HPK - Ring Energy: Strategy Shift

2023-11-23 06:40:47 ET

Summary

- Ring Energy is changing its strategy to grow through acquisitions as a way of reducing the debt ratio to acceptable levels.

- Management believes that the debt ratio needs to be in the 1.0 to 1.3 range for the stock to break out of its current range.

- Vital Energy successfully implemented an accretive transaction strategy to reduce the debt ratio to acceptable levels.

- HighPeak Energy faced challenges with debt refinancing due to intolerant market conditions.

- The sale of stock by Warburg Pincus is something that management can do nothing about. Therefore, the debt issue is the one to resolve.

I have previously discussed the situation that Ring Energy ( REI ) has been in several times ever since fiscal year 2020 changed the rules for the oil and gas industry. The focus on free cash flow remains. What is changing is how (the strategy shift) to get that free cash flow. Management is now going to grow by acquisition as the route to get that free cash flow has been closed to this company as it has been closed with the whole industry. So far, the deals that have been done have been excellent. But the key to survival is to do enough of them so the company gets out of the debt straight-jacket. It is therefore a very big deal that management is facing that issue. Depending upon the execution of this strategy, there could be considerable recovery potential to the stock.

Management's Changing View

This management (when I talked to investor relations), like many managements I follow, is concerned about the undervaluation of the stock. But since 2020 when it was readily evident that price-earnings ratios had collapsed (after a very trying 2015-2020), really much of the industry faced the same issue. The key question is what can be salvaged while reducing the debt ratio. Management may have tried to salvage too much which resulted in not enough deals.

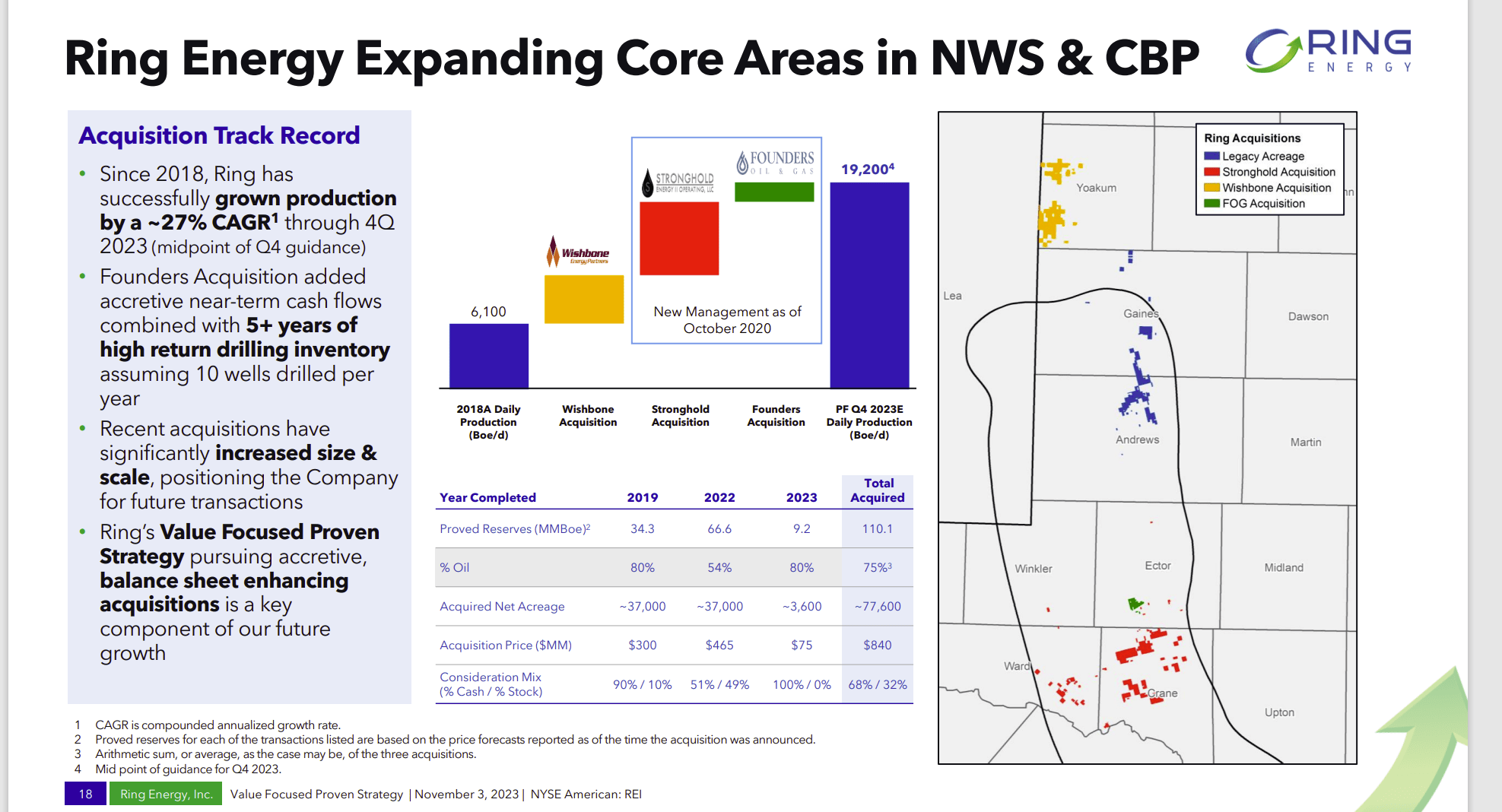

Ring Energy Recent Acquisition History (Ring Energy Corporate Presentation Third Quarter 2023)

{kind=link}

The big deal here is that management has now embraced accretive balance sheet enhancing transactions as noted in the lower left-hand corner. This strategy (at least so far) has prevented the debt ratio from heading back to where it was in the past before fiscal year 2022 gave that ratio a large helping hand.

As a quick aside, the current quarter (where oil prices did rise for a bit) may likely boost cash flow to also help debt repayment progress. This buys management still more time to resolve the issue. Management believes that the debt ratio needs to be in the 1.0 to 1.3 range for the stock to break out of the current range.

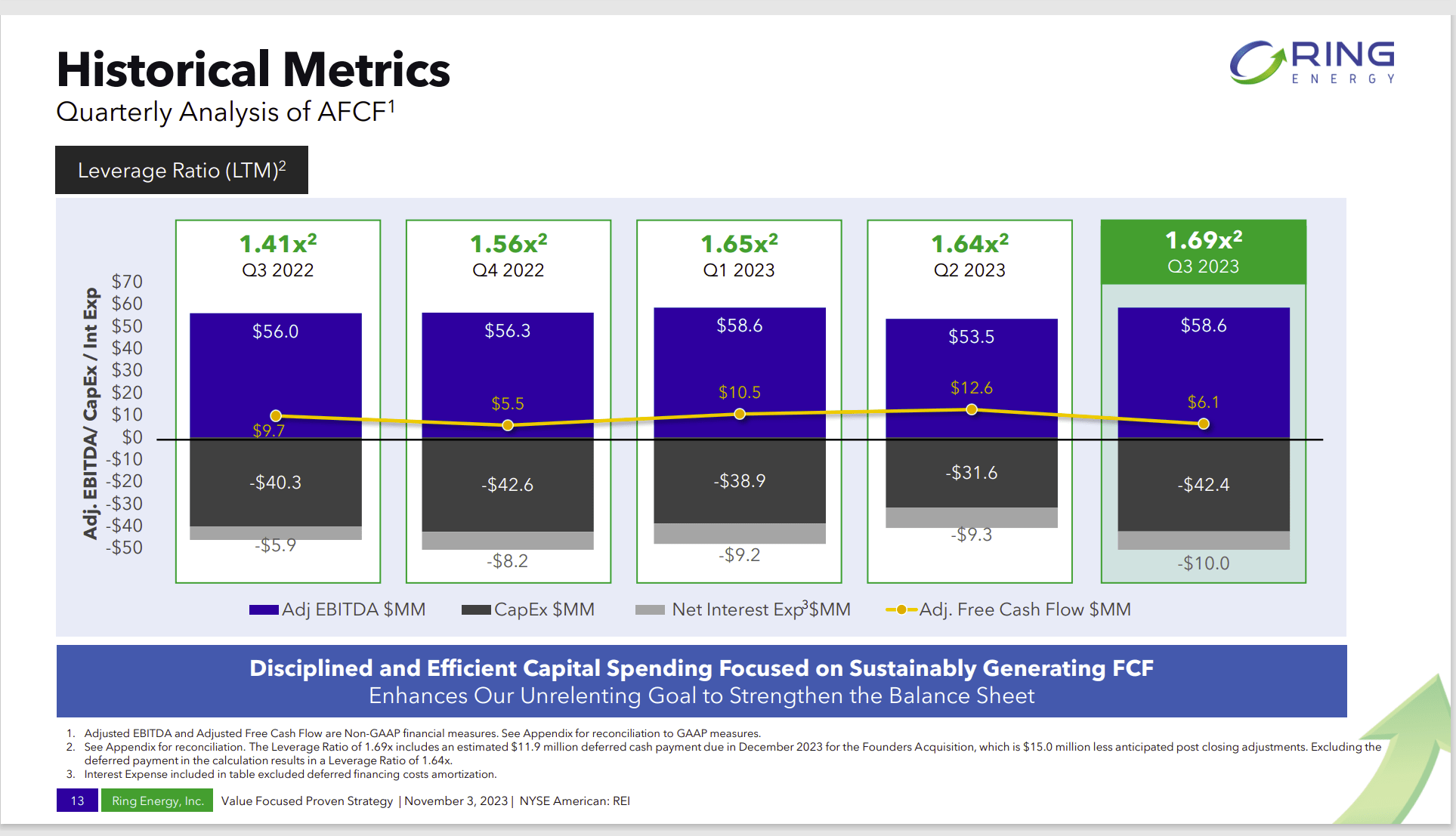

Ring Energy Historical Debt Ratio And Free Cash Flow Since The Second Quarter Of Fiscal Year 2022 (Ring Energy Corporate Presentation Third Quarter 2023)

{kind=link}

The latest acquisitions including one that used a fair amount of stock enabled the debt ratio to essentially stabilize as shown above. That is definitely an accomplishment in the eyes of Mr. Market. But the challenge remains in the eyes of Mr. Market.

What may need to happen is some flexibility regarding the undervaluation of the stock. That may make it easier for management to make accretive transactions in the future. There needs to be a realization that the undervaluation will not be resolved unless more accretive deals are made.

Therefore, the reserves behind each share of stock may have to be disregarded up to a certain point until that debt ratio is where it meets both debt market and stock market demands. Otherwise, even shareholders will not be beneficiaries of the current valuation.

Vital Energy

Here is a company that was in a far better position to ignore the reserves behind each share that handicapped previous management from gaining that necessary free cash flow. The idea behind the history here is that sometimes you have to give up some of what you have as a shareholder to get anything back (distasteful as that may seem).

It is definitely not "fair" in that someone changed the rules while the "game" of growth was being played. But some days, business rules are just not fair.

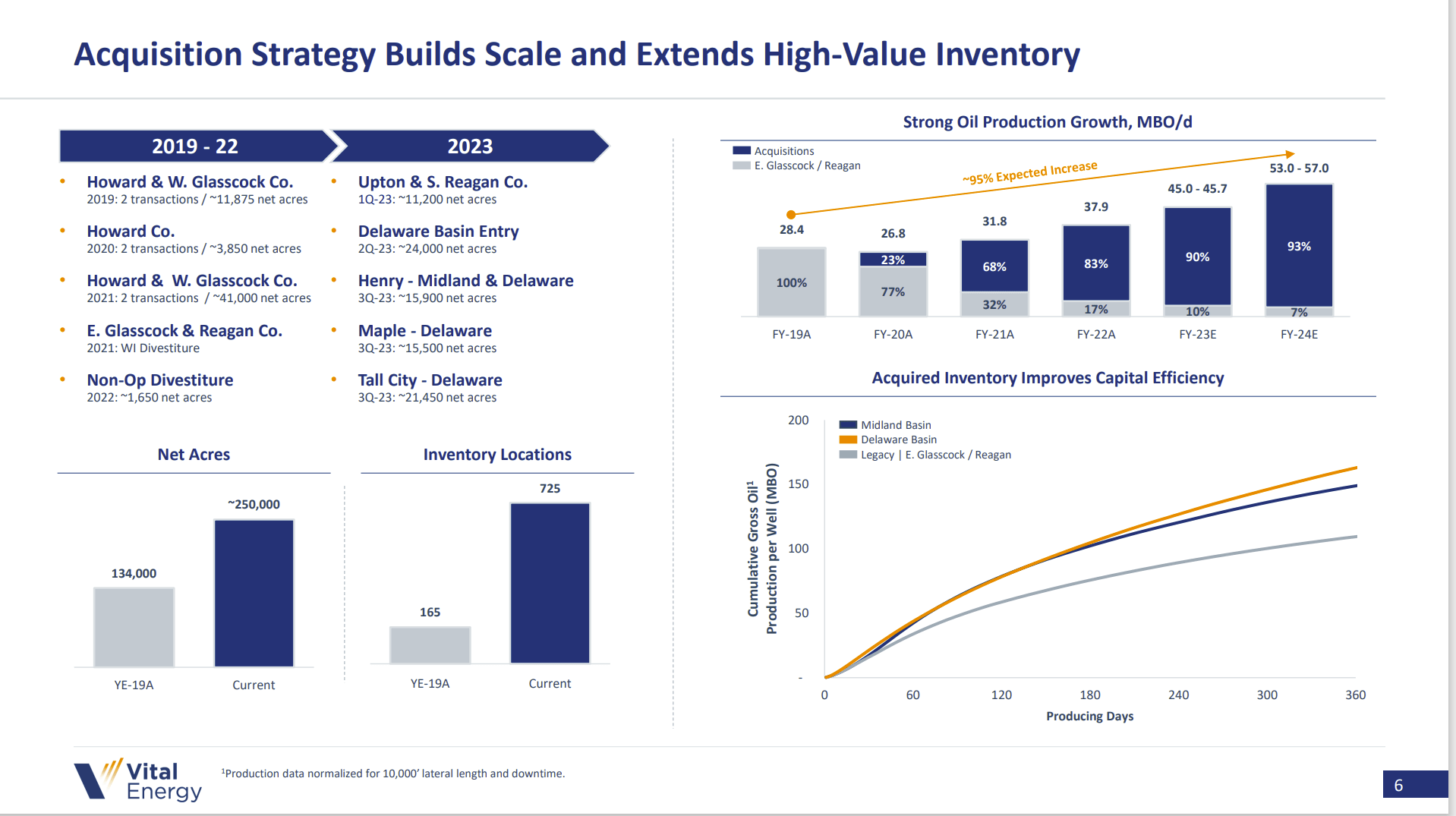

Vital Energy History Of Acquisitions Including The Latest Three Done All Together (Vital Energy Third Quarter 2023, Earnings Conference Call Slides Third Quarter 2023)

{kind=link}

Vital Energy ( VTLE ) began with small acquisitions a few years back as soon as new management "came in the door". The reason for this was that the previous management had a reserve-based strategy and periodically sold what was developed (while keeping a certain amount of production to grow) to keep the debt down. The period 2015-2020 put an end to that idea.

Previous management had been successful with companies before the current company was shown the door. But with negative cash flow, the current management needed to get to work "yesterday". Clearly, they did.

As I noted before, the focus was on accretive transactions with the value of the stock used in these transactions a secondary consideration. This allowed cash flow to grow considerably.

After all, it is hard to argue that the stock is undervalued when the stock market is not going to change its attitude towards the company's stock until the company management fixes the problem. It was admittedly an easier position for a company with a lot of gas reserves to take. Ring Energy has oil reserves and so may be in a tighter spot. The solution in the eyes of the market may still be the same though.

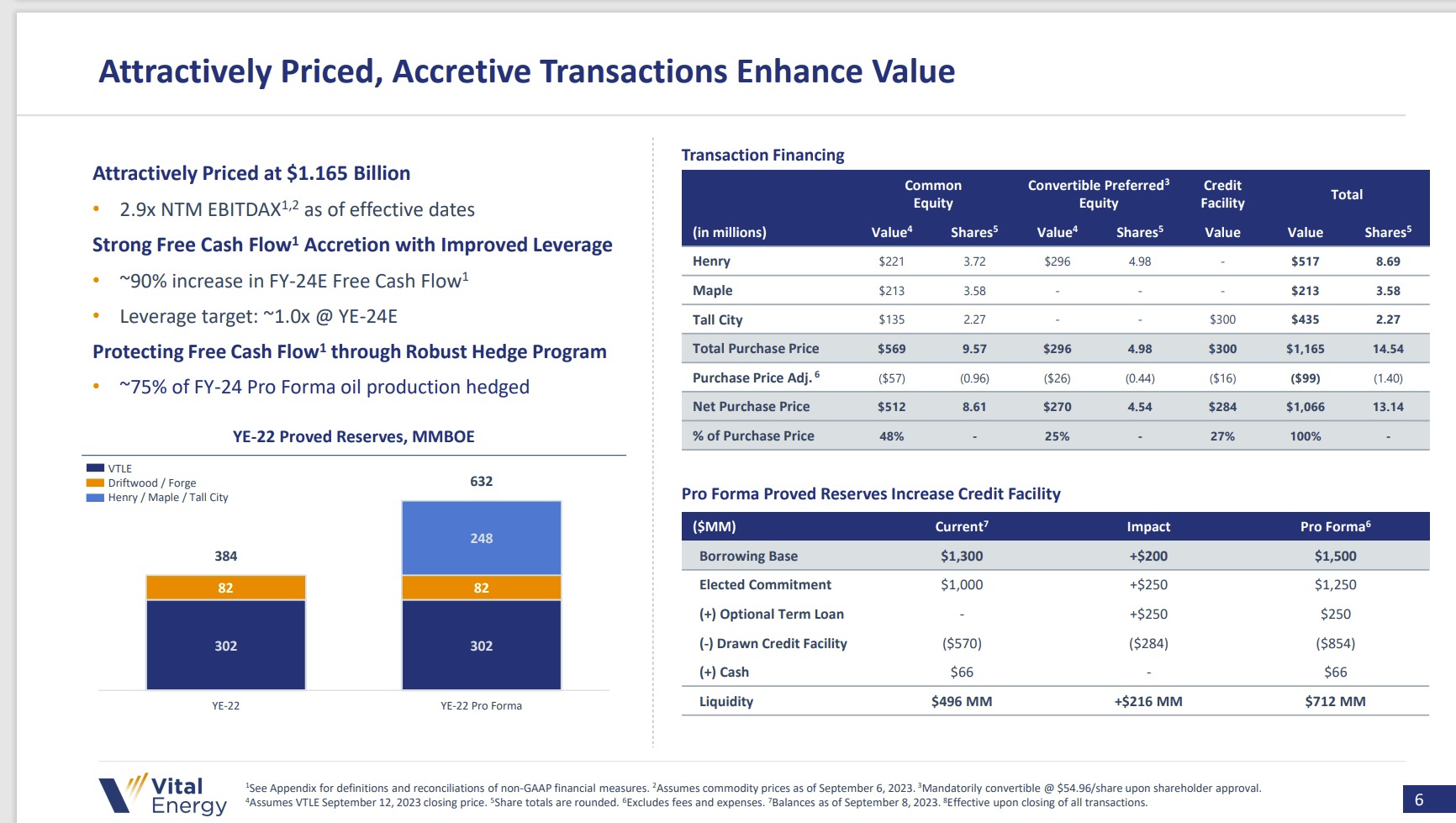

Vital Energy Acquisition Presentation September 2023 (Vital Energy Acquisition Presentation October 2023)

{kind=link}

All the previous acquisitions enabled management to do the acquisitions above for stock. The goal here was to basically issue enough stock that management put that the market and shareholders would see a debt ratio of 1.0 using assumptions acceptable to the stock market. That puts an end to the debt issue for this company. (Note that two acquisitions closed, and the preferred stock issued until shareholders voted to make more stock available has now been converted.)

Comparably Ring Energy is in the early stages of the acquisition program. Management has dipped its toe into the pathway that Vital Energy took. Now it needs the nerve to go further along this pathway realizing that this is the only way to get any undervaluation back. This also means that the chances of shareholders realizing part of the undervaluation are heavily dependent upon the ability of management to do deals.

Admittedly, it is a slippery slope and shareholders could end up with a viable company at the current price and no undervaluation. It happens. Now that is better than no company (which is a big risk in the next cyclical downturn). But it is reasonable for shareholders to expect a better result without constraining management to the point where enough progress is not being made. This is currently a buyers' market by most accounts. Therefore, any possible deals are not likely to get better.

Not doing anything more by not using Ring Energy stock could well consign the stock to its current price for a long time (with a significant chance of a worse outcome). The days when the market would allow the company to drill profitable wells using debt until cash flow grew to a decent level are gone. As both managements implied in their slides, you now do deals until cash flow is at a decent level.

HighPeak Energy ( HPK ) just found out the hard way that such a debt laden pathway no longer exists. Fortunately, the company was still able to get a line of credit. But now things need to get back into the mainstream so that the line of credit becomes traditional. Naturally, along with that line of credit came a promise to repay debt. This management got far further with its plans than I expected. So, it is in a better position to repay debt. But the story also serves as a warning that the market is rather intolerant of certain debt ratios.

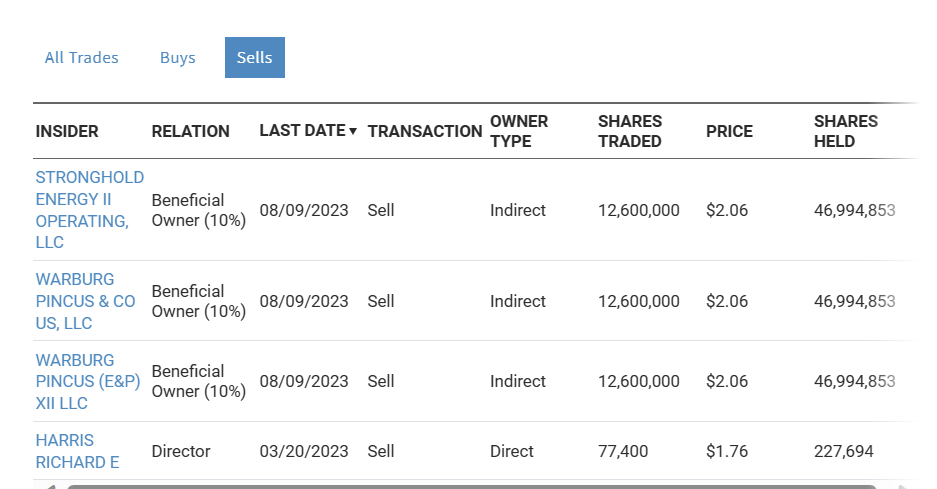

Warburg Pincus

Warburg Pincus and some of the associated (managed) funds have representatives on the board of directors of Ring Energy. The sale of stock by these entities has caused some concern among Wall Street Analysts.

Ring Energy Summary Of Warburg Pincus & Associated Entity Sales (NASDAQ Website November 22, 2023)

{kind=link}

Forgotten in all this concern is that any entity that receives stock will likely cash in some of the stock to meet its own obligations that are really none of the business of the market. It is not necessarily a negative vote on the future of the company so much as "business obligations" having nothing to do with the company.

What should instead concern the market is that the representatives of Warburg Pincus still owned quite a bit of outstanding shares as shown above and their representatives are still on the board of directors. Therefore, the interests of this group of entities still is lined up with the common shareholders. Many times, an entity like this can be a positive help for a company that needs to make deals. Still there is a risk that the situation will not help the stock price long-term.

Key Takeaways

There seems to be a shift in management strategy of Ring Energy to follow others that are successful in getting out of the debt straight-jacket. The key is to do enough transactions fast enough that the company can adequately get through the next inevitable cyclical downturn.

Most companies I follow that fail, do so because they don't do enough transactions to "get going". The transactions that are done are good transactions that benefit shareholders. But not enough means there is too much debt when hostile conditions arrive in this low visibility industry.

The very first slide to me means that management is beginning to face some very tough decisions about the ability of the company to thrive as it once did. But that same management cannot take too long or the ability to make accretive deals will be gone.

Ring Energy management has clearly improved the company finances, or the debt ratio would not have had the muted response to lower oil prices earlier in the fiscal year. Now it may be time to do more of the same sooner than later to head to where Vital Energy got to very quickly. That goal is the ability to forecast a debt ratio in the 1.0 to 1.3 range with a promise to take it lower in the future. Keeping what undervaluation, you can, through good deals is the tricky part.

Management indicated to me that the debt issue and the stock sales are foremost on the mind of Mr. Market. But it will likely be up to management to do something about the debt issue. The stock price will likely take care of itself as the debt issue gets resolved.

As far as the stock sales, any owner of the stock has a right to sell whenever it wants to. Warburg Pincus has a finite number of shares to sell. Therefore, the problem will resolve itself at some point. Management really cannot spend time on something it cannot control no matter how material that issue may appear to be.

Any success in further lowering the debt also brings shareholders closer to the recovery potential of the stock. EQT ( EQT ) is probably the furthest along in this strategy. By all accounts the strategy is complete with the stock more than doubling from its lows. It looks like there is more to come for EQT shareholders as well. Ring Energy shareholders have to get there to "done" first. I have a lot of faith that this management will get to "done".

For further details see:

Ring Energy: Strategy Shift