BRENF - Riding The Green Wave: Why Brookfield Renewable Is Your Next Must-Have Investment

2023-08-10 09:15:00 ET

Summary

- Triple Triumph: Brookfield Renewables shines with dividends, growth, and clean energy, targeting a 12-15% long-term total return.

- Global Leader: With 25,900 MW in 20 countries, Brookfield spearheads the renewable energy shift, offering attractive long-term investment potential.

- Nuclear Future: Regulatory hurdles aside, an ambitious nuclear power plant equipment deal unlocks future growth avenues.

- Investor Appeal: A consistent dividend record, solid balance sheet and a massive pipeline make Brookfield Renewables a compelling buy at a 5% yield.

The Q2/2023 earnings season is in full swing which always marks an especially busy time for me given that I want to capitalize on unwarranted sell-offs and continued stock price weakness.

I am looking for attractive stock prices, profound long-term investment cases, and 4%+ dividend yields. This year my best performers next to Apple ( AAPL ), Microsoft ( MSFT ), AMD ( AMD ) and Nvidia ( NVDA ) are my investments in Business Development Companies which are one of the main beneficiaries of rising interest rates.

In contrast, this year's underperformers are debt-reliant entities, primarily in REITs and capital-intensive energy partnerships. Notably, NextEra Energy Partners ( NEP ) and Brookfield Renewable Partners ( BEP ), favorites of mine, have faced setbacks in this regard.

Amid the COVID-19 pandemic, Brookfield Renewable Partners shone, but lost momentum due to rising inflation and interest rates. With the Fed Funds Rate exceeding 5%, investing in 5% yielding BEP appears less appealing against lower-risk Treasury market options.

While this diminishes short-term enthusiasm, the long-term horizon, my focal point, unveils generational buying prospects at current Brookfield Renewables' prices.

What is going on at Brookfield Renewable?

Brookfield's latest earnings were reported August 4, 2023, for the second quarter of 2023 which showed decent FFO per unit growth of 4.3% and YTD FFO growth of 9.6% with FFO climbing to $0.91 for the first two quarters of 2023.

My quarterly highlights include:

- Investing $1.3B into growth activities ($300M net to Brookfield Renewable)

- Commissioning approximately 1,500 megawatts of capacity

- Asset recycling activities have already generated north of $400M in proceeds

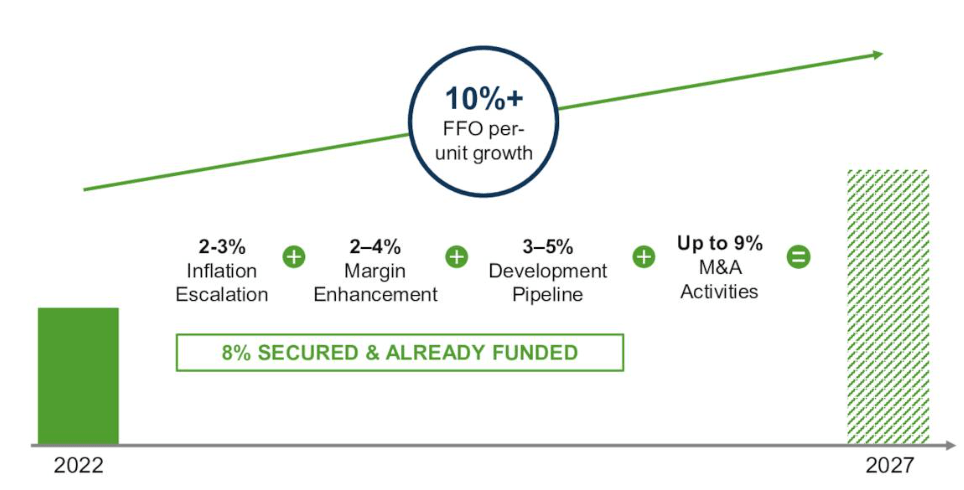

The best news so far though is actually the almost double-digit FFO growth YTD which sets the company into a strong position towards achieving its long-term 10%+ FFO per-unit growth.

{kind=link}

FFO Growth Targets (Investor Relations)

This is also emphasized by recent commentary from Brookfield's management:

In closing, we remain focused on delivering 12% to 15% long-term total returns for our investors. To do this, we will continue to leverage our differentiated growth capabilities, advancing our significantly derisk pipeline of projects, being opportunistic in the current market and investing in our operating to add value.

Source: Brookfield Renewables Q2/2023 Earnings Call

Brookfield Renewables is the leading global decarbonization leader with over 25,900 MW of operating capacity spread across 20 countries with around half of that capacity situated in North America. Its business covers renewable energy assets such as hydro, wind, solar and distributed storage.

Its long-term pipeline features projects with an operating capacity in excess of 130,000 MW of which almost half is attributable to Brookfield's solar business. A further 5,000 MW are planned for commissioning in 2023 and another 19,000 MW in the near future. The 5,000 MW planned for this year will add approximately $70M of incremental FFO to the company.

Overall, these growth levers coupled with previously mentioned M&A activities should drive annual FFO per share growth in excess of 10% and thereby add another successful chapter to the stock's long-term track record of strong performance. Management already confirmed that it had locked in at least 8% annual FFO per share growth, and thus with increasing confidence, investors can bank on double-digit FFO growth into the year 2027.

Brookfield Renewables sports a superior balance sheet resilient enough to cope with the current interest rate environment as the company held more than $4.5B of available liquidity by the end of June 2023 as well as top BBB+ investment-grade credit rating. Thanks to Brookfield Renewable's unrivaled balance sheet and financial position, even today's hawkish interest rate environment is not a disadvantage - if anything it is a competitive advantage as other players cannot boast such strong financial health and resilience as more than 90% of its borrowings are fixed-rate debt.

Whatever way you look at it, Brookfield is positioned for multi-year and potentially multi-decade double-digit FFO growth and additional organic growth drivers coupled with new acquisitions which Brookfield is actively seeking will further add to its growth potential.

One of those initiatives though - the big $7.9B deal for acquiring nuclear power plant equipment maker Westinghouse Electric - is currently facing regulatory hurdles as reported by Reuters.

The Competition and Markets Authority ((CMA)) said it had invited comments on the deal from interested parties. It did not give any further details.

Source: Reuters

The market's reaction to this news seems puzzling since it's part of the regular regulatory approval process. However, it unexpectedly impacted Brookfield Renewable Partners' stock price. Management remains unfazed by this development, and investors are advised to disregard the noise and concentrate on the crucial aspect: :

And I would say none of this is unexpected or unusual. And we are simply going through the typical process for a transaction of this nature.

Source: Brookfield Renewables Q2/2023 Earnings Call

If this deal materializes, it is a big bet on a prosperous nuclear future. I firmly believe in the potential of nuclear energy, which is clearly on the rise. Westinghouse, a major nuclear services player, stands to enhance the industry. The $8B transaction, set to conclude in H2 2023, already benefits Brookfield as nuclear gains traction for clean and dependable baseload power generation.

What's in it for Dividend Investors

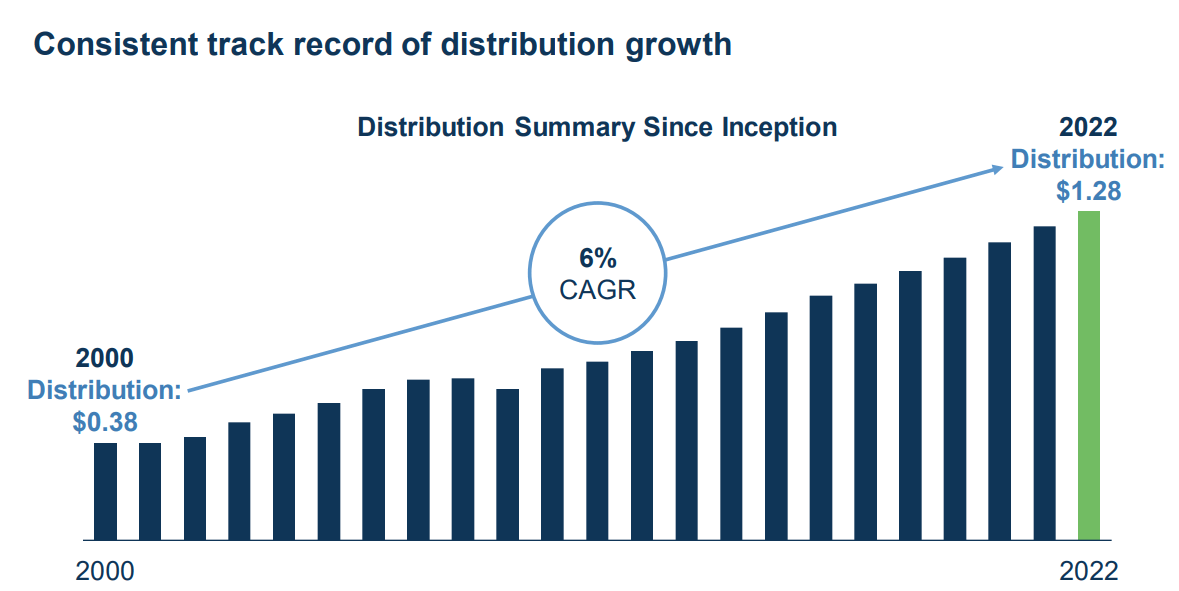

Brookfield Renewable features an impressive dividend track record with a long streak of consecutive dividend increases. Over the last couple of years, the distribution has been growing at a 6% clip and this sort of pace is expected to continue as Brookfield is working towards its goal of achieving a 70% FFO-based payout ratio. YTD its payout ratio stands at 74% and is inching closer to that target ratio despite the company raising its dividend by another 5.5% in early February this year.

Overall, Brookfield Renewables is a must-own long-term dividend growth stock despite its distribution only growing by 6% on a CAGR basis which may appear lackluster in the current interest rate environment. However, at a 6% clip this means that the distribution increased from $0.38 in 2000 to $1.28 in 2022 and thus more than tripled.

{kind=link}

Consistent Track Record of Distribution Growth (Investor Relations)

A 6% average growth rate over decades is primed to deliver substantial income and given Brookfield's pipeline, its access to capital markets, and its secured cash flow growth, basically all roads lead to substantial future FFO growth. The projected 10%+ business growth in the next five years anticipates 5-9% annual distribution expansion. Hence, there's compelling evidence that the past 6% CAGR can be mirrored over the next two decades, with a prudent outlook for a high single-digit distribution CAGR for Brookfield Renewable Partners.

Investor Takeaway

Brookfield Renewable Partners, a global leader in renewable energy, possesses a diverse portfolio covering hydroelectric, wind, and solar assets. As the urgency to combat climate change fuels the shift towards cleaner energy sources, the demand for renewables continues its upward trajectory, presenting a compelling growth opportunity for global industry players like Brookfield Renewable Partners.

A lot of that growth over the next five years has already been secured and thanks to the partnership's strong financial position I have full confidence management will continue to find additional attractively valued growth opportunities and continue its 12-year dividend growth streak.

Regulatory uncertainty or even scrutiny is common practice in the energy sector and should not spook investors at all. If anything, it is time to embrace the current downtrend in its stock price.

Long-term, all roads lead to future FFO and distribution growth and with its current starting yield in excess of 5% again this for me presents a generational buying opportunity I certainly won't regret.

For further details see:

Riding The Green Wave: Why Brookfield Renewable Is Your Next Must-Have Investment