HIVE - Riot Platforms: Best In Class Bitcoin Miner

2023-10-31 04:14:56 ET

Summary

- Bitcoin miners have outperformed Bitcoin this year, making them a leveraged proxy to Bitcoin, but not all miners are built the same.

- Riot Platforms benefits from power curtailment and selling back to the grid, providing a lucrative hedge against adverse weather conditions.

- Riot's focus on longer-term growth, conservative Bitcoin management strategy, low energy costs, and advantage in the power curtailment market make it a bullish investment.

- Downside factors include: a prolonged halving impacting mining economics, share-based dilution, and a shift in management strategy.

Introduction

Bitcoin miners have outperformed Bitcoin (BTC-USD) this year and have served well as a leveraged proxy to Bitcoin. The price action in June/July was positive following a technical breakout and optimism around the spot Bitcoin ETF being filed by BlackRock . There wasn’t much else to suggest an enormous rally in miners relative to Bitcoin during that period especially as mining conditions remained tough through hot conditions in summer along with record-high network difficulties. As a result, the weak macro environment along with the Bitcoin halving next year being priced in has evaporated all the summer breakout gains for miners including Riot Platforms ( RIOT ). The recent price of Bitcoin breaking above the summer highs has not trickled down into miners meaningfully yet due to a weak equity market and the impact of the halving next year. However, I believe that there are a variety of reasons to stay bullish on Riot namely in the form of a focus on longer-term growth, a conservative Bitcoin management strategy, comparatively low energy costs, and an advantage in the power curtailment market.

The Bull Case

Power curtailment advantage

RIOT benefitted big time from power curtailment and selling back to the grid in the hot summer months, for Q2 they made 10.5m, a 136% increase YoY and represented roughly 25% of their total mining revenue . In August 2023 alone, they made $24.2m from power credits plus another $7.4m in demand response credits due to soaring electricity prices in Texas. They are in a fortunate situation where their cost of mining is one of the lowest at ($8,389/BTC based on Q2 filings) and they can choose to shut off machines and curtail power back to ERCOT when mining economics become unfavourable. Not only does this have a positive impact and helps stabilise energy prices in Texas, but it also adds a lucrative and consistent hedge against adverse weather conditions which would force other miners to operate at a reduced capacity. I believe that this unique position and agreement with the local energy provider could expand further and enable them to receive more power credits as they grow their operations.

Focus on growth and a conservative balance sheet

Riot announced the acquisition of 33,280 MicroBT immersion cooled miners in June 2023 at roughly $22 per Terra Hash adding a further 7.6 E/Hs to their fleet, bringing a total of 20.1 EH/s once fully deployed in 2024 making them one of the highest listed miners only behind Marathon Holdings and having one of the best fleet efficiencies within the industry at 26.5 J/TH. They also have the option to purchase an additional 66,560 at the same price which could bring their total hash rate to 35.4 EH/s in 2025.

The investment in immersion cooling technology will also serve better in harsher summers, especially for Riot who are solely based in Texas where weather conditions in summer can be harsh. The larger investment upfront in building out immersion cooling technology will mean that the replacement cycle of their machines can be extended by up to several years (typical depreciation schedule is four years) especially as Riot has the optionality to turn off machines in hot conditions and generate revenues through power curtailment.

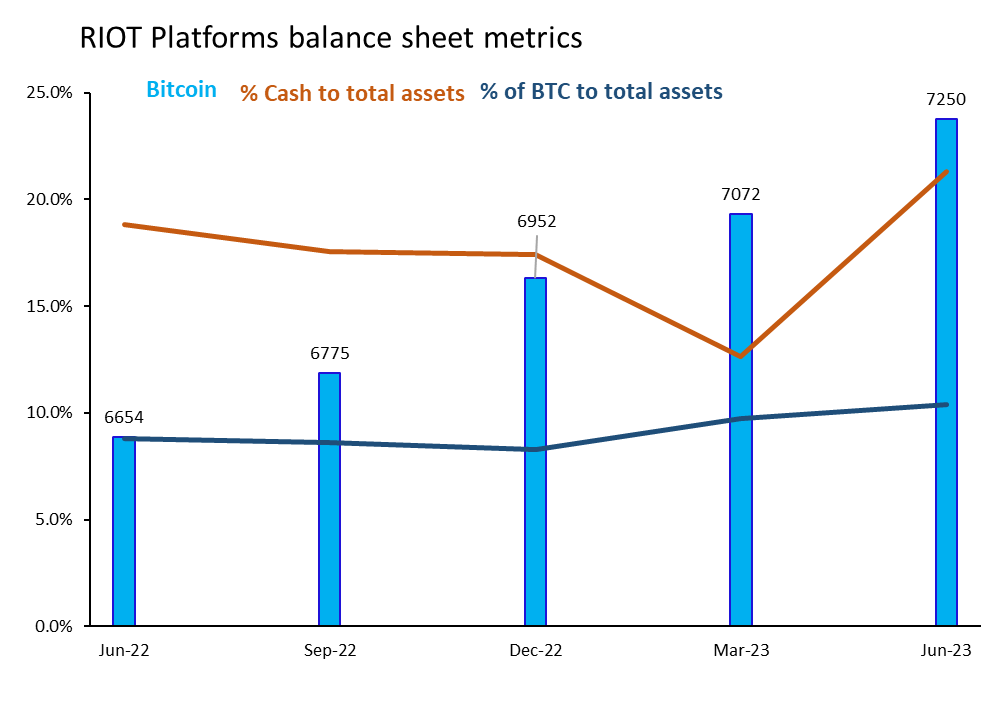

Riot is one of the more well-capitalised miners with little debt, a cash balance of $289m, and a comparatively healthier balance sheet than other miners. Riot has maintained a cash balance of at least 15% in the past year of declining Bitcoin prices suggesting that they have ample liquidity on hand during times of market downturns, I would expect this to remain the case throughout the Bitcoin halving period as operating conditions get tougher (more on this below). Nevertheless, they have also maintained about a 10% Bitcoin to total assets position which I consider a healthy amount. The reason is that their balance sheet is better insulated from volatility in Bitcoin prices which could otherwise have a material impact on impairment charges if they instead chose to hold higher Bitcoin balances. Year-to-date, they have been selling most of their monthly Bitcoin production (at least 85% each month this year) which I believe is prudent as you are essentially dollar cost averaging into spot Bitcoin prices and eliminating price risk.

{kind=link}

Focus is on Bitcoin and not AI

As it stands, Riot’s sole focus is on Bitcoin only; 75% of its revenue comes from mining, 10% from hosting, and 15% from engineering. With the recent boom in AI, other miners such as Hut 8 ( HUT ), HIVE Digital ( HIVE ), Applied Digital ( APLD ), and Iris Energy ( IREN ) are trying to pivot into High Performance Computing which has much higher capex requirements and unproven revenue potential thus far. Not only this, converting mining into AI data centres is much more challenging as these GPUs are more sensitive to dust and debris which could compromise machinery. AI warehouses also get much warmer than Bitcoin mining so accommodating for cooling is a bigger challenge, especially in summer. Miner’s pivoting into AI will also essentially have to compete with all-sized hyperscalers and although they might offer shorter-term contracts of between 3 to 12 months, the sustainability of operations is questionable. In addition, the wave of AI is much more difficult to extrapolate in the medium to long term as TSMC indicated earlier this year . Personally, I think that the pivot into AI is a long and challenging road, and, in my view, this puts Riot ahead of other miners as they are insulated from movements in AI and purely focused into Bitcoin with a clear strategy and plan.

Downside Factors

Bitcoin halving and prices

The Bitcoin halving event in 2024, which is well known, will halve the block reward for miners and seriously impact profitability in the short run. We could potentially see a fall in the global hash rate and network difficulty which could offset the reduction in block rewards and potentially reduce the price of ASIC machinery assuming demand for them starts to wane. This could lead to a lower total asset value for Riot, especially with these machines depreciating in the background, which could impact the share price in the short term. The one way that this can be compensated is through appreciating Bitcoin prices (which has typically been the case in prior post-halving cycles) and would act as a hedge against reduced block rewards. If Bitcoin fails to appreciate, we could see several closures in the mining industry, and whilst this would impact Riot’s share price, the company currently stands on good footing to survive. Based on my model and estimates, assuming current Bitcoin prices at $33,000 and a 30% drop in network difficulty, the total cost to mine plus operating expenses is approximately $25,000 per Bitcoin for Riot, which means that Riot would still be profitable post-halving. Nevertheless, the halving could provide a clean slate for mining economics as we’ve seen record high hash rates and network difficulty which may turn offline thus benefitting well-capitalised miners like Riot in the longer term.

Fully funded for now, but expect longer-term dilution

In March 2022, Riot entered an ATM offering under which they could offer up to $500m in shares of their stock and the company received net proceeds of 184.7m. In December 2022, they already issued 304m, so they have approximately 10m left. I wouldn’t be surprised if they choose to tap into the ATM market again next year which I believe isn’t priced into the market just yet. For example, if they wanted to exercise the option of purchasing the additional 66,560 miners, they will need to raise more capital through equity financing, despite regular sales of Bitcoin, which could range between 20-30% cost of equity, especially if you consider delays or greater than anticipated costs to build out their facilities. Debt financing (if available) could be more costly after several blow-ups last year and interest rates at 5.5%. The loans for some miners back in 2021 had rates north of 15%, so I wouldn’t be surprised to see interest rates near the 30% mark in current conditions, thus making equity financing potentially cheaper and easier to obtain. The only way around this is for Bitcoin to appreciate more than Riot’s cost of capital, but when you factor in the halving and network difficulty, the calculations become more complex which adds uncertainty to the future value of the company.

Investment Idea

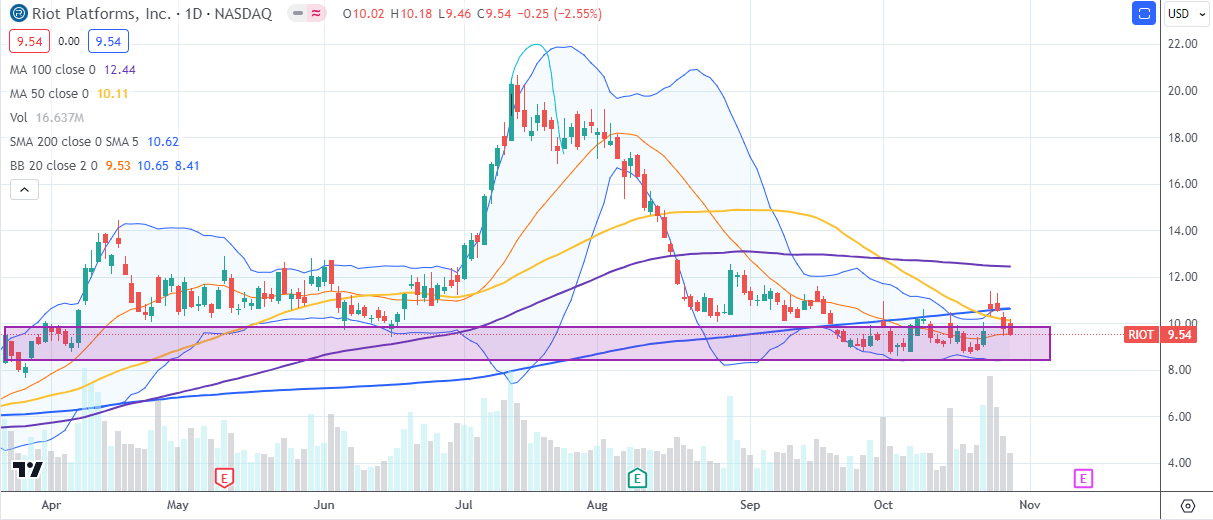

Riot seems to be technically supported in this $8-10 area which represents the level prior to the summer breakout, if Bitcoin prices continue to grow from here, I believe that Riot can continue to grind back higher towards the $20 over the next year. As options are liquid in Riot, a simple buy-write options strategy could work here. Buy the stock and sell weekly or bi-weekly 20-25 delta call options to capture some of the upside volatility in the turbulent months leading up to the halving.

All things considered, miners have extreme volatility, and despite selling 20-25 delta calls, at some point, a substantial breakout could lead to your shares being called away. If they are close to, or at the money, you could roll the options to the next expiry and avoid them being called away. Ultimately, as I am longer-term bullish, I am only willing to risk 50% of my total shares through the options writing strategy, simply because if my shares do get called away, I’m still left with 50% of my position for the medium to longer term.

{kind=link}

The price of Bitcoin seems to be supported by positive sentiment and therefore, I anticipate a new floor being around the $30,000 mark, and upside resistance near the $40,000 mark which, if reached, would more than offset the halving impact for Riot, at least in the near term. However, my bet is on longer-term Bitcoin appreciation and mining economics correcting after the halving, in which I believe that Riot is best positioned to grow from. I do think we are on the cusp of a bull market in Bitcoin for a variety of factors such as deteriorating macro conditions, institutional adoption, and the eventual realisation of managers seeing Bitcoin as a diversifier in a portfolio due to low correlations with other asset classes.

Risk Management

If Bitcoin craters down and breaks the $30k support convincingly, we can hedge the position by using a collar, i.e. sell a call and purchase a put to protect against some of the downside risk. I will abandon the idea altogether if I start to see complacency in management and their operations namely in the form of:

- Frequent delays in building out facilities and higher than anticipated costs to mine

- Aggressive treasury management of Bitcoin in the form of trying to time the market or letting machines idle (aside from power curtailment) instead of mining which would be evident with higher downtime, in particular from their Corsicana facility

- Shift in operations into AI or other ventures outside of Bitcoin-related operations

Conclusion

Bitcoin mining is essentially a power and energy market play and I believe that Riot has an edge from their agreement with ERCOT and their history in managing various cycles in commodity markets and Bitcoin. This diversification in revenue makes Riot more than just a pure mining company, however, I remain vigilant on whether Riot explores this avenue too far which could have a material drag on uptime, like other miners seeking expansion into AI which is an unproven market. In the long run, their low cost to produce, efficient mining fleet, and conservative balance sheet can help insulate against the downside from the halving next year whilst still being able to participate in the upside when mining conditions become favourable and when Bitcoin prices appreciate.

For further details see:

Riot Platforms: Best In Class Bitcoin Miner