CWYUF - RioCan: A Welcome 6% Distribution Increase

2023-03-06 17:26:42 ET

Summary

- RioCan offers a forward yield of 4.9% following two consecutive annual distribution increases.

- Of its peer group of large TSX-listed retail REITs, RioCan has the lowest payout ratio as well as the lowest yield, highlighting the opportunity for further dividend growth.

- Following a distribution cut of 1/3 in 2020, this second increase is a strong signal the company is executing on its strategy.

- RioCan continues to improve the quality of its portfolio and has positioned itself to reward unit-holders over the long-term.

Author’s note: All figures listed in Canadian currency unless otherwise noted.

Investment Thesis

Regular readers will know that I am a long-term unit-holder of RioCan Real Estate Investment Trust (REI.UN:CA )( RIOCF ). I have shrunk and expanded my position over various stages of the cycle; however, I have owned the REIT continuously since 2007. RioCan is one of the holdings I doubled down on during the height of the pandemic with an average cost of ~$14.

RioCan has been executing on several strategic initiatives that have enhanced the quality of the portfolio. The company’s recent 6% distribution increase is the second in its journey to rebuild investor trust following its 2021 dividend cut. The increase is an indication that the REIT’s strong fundamentals and development pipeline are generating stable, and growing AFFO. I believe RioCan is fairly valued, and it continues to improve the quality of its portfolio.

RioCan recently issued encouraging guidance for 2023 that includes FFOPU of $1.77–1.80, implying 4% YoY growth. This growth is predicated on a 3% increase to SPNOI and development spending of $400–450M.

RioCan has the lowest payout ratio as well as the lowest yield, highlighting the opportunity for further dividend growth.

RioCan Dividend Yield and Payout Ratio (RBC Capital Markets)

For investors seeking growing monthly income, RioCan offers a reasonably-priced option with a nearly 5% yield that has room to grow.

REIT Overview

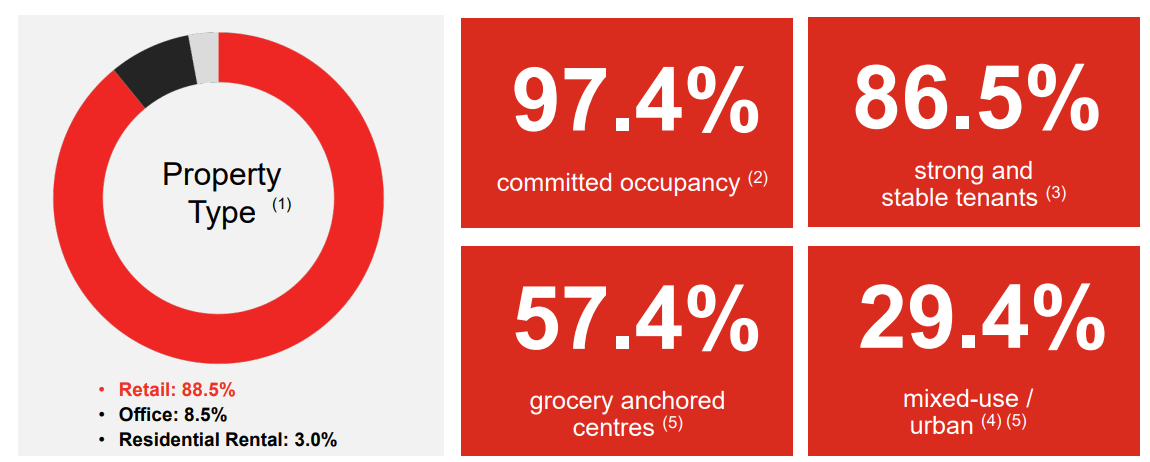

By exiting, its secondary markets, the REIT has substantially completed its shift to focus on major-markets. RioCan now derives 92% of its rental revenue from Canada’s six largest metro areas: Vancouver, Edmonton, Calgary, Toronto, Ottawa, and Montreal. Importantly, RioCan has achieved a significant 53% concentration in North America’s 6th largest metro area, the Greater Toronto Area ((GTA)).

With a focus on large urban centers, RioCan has advanced a development program that combines residential and mixed-use sites in high density, high income urban settings served by mass transit infrastructure. RioCan’s 10 rental residential properties account for around 3% of total NOI. This segment is growing quickly though as residential accounts for 89% of the REIT’s 41,000 sq. ft. of net leasable space in planning and development.

RioCan Tenant Mix and Profile (RioCan Investor Materials )

{kind=link}

RioCan’s tenant mix has deliberately evolved to focus on leases that focus on retail experiences, necessity-based retailers and services and less on big box retail. This has helped to "Amazon-proof" the portfolio and attracted higher quality tenants. For a closer look at RioCan’s operations please see my previous coverage “ RioCan: Building Your Retirement Income ”.

A Growing Distribution

In January 2021, RioCan cut its distribution from $0.12 monthly to $0.08 monthly. This was a move that brought the payout ratio down from around 99% of AFFO to 67% in 2021. Similarly, the forward yield on the REIT dropped from over 8.1% to around 5.4% with the reduction.

With the level of distribution in a more comfortable range, RioCan has been able to resume distribution increases, as SPNOI increases and incremental revenue through development come on line. On February 16, RioCan announced a substantial 6% distribution hike to $1.08/unit annualized payable March 7, for shareholders of record Feb. 28. This follows a similar increase one year earlier when RioCan increased the distribution to $0.085 monthly from $0.08.

The new monthly distribution of $0.09 is well supported with a current AFFO payout ratio of 66% and provides more runway for future increases. RioCan’s recent 2023 guidance suggests an FFO Payout Ratio of between 55% to 65%. RioCan now has a forward yield of 4.9%; a distribution that is 75% of the pre-cut level. As of Q4 2022, RioCan has the lowest payout ratio as well as the lowest yield on its peer group of large TSX-listed retail REITs.

Returning Capital to Unit Holders

During 2022, RioCan repurchased approximately 9.5M units for cancellation at a weighted average purchase price of $21.36 per unit and a total cost of $203.9M. This equates to the repurchase of approximately 3.1% of units outstanding. Funding its growth program, increasing its distribution, and returning capital to shareholders through repurchases represents an ambitious demand on the company’s capital. Achieving all three of these capital priorities in 2022 was enabled by the excess free cash flow made available from the $460M of non-core asset dispositions completed in 2022.

Going into 2023, RioCan renewed its NCIB, to acquire up to a maximum of 30,247,803 units, or approximately 10% of the public float. On the company’s recent earnings call, CEO Jonathan Gitlin confirmed that repurchasing units will not be as significant a priority in 2023 as it was in 2023. So while the NCIB is approved for a large quantity of units, RioCan is likely to use it opportunistically on unit-price weakness.

Risk Analysis

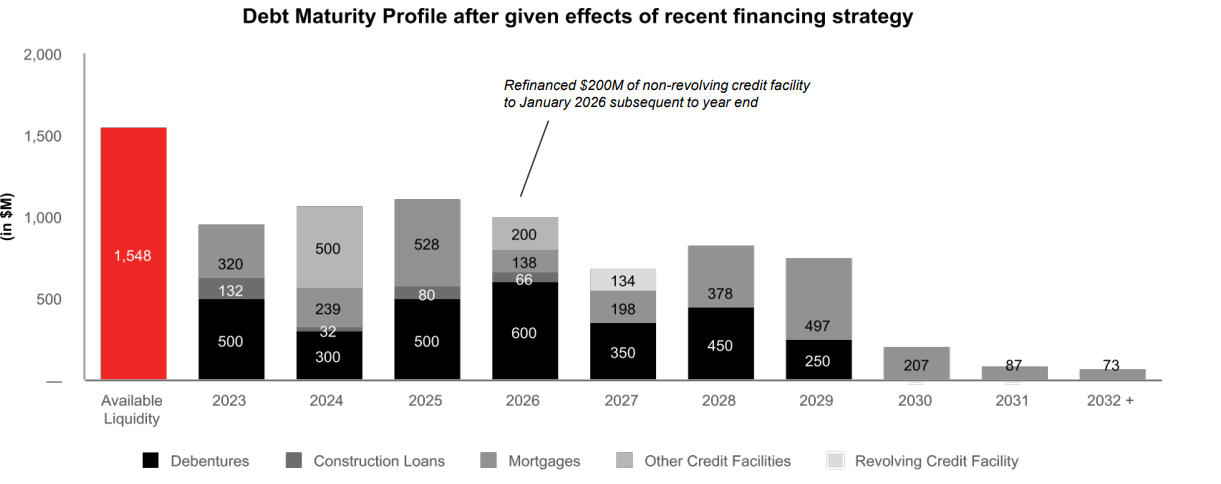

In an era of rising interest rates, its important to look at debt. RioCan’s net debt-to-EBITDA ratio for the full year 2022 was approximately 9.5X, this is ahead of the company’s target of 9X. EBITDA growth from new inventory should bring leverage down to 9X in 2023. RioCan has a liquidity ratio of 22% with $1.47B in liquidity on $6.75B in total debt. The REIT’s Debt/GBV ratio of 45.2% has held steady since 2020. RioCan’s debt maturity profile is well laddered out to 2029 and beyond. RioCan’s current WATM is 3.4 years, below its goal of 5 years.

RioCan Debt Maturity Profile (RioCan Investor Materials )

{kind=link}

There have been a number of retailers announcing closures and bankruptcies in Canada in recent months including Bed Bath & Beyond Inc. ( BBBY ) and Nordstrom Inc. ( JWN ). Fortunately, RioCan is well diversified with no single tenant accounting for more than 5% of NOI. Bed Bath and Beyond, for instance accounts for approximately $8M in revenue, or $0.03 per unit. RioCan’s top ten tenants account for 28.3% of NOI. This compares favorably to other retail REITs: 47.5% for SmartCentres REIT (SRU.UN:CA)( CWYUF ), 72.7% for Choice Properties REIT (CHP.UN:CA)( PPRQF ) and 53.7% for Plaza Retail REIT.

Reasonable Valuation

The resumption and continuation of distribution growth signals to investors that RioCan is back to a growth footing. The REIT’s discount to NAV has shrunk to about 7% recently, while NAV has held steady. This is inline with the large cap retail REIT sub-sector average of a 6% discount. With a P/AFFO multiple of 15X, RioCan is slightly cheaper than it’s peer group at 16X and inline with the REIT's historical average.

Investor Takeaways

RioCan offers a steady and growing monthly distribution. The REIT continues to demonstrate it can execute on its strategy of major-urban market mixed-use residential and retail development. With a best-in-class payout ratio, RioCan has the best propensity for future dividend growth of the large Canadian retail REITs. The REIT’s second distribution increase in as many years underscores the REIT’s commitment to rebuild investor confidence. For investors seeking growing monthly income, RioCan offers a reasonably-priced option and a 4.9% yield.

For further details see:

RioCan: A Welcome 6% Distribution Increase