RTMVF - Rightmove: Weakened End Market No One Is Talking About

2023-11-29 03:53:47 ET

Summary

- Rightmove has historically been heavily reliant on ARPA hikes to drive top-line growth.

- Calls with experts, channel checks, and our internal analysis have revealed holes in this model going forward.

- Consensus has yet to price in this future weakness, leading to meaningful opportunity for underperformance.

Core Story

At first glance, many long-term value oriented investors may find it difficult to get around a short investment on Rightmove [LSE:RMV] ( RTMVF , RTMVY ), given that it possesses qualities of a fundamentally good business, such as strong network effects along with low leverage, high margins and great free cash flow conversion.

While we do not disagree that RMV ticks multiple boxes of a great business, we believe that it does not serve as a great long-term investment. This is because the strengths of the business are known by every single covering analyst and investor out there, so it is very likely that these fundamental strengths are already priced in to the current share price.

Historically, RMV has returned over 1,000% to its shareholders.

Yahoo Finance

However, digging into the numbers reveal that their growth story has been one that was largely driven by rapid Average Revenue Per Advertiser (ARPA) hikes rather than by Memberships Growth (which has remained relatively flat)

Company Reports

We believe that this is a cause of concern as a growth story that is driven by pricing is almost never a good thing. In fact, I think that RMV is approaching a very real upper bound in its ARPA and that small agent churn is going to approach an inflexion point (within the next 1.5-2 years). The combination of these two factors will cause RMV to see fundamentally weaker growth prospects compared to what consensus is currently underwriting , leading to continued consensus underperformance going forward, catalyzing downward movements of the share price toward what we believe to be the true intrinsic value of the company.

Business Model

Rightmove is the dominant property listing portal in the UK with an estimated ~84% market share as of 1H FY23 , generating ~ 72% Operating Margins and ~56% Net Income Margins. They make money through 3 key ways, which are:

Firstly, Agency Revenue, which can be broken down into Agency Subscribers x Monthly Agency Average Revenue Per Advertiser (Agency ARPA) x 12 months. This comprises by far the largest proportion of the company's total revenue at ~73%. This driver is where our variant view comes into play and is where our largest delta versus consensus comes from.

Secondly, New Homes Revenue, which can be broken down into New Home Developers x New Homes Monthly ARPA x 12 months. This comprises 17% of the company's total revenue. We will not be taking a variant view on this segment and will be projecting in-line with consensus.

Finally, Other Revenues, such as Third-Party Advertising, Data Services, Tenant Services and Mortgages, make up 10% of the company's total revenue. We will not be taking a variant view on this segment and will be projecting in-line with consensus.

Industry Overview

To better appreciate what truly drives our thesis points, it is crucial to develop a deeper understanding of the Real Estate Agency Industry in the UK, as it is these estate agencies that drive revenue for RMV's business.

Office for National Statistics

Office for National Statistics

Over the past few years, the UK Estate Agency Industry has been seeing an increasing composition of small estate agencies that make <100k GBP/annum, as growth of these agencies have been outpacing that of larger estate agencies. Consequently, small estate agencies have an increasingly large role to play in driving RMV's revenue.

Moreover, the UK Estate Agency Industry is also characterized by a lack of entry barriers, as no formal qualifications are required to become an estate agent . This leads to a lack of agent sophistication, which leaves them unable to properly measure the ROI of listing their properties on RMV.

Internal Analysis

A simple unit economics analysis also reveals that economics are currently heavily skewed toward larger estate agencies, as these players have leverage with RMV and are able to negotiate significantly more favorable terms, leaving smaller, independent agencies at an incredible disadvantage.

Finally, another important thing to note is that given the proliferation of property listing services amongst real estate agencies in the UK (which often takes up a sizable portion of the agents' total costs), there is incredible incentive to consolidate as larger players can fold up the RMV contracts of the smaller players that they acquire into the same subscription, leading to immense cost savings. In fact, calls with industry experts (sign-in required) reveal that they expect the share of large agencies to quadruple over the next five years, from ~5% today to ~15% by FY27. As consolidation occurs, we should expect to see an uptake in agent churn from RMV as these contracts will be cancelled.

Estate Agency Dynamics Do Not Support The ARPA Growth Runway Embedded In Street Expectations

Sell-Side Reports

At the moment, the street believes that RMV has sizable headroom for agency ARPA expansion going forward, mainly by arguing that RMV's current take rates of ~6% (% of total commission pool) is still premature and can see further expansion (by ~2x) to up to ~13%, which is what REA Group (ASX:REA, one of Australia's most dominant property listing portals) currently charges.

Property118

However, our analysis confirms that this belief is overly bullish as Australia's agent monetization premium can largely be explained by their structurally higher commission rates (~5.7% in AUS vs. ~1.5% in UK). We believe that agents in the UK are fundamentally unable to charge meaningfully higher commission rates on a property transaction, as the glut of small agencies with no unique selling point (USP) leads to competition by price, while historical rise of online agencies such as Purplebricks that charge razor thin commissions of <1% have further dragged down the bottom end of the industry (small estate agencies).

Internal Analysis

Moreover, digging deeper into the numbers reveals that in reality, small estate agencies in the UK are already being heavily monetized, with take rates going up to a staggering ~31% of their total commissions. This greatly surpasses the theoretical 13% goal lauded by the Sell-Side, telling us that these small agents are being placed under immense levels of financial strain.

Foxtons Company Report, Expert Calls

The only reason why total take rates remain at a "low" 6% is because of the larger agencies in the industry that are able to not only negotiate preferential pricing with RMV, but also spread out the subscription charges over a larger base of commissions given their larger scale of operations. Using estimates gathered from expert calls with the Head of BD at Foxtons, we were able to obtain an estimate for how much Foxtons pays RMV per branch, which we note is a significant 48% discount to the average ARPA charged by RMV. We do not see meaningful monetization opportunities possible with these large agencies given that they serve as "anchor tenants" and have significant leverage when negotiating pricing with RMV.

As a result of our observations, we believe that there is negative delta to be observed in terms of agency ARPA from what the Street is currently underwriting.

Rightmove's Small Agent Base Is At An Understated Risk Of Churn

Given Rightmove's strong retention rates over the years, the Street appears to be extrapolating from past performance and is underwriting strong retention rates going forward. We hold a differentiated view as we believe there is evidence to suggest that small agent churn is approaching an inflection point, which will lead to a significant drop in agency branch numbers and hence negative delta versus consensus expectations.

We observe that over the past few years, amidst a growing UK estate agency industry (in terms of total number of estate agencies), RMV's rapid ARPA expansion growth strategy has caused them to lose share amidst agents. We believe that this is a reflection of agents increasingly perceiving RMV as a less essential service.

Company Reports, Internal Analysis

Moreover, channel checks have revealed to us that sentiment towards RMV is high (agents discontent has mainly been linked to the unjust pricing hikes that RMV has implemented), with an estimated 85% of the agent base resenting RMV. Some findings from our channel checks that stood out were:

Forum Checks

Facebook, Property Industry Eye

We believe that RMV may not have the well-being of their agents as a key priority and seem to be aggressively implementing ARPA hikes in a bid to maximize profits. If RMV continues on this path, we could see a significant number of agents churning from their platform towards a competitor.

The discontent by small agencies towards RMV is further exacerbated when we consider how small agents are not engaged with on the same frequency by RMV's account managers as compared to larger estate agencies. It is important to note that this was different from the past where every customer was spoken to at the very least once every 3 months or so.

Tegus

Moreover, there has also been a high rate of turnover amongst account managers at RMV, which has made it even more difficult for the company to establish strong and long-lasting relationships with small estate agencies.

Next, thinking about what the next best alternative for agents is, we looked to experts once again and found that Zoopla actually provides (sign in required) significantly higher value, charging ~? of RMV's price, but offering higher lead quality, ROI, and higher levels of agent friendliness, losing out only in terms of brand reach.

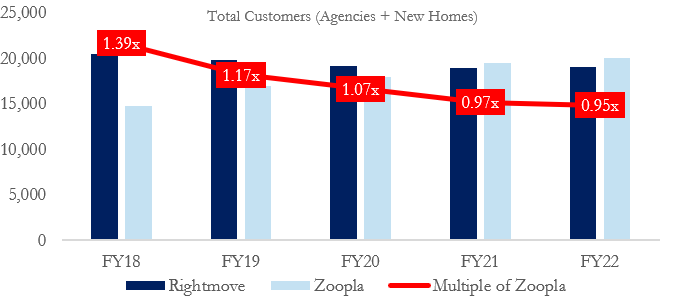

In fact, looking at the numbers, we see that Zoopla was able to surpass RMV in terms of the size of their customer base back in FY21, and the gap has been widening ever since. Zoopla's growing customer base gives us conviction that more agents are increasingly appreciative of the value that Zoopla provides, and are able to see themselves surviving without RMV's services.

Company reports, Zoople press releases, Internal Estimates

{kind=link}

While it may be difficult to ascertain when exactly the exodus of RMV's small agent base will occur, we believe that it will likely occur in the next 1-2 years based on our internal calculations as continued ARPA hikes by RMV will drive small agent profits to a level below the minimum wage-level in the UK, providing a heavy incentive for them to leave the platform.

Internal Analysis

Base Case Valuation

For our valuation we used a DCF model, at a 9.1% WACC (in-line with consensus) and have identified the key points of differentiation we have from the Street (for our base case). We believe that underperformances of these metrics relative to expectations will place downward pressure on share prices.

Internal Analysis

In terms of Agency Branch numbers, we project them to largely be in line with consensus until FY24 as agent frustration continues to build up to unsustainable levels. In FY25, we expect to see significant churn in small estate agencies as many of them reach their breaking points given RMV's continued aggressive hikes, leading to significant negative delta going forward.

Internal Analysis

With regards to Agency Monthly ARPA, we expect it to grow in line with consensus until FY25 as RMV continues its aggressive ARPA hikes to drive going forward. From FY26 onwards, we underwrite significant ARPA contraction as RMV desperately attempts to attract back the churned agencies, leading to negative delta versus consensus.

Internal Analysis

The revenue variance seen above is largely driven as a function of the delta we have in terms of agency branches and agency ARPA, leading to lower than expected agency revenues. On the other hand, New Home Developers Revenue and Others Revenue are simply projected to grow in-line with consensus as we do not have a variant view on these segments and believe that current consensus estimates are reasonable.

Internal Analysis

Consequently, as a significant component of RMV's costs are tied to investments in portal upgrades and labor (both of which should continue to grow at historical rates going forward), Operating Margins going forward should contract due to revenue drop-throughs.

Ultimately, underwriting an Exit P/E multiple contraction to 20.0x due to fundamentally weakened growth prospects and a conservative perpetual growth rate of 2.0%, we arrive at a base case target price of 419.9 GBX, representing a 16.8% upside.

Risks

Recognizing both the inherent risks and potential catalysts is paramount for making well-informed decisions that help us to maximize value. A key risk to consider would be a pivot in the company's business strategy towards charging estate agencies on a per listing basis, balancing out their unit economics.

However, there has not been any mentions by management about the possibility of such a strategy occurring. Such a strategy will likely be unpopular with the larger estate agencies like Foxtons who serve as "Anchor Tenants" that help the company attract smaller agencies. Consequently, the likelihood of a significant shift in the company's business strategy is low, leading to a sustained imbalance in unit economics.

Catalysts

Going forward, key catalysts that would cause the share price to revise downwards would be underperformances in Agency ARPA and Agency Membership numbers in upcoming earnings calls.

Conclusion

To conclude, we believe that while RMV possesses qualities of a fundamentally strong business, these strengths are common knowledge amongst possibly the entire investing community and is likely to have already been priced in. What we are playing for is an overstated ability to continue hiking ARPA along with an underlooked risk of their core small agent base churning from their platform due to insights we gained through our primary research (expert calls and channel checks with small estate agents).

Ultimately, given that our argument is largely driven by personalized insights we gleaned through expert calls and conversations with small estate agents in the UK (which is non public information), we think that investors should exercise discretion and make their own judgements when it comes to evaluating this opportunity. A potential way to do so would be by keeping track of small agent sentiment on RMV by looking at various property forums and facebook pages while also keeping an eye out for developments that could alter the competitive dynamics within the property listing industry in the UK and weaken RMV's dominant positioning.

Editor's Note: This article was submitted as part of Seeking Alpha's Top 2024 Long/Short Pick investment competition , which runs through December 31. With cash prizes, this competition -- open to all contributors -- is one you don't want to miss. If you are interested in becoming a contributor and taking part in the competition, click here to find out more and submit your article today!

For further details see:

Rightmove: Weakened End Market No One Is Talking About