SSO - Risk On: Looking Forward To A Soft Landing

Summary

- So far, the Fed has threaded the needle between declining inflation and strong employment.

- Data remains strong with not only employment, but consumer spending and economic growth continuing to hold up.

- Stocks have priced in various scenarios, but likely have been too pessimistic given historical norms.

Since the Fed started tightening, the phrase “soft landing” has been used countless times in articles, by financial media talking heads, and just about anywhere you look (other than memes complaining about egg prices). The general concept of a soft landing is relatively easy to comprehend: reduce inflation without causing a recession. This definition is simplistic and doesn’t provide quantifiable metrics against which to judge the economy and the work of the Fed.

How To Define A Soft Landing

How can we quantify a soft landing, and how can we conclude that inflation has been successfully contained? To many, a soft landing will feel like a recession, or worse. People will lose their jobs, default on car and credit card payments, and file for bankruptcy. Unfortunately, the media will pick up on these stories and extrapolate them to the broader economy to imply that conditions are worse than they are. The fact is that most people won’t lose their jobs, won’t default on debts, and won’t file for bankruptcy. Most people and businesses will continue to grow, albeit at a potentially slower pace. So let’s look at the key factors that define a soft landing in turn.

Employment

Recent layoffs, particularly within the tech sector have received a lot of coverage from both financial and traditional media. While these changes are important, they are by no means an indication of the strength of the aggregate economy. Tech employment, including some jobs within the communication services and consumer discretionary industries, represents less than 10% of the U.S. labor force. However, the market cap of these firms represents more than 30% of the S&P 500. This is a classic example of a divergence between what happens in the stock market and what happens in the real economy. Don’t get me wrong, many of the job cuts are highly paid individuals that are also prodigious spenders. There will be some ripples through the broader economy as a result of layoffs, but at this point, there is no reason to believe those ripples will cause any major damage.

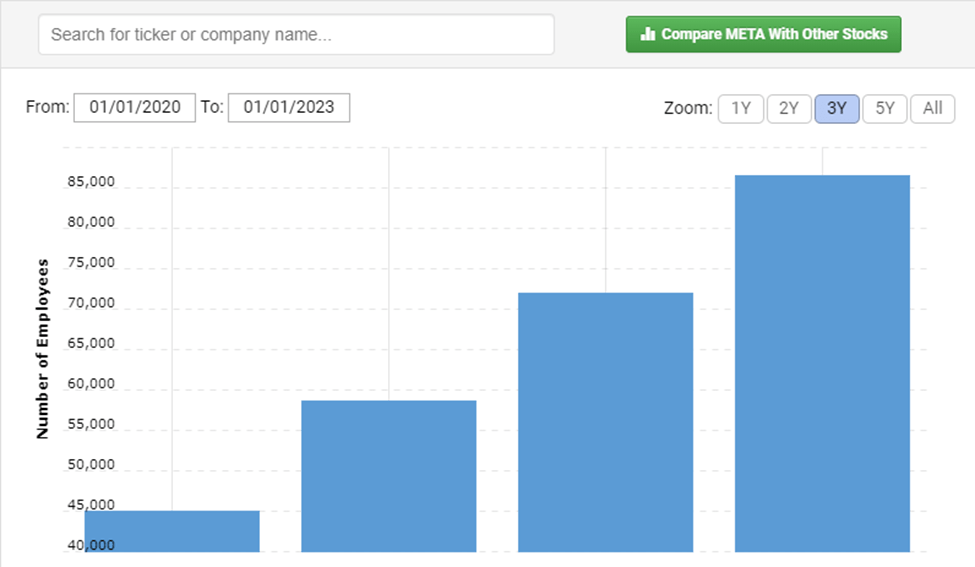

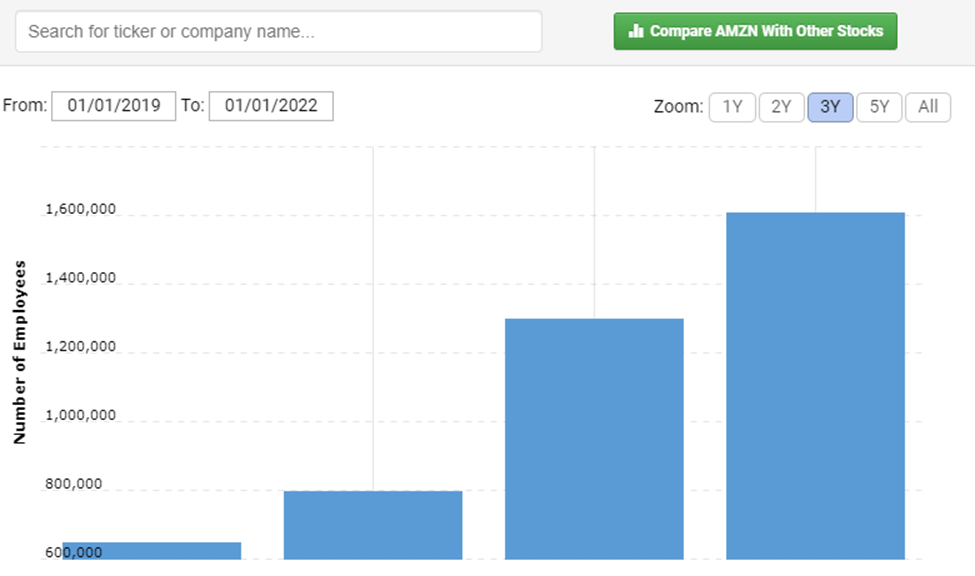

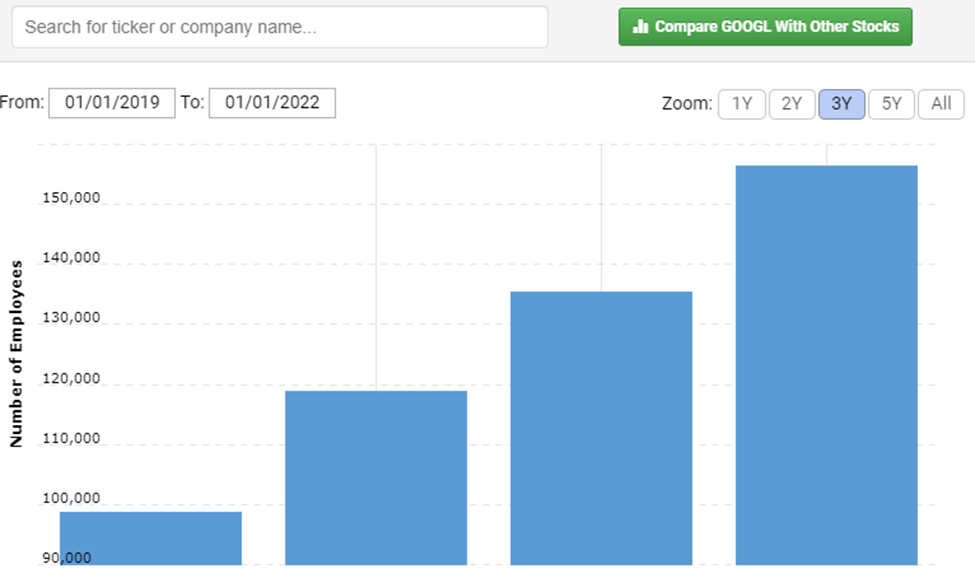

In many cases, the tech layoffs are a means of right sizing the labor input at these companies. Several large tech companies, including Meta ( META ), Amazon ( AMZN ), and Alphabet ( GOOGL ) (GOOG) increased their labor force in excess of 50% over the last three years alone. In the cases of Meta and Amazon, headcount grew by more than 100% during the last three years. In other words, many of the layoffs are simply a reversal of those hiring sprees, and in many cases are returning headcount to the levels of 12-18 months ago. Not something to get too excited about.

{kind=link}

{kind=link}

{kind=link}

Layoffs Will Continue

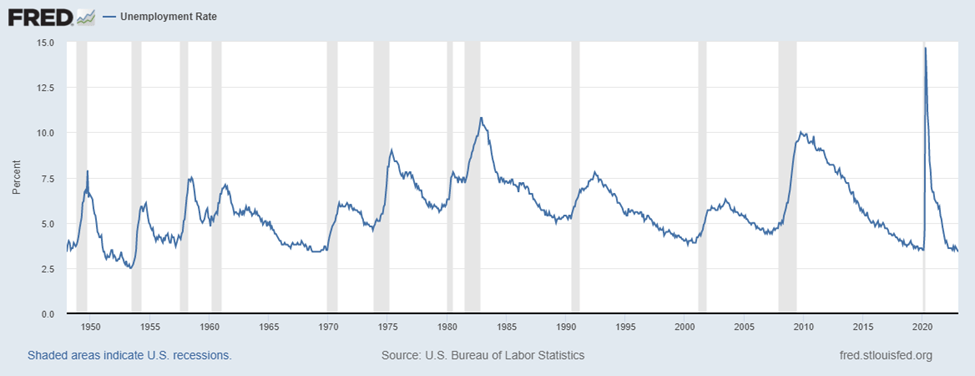

It is reasonable to expect layoffs to continue in certain corners of the economy. That said, the January jobs report is an important data point when evaluating the current economic conditions in the U.S. The U.S. economy added 517,000 jobs during the month, compared to expectations of around 187,000. The blowout month caused the unemployment rate to decline to 3.4%, the lowest level in more than 50 years.

{kind=link}

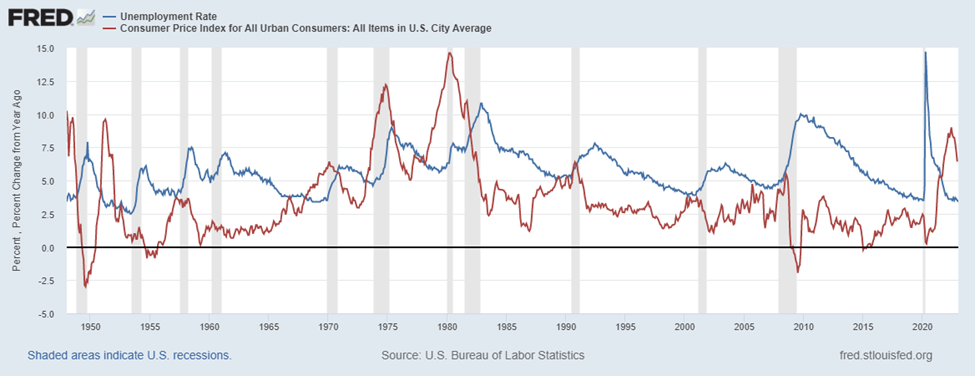

Should the strong employment status cause the Fed to step on the gas? Maybe, but not necessarily. While employment has remained resilient in the face of rising rates, inflation has steadily declined since peaking nearly a year ago. In other words, the current set-up is for a soft landing: declining inflation to more normal levels while employment remains steady.

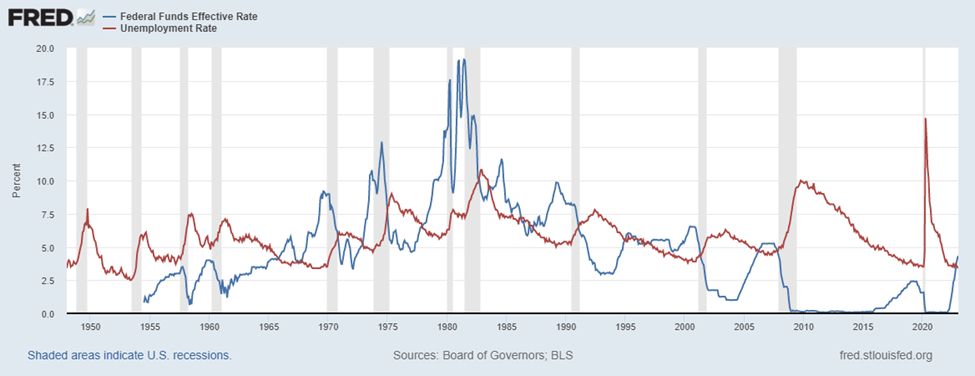

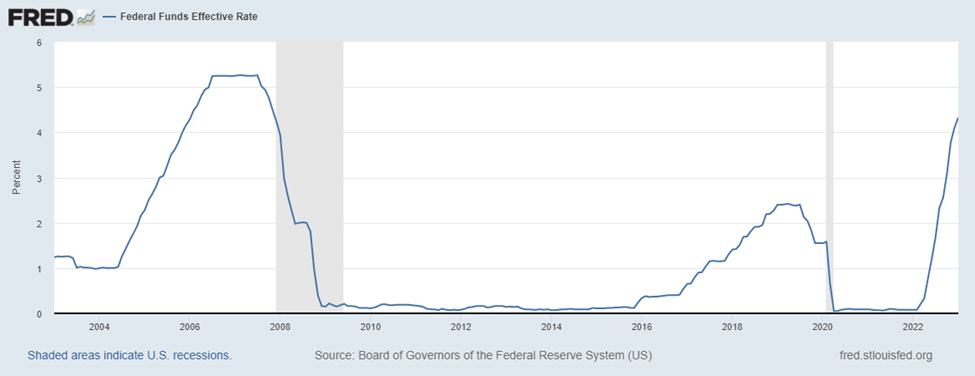

But before we get too excited, the relationship between unemployment and inflation, and unemployment and the Fed funds rate should be considered. Typically, unemployment lags the rise in inflation and subsequent rise in interest rates. While this relationship is moderate, it does imply that there can be about a 2 year lag between peak inflation and unemployment. A similar lag is present between the Fed funds rate and unemployment.

Federal Funds Effective Rate versus U.S. Unemployment Rate (St. Louis Federal Reserve)

{kind=link}

{kind=link}

While there has been about a 2+ year lag between peak inflation and peak unemployment historically, this isn't necessarily the case this time. Like so many things over the past 3 years, that relationship appears to be breaking down. Inflation is on a downward trajectory while unemployment is holding steady, even improving in the most recent month. This is not what has been experienced in the past (in a good way so far.)

Consumer Spending

In addition to recent, and likely continuing, layoffs, investors should expect to hear about a slowdown in consumer spending. Monthly growth figures were negative in November and December of 2022 and that trend is likely to continue. However, coming out of the pandemic, consumer spending/retail sales exploded higher, and advanced significantly above average long-term growth. So while a slowdown in spending will feel like a shock to many, in reality it will likely result in a return to the long-term average growth trend (in dollars, while unit consumption increases with falling inflation).

Normalizing of spending, like other economic factors, will look like a recession to many, but it may simply be a return to long-term trends.

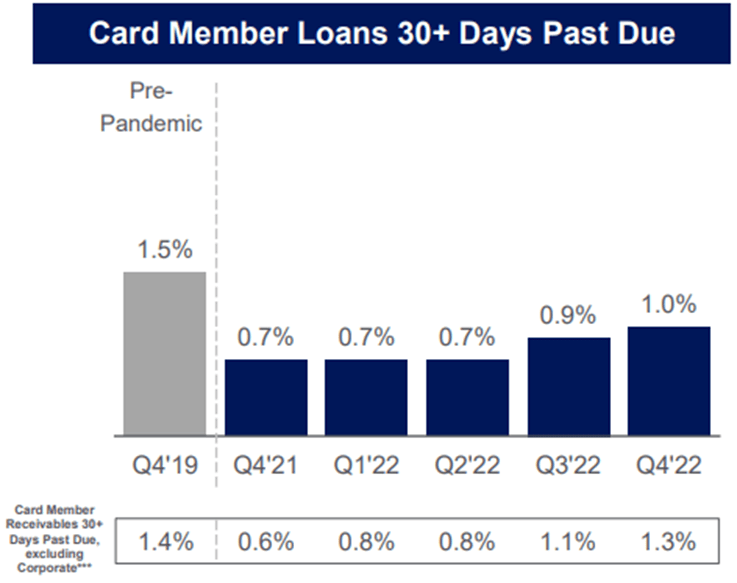

Credit card companies have reported strong spending while the number of loans that are at least 30 days past due is below the pre-pandemic level. While the rate has been increasing in recent quarters, this may be another sign of normalizing from the glut of pandemic spending and not cause for concern. The chart below is from American Express (AXP).

{kind=link}

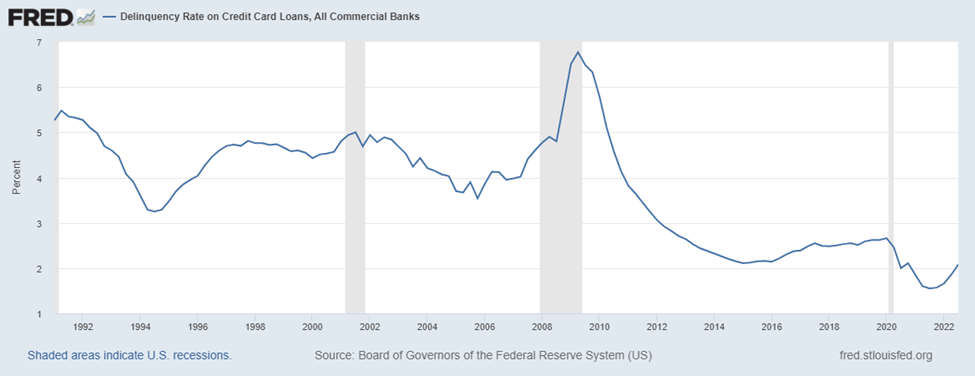

Looking more broadly at data collected by the Federal Reserve, the trends and directional accuracy remains intact.

{kind=link}

Growth and Inflation

While the Fed appears to be doing a good job threading the needles of what was previous thought to be impossible/unlikely, there are numerous factors that would be expected to be meaningful growth drivers. The change in Covid policy and reopening of China is a yet to be realized as an upside catalyst. It is not unreasonable to expect this factor alone to have a disinflationary effect while also facilitating consumer spending here and abroad while thawing frozen supply chains. From that perspective, more economic activity + disinflation = strong and strengthening U.S. and global economy.

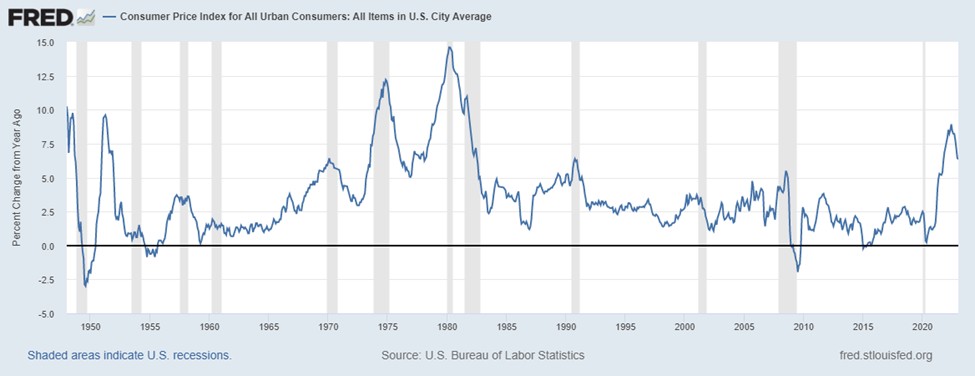

The trailing 12-month change in December was 6.5% as inflation continues to trend lower. Real GDP growth was 2.9% for the fourth quarter of 2022 while nominal growth was 7.3%.

{kind=link}

Fed Activity

The Fed has acted in its most hawkish manner in decades over the last year, bringing the Fed funds rate from effectively zero to a target range of 4.50%-4.75% following its most recent 25 bps hike. This is the highest level for the target rate in more than 15 years (since 2007).

{kind=link}

The impact of these moves has been mixed. While inflation has started to decline, as has activity in the real estate market, unemployment and general business activity has remained resilient. As noted above, the current unemployment rate of 3.4% is the lowest in more than 50 years, and GDP continues to grow at a solid pace.

What is the Fed to do? That depends on their true objectives. By mandate, the Fed is tasked with maintaining stable prices and employment. Inflation has been declining steadily for months, and employment has remained stable, so this appears to be a success at this time. However, if the Fed fears that inflation is driven by employment and wages, then we could see them continue their hawkish approach to ultimately slow growth and increase unemployment.

In a vacuum and using a strictly academic approach, the Fed could use the Taylor Rule for determining what the Fed funds rate should be. There are many pitfalls to this approach as it completely ignores employment, wages, and is dependent mostly on data points that are a snapshot in time and may not fully represent the trend in inflation and growth.

Using the Taylor Rule to calculate an estimate, we see that the output makes no allowance for the fact that interest rates and the inflation rate are converging, which would allow the Fed to move to a more neutral position before ultimately lowering rates once inflation reaches the target level in the 2%-3% range.

So, let’s use a simple form of the Taylor Rule and calculate what the target rate would be given current data.

Taylor Rule:

R = p + 0.5y + 0.5(p - 2) + 2

Where:

R = nominal fed funds rate

p = the rate of inflation

y = the percent deviation between current real GDP and the long-term linear trend in GDP

R= 6.4% + 0.5(2.9%-3.12%) +0.5(6.4%-2) +2

R=6.4%+(-.11%) +2.20%+2 = 10.49%

Because this method is strictly academic, and doesn't incorporate the dynamic nature of markets, the estimate is laughably high. Could one have argued that this was the proper rate in a static world when CPI was above 9%? Perhaps, but that would have been short-term. At this point, with converging interest and inflation rates, I believe that the Fed is close to reaching what should be a neutral stance and will have successfully threaded the needle between inflation and employment to reach a soft landing.

Putting It All Together

Putting these factors together, we can start to close in on targets to determine what a soft landing will look and feel like. With a reversion to trend on consumer spending and declining inflation, real GDP growth may approach zero, with nominal GDP growth remaining positive by roughly the rate of inflation.

Unemployment is likely to rise, but not to significant levels. For decades economists have debated what full employment is and what impact that might have on inflation. Prior to the pandemic, we had unemployment of 3.5% and low inflation. We are back below 3.5% unemployment at 3.4%, but with higher inflation, 6.4% as of the last report for CPI. I’m not sure what the Phillips Curve would look like right now, and how it can be reconciled with how the economy has behaved over the last 3+ years. So would a move in inflation down from 6.4% to 3% or below cause unemployment to rise 0.50%-1.00% or more, bringing the rate to 4.5%+? Time will tell. But while that magnitude of a move in unemployment would be perceived as significant, it is likely not enough to cause a deep or prolonged recession. For perspective, back in the late 1990s when unemployment reached the low 5%s, economists debated whether that was full employment and whether dropping below 5% would drive inflation significantly higher.

So what would I qualify as a soft landing? Realistically, I would say sub 5% unemployment, real GDP growth at least 0% (nominal above positive), and inflation that continues to decline and ends 2023 in the 3-4% range.

At this point in time, there is a lot of evidence suggesting that the U.S. economy will experience a soft landing. This is good for stocks, good for jobs, and good for the average American. While negativity sells better, there is a solid case to be made right now for optimism.

What To Expect From Stocks

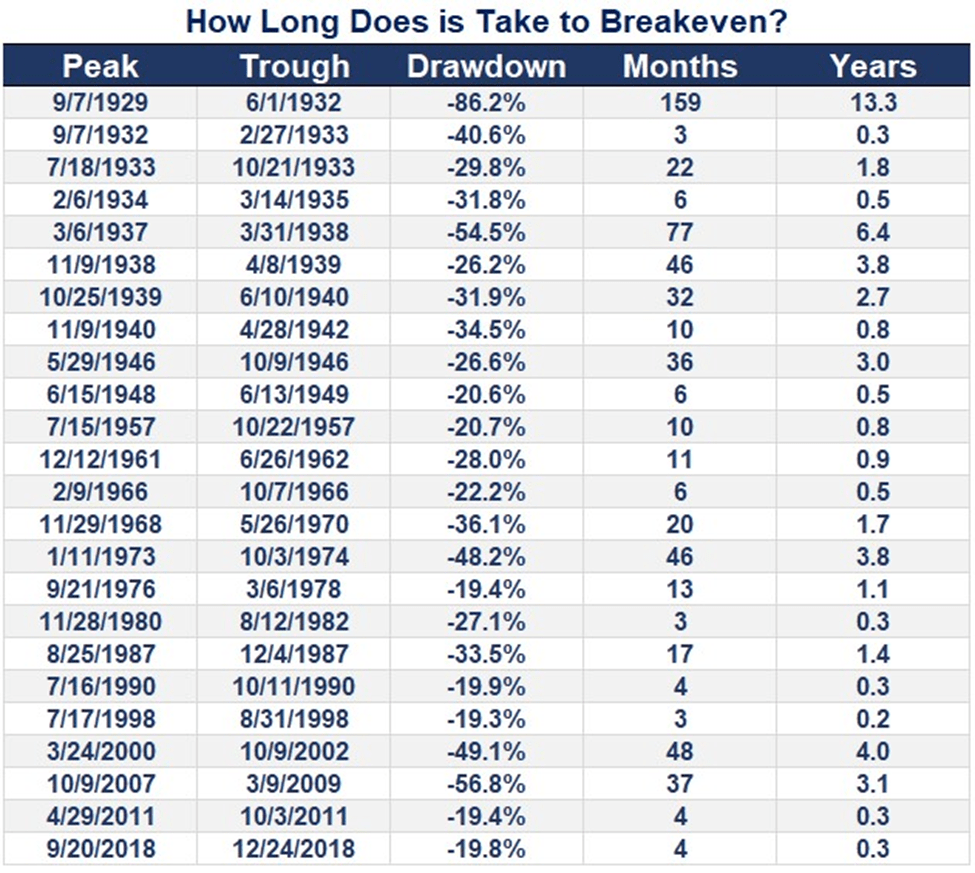

The question during an uncertain period in economic news is when will stocks sniff out the inflection point? And, how far in advance? In this case, it is reasonable to ask if that pivot is already underway? If the answer to the latter is yes, then great. In any case patience will be very profitable for long-term investors as current asset values will be seen as a bargain in the not-too-distant future. While I'm not assuming that the worst is necessarily behind us completely, it is reasonable to expect asset prices to reach new highs within the next 3 years. Historically, this would be on the long end for the length of time for stocks to recapture their previous highs.

Breakeven: Peak to Peak (A Wealth of Common Sense: Ben Carlson)

{kind=link}

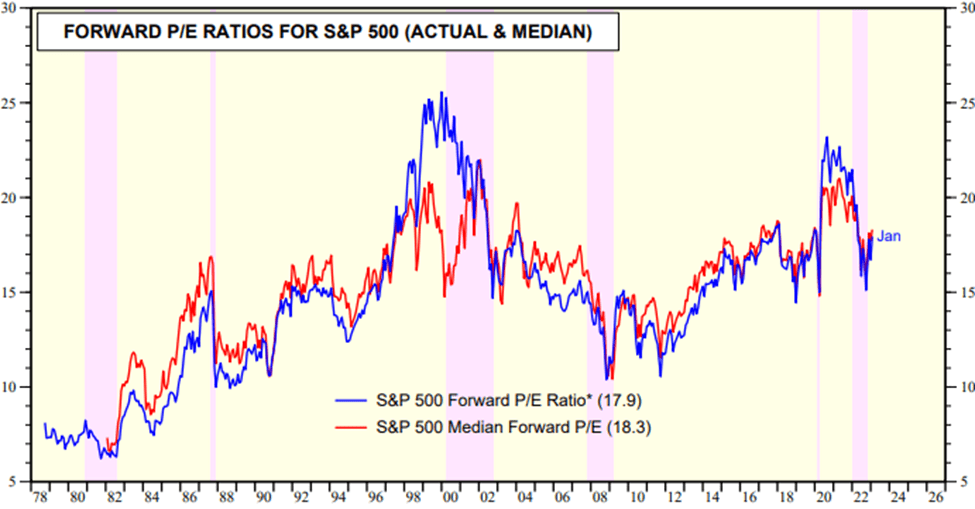

Now that we have looked at the historical track record for stocks returning to previously reached peaks, we should also look at valuations. By historical standards, according to this chart from Yardeni Research, the stock market is in line with historical averages. Looking at the various segments (not pictured, but also available from Yardeni Research) of the S&P based on market cap, we see that the mega cap companies have pulled the average higher, implying that the market valuation is healthier than the total forward P/E ratio would imply.

{kind=link}

Note: Chart from Yardeni Research as of 2/13/2023

Average weekly price divided by 52-week forward consensus expected operating earnings per share.

Note: Shaded red areas are S&P 500 bear market declines of 20% or more. Yellow areas show bull markets.

Source: I/B/E/S data by Refinitiv.

Final Thoughts

Predicting the future is futile. Data changes quickly, regularly, and in unpredictable ways. Narratives often overstay their welcome. Wanting an outcome, or hope, does not change reality. In other words, today’s future expectations on the economy, employment, and inflation will become dated and forgotten quickly while pessimism will persist despite the data. There is no place for pride and emotional reactions in investing. I have structured this article and my argument for optimism around the currently available data. As we all know, that data, and world can change quickly and without notice. While I think the probability of a recession has declined, it can definitively still occur, and bring with it its negative realities in terms of the real economy and financial markets. Please take what I discuss in this article with a grain of salt and consider it in the broader context of your overall asset allocation and long-term financial plan. Thank you for reading, and I look forward to seeing your comments below.

For further details see:

Risk On: Looking Forward To A Soft Landing