RTNTF - Rio Tinto: Healthy Dividend Yield Attractive Valuations

2023-07-19 15:21:08 ET

Summary

- Multicommodity miner Rio Tinto hasn't had a great 2023 in the stock markets, which is expected in the current macroeconomic context.

- Its financial performance weakened in 2022 and has likely continued to do so in H1 2023, results for which are due soon, and beyond, for the next couple of years.

- But its stock price has over corrected in my view, especially given its healthy forward dividend yield and long history of paying dividends.

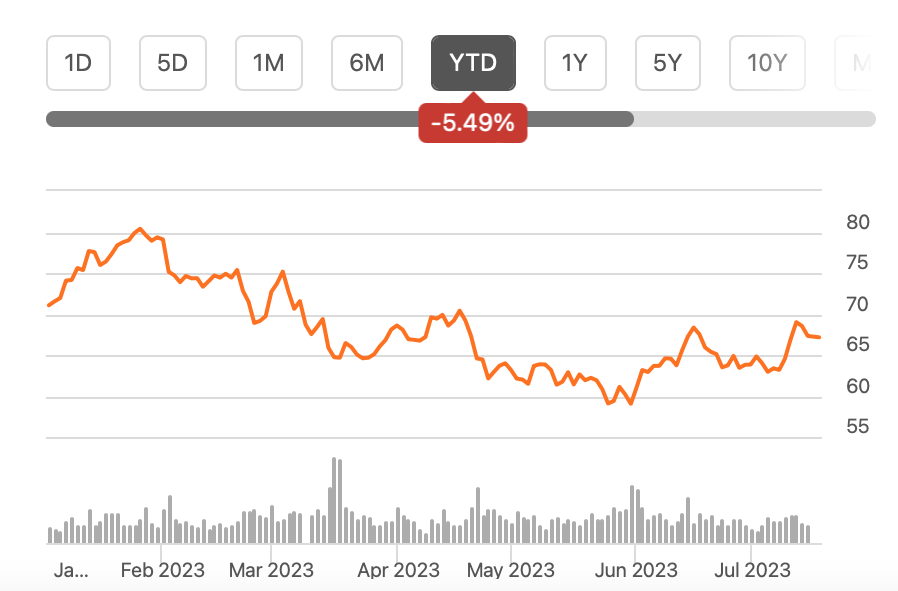

The British-Australian multicommodity miner Rio Tinto's ( RTNTF ) ( RIO ) NYSE listing has seen a price drop of 5.5% year-to-date. Its pink listing has done slightly better with 1.2% gains, but even that is nothing noteworthy.

With the outlook for miners possibly dim in the current macroeconomic context, it’s not hard to see why. That doesn’t mean that things can’t get better. Recently I looked at its mining peer, Anglo American (NGLOY). Unpacking that story revealed that while indeed it is showing a slowdown, its price has over corrected. Could the same be true for Rio Tinto? Let’s find out.

Price Chart (Source: Seeking Alpha)

{kind=link}

Hefty dividend yield

Before anything else, I think it’s worth pointing out that the true gains from an investment in RIO will only be seen over time. The simple reason is that it is a hefty dividend stock. The company’s trailing twelve months [TTM] dividend yield is 7.3% . And over the last five years, it has been an even higher 10.5% on average. Sure, it’s expected to fall in the next year or so. But even then its forward yield looks good at 6.7%.

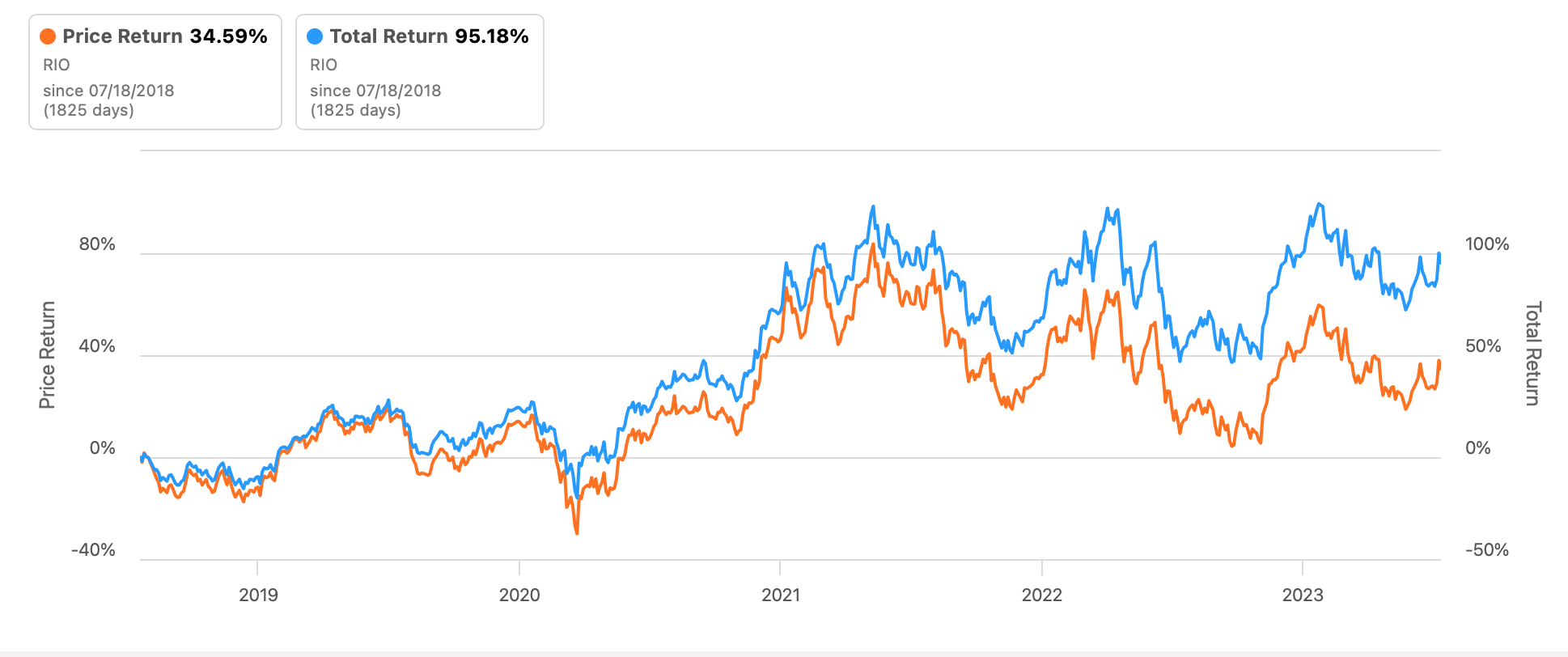

This, of course, shows up in the total returns from the stock. For an investment made in RIO over the past 5 years, the price returns would have been 35% (see chart below). This isn’t the worst in itself. But the total returns at 95% show that it close to doubled investors’ capital over this time, on account of its strong dividends.

{kind=link}

In fact, the company is also committed to paying dividends, not having skipped a beat over the past decade. It has even paid special dividends four times in this time period. In other words, I think it is one to consider a long-term passive income investment, that has a likelihood of price gains over time too.

Financials set to weaken further

The one aspect of dividends that does concern me, however, is the payout ratio. For 2022, it was at 85.6% , which is the highest it has been since 2013. This would not have necessarily been a challenge if Rio Tinto’s performance were expected to improve this year. It’s not. Analysts expect its earnings to decline for the next two years, before picking up pace in 2025. They are even more pessimistic about revenues, which are slated to fall for the next four years. This means, much of the progress on sales made in the last two years could potentially be wiped out by the end of 2026.

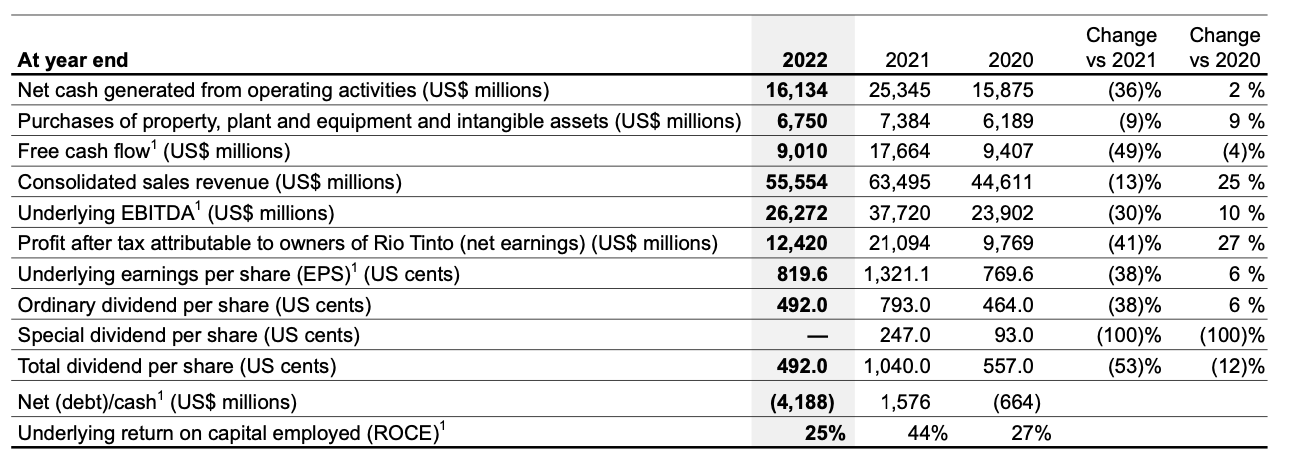

With a slowdown in the developed West and China’s growth not living up to post-lockdown expectations, it’s not hard to see why analysts expect Rio Tinto to weaken for now at least. Weakness was already evident at the end of 2022 when the company reported a 13% decline in revenues and a 38% fall in underlying EPS (see table below).

Key Financials (Source: Seeking Alpha)

{kind=link}

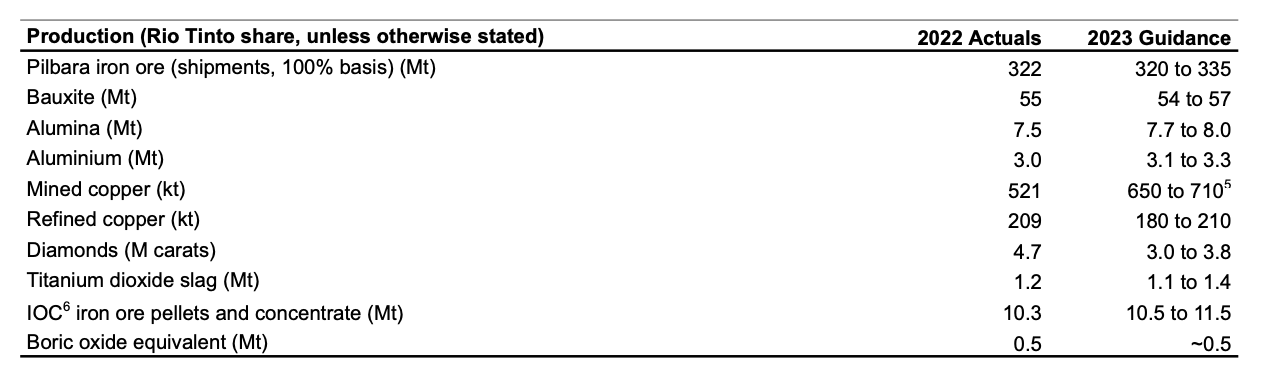

I’m not holding my breath for its first half of 2023 (H1 2023) results due in the last week of July either. Over 84% of the company’s underlying earnings in 2022 came from iron ore, which can be expected to be the driving force for the upcoming numbers too. While Rio Tinto does expect some increase in the commodity’s production (see table below), it is unlikely to make up for the sluggishness in iron ore prices.

{kind=link}

There could be some improvement in the second half of the year, though if China’s expected fiscal stimulus comes through. The country is the biggest global metal consumer, whose inflation levels are so low they might be indicative of a coming slowdown, besides the softer than anticipated real economy indicators. If iron ore prices do pick up, the outlook for RIO can improve.

Competitive valuations

Even at the current and projected performance levels though, it’s interesting to note that the stock looks competitive in terms of market valuations. RIO’s forward price-to-earnings (P/E) ratio is at 8.5x for 2023, which is lower than the 14.3x for the materials sector. It is also lower than the stock’s own average forward ratio for the eight years of 2015 to 2022 of 10.1x.

Similarly, the TTM P/E is at 9x compared to 13.9x for the sector and its own historical average of 11.6x . Based on this, it appears that the stock has an upside of at least 20% right away.

Further, I think the case for a sustained healthy dividend yield is maintained, in line with analysts' forecasts even if the company’s earnings weaken. Even if Rio Tinto decides to reduce the dividend payout ratio to the last five years’ average levels of 61.5%, its dividends for 2023 will still be at $4.6 per share. This means a forward dividend yield of 6.9%, which is in fact even better than what analysts forecast.

What next?

I think there’s a very good case to buy the Rio Tinto stock right now, which is the exact conclusion I came to with respect to Anglo American too. Mining stocks are cyclical by nature. And if they are bought at the bottom of the cycle, the potential gains to be made during an upturn can be significant. RIO has managed to double investor capital over the last five years, in no small part due to its generous dividends. These of course were dependent on healthy financials, with revenues’ compounded annual growth rate [CAGR] over the past five years is a healthy 6.8% and EPS growth at 9.4%.

Even right now, at the relatively weak end of the cycle, RIO’s valuations look competitive compared to the materials sector. Even discounting the fact that some mining stocks are more valued than others right now because of rising demand, like uranium for instance which is seeing rising demand on nuclear energy’s resurgence, by its own historical levels too, RIO looks very attractive right now. Added to that is the relative safety of its dividends. The company’s dividend payout ratio is high, to be sure. But even if it were to drop to more reasonable levels, its dividend yield would continue to look healthy.

It might take some time for the cycle to turn in its favor again, but as the macroeconomic cycle picks up, there will likely be even better times ahead for it.

For further details see:

Rio Tinto: Healthy Dividend Yield, Attractive Valuations