45% |

| 12.69% |

There's no doubt the situation improved dramatically between 2019 and 2020, with Fluence completely changing its operational level during that two-year span. However, since then, the profit margins have remained low.

The good news is that with the scaling up of operations, operating expenses have decreased significantly. In Q3 2023 data , the OpEx/Revenue ratio stood at 10.9%, and the gross profit was 4.1%.

For 2024, a significant improvement in the gross profit margin is fortunately forecasted. Fluence mentioned in the last earnings call that contracts signed in recent months expect margins of 10-15%. Moreover, only $100-150 million of next year's revenue will come from legacy contracts with the reduced margins shown until now. Additionally, the company is optimistic about further margin improvement in 2025, when full-scale production in the Utah plant will have begun. In the words of CFO Manavendra Sial :

"So I think just from how to think about the 2024 margins, we are signing contracts in the 10% to 15% margin range and that is still the case. And but the Q4 margin is a good proxy for how to think about 2024 margins, right? And as we have a little bit more contribution from our services business and our digital business maybe takes up a little bit, but Q4 is a good proxy for 2024 and that will continue to increase as we go from 2024 to 2025, so that's one. [...] we are done with most of our legacy projects. I think there's about $100 million to $150 million that trickles into 2024, mostly done in the first half of the year."

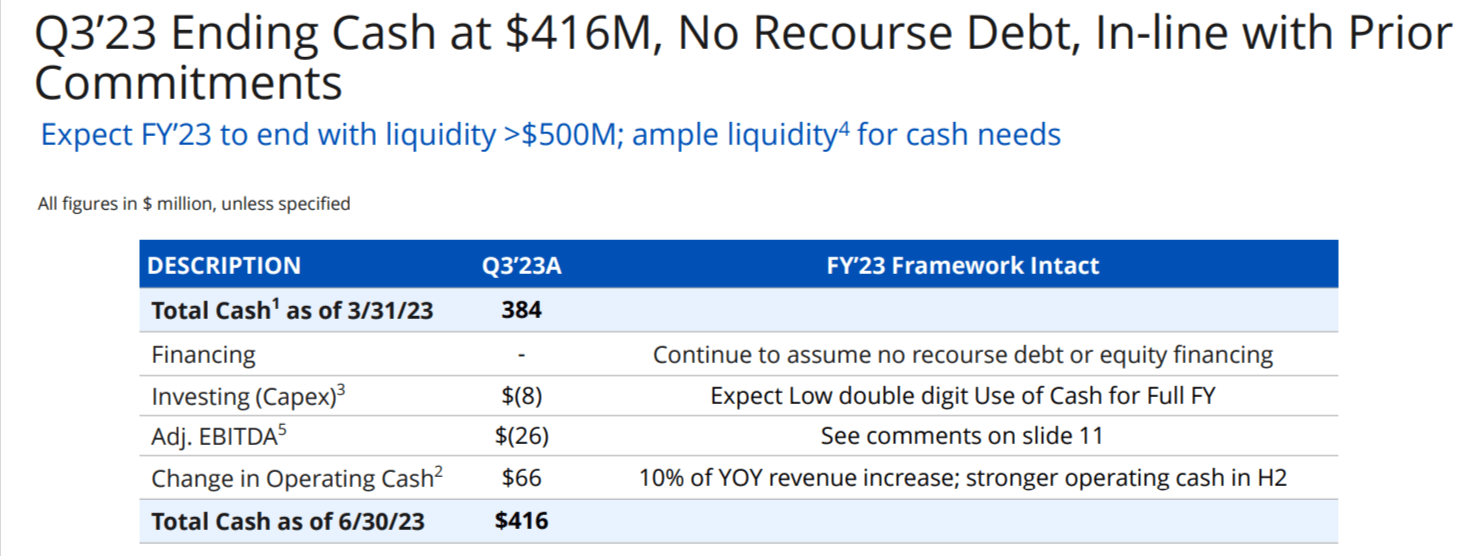

No Pressure from Cash Flow and Debts

As of June 30, 2023, Fluence had $416 million in cash and equivalents. This is against virtually non-existent debts: long-term debts are just $21 million, and the company generated cash from its core business in the third quarter. Fluence's forecast is to close the fourth quarter of the year with a break-even in cash flows, and the company believes it has ample resources to cover the liquidity need for 2024.

One thing that struck me is that the company continues to maintain capex forecasts of $10-15 million in 2024, despite accelerating revenues. This is also thanks to the fact that the Utah plant is a contract manufacturing facility, and hence Fluence didn't have to build the factory using its resources.

Fluence Energy - Q3 Earnings Presentation

{kind=link}

2026: The Key Year

If everything goes as planned, Fluence shareholders are well-positioned for a significant reward in 2026. This is due both to the expected improvement in gross profit margins and the constant decrease in the OpEx/Revenue ratio. The gross profit margin should start to stabilize around 15%, with the OpEx/Revenue ratio settling around 9-10%. Since depreciation and amortization have minimal impact on Fluence's balance sheets, we're left with an EBITDA margin of approximately 5.5%.

The company expects a revenue growth rate of 35-40% for 2024. To be pessimistic, let's assume that in 2025 revenues grow only by 20% and another 15% in 2026. The scenario would look as follows:

| Forecast for 2026 ($ millions) |

| Revenue |

| 3795 |

| Gross Profit |

| 569.25 |

| Opex |

| 360.525 |

| D&A |

| 3 |

| EBITDA |

| 211.73 |

With at least $60 million coming from its battery production, there will likely be no difference between EBITDA and net income. At the current market capitalization, this implies a 2025 price/EBITDA ratio of 21.20. Considering this would be a conservative revenue forecast for a rapidly growing company, given expanding margins and the complete absence of debt, coupled with likely lower interest rates than today, it's hard to believe such a company would be valued at less than the 34 price/EBITDA ratio that Enphase Energy (ENPH) currently commands.

If Fluence's valuation matched Enphase's multiples, this would mean that by 2026 the company could be valued at $7.198 billion. This suggests a potential upside of 54% over three years.

Final Thoughts and Conclusions

Fluence has proven to be a company capable of setting ambitious goals and consistently exceeding them. It's riding the wave of a rapidly growing sector without burning cash or accruing debt. The company's fundamentals are excellent from all perspectives. The energy storage industry is central to both onshoring hardware production policies for the energy transition and those related to increasing energy produced from renewable sources.

Given my calculations, I believe all the foundations for a sound investment are there. My long-term plan remains to hold the shares in my portfolio until 2026, but I will regularly update my forecasts along the way.

For further details see:

Riding The Green Wave: Fluence Energy Is A Top Pick