RTMVF - Rightmove: Magical Margins Drive Value

2023-04-18 14:18:53 ET

Summary

- Rightmove plc is a UK-listed business that operates property portals in the UK and internationally.

- Rightmove has grown quickly due to the digitization of the industry, product expansion, and the superiority of Rightmove's platform.

- Short-term headwinds are present but mortgage rates have likely peaked.

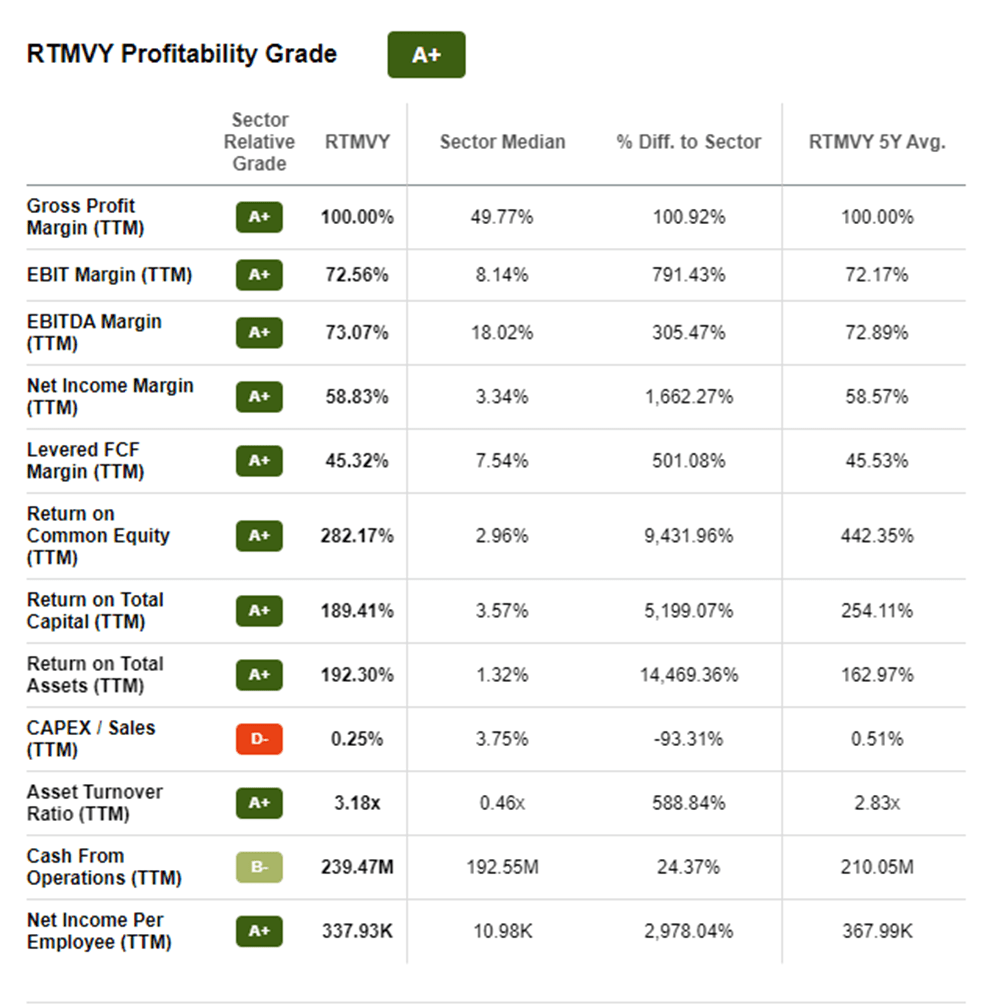

- Margins are fantastic, with Rightmove achieving an EBITDA-M of 73% and a FCF-M of 45%. Dividends and BBs should grow healthily long-term.

- Our DCF valuation suggests an upside of 14%.

Company description

Rightmove plc ( RTMVY ) is a UK-listed business that operates property portals in the UK and internationally. Its Agency segment provides advertising services for property resale and letting, along with tenant references and rent guarantee insurance services to landlords. The New Homes segment offers property advertising services to new home developers and housing associations. The Other segment provides advertising services for overseas and commercial properties, as well as mortgage services and non-property advertising and data services.

Share price

Rightmove's share price has trended upward in the last decade, consistently gaining as the business has grown. There has been some volatility, as the company's fortunes are tied to the health of the UK housing market, which has been impacted by such events as Covid-19 and rising rates.

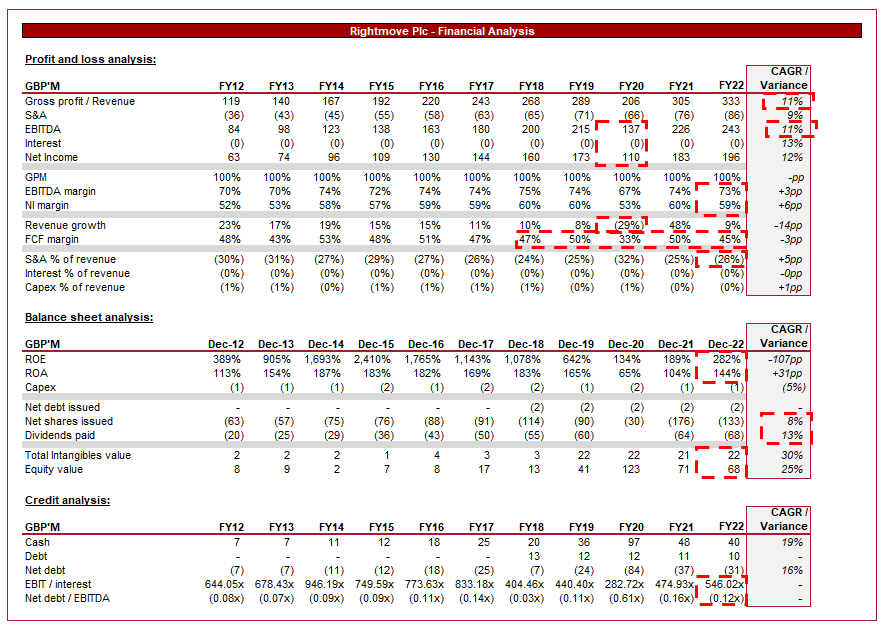

Financial analysis

{kind=link}

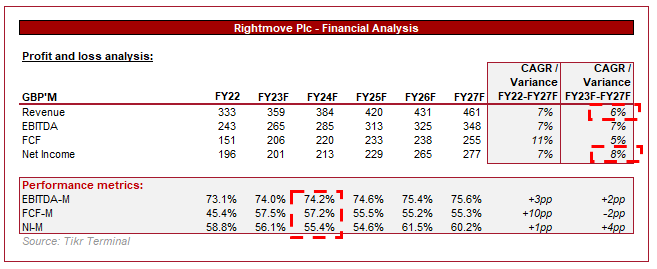

Presented above is Rightmove's financial performance for the last decade. We are very impressed by the company's accretive growth.

Revenue

Revenue has grown at a CAGR of 11% across the last 10 years, driven by both market factors and innovation from Rightmove.

One of the key trends impacting the property industry is the shift toward digitalization. Consumers are increasingly opting to use online portals to search for properties, benefiting from the convenience of browsing at home. Rightmove has revolutionized the industry in the UK, investing in its platform to make it user-friendly and offer a seamless experience. The old real estate model was far more time-consuming for buyers, as it involved speaking to numerous agents to find all the properties available on the market. The best form of innovation is giving consumers what they want, not trying to convince them of what they need. Although we have referred to this as a trend, the market has fundamentally shifted and will continue to do so toward Rightmove.

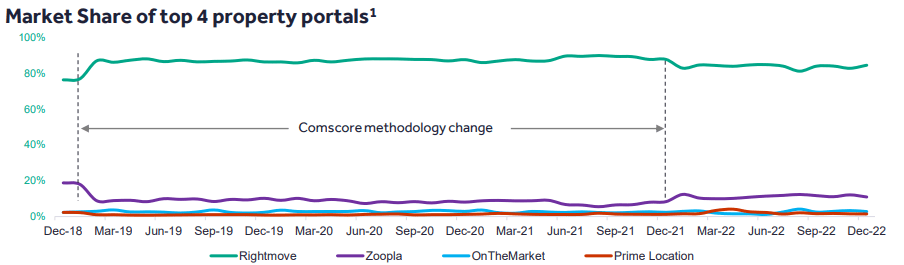

We have also seen growth in the rental market in the UK, with home ownership becoming increasingly difficult for the younger generations. Further, we are seeing growing demand for flexible, short-term rentals, as a greater number of people seek flexibility due to lifestyle/work. Rightmove has looked to increase its exposure to the rental market also, allowing landlords to list their properties to both students and the wider public. This allows Rightmove to monetize accommodation regardless of whether a property is purchased or not. As the following data illustrates, Rightmove continues to grow its market share.

Rents (Rightmove)

AI and machine learning is both an opportunity in the market and an area of expertise. Rightmove has invested in technology which enables it to provide personalized recommendations to users based on their current searches and pre-defined criteria. The company is also developing other tools such as a way to provide estimate valuations, property risks, and investment opportunities.

A key factor driving revenue is Rightmove's superior offering, which is a combination of the factors we have stated above, as well as consumers voting on what they believe to be the best option to use. As the following chart illustrates, Rightmove has by far the largest market share in the market. This is important to us as the investment proposition here is essentially a marketing business and so it is key to bet on the correct horse, as there are no assets to fall back on.

{kind=link}

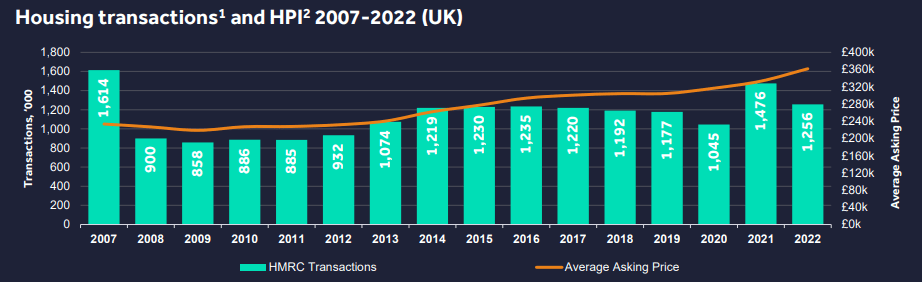

The COVID-19 pandemic has also had a significant impact on the property industry, contributing to an initial decline in volume. Rightmove was hit hard by this, experiencing a 29% decline in sales. However, the number of app visits remained strong and the subsequent housing boom drove a rapid recovery.

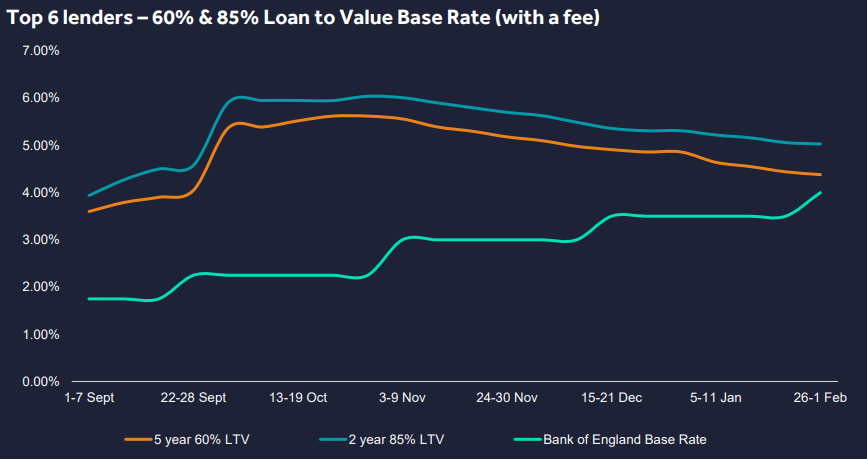

We are currently experiencing difficult market conditions with rates continuing to rise and consumers seeing a decline in their discretionary income. These are difficult conditions to transact in and so it is unsurprising to see many consumers avoiding the market. With this, we have seen house prices continue to fall, experiencing the largest decline since 2009 . Context is key, however. We saw an unprecedented run-up post-COVID and so seeing a correction from this is not unusual.

Further, there is evidence to be hopeful. Despite rates rising, the UK fixed mortgage market is continuing to see product rates decline, likely due to falling uncertainty around how rates will move in the medium term.

{kind=link}

Regardless, the industry is cyclical in nature and so investors will need to accept that they will face slowing conditions as economic conditions change.

Looking long-term, the key driver will be continued health in the UK property market. Many might be questioning this with Brexit and continued weakness across Europe but we are less bearish. The UK housing market has shown itself to be robust for longer than most countries. The GFC is the closest the market came to destruction, yet all major cities have exceeded their pre-GFC ATHs, with London bouncing back within 3 years. This is a stark contrast to countries like Spain and Italy, which still has non-performing properties to this day that are in negative equity. One of the reasons the market is so robust is due to the homeownership and landlord culture in the UK, which acts as a price support against shocks. If economic conditions are difficult as they are currently, Brits stop selling and defer buying. This might sound bad for Rightmove but long term it is good, as it means we do not see wild swings in market prices which can impact confidence in the market.

{kind=link}

{kind=link}

Revenue growth opportunities beyond the UK will come from overseas expansion, with Rightmove offering properties overseas as part of their current product suite. This is not necessarily something that is focused on currently but allows more wealthy individuals to find properties. The scope here is that it can become an offering for the masses, although might be difficult for Rightmove to understand each market's local dynamics, as well as gain market share from the current players. Our view would be to focus on a niche rather than attempting to enter any of these markets.

{kind=link}

Margins

Rightmove has seen impressive margin improvement across the historical period, gaining 3ppts of EBITDA and 6ppts of FCF. This has been driven by superior pricing as the business has developed its market-leading position, as well as sales mix in recent years. As the following illustrates, New Homes have been the main contributor to growth in H2 2022. This segment generates greater ARPA and thus has been more greatly accretive for the business.

APRA Agency and New Homes (Rightmove) APRA Agency and New Homes (Rightmove)

Balance sheet

Moving onto the balance sheet, we see how truly asset-light this business is. It continues to generate wild efficiency returns, with a ROE of 144%.

Management has been active with distributions to shareholders, growing dividends at a rate of 13% and buybacks at 8%. Our view is that this should be sustainable going forward.

Rightmove is also conservatively financed, with minimal debt utilized. This gives the business flexibility should market opportunities present themselves.

Outlook

{kind=link}

Presented above is Wall Street's consensus view on Rightmove's coming 5 years.

Revenue is expected to grow at a rate of 6%, representing healthy growth but below what it has achieved historically. This is more of a reflection of the business being more mature now, with far less market share to take. Our view is that this is attractive.

Margins are expected to improve further, which is surprising given the level they are already at. This is a reflection of improving transaction economics and continued rising home prices. We are not pricing this in but see the possibility of continued expansion.

Peer comparison

{kind=link}

Presented above is Rightmove's profitability compared to a cohort of communication services businesses. The industry as a whole is highly competitive, with the average margins in the industry reflecting this. Only 20 of the 253 businesses have an A+ rating and Rightmove is one of them. The key is how efficiently the business translates its income to FCF, essentially incurring some operational payroll costs.

{kind=link}

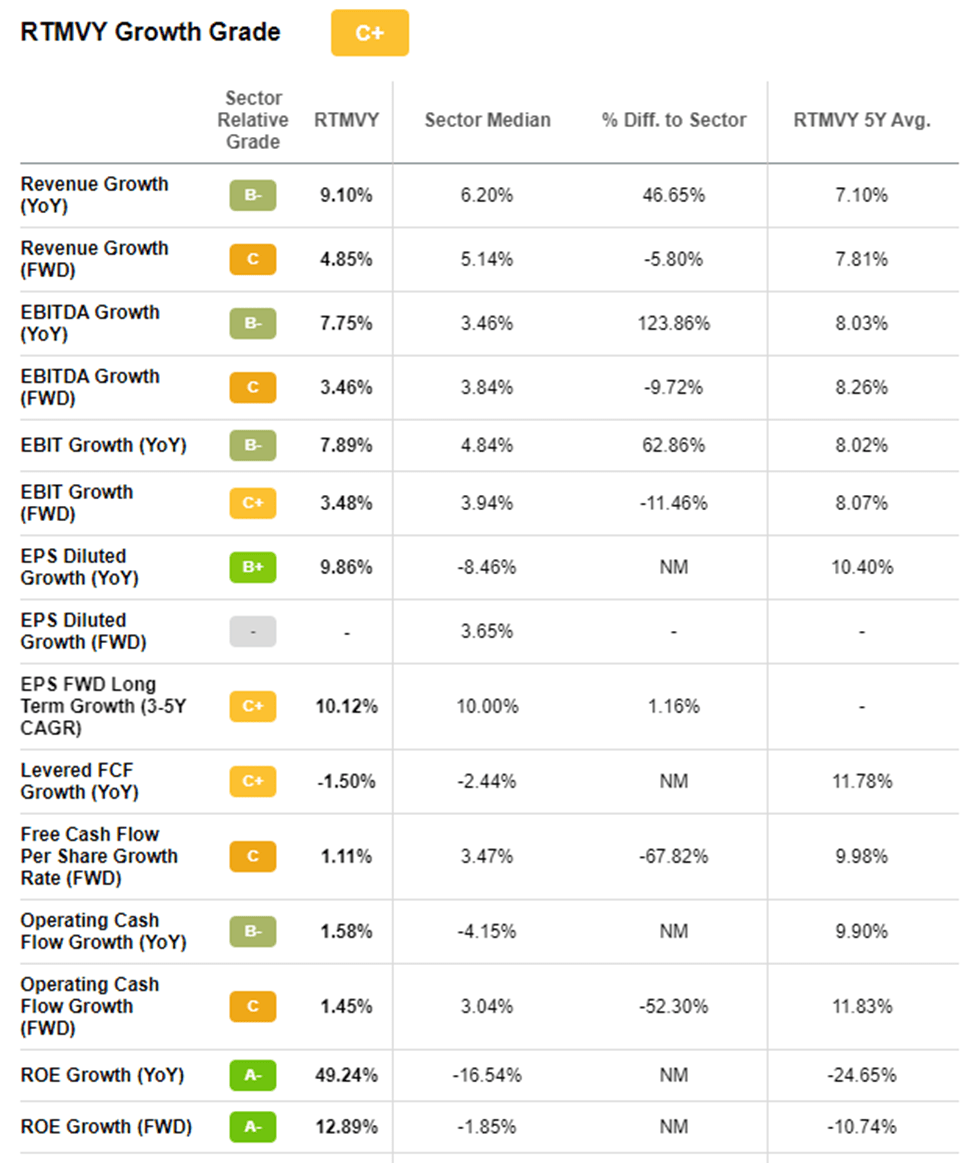

Growth does not score as well but is nonetheless great in our view. Rightmove still outperforms the sector on all key metrics.

Valuation

{kind=link}

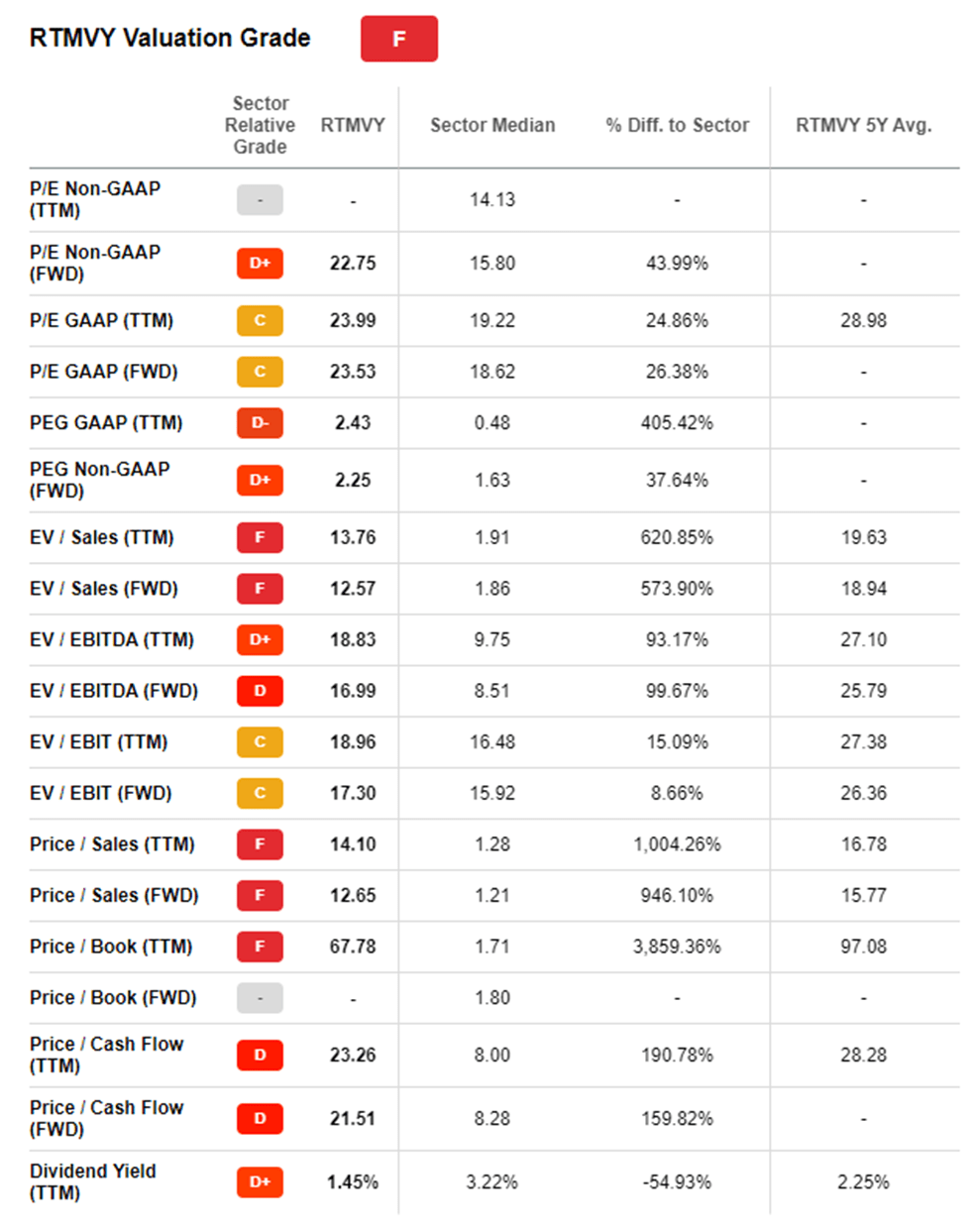

Given Rightmove's superior financial performance, it is unsurprising to see the business trading at a premium to its peers. Things rarely come for free in this world. Our view is that a large premium is justified on the profitability alone, given the level of revenue that flows straight to cash returns. To more reliably estimate its value, we have conducted a DCF valuation of the business, with the following key assumptions:

- Flat year in FY23, followed by growth in the range of 3-7%.

- FCF conversion of 47-49%.

- An exit multiple of 23x, a discount rate of 9%, and a perpetual growth rate of 2.5%.

Based on this, we derive an upside of 14%, although consider our assumptions to be on the conservative side.

Final thoughts

Rightmove is a fantastic business. It has created a service that consumers want to use while developing an attractive monetization model. The commercial prospects of the business and the UK stack up, which should see growth continuing in the coming years. Margins do have the possibility to expand but we are not pricing this in. Key risks are short-term in nature and cyclical. Our valuation suggests a 14% upside from here.

For further details see:

Rightmove: Magical Margins Drive Value