RIGL - Rigel Pharmaceuticals: A Strong Finish To 2022 And A Potentially Transformative 2023

Summary

- In terms of product sales, RIGL has been a one drug company with Tavalisse in immune thrombocytopenia.

- The recent approval of Rezlidhia opens the door for investors to track the growth of another drug, a new source of excitement.

- The potential for sales growth with Tavalisse is still there, the COVID indication could still materialize with more shots on goal ahead.

Since I last wrote about Rigel Pharmaceuticals ( RIGL ) the company provided encouraging updates on their leukemia drug Rezlidhia (olutasidenib) and some bad news on the company's COVID trial of fostamatinib. This article takes a look at the prospects of Rezlidhia and where RIGL stands in the COVID indication.

Approval and Launch: Rezlidhia

On December 1, RIGL announced Rezlidhia had been approved by the US Food and Drug Administration ((FDA)) in relapsed/refractory acute myeloid leukemia patients with a susceptible IDH1 mutation. While the PDUFA date for RIGL's olutasidenib was February 15, 2023, an early December approval is a nice surprise for the company. I wondered what RIGL would be able to make of the early approval, but December 22 saw RIGL announce the availability of Rezlidhia, meaning the company has made the most of an early approval. RIGL has been quick to note the good fit of Rezlidhia with Tavalisse in the commercial and medical affairs infrastructure since it got a hold of marketing rights to the drug from Forma Therapeutics in August 2022.

{kind=link}

The positive news comes on top of updates from a phase 2 trial of Rezlidhia in the AML indication, where RIGL noted durable responses to Rezlidhia that looked very impressive compared to the already approved competitor Tibsovo (ivosidenib) from Servier Pharmaceuticals. That comparison is cross-trial, Tibsovo and Rezlidhia haven't been compared in a head-to-head study, but participants on RIGL's recent earnings call were quick to point out the strong data. The company didn't have a concrete answer as to why their drug appeared better than the obvious competitor, but the idea that the difference isn't down to the trial simply enrolling different demographics means that prescribers might reach for Rezlidhia over Tibsovo in the AML indication.

... We cannot identify the one reason why all those signals look so good, but we can rule out a few things. For example, we look at the baseline demographics between the two studies with the numbers and the patient populations appear to look comparable . We do notice that we have a very high, higher number of the complete responders that I said earlier, the ones who really have full hematologic recovery. And we do know that better your initial response is the better the long-term prognosis and the duration of response, so that might contribute.

Wolfgang Dummer, Executive Vice President and Chief Medical Officer, RIGL Q3'22 earnings call , emphasis mine.

In a subsequent upgrade , Yigal Nochomovitz at Citi noted the strengths of Rezlidhia in efficacy and reduced cardiotoxicity vs Servier's Tibsovo and forecasted 50% of market share for the drug.

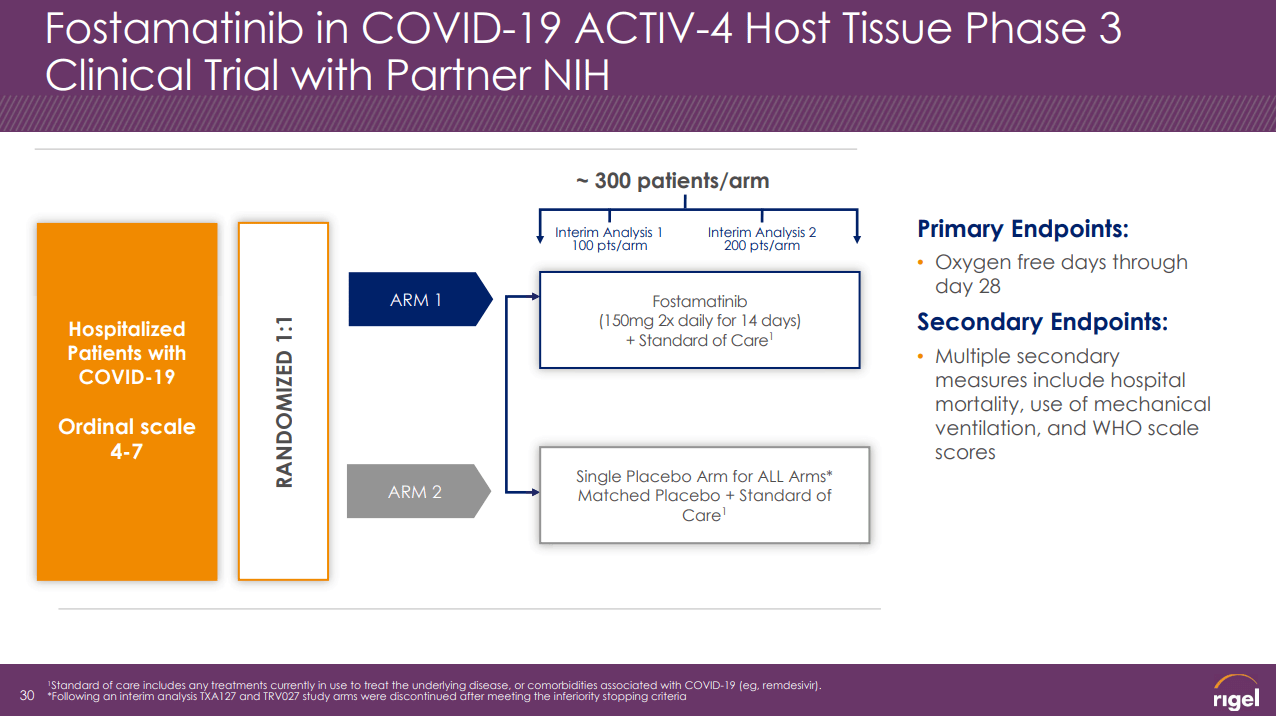

The phase 3 COVID study fails

RIGL's phase 3 study of fostamatinib plus standard of care ((SOC)) vs placebo plus SOC in COVID, ended up enrolling only 280-patients out of a planned 308. On November 1, RIGL reported the top-line results from the study. From Day 1 to Day 29, patients on fostamatinib plus SOC (n=141) spent an average of 6.9 days on oxygen, compared to 9.0 days on average in the placebo plus SOC group (n=139). That difference wasn't statistically significant, so the primary endpoint was missed (p=0.0603). You have to wonder how things might have been had RIGL waited to enroll 308 patients.

RIGL's original phase 2 study of fostamatinib in COVID was in just 59 patients, and the primary outcome measure was the number of participants with at least one serious adverse event ((SAE)). Fostamatinib was numerically superior to placebo on this endpoint.

By day 29, there were three SAEs in the fostamatinib plus standard of care (SOC) group of thirty patients compared to six SAEs in the placebo plus SOC group of twenty-nine patients (p=0.23). Of these, there was a reduction for the disease related SAE of hypoxia in the fostamatinib group compared to placebo (1 vs 3, respectively; p=0.29).

Comments from RIGL press release , April 13, 2021.

With only 59 patients in the study, and only so many patients actually experiencing an SAE, it isn't surprising that the phase 2 study didn't end up producing a significant result by this measure.

At 29 days however, the difference in change on the ordinal scale between fostamatinib and placebo didn't achieve statistical significance (mean change -4.2 compared to -3.3, p=0.12), but still trended in favor of fostamatinib. The ordinal scale ranges from 8, death, to 1, not hospitalized with no limitations on activity. Those enrolled in the study ranged from 7, hospitalized, on invasive mechanical ventilation or extracorporeal membrane oxygenation (ECMO) to 5, hospitalized, requiring supplemental oxygen, at baseline. This change at 29 days was the first secondary outcome measure listed on the clinicaltrials.gov entry for the trial.

Considering the phase 2 data and phase 3 data certainly trended in favor of fostamatinib, the possibility that with a bit larger trial, fostamatinib might succeed, is still in play. That possibility exists with the ACTIV-4 study , and while I can't say the data in that study has trended in favor of fostamatinib, fostamatinib made it through interim analysis without stopping in the ACTIV-4 study, whereas two other drugs were stopped (TXA127 and TRV027) after meeting the inferiority stopping criteria.

{kind=link}

The current clinicaltrials.gov estimated primary completion date form the ACTIV-4 study is February 10, 2023. A second clinicaltrials.gov listing was created in October 2022, and lists international sites (as opposed to US sites in the first listing) in Brazil, Germany, South Africa and Spain. Whether or not this will accelerate or delay the production of a result from the trial isn't clear, so those following RIGL should keep an eye on updates to the clinicaltrials.gov entry as we approach the listed completion date.

Financial information

RIGL announced total revenues for Q3'2022 (ending September 30, 2022) of $22.4M including net product sales of $19.2M for Tavalisse, up from $18.6M the quarter prior. Net loss was $19M for the quarter and RIGL finished the quarter with cash, cash equivalents and short-term investments of $81.6M. Net cash used in operating activities was $51.85M in the first nine months of 2022 so at the current rate RIGL would be out of cash in under 18 months. To be fair, RIGL has made cuts to the workforce so savings there should be seen in the future, RIGL expects about $7M-$8M annually starting 2023. The principal owing on RIGL's loan from MidCap Financial trust was $40M as of September 30, 2022. With the Japanese approval of fostamatinib in ITP announced on December 23, by RIGL's partner Kissei Pharmaceutical ( KSPHF ), RIGL can expect a $20M milestone payment, possibly late this year or in Q1'23.

RIGL also has $48.9M of outstanding financing liability to Eli Lilly ( LLY ) as of September 30, 2022, as the two are developing RIPK1 inhibitors together. LLY has billed RIGL $12.4M up to September 30, 2022, which RIGL has paid in full, since the agreement with LLY was made in February 2021. Thus far then, the LLY agreement hasn't been draining RIGL's funds too rapidly. With 172,836,336 shares outstanding as of October 28, RIGL has a market cap of $224.7M at $1.30 per share.

Conclusion

Overall the potential for revenue growth with Tavalisse is still there, and while the anemia indication looks off the cards for now, I don't think the same can be said about COVID. Meanwhile, early approval and launch of Rezlidhia offers an opportunity to provide topline growth for RIGL, which will help reassure investors the Forma/olutasidenib deal was worth the price paid. I consider RIGL to be a strong buy heading into 2023 on the improved potential of Rezlidhia and the potential of a successful result with fostamatinib in COVID-19. The risks of any long are several fold, a few worth considering are the potential failure of fostamatinib in the ACTIV-4 study, a slow launch for Rezlidhia and weak sales growth of Tavalisse in the existing ITP indication.

For further details see:

Rigel Pharmaceuticals: A Strong Finish To 2022 And A Potentially Transformative 2023