RTMVF - Rightmove: 10%+ EPS Growth But Only After 2023

2023-03-07 03:54:40 ET

Summary

- 2022 results showed the strength of Rightmove’s business, with a 10% EPS growth achieved on a flattish customer count.

- The 2023 outlook implies a flat EPS, due to lower ARPA growth, cost increases, and a higher tax rate.

- 10%+ EPS growth will likely resume in 2024, helped by growth in Other Revenues and small improvements in EBIT margin.

- Shares have a 24.5x P/E and a 1.5% Dividend Yield. There is an additional upside if the U.K. housing transaction volume starts growing again.

- With shares at 570.8p, we expect a total return of 44% (14.1% annualized) by 2025 year-end. Buy.

Introduction

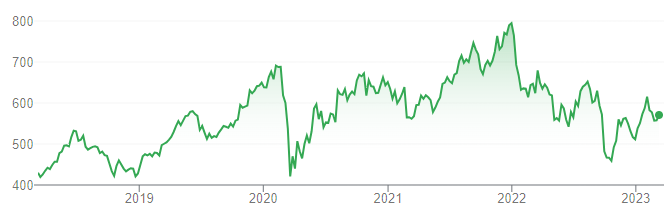

Rightmove PLC (RTMVY) (RTMVF) released 2022 results on Friday (March 3). Shares fell 1% on the day but rebounded 2% on Monday, though they are still down 12% in the past year and nearly 30% below their December 2021 peak:

{kind=link}

We upgraded our rating on Rightmove to Buy in October 2021. Since then shares have lost 14% (after dividends). (Our Buy ratings during parts of 2019 and 2020 were more successful, generating gains of 30% and 41%, respectively.)

2022 results showed the underlying strength of Rightmove's business, with an 10% EPS growth driven by Average Revenue Per Agent ("ARPA") growth and buybacks. However, 2023 outlook implies a flat EPS, due to a lower ARPA growth, cost increases and a higher tax rate. 10%+ EPS growth will likely resume in 2024, helped by growth in Other Revenues and small improvements in EBIT margin. There can be additional upside if U.K housing transaction volume starts growing again. Rightmove shares currently have a 24.5x P/E and a 1.5% Dividend Yield. Our forecasts indicate a total return of 44% (14.1% annualized) by 2025 year-end. Buy.

Rightmove Buy Case Recap

Rightmove is the #1 residential property listings website in the U.K. Its revenues consist primarily of subscription fees from estate agents (74% of 2022 revenues) and developers (16%), with different fees based on package tiers, products purchased, the number of branches and volumes. The company is also generating increasing amounts of revenues (10% of 2022 revenues) from other products, including commercial real estate, data services and mortgages.

We believe Rightmove will retain its dominance in U.K. residential property listings, helped by the network effect on its platform and the quality of its product features. The company has continued to enhance its value-add to customers by adding new features and by expanding into adjacencies such as tenant referencing and landlord insurance.

In our last article in July 2022, we had forecasted an 11% EPS CAGR from 2022 onwards, based on:

- Revenues growing at high-single-digit annually, driven by continuing Average Revenue Per Agent ("ARPA") growth from both price increases and customer upgrades, as well as a small growth in the number of customers

- EBIT margin recovering to 75% and then remaining stable thereafter, given Rightmove is a platform business with low incremental unit costs and natural operational leverage

- Management to continue to return all earnings to shareholders in dividends and buybacks

- Shares to trade at a P/E multiple of 30x at exit

Rightmove's 2022 results and outlook support our overall earnings growth expectations, but with a different balance of contribution between revenues and EBIT margin, and with 2023 likely to represent a pause in EPS growth.

Rightmove 2022 Results Headlines

2022 results showed the underlying strength of Rightmove's business, with EPS growth growing 9.8% year-on-year:

| Rightmove Profit & Loss (2019-22) Source: Rightmove results releases. NB. 2019 dividend excludes a 3.2p final dividend that was declared but not paid. |

Agency & New Homes revenues grew 9.2% year-on-year in aggregate, with a flattish (up 0.2%) total customer count and an ARPU growth of 10.5%. Within the customer count (measured at year-end), Agency customers fell 1.1% but New Homes customers grew 7.8%, reflecting a weaker housing market in H2 (following rate rises and macro uncertainty in the U.K.) that reduced new agency formation but encouraged more advertising by developers. Within the £125 ARPA growth, over 60% came from customers upgrading or buying more products, while the rest came from price increases.

Other Revenues grew 7.8% (£2.3m), with double-digit revenue growth in Commercial, Data Services and other products offset by a £2.6m revenue decline in Mortgages, the latter after Rightmove changed its monetization model there from a fixed marketing fee to commissions at the end of 2021.

Costs excluding Share-Based Compensation ("SBC"), or Underlying Costs in management terminology, grew 14.3% in 2022. Cost growth was driven by both new hires (headcount grew 12%) and by wage inflation, the latter also including a £1,000 per-head cost-of-living allowance and a decision to bring forward the 2023 pay rise to October 2022.

Reported EBIT grew 6.7%, or 7.9% excluding the £2.4m prior-year gain related to the write-off of a contingency payment related to the Van Mildert acquisition. Underlying EBIT, which also excludes SBC, grew 7.4%. Reported EBIT margin fell from 74.2% to 72.6%, while Underlying EBIT Margin fell from 75.0% to 73.8%.

Reported Net Income grew 6.9% and, with the share count having fallen 2.6% after buybacks, Reported EPS grew 9.8%. Underlying EPS, which excludes both SBC and the Van Mildert gain, grew 9.1%.

2022 EPS growth was largely driven by APRA growth (10.5%) and buybacks (2.6%), with minimal contribution from a flattish customer count, partially offset by a lower EBIT margin.

Across the 2019-22 period, which included a sharp reduction in revenues in 2020 from COVID-related customer discounts, Rightmove achieved CAGRs of 4.8% in revenues, 4.1% in EBIT and 6.2% in EPS.

Rightmove 2023 Outlook

Management's 2023 outlook implies a flat EPS, due to a lower ARPA growth, cost increases and a higher tax rate:

- Customer count to be "broadly stable", with "a small shift" from Agency to New Homes

- APRA growth in the middle of the previous £95-105 range, i.e. 7.6% on 2022 APRA of £1,314

- Other Revenue growth to be "healthy"

- Underlying EBIT margin of "around 73%", i.e. a small decline from 2022 (73.8%)

- Tax rate of 25%, compared to 17.9% in 2022, in line with the U.K. government's announced tax hike

Revenue assumptions are based on a relatively weak U.K. property market, but with Rightmove's APRA growth driven by "new product launches, ongoing product uptake and pricing actions". Cost assumptions include a 5% inflation increase in wages (compared to 3% in 2022) and further investments, offset by the absence of 2022 one-offs.

Applying these assumptions (and some of our own) imply a 2023 Net Income that is about 1.5% lower year-on-year, and a 2023 EPS that is flattish after buybacks.

10%+ EPS Growth from 2024

Rightmove's 10%+ EPS growth will likely resume in 2024, helped by growth in Other Revenues and small improvements in EBIT margin.

CFO Alison Dolan stated that Rightmove is expecting Other Revenues to "increase by about £10m a year" after 2023:

"Those businesses are so linked to the core business. The incremental investment is largely people and this means that they are very high-margin businesses … So margins in excess of the core business are being delivered by both data services and commercial real estate. As a category, once we're out of '23 … you should expect to see that other line increase by about £10 million a year, so already becoming already EBITDA accretive.

Each £10m in incremental revenues is worth around 3% of revenue growth (based on 2022).

Similarly, on margin, she agreed with an analyst question that the 73% Underlying EBIT Margin guided for 2023 will likely represent the trough, though she also rules out aiming for a return to 75%:

We fully intend to continue to deliver margins in excess of 70%. Having said that, returning to 75%, 76% is not an ambition that we particularly have either, as we -- particularly as we get behind these strategic initiatives. So is it the trough, probably broadly, but I'm talking within a 1%, 2% range."

Overall, compared to our original investment case, Rightmove now seems to be guiding to a higher revenue growth (driven by Other Revenues) but a lower peak EBIT margin over the medium term.

The combination of Rightmove's typical high-single-digit ARPA growth (from both price and mix), a flattish customer count, another 3 ppt of growth from Other Revenues and small improvements in EBIT margin will likely lead to a high-single-digit EBIT growth, which will in turn generate a 10%+ EPS growth including buybacks.

Upside if U.K. Real Estates Grow Again

There can be additional upside if the number of U.K housing transactions resume growing after years of stagnation.

Rightmove has been experiencing a decline in its customer count since 2019, including a much larger decline during COVID-19, though APRA growth has remained a reliable driver of revenue growth:

| Rightmove Revenue Growth by Component (2011-2022) Source: Rightmove company filings. |

Management commentary has attributed Agency customer declines to weakness across the U.K. real estate industry. As outgoing CEO Peter Brooks-Johnson explained on the call:

The political and economic uncertainty following the Brexit vote in 2016 saw the property market fall for 4 consecutive years. In this sustained slower market, we saw Agency branches stay stable for the first 2 years and then fall by a total of 6% over the second 2 years"

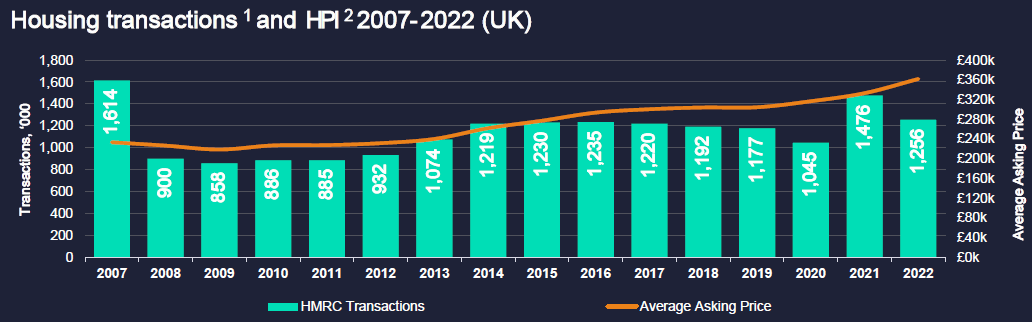

Data shows a multi-year decline in the number of housing transactions since 2016, only briefly interrupted in 2021 with a post-COVID rebound as well as temporary reductions in property transaction taxes to support home buyers:

| U.K. Housing Market Volume & Price (2007-22) Source: Rightmove results presentation (2022). N B. HMRC = His Majesty's Revenue & Excise; HPI = House Price Index. |

{kind=link}

Rightmove weekly sales data showed that property transaction volumes have fallen below their pre-COVID 2019 levels again since October 2022, though recovering since a trough in December:

| U.K. W eekly Residential Sales Agreed, Indexed to 2019 (Since Q4 2022) Source: Rightmove results presentation (2022). |

If/when U.K. housing transaction starts growing again, the number of U.K. real estate agents can increase substantially, and Rightmove's revenue growth will likely enjoy an additional impetus on top of the usual ARPA growth, generating further upside in the stock.

Rightmove Stock Valuation

At 570.8p, Rightmove stock is trading at a 24.4x P/E and a 4.0% Free Cash Flow Yield:

| Rightmove Earnings, Cashflows & Valuation (2019-22) Source: Rightmove company filings. |

Total dividends in 2022 were 8.5p, representing a Dividend Yield of 1.5%. Management has a policy to return all earnings to shareholders, with approximately one third to be done in dividends and two thirds in buybacks.

Rightmove Return Forecasts

Actual 2022 EPS (23.4p) was roughly in line with our forecast (23.5p).

We reduce our assumptions on Net Income, increased them on buybacks and cut our exit multiple. We now assume:

- Net Income to be flat at £196m (was £218m)

- Thereafter, Net Income to grow at 8% annually (was 9%)

- Share count to fall by 2% annually (was 1.5%)

- Dividends to be based on a 35% Payout Ratio (unchanged)

- 2025 year-end P/E of 27.5x (was 30.0x)

We are not explicitly modelling a downturn in the U.K., as we believe the negative impact on Rightmove earnings would likely be quickly offset by stronger growth in subsequent years.

Our new 2025 EPS forecast is 9% lower than before (31.9p):

| Illustrative Rightmove Returns Source: Librarian Capital estimates. |

With shares at 570.8p, we expect a total return of 44% (14.1% annualized) by 2025 year-end.

Is Rightmove A Buy? Conclusion

We reiterate our Buy rating on Rightmove PLC stock.

For further details see:

Rightmove: 10%+ EPS Growth, But Only After 2023