RTMVF - Rightmove: A High-Quality Business At An Attractive Entry Point

2023-03-13 09:30:04 ET

Summary

- The business enjoys strong economic moats via a natural network effect - stable c.80% market share over the past decade.

- Rightmove has a strong financial track record, and a history of willingness to return capital to shareholders.

- Macro headwinds provide an attractive entry point for a business that has continued to deliver growth.

Investment Thesis

Since the start of 2022, Rightmove (RTMVF) has traced downwards by c.25% due to wider macro headwinds. The stock trades at a discount vs pre-COVID levels and trades close to a 10-year low a forward EV / EBITDA basis. This is despite the business continuing to deliver on consistent growth over the recent years, enjoys an extremely strong competitive moat in the market it plays in with ~80%+ market share over the past decade, and boasts a highly capable management team. In an inflationary environment, the stock may even be a net beneficiary as there is minimal inflationary pressure on input costs given the digital nature of the business (EBITDA margins are high at ~70%+). It is my view that the market has mispriced the value of the business and does not fully recognise the strength and attractiveness of the business model.

Introduction

To give a brief introduction of Rightmove and the market it operates in, Rightmove operates in the online real estate portal industry, somewhat as part of a duopoly with Zoopla, with minor players including OnTheMarket.

Essentially, Rightmove links estate agents and new home developers on one end of the market to users in the process of buying or renting a property on the other end. Rightmove makes money by charging agents / developers a monthly membership fee and by selling additional marketing services to these agents / developers as they try to promote their listings to users who browse Rightmove’s portal of listings. In most cases, these fees are charged on a per physical office basis and Rightmove does not charge the user anything. Agents represent the bulk of revenues – c.75% for 1H22

Competitive Moats

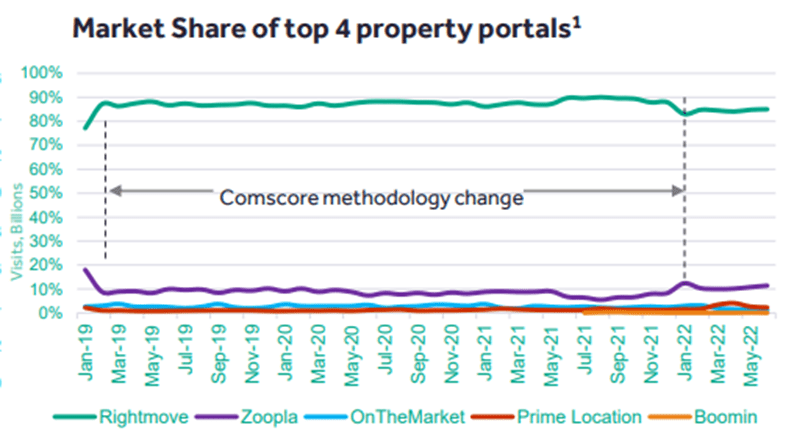

As the market leader by far in the UK with c.80%+ market share , the business enjoys strong competitive moats and has been able to consistently maintain a competitive advantage against its peers as can be seen from the stability of its market position over the past decade.

Company Investor Presentation Company Investor Presentation

{kind=link}

{kind=link}

Firstly, by virtue of the nature of the online real estate portal industry, the fact that it has a majority market share solidifies the barriers of entry against other competitors. Homes are a unique one-off purchase, often the largest single purchase for an individual. This means that (i) users typically want to view and assess the largest selection of properties and (ii) agents / developers similarly want the properties they are managing to be featured to the most number of users. As such, the more users a platform has, the more agents / developers would want to be on the platform as well. Similarly, the more listings there are as a result of having more agents / developers, the more users would want to be on it. This network effect makes it challenging for new players to successfully penetrate the market since both customers and agents / developers want to be with the largest player, in this case, Rightmove, with more than 80%+ market share.

Secondly it competes primarily with two other players (Zoopla and OnTheMarket) and competes well against them. Note that Prime Location is an associate of Zoopla, while Boomin went into liquidation in Oct 2022.

Rightmove’s first mover advantage has enabled it to capture a majority of the market by accumulating both agents / developers and users over the years since 2000. Since there is little incentive for either side to move to other online platforms, Zoopla has largely tried to do this in two ways. 1) Offer agents / developers lower fees compared to Rightmove in listing their properties. Zoopla ARPA is about a third of Rightmove’s. 2) Offer users a range of additional services that users are likely to encounter when buying a new house. While it is true that Zoopla has seen some growth historically supported by a series of acquisitions, growth has slowed especially after the launch of OnTheMarket in 2015. Interestingly, OnTheMarket was initially created to break the duopoly in the market and hence, there was a rule that ensured agents on OnTheMarket could only list on one other portal, either Rightmove or Zoopla. Given that the number of agents with Zoopla fell 16% in 2015, it seems that Rightmove was deemed by agents to be the “undroppable” platform and Zoopla is left to compete with OnTheMarket.

These factors contribute to Rightmove’s strong pricing power, allowing it to consistently take advantage of its sticky customer base by increasing ARPA, which stands for Average Revenue per Advertiser, over the last 10 years at a CAGR of c.10%+ while at the same time maintaining the number of agents / developers onboard. The fact that Rightmove also does not have any costs of revenue and most of its costs are a result of administrative costs from labour and rent, which are unlikely to rise as quickly as revenue, this has translated to both strong historical growth in revenue and high attractive EBITDA margins. Following a blip in 2020 as advertisers naturally cut marketing expenditure during the COVID period, the business has largely recovered in 2021 and such an attractive business model should enable Rightmove to continue enjoying strong earnings growth over the next few years as ARPA grows.

Company Investor Presentation

Revenue and EBITDA have continued to demonstrate strong growth over the historical period. Similarly, the business is extremely cash flow generative with minimal capex requirements – FCF is typically c.90%+. In turn, management has also demonstrated a willingness to return value to shareholders. For instance in FY21, they had issued GBP78m of dividends and repurchased GBP200m of shares.

Growth opportunities moving forward

Rightmove also has opportunities moving forward.

Although most agents / developers are already online on either Rightmove or Zoopla, suggesting that growth in number of agents / developers may already be limited, agents / developers are constantly seeking better products and services to better market their property listings to potential customers. Despite a blip in 2020, Rightmove has seen ARPA rebound almost immediately in 2021 levels above pre-COVID figures as they continue to deliver higher quality products to customers. On the 1H2022 earnings call, CEO Peter Brooks-Johnson also alluded to a GBP100 increase as the expected cadence for the business moving forward for FY23.

In 2017, Rightmove also alluded to a longer-term ARPA target of 2.5k . At that point, ARPA was only around the 1k level. Considering that since then, APRA has continued to increase c.30% to 1.3k, management has been able to deliver on growing this and is well on track to achieving their pre-set targets – lending credibility to its forecasts moving forward.

Attractive entry point following macro concerns

Since the start of 2022, the stock has traced downwards by c.25%. In early 2022, this was driven by broader macro concerns as the Ukraine war intensified and in Sep 2022, the stock retreated further as investors were spooked by the UK government’s new economic plan at the time. While the political (and economic) situation in the UK has since stabilised following the appointment of a new PM at end Oct 2022 and the stock has since rebounded slightly, Rightmove still trading at a c.15% discount vs pre-COVID levels. While share price levels provide an attractive entry point, this is even more appealing on a forward EV / EBITDA basis where the stock trades close to a 10-year low at c.18-19x.

{kind=link}

NTM EV / EBITDA ((X))

{kind=link}

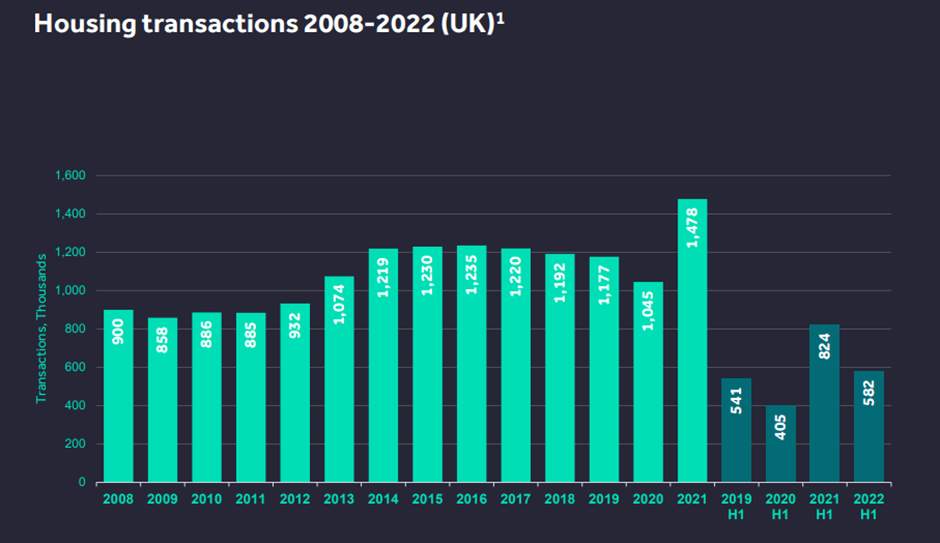

Despite the negative macro environment in 2022 and the rising mortgage rates in the UK, the number of housing transactions that took place in 1H2022 (582), while lower than that in 1H2021, was still c.8% higher vs 1H2019 (541) pre-COVID. There have even been renewed expectations that interest rates on mortgages are expected to fall in the near term after the Bank of England’s recent suggestions that inflation may come under control sooner rather than later. This would naturally lead to a stronger real estate outlook in the country and should translate to a more attractive environment for Rightmove’s business.

{kind=link}

Regardless, even in an inflationary environment, Rightmove is likely to be a net beneficiary. Being 100% digital, there is minimal inflationary pressure on input costs – labour costs likely being the key one. On the flip side, there is arguably more room for revenue growth in an inflationary environment via price increases. While management have said that they don’t think about price increases as a function of inflation (and instead bases this on the value being delivered to its customers), Rightmove is more likely to benefit from an inflationary environment. Given the importance of the Rightmove platform to its customers’ businesses, demand is likely to be price inelastic.

Risks

A prolonged and severe downturn in the UK property market in the coming years could result in a slowdown in the number of housing transactions and force the eventual closure of some agent / developer offices, which would have a negative impact on Rightmove. However in such a scenario, I think it would be likely that agents / developers would look to reduce marketing expenditures in other areas first (e.g. offline spend, online spend on smaller portals with lesser reach), before assessing whether to potentially reduce visibility on such a large platform like Rightmove. Smaller players would also have less resources needed to get through such a difficult period and could result in Rightmove gaining market share against its competitors in a downturn.

Conclusion

Fundamentally, Rightmove has a very attractive business model with strong economic moats. The recent macro headwinds have provided an opportunity for a cheap entry point to the stock despite the company likely being a net beneficiary in a market downturn. It has fully recovered from the underperformance seen during COVID and has financial performance has surpassed pre-COVID levels (e.g. EBITDA now higher) but its share price remains below pre-COVID levels. The high cashflow-generative nature of the business combined with management’s historical willingness to return capital to shareholders makes this a highly attractive situation.

For further details see:

Rightmove: A High-Quality Business At An Attractive Entry Point