RMNI - Rimini Street: Cheap For A Reason

2023-09-20 18:00:00 ET

Summary

- Rimini Street has a history of legal issues and copyright infringement lawsuits with Oracle, posing significant legal risks.

- The company has demonstrated solid financial performance, with revenue compounding at 23.5% over the past decade and improving profitability metrics.

- Despite its attractive valuation, the legal risks and potential damage to the company's reputation make it too risky to invest in Rimini Street.

Investment thesis

When I started my analysis of Rimini Street ( RMNI ), I thought I had found a hidden gem with a massive upside potential. Revenue compounded at 23.5% over the past decade, and profitability metrics have steadily improved as the business scaled up. But then I discovered a major reason why the stock is so cheap. Rimini faces massive legal risks and has a "rich" history of litigations related to intellectual property infringement. The company has already lost several courts to Oracle ( ORCL ) since 2010 and lost a lot of money and massive attorney's fees. That said, I would not recommend investing in the stock and assigning it a "Hold" rating.

Company information

Rimini Street, Inc. and its subsidiaries are global providers of end-to-end enterprise software support, products, and services. RMNI offers a comprehensive family of unified solutions to run, manage, support, customize, configure, connect, protect, monitor, and optimize clients’ enterprise applications, databases, and technology software platforms.

The company's fiscal year ends on December 31 with a sole operating and reportable segment. According to the latest 10-K report , the company generated about 47% of its sales in FY 2022 outside the U.S.

{kind=link}

Financials

The company demonstrated a solid financial performance over the past decade, with annual revenue compounding at a staggering 23.5%. As the business scaled up, profitability ratios expanded substantially. Wide and consistently improving gross margin allows RMNI to effectively balance between reinvesting in growth and sustaining a wide free cash flow [FCF] ex-stock-based compensation [ex-SBC] margin.

{kind=link}

The FCF margin has been consistently positive over the past five years, which means the company has built a strong balance sheet. RMNI is in a solid net cash position with healthy liquidity metrics. The company does not pay dividends and rarely conducts stock buybacks. Given the ability of the company to deliver strong revenue growth and profitability improvement, I think that allocating spare capital to reinvest in business is sound.

Seeking Alpha

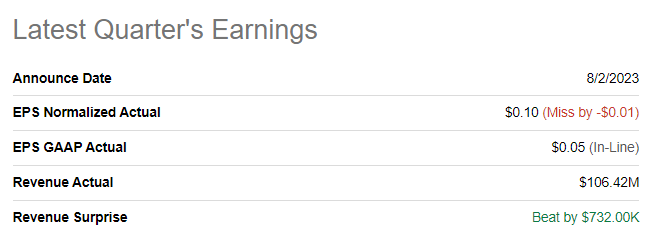

The latest quarterly earnings were released on August 2, when the company topped consensus revenue estimates but missed in terms of the EPS. Revenue grew 5.2% YoY, and the adjusted EPS expanded from $0.07 to $0.10. The gross margin has been flat YoY at 63%, and the operating margin expanded by more than 150 basis points.

{kind=link}

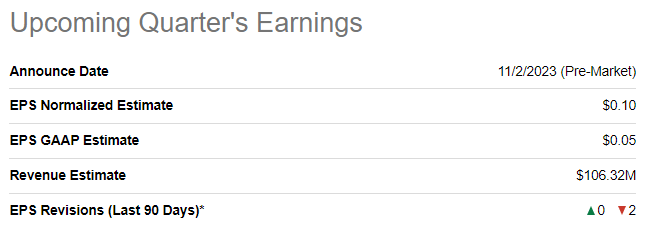

The upcoming quarter's earnings are expected to be released on November 2. Quarterly revenue is expected by consensus at $106 million, which indicates a 4% YoY growth. The adjusted EPS is expected to be flat sequentially at $0.10.

{kind=link}

It might seem that Rimini is a hidden gem, but I have to disappoint my readers. The company has a "rich" history of litigations. Since 2010, the company and its CEO have been involved in continuing litigation with Oracle. Rimini paid almost $90 million to Oracle in 2016 since the company was found liable for "innocent" copyright infringements. The most recent lawsuit also related to copyright infringement from RMNI. In July 2023, Oracle won another case, meaning the court confirmed allegations about Rimini's misconduct again. I think that Rimini's track record of litigations means that legal risks are vast, and its attractive valuation is explained by it. Apart from potential requirements to pay substantial amounts of money to Oracle and attorneys, these litigations limit the company's ability to grow.

Being found guilty of intellectual property infringement severely hits the company's reputation, meaning customers might discontinue operations with Rimini. Having a bad reputation also means it would be harder to attract new customers. That said, the company faces substantial risks of revenue declines and profitability shrinkage in case of major customer loss.

Valuation

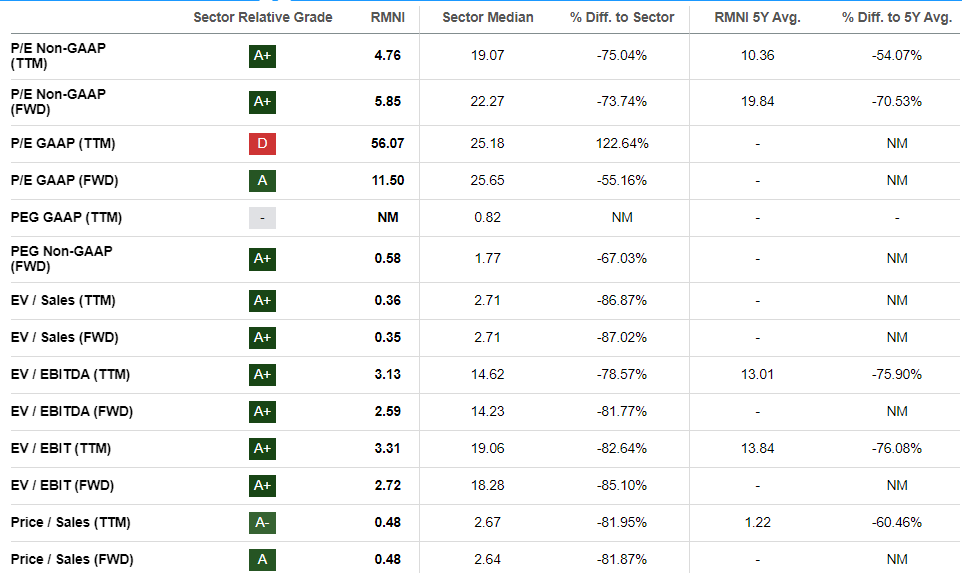

The stock almost halved year-to-date, significantly underperforming the broader U.S. market. RMNI, at the moment, trades almost five times lower than its all-time high achieved in Autumn 2021. Seeking Alpha Quant assigns the stock the highest possible "A+" valuation grade because current multiples are substantially lower than the sector median and historical averages.

{kind=link}

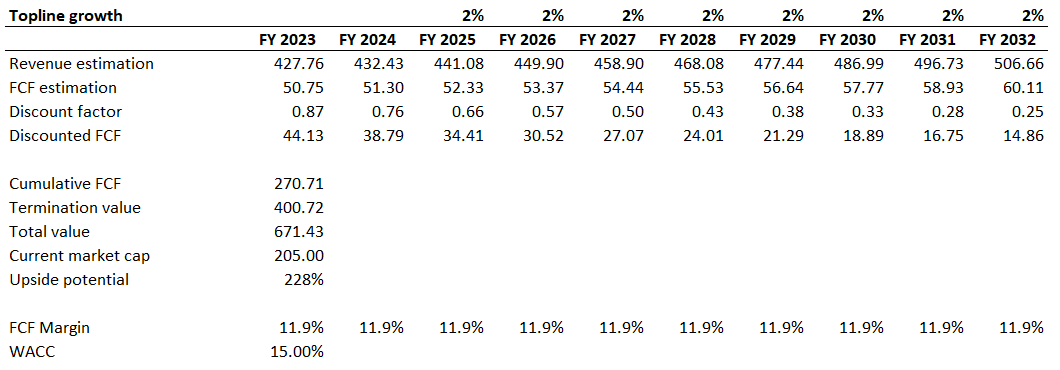

Since RMNI is a growth company, I want to proceed with my valuation analysis by simulating the discounted cash flow [DCF] model. Due to the company's small scale, I use a substantial 15% WACC for discounting. I have consensus revenue estimates available for the upcoming two fiscal years and project a meager 2% revenue CAGR for the years beyond. I use the last five years' FCF margin ex-SBC for my base year and expect no expansion in the future.

{kind=link}

According to my calculations, the business's fair value is $671 million, which means the stock has the potential to more than triple. However, it is crucial to emphasize that my valuation analysis only considers quantitative factors, while qualitative ones are ignored. It looks impossible to me to reliably calculate a provision related to the company's massive legal risks. But the financial effect of litigations might be massive, and the company admitted in its latest 10-K report that it might run out of liquidity as litigations drain the company's pockets. That said, the dirt-cheap valuation looks fair, considering the elephant in the room.

Risks to consider

Apart from the substantial legal risks, which I described in the "Financials" section, the company also faces significant foreign exchange risks as RMNI generates about half of its sales outside the U.S. Unfavorable fluctuations in foreign exchange markets would adversely affect the company's earnings.

The company faces fierce competition since the business model is asset-light and does not require major capital expenditures. That said, barriers to entry are very low, and the company's solid profitability metrics suggest that the niche will be attractive for new players.

Bottom line

To sum up, I do not recommend investing in RMNI and assigning the stock a "Hold" rating. While financial performance has been solid and profitability metrics are wide, the company's history of litigations related to copyright infringement suggests it is highly likely that impressive profitability metrics were achieved at the cost of the company's reputation. Legal risks are substantial, and a history of losing courts to Oracle suggests that Rimini's approach to business was indeed not legally acceptable. Therefore, I would ignore RMNI's attractive valuation because legal risks are difficult to quantify and incorporate into my valuation analysis.

For further details see:

Rimini Street: Cheap For A Reason