RSKD - Riskified: Still Decent Upside Under Conservative Assumptions

2023-07-21 11:16:35 ET

Summary

- RSKD has seen a steady improvement in its fundamentals. Growth is relatively steady, and TAM is massive and growing.

- My target price model suggests a price of $5 at year's end, an 8.7% upside. However, assumptions are conservative.

- Near-term risks are minimal to moderate. I rate the stock a buy.

Riskified (RSKD) is a global technology company specializing in fraud prevention and e-commerce risk management solutions. The company provides a range of services and tools to help online businesses mitigate fraud and reduce chargebacks.

RSKD went public in 2021 and reached an all-time high of ~$37. However, the share price has gradually declined since then. For most of 2022 and 2023, the stock has been trading sideways between the $4 and $5 range. The stock is up ~1% YTD, and currently trading at ~$4.7 per share.

I give RSKD an overweight rating. Risk remains minimal to moderate in my view, but there is an attractive enough upside. My target price model suggests that RSKD may see at least a ~8% upside in FY 2023.

Catalysts

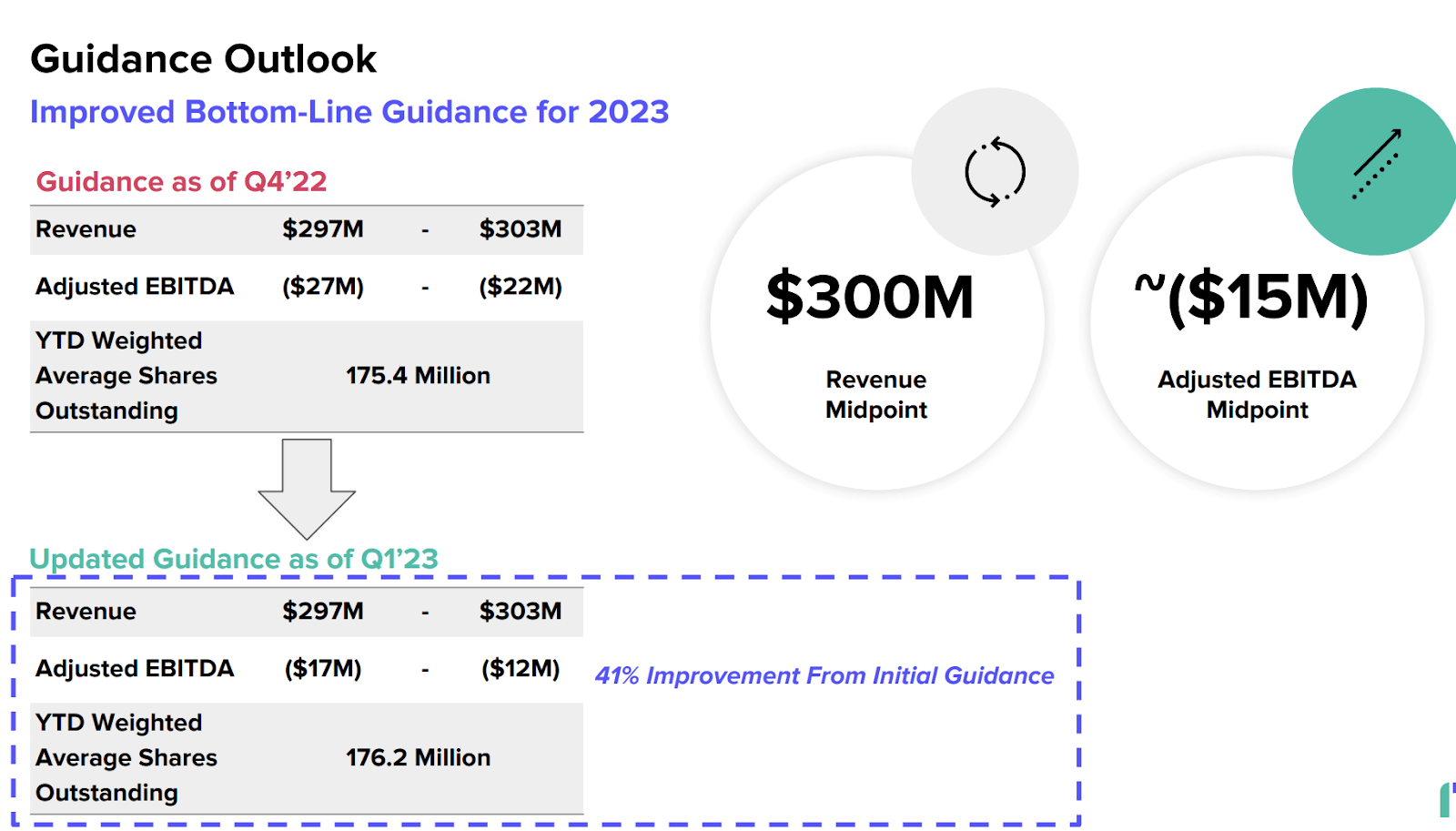

Overall, RSKD’s fundamentals have been decent and improving. Despite the consistent double-digit growth, annual revenue growth has declined from over 30% to ~14% last year. However, RSKD most recently saw revenue growth reaccelerate to 17% in Q1, a rather solid display given the macro weakness.

Furthermore, RSKD’s profitability and operating cash flow / OCF generation, which had been unimpressive, also improved. OCF turned positive in Q1 and the net margin narrowed to around 26%, which was a wider loss compared to the previous quarter, but a much better figure than the over 40% - 50% loss margin seen last year.

Given the ongoing cost optimization initiative into FY 2023, I expect overall profitability to improve further. The execution here has been relatively positive:

Adjusted EBITDA for the first quarter was negative $5.2 billion, a 62% year-over-year improvement. We have meaningfully improved our adjusted EBITDA performance on a year-over-year basis for the third consecutive quarter since making the decision to accelerate our timeline to reach profitability.

Source: Q1 earnings call.

I believe that there is still a lot of room for improvements in adjusted EBITDA beyond Q1 - having improved the figure for three consecutive quarters, and RSKD still saw a rather elevated YoY figure of 62% in Q1.

{kind=link}

As RSKD continues with the initiative, I don’t think that a further guidance lift as seen in Q1 is impossible at all. On that note, one positive attribute I noticed about RSKD is the management’s proactive approach to improving the bottom line despite its strong balance sheet. RSKD had ~$480 million in cash as of Q1 with negligible debts.

I don’t think that the management’s actions should be viewed as an over-conservative approach in running a growth company like RSKD. The common problem many growth stocks have faced in recent times is not only the lack of cash flow but also, more importantly, the ability to be cash flow positive at all. This does not seem to be the case with RSKD, which continued to improve its fundamentals and reported a positive OCF in Q1.

{kind=link}

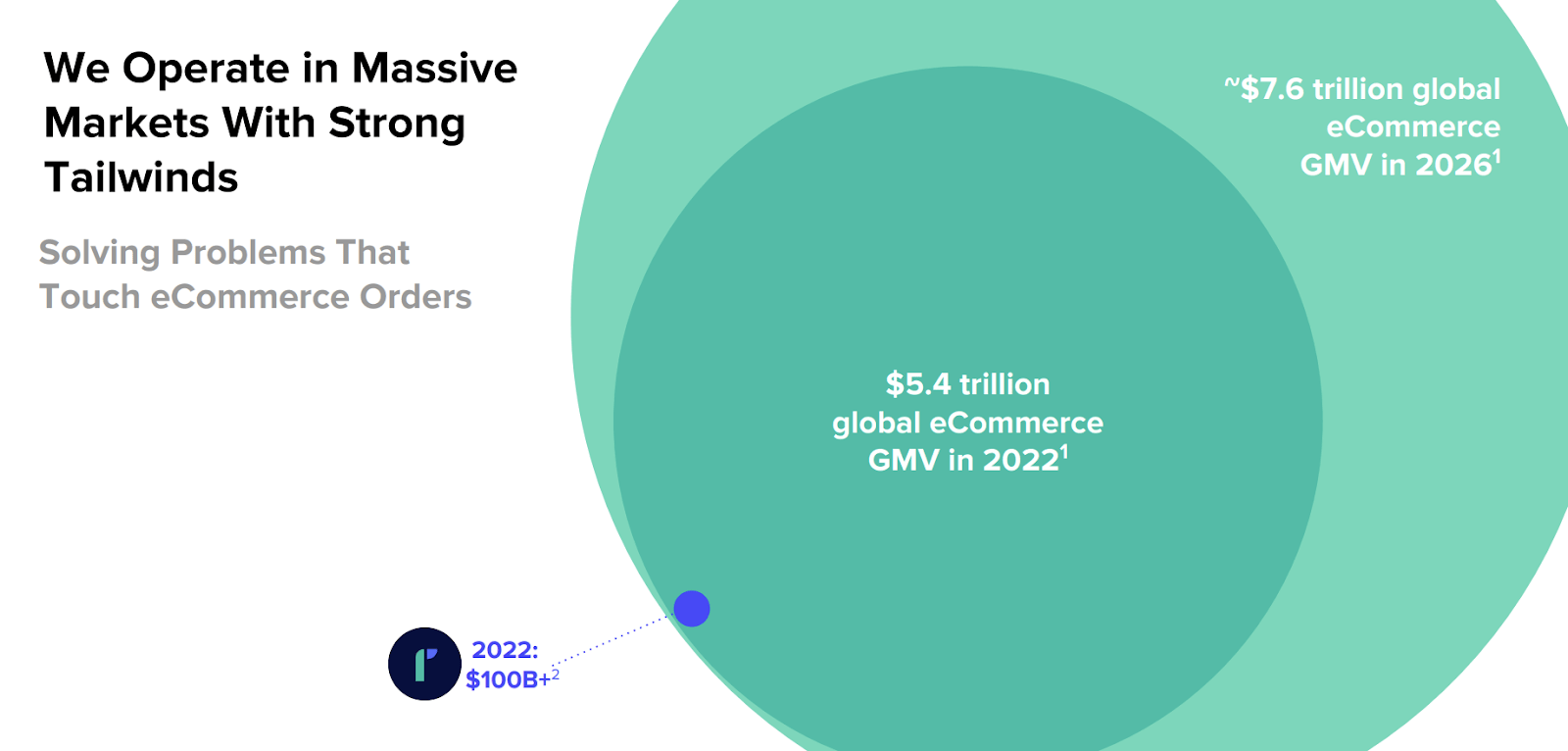

Additionally, RSKD is in a good position to see growth reacceleration beyond FY 2023 as the macro weakness subsides, given the massively growing TAM in eCommerce. As merchants grow in size, so do the pain points around fraud and chargebacks. I believe that RSKD has a unique solution to solve these issues. Furthermore, given the depth at which RSKD's solution needs to be integrated into the merchant’s infrastructure to generate meaningful results, the solution has a mission-critical nature that implies high switching costs.

Risk

Near-term risk remains minimal to moderate. While the macro weakness may affect the business performance of eCommerce merchants operating in certain verticals, such as home categories, I think that RSKD is probably quite diversified in terms of verticals . It is also a temporary headwind that may subside in the future, and once it does, RSKD may unlock higher revenue growth.

However, one area where RSKD needs to actively explore is mitigating its merchant concentration risk further:

For the three years ended December 31, 2022, 2021 and 2020, our three largest merchants in the aggregate accounted for 25%, 30% and 36% of our revenues, respectively. In addition, our five largest merchants in aggregate accounted for approximately 34%, 39% and 49% of our revenues for the years ended December 31, 2022, 2021 and 2020, respectively.

Source: RSKD’s 20-F.

As I had expected before I even jumped into this analysis, this seems to be an inherent risk for some companies providing business solutions for the largest eCommerce merchants with a take-rate business model . This may have been mitigated to some extent by the mission-critical nature of RSKD’s offering. Nonetheless, a hypothetical single churn within one of the three largest customers would still negatively impact RSKD’s revenue by 8% on average - an undesirable figure.

Valuation / Pricing

My target price for RSKD is driven by the following assumptions for the bull vs. bear scenarios of the FY 2023 target price model:

-

Bull scenario (50% probability) assumptions - RSKD to deliver revenue of ~$303 million, a 16% YoY growth, at the highest end of the guidance. I assume a P/S of ~3x across both bull and bear scenarios, where the stock is trading at the moment.

-

Bear scenario (50% probability) assumptions - RSKD to deliver revenue of ~$290 million, an 11% YoY growth, below the lowest end of the guidance range.

author's own analysis

Consolidating all the information above into my model, I arrived at an FY 2023 weighted target price of ~$5 per share. Since RSKD is trading at ~$4.6, the stock appears to offer an 8.7% upside. I rate the stock a buy. There are a few reasons why my overall assessment is rather conservative.

The 11% growth for the bear scenario assumes the worst-case scenario where one of the largest customers would churn in addition to RSKD meeting the lowest end of the guidance. I also assign a 50% probability for the scenario, which is highly conservative. I further believe that it is possible for the P/S to expand to ~4x, as it did in beginning of 2023, if the company can demonstrate bigger surprises in bottom-line improvements at year’s end. In that situation, RSKD may end the year with a price per share of ~$6, a ~30% upside from today.

Conclusion

RSKD's fundamentals have been showing decent improvement, despite a decline in annual revenue growth from over 30% to approximately 14% last year. However, the company experienced a solid revenue growth acceleration of 17% in the face of macro weakness. Near-term risks are considered minimal to moderate, but it's crucial for RSKD to address its merchant concentration risk actively.

The target price for RSKD is estimated to be around $5 per share for FY 2023, indicating an 8.7% potential upside from the current trading price of $4.6. Based on this analysis, I rate the stock a buy. Moreover, with conservative assumptions, there is a possibility that RSKD's price per share could reach around $6, presenting a potential upside of approximately 30% from the current value.

For further details see:

Riskified: Still Decent Upside Under Conservative Assumptions