RIO - Rio Tinto: Oyu Tolgoi Ramp-Up Mine To Be Priced In

2023-07-31 12:13:00 ET

Summary

- Rio Tinto released its Q2 production results confirming a solid commodity mix output.

- The company upside is related to organic growth in copper thanks to the Oyu Tolgoi mine facility.

- Guidance was unchanged primarily, and so we confirm our buy rating.

Last week, Rio Tinto ( RIO , OTCPK: RTPPF , OTCPK: RTNTF ) released its second-quarter production results report. After a solid stock price performance recorded in 2022, since our latest publication called " Positive 2023 Start ", Rio Tinto's share is up by an additional 4.56%. Our buy rating is supported by 1) a better commodity EBITDA mix versus BHP Group (BHP) with organic growth in copper, 2) M&A optionality , and 3) a juicy dividend yield that supports our margin of safety combined with a zero debt balance sheet, and 4) more importantly a solid track record in production (you can check our 2022 production analysis releases: Q1 , Q2 , Q3 , and Q4 ).

{kind=link}

Q2 Production Results and Changes

Here at the Lab, we positively view Rio Tinto Q2 performance, even if the company has provided a couple of tweaks. In detail, below are the latest commodity MIX sub-results:

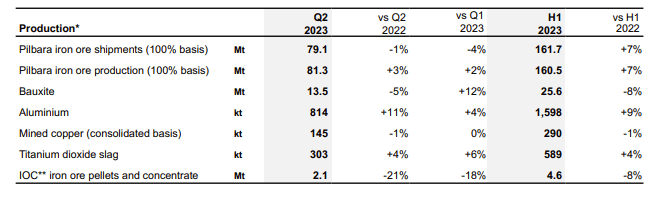

- Pilbara iron ore : shipments were in line with estimates and lower than production. This was due to CAPEX maintenance at Port Dampier and a train derailment . H1 performances were impacted by lower realized iron ore prices ($98.6 per ton versus last year's average of $101.56 per ton);

- Mined copper outcome was higher than Wall Street consensus (production at 145kt vs. 135kt). Escondida mine is still struggling with lower output, but Oyu Tolgoi's ramp-up is well on track;

-

Refined Copper : there was a limited impact on the Kennecott smelter shutdown, expected to last until September. As a result, Rio Tinto lowered the production guidance from 180-210kt to 160-190kt;

-

Aluminum output was up by 11% on a quarterly basis, backed by an ongoing ramp-up at Kitimat & Boyne facility, while Bauxite performance was softer due to rainfall impacts. This is why the company lowered the guidance to the lower-end range target.

Rio Tinto Production in a Snap

{kind=link}

Source: Rio Tinto Q2 press release

{kind=link}

Changes to Estimates

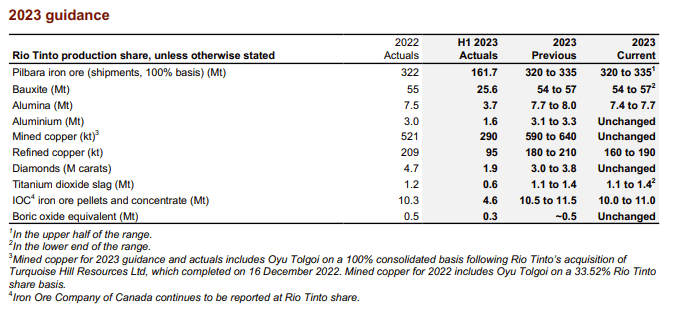

- Here at the Lab, we expect iron ore shipments to be higher in H2 2023, and this is also supported by the company, which increased its internal guidance towards the upper half end. In addition, cost guidance was left unchanged, and so are our estimates;

- Considering the La Granja mine sale , Rio Tinto has an internal cash cow, which we believe is not well priced by the market. According to our estimate, Oyu Tolgoi will provide significant cash flow in late 2024, with an upside risk if performance can be maintained. At the worldwide level, the mine is set to become one of the most extensive industrial copper facilities with 500 ktpa from 2028 and a low-cost curve. Rio Tinto will also diversify its iron ore exposure providing relief on a diversified commodity MIX. In our estimate, the Oyu Tolgoi CAPEX project is budgeted at $7.1 billion, of which $1.4 billion remains to be invested until 2026. In 2025, the new copper industrial complex will represent over 10% of the total group's EBITDA on our internal estimates (over 15% at total capacity with a forecast of $4 billion at the EBITDA level);

- On the negative side, Refined Copper issues will likely result in lower volumes in H2. This is the reason why Rio decided to reduce its guidance and slightly increase its cost basis.

Conclusion and Valuation

With the latest results, we are slightly updating our financial model, reducing our EBITDA estimates. Despite minor changes just related to copper, Rio Tinto delivered a solid performance with a potential upside, thanks to Oyu Tolgoi's underground project ramp-up.

In the quarter, the company had a $0.9 billion working capital higher requirement, and in our estimate, 50% is expected to reverse in H2 2023. At the current spot price, Rio Tinto FCF yield is slightly above 8%, with a forecast dividend yield of 6.11%. Plus, the company is cash positive. This fully supports our buy-rating investment called " Positive Commodity Mix Evolution ."

Indeed, continuing to value Rio Tinto with a 12-month target price at a 5x EV/EBITDA multiple, we confirmed our £72 target price (A$140 per share). The company is currently trading at an EV/EBITDA of only 4.3x. On the other hand, we remain cautious about the macro evolution and flag potential lower dividend estimates due to the likely increase in CAPEX in the medium-term horizon. In addition, despite the agreement with the Mongolian state, government stability is another factor to consider. As a reminder, Mongolia owns a 34% equity stake in Oyu Tolgoi.

For further details see:

Rio Tinto: Oyu Tolgoi Ramp-Up Mine To Be Priced In