RSKD - Riskified: Strong Growth Outlook Yet Negative Margins Remain A Concern

2023-12-24 02:50:06 ET

Summary

- Riskified is a software company specializing in fraud and chargeback prevention technology for the e-commerce sector.

- RSKD has experienced strong revenue growth but negative bottom-line margins due to rising SG&A expenses.

- Anticipated growth in e-commerce and increasing e-commerce fraud cases are expected to positively impact RSKD's future growth outlook.

- My conservative relative valuation indicates modest single-digit upside potential, therefore leading to my "Hold" recommendation.

Synopsis

Riskified ( RSKD ) is a company that offers software as a service specializing in fraud and chargeback prevention technology, particularly in the e-commerce sector.

RSKD’s historical revenue growth has been robust, growing in the double-digit range. However, bottom-line margins are negative, and losses have expanded. These losses were mainly driven by rising SG&A expenses. In 3Q23, revenue continued to grow strongly due to the successful execution of its go-to-market strategy, and there was an improvement in its net losses, driven by effective SG&A management.

Looking ahead, anticipated growth in e-commerce and increasing e-commerce fraud cases are expected to positively impact RSKD’s future growth outlook. However, ongoing uncertainties caused by inflation have led management to revise the 2023 revenue guidance downward. Given this mixed outlook and the modest single-digit upside potential in its share price, I am recommending a hold rating for RSKD at this juncture.

Historical Financial Performance

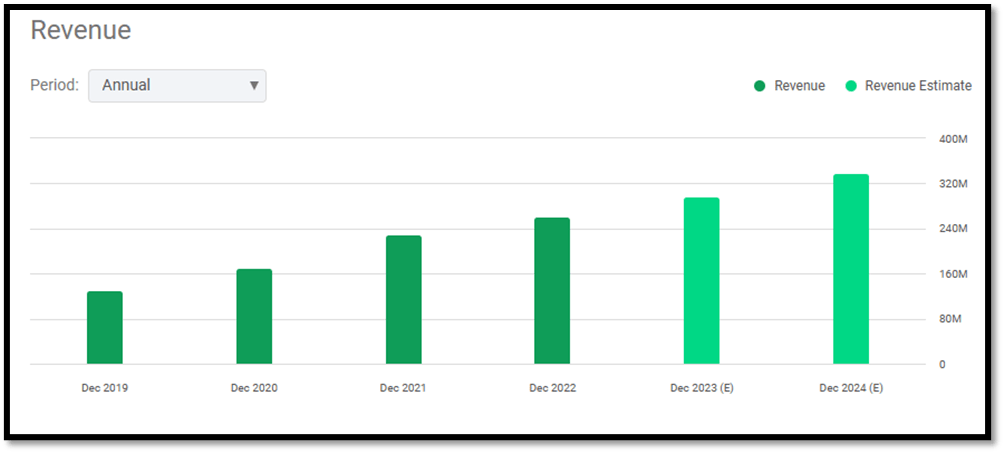

From 2020 to 2022 , RSKD’s revenue growth has been growing strongly, and it is in the double-digit range. In 2020 and 2022, growth was in the 30% range as COVID-19 boosted sales in the e-commerce sector, which benefited RSKD as it provides e-commerce risk management solutions. In 2022, growth slowed down to ~14.01%. I believe the slowdown in 2022’s revenue growth has to do with RSKD’s strategic decision and focus to improve profitability by reducing overall expenses. As a result of this, management decided to slow down hiring . However, management does not anticipate the hiring slowdown to have any negative impact on its growth outlook in the long term.

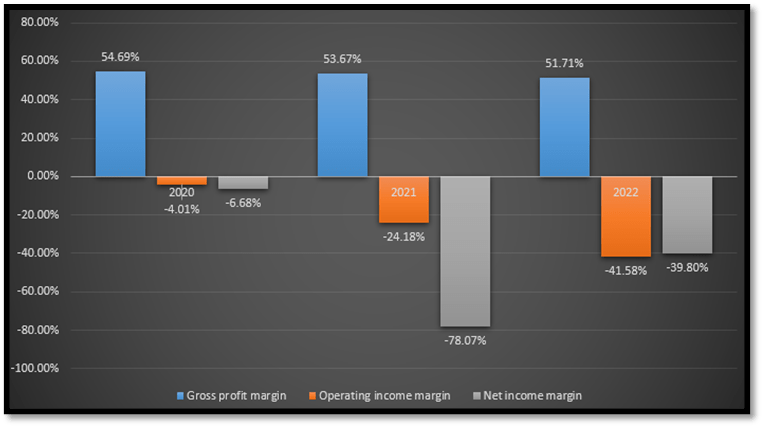

Author's Chart

When I analyze RSKD’s margins, it’s clear that it is unprofitable at the bottom line. As of 2022, both operating income and net income margin are in negative territory. There is a stark contrast when compared with 2020 when its losses were in single-digit percentages. Next, let's dive deeper into its P&L and try to understand what drove its losses deeper into the red.

{kind=link}

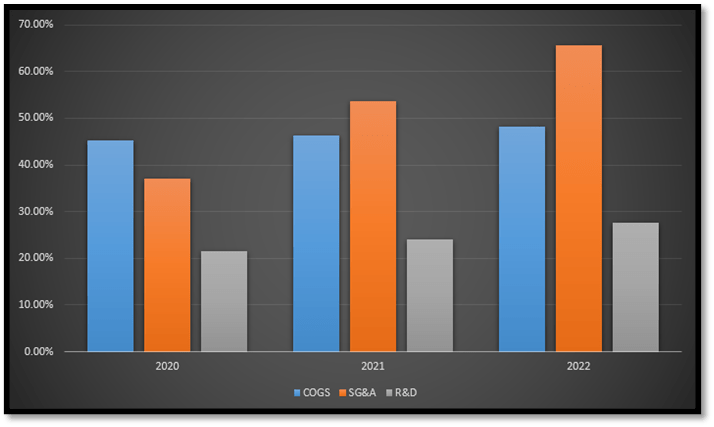

Based on the following chart I have created, it is clear that the main driver of cost is SG&A. In 2020, it only accounted for ~37.11% of total revenue, but by 2022, it had skyrocketed to ~65.73%. This significant rise in SG&A was due to the need to drive top-line revenue growth, which is common for young technology firms such as RSKD. In terms of COGS and R&D, it has been quite stable over the last three years.

{kind=link}

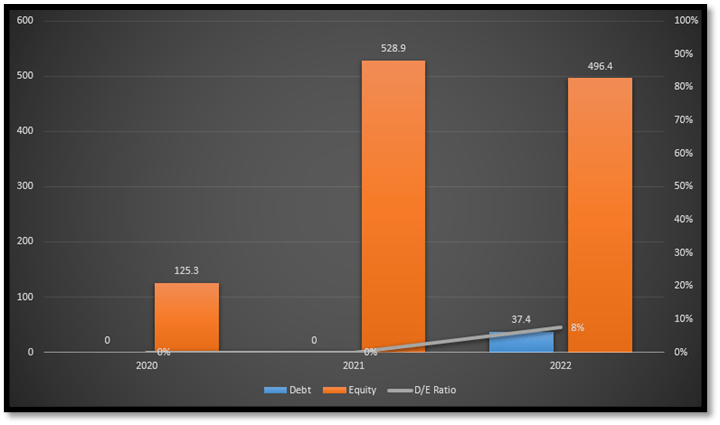

With negative margins, it's important to take a look at its debt levels on its balance sheet, as it gives us a sense of its current liquidity and solvency situation. Based on the following chart, it's quite clear that its debt-to-equity ratio [D/E] is extremely low, in the single-digit range. However, I do notice there is a slight uptick in debt in 2022, causing D/E to rise to ~8%.

{kind=link}

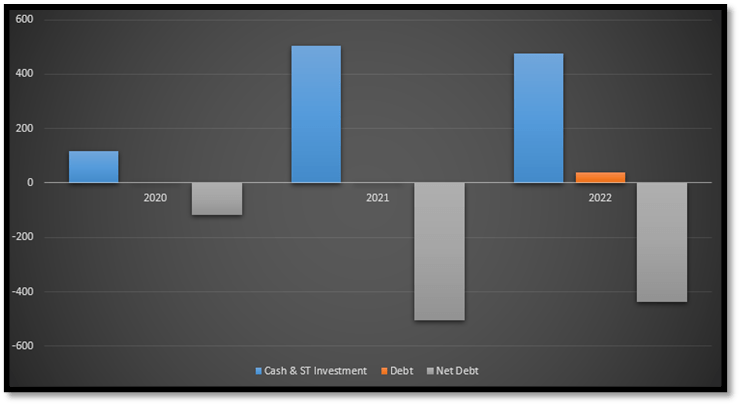

Although it might be nerve-wracking to see debt alongside negative margins, I believe that examining the net debt provides a clearer understanding of RSKD’s financial strength. Net debt is defined as total cash and short-term [ST] investments minus total debt. From the following chart, it is clear that RSKD has more than enough liquid cash to cover its debt levels. Therefore, I do not expect any issues arising from its debts.

{kind=link}

Analyzing RSKD’s 3Q23 Earnings

In 3Q23 , RSKD reported revenue growth of ~14% year-over-year, driven by its successful execution of its go-to-market strategy. RSKD has been successful in adding new merchants, retaining and upselling existing ones, and expanding market share.

Looking at its 3Q23 margins, it is clear that there are improvements in its operating income and net profit margin as both of its losses contracted. For 3Q23, the operating income margin improved ~6% to negative 35%. Net income margin improved ~12% to negative 29%.

In 3Q23, I noticed a slight contraction in the gross profit margin, which was due to a significant fraud event reported by one of its largest merchants. However, management believes and states that they do not anticipate this event affecting the subsequent quarters. Therefore, I expect to see the gross profit margins return to normalized levels in the upcoming quarters.

Author's Chart

The improvement in margins is attributed to effective SG&A cost management. In 3Q23, SG&A as a percentage of total revenue contracted year-over-year to ~54%, down from 2Q22’s ~66%. This represents an improvement of ~12% in SG&A costs. On the other hand, R&D was not sacrificed in order to improve margins, and this is especially crucial for a young technology firm that specializes in software solutions.

Author's Chart Riskified IR

Strong E-Commerce Growth Will Support RSKD’s Future Growth

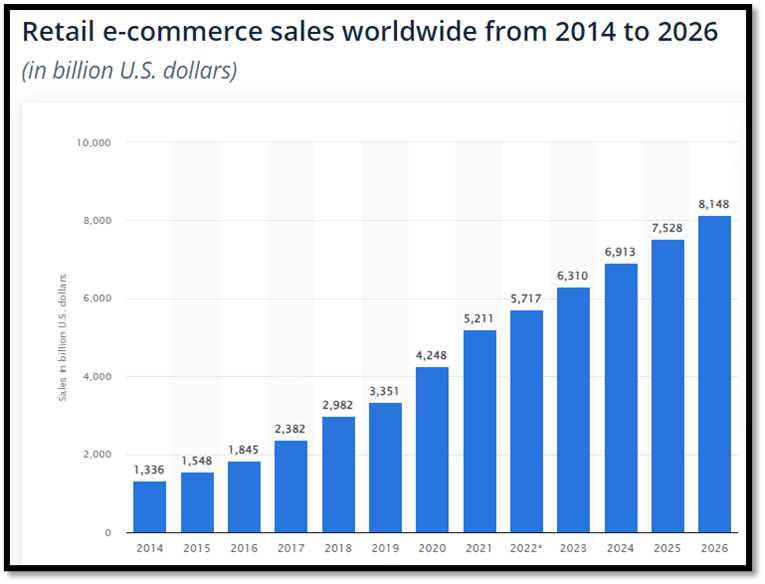

In 2022, global e-commerce sales reported a figure of ~$5.7 trillion, and it is expected to reach ~$8.1 trillion by 2026. This represents a CAGR of ~14.9% [2014–2026], and it is expected to continue growing until 2026. This strong double-digit growth in the global e-commerce market will bolster RSKD’s future revenue as it sells e-commerce risk management software solutions such as fraud and chargeback prevention technology.

{kind=link}

With growing e-commerce sales, e-commerce fraud is bound to increase. Based on statistics released by Mastercard , it was stated that global e-commerce fraud has been rising. In 2022, losses reached a staggering $41 million, and they are anticipated to continue to increase in excess of $48 million by 2023. Out of all the countries globally, North America [NA] has the highest level of e-commerce fraud, accounting for ~42% of all e-commerce fraud globally.

According to the following quote by RSKD’s CFO, Aglika Dotcheva, the US is RSKD’s largest region. Therefore, I anticipate that the rising fraud cases in the US due to the anticipated growth in e-commerce sales will increase the demand for RSKD’s solution.

Quote : “Finally, we also saw revenue growth across all geographies. Our third quarter revenue in the United States, our largest region, grew by 9% year-over-year”

Inflation Is Still Casting Shadows and Uncertainty

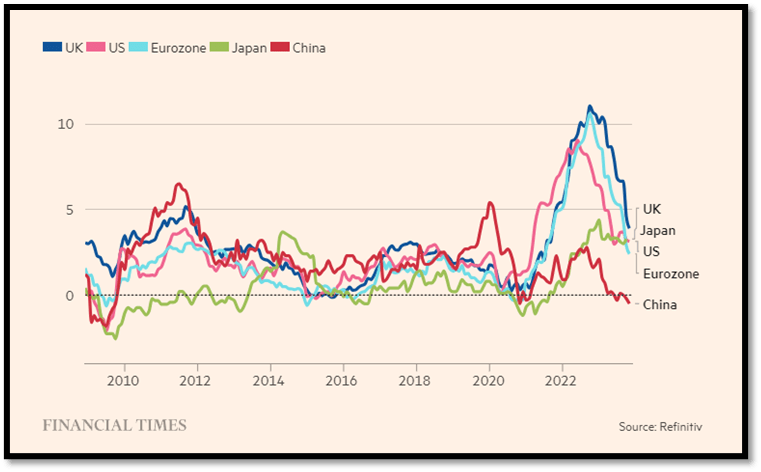

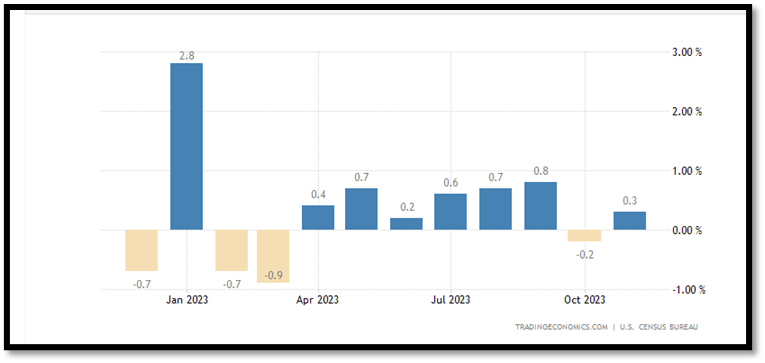

Based on the global inflation chart , there is a clear trend toward cooling inflation. Consequently, this decrease in inflation has bolstered retail spending. The second chart shows clear signs that US retail spending has been growing since April 2023, except for October 2023, partially due to the United Auto Workers strike , which affected the supply of automotive vehicles. The improvement in retail spending is likely to benefit RSKD as it will support e-commerce sales, thereby enhancing its growth outlook.

However, it's important to note that while inflation has significantly cooled from the 2022 spike, it remains above the target rate of ~2% in many countries. This situation continues to create macroeconomic uncertainties globally, as the market is still uncertain about when inflation will stabilize, which is a key factor in determining the direction of central banks' interest rates.

{kind=link}

{kind=link}

Updated Guidance Reflects the Macro Environment Uncertain

Due to the uncertainty caused by inflation being above the central bank's target rate, RSKD has updated its 2023 guidance . Previously, revenue was in the range of $298 to $303 million, but it has been revised to $297 to $300 million.

On the EBITDA side, it has been revised from a range of negative $17 to $12 million to negative $14.5 to $12.5 million. I welcome this EBITDA adjustment as it signals management’s confidence in its cost management initiatives and displays its commitment to drive margin improvement.

Comparable Valuation

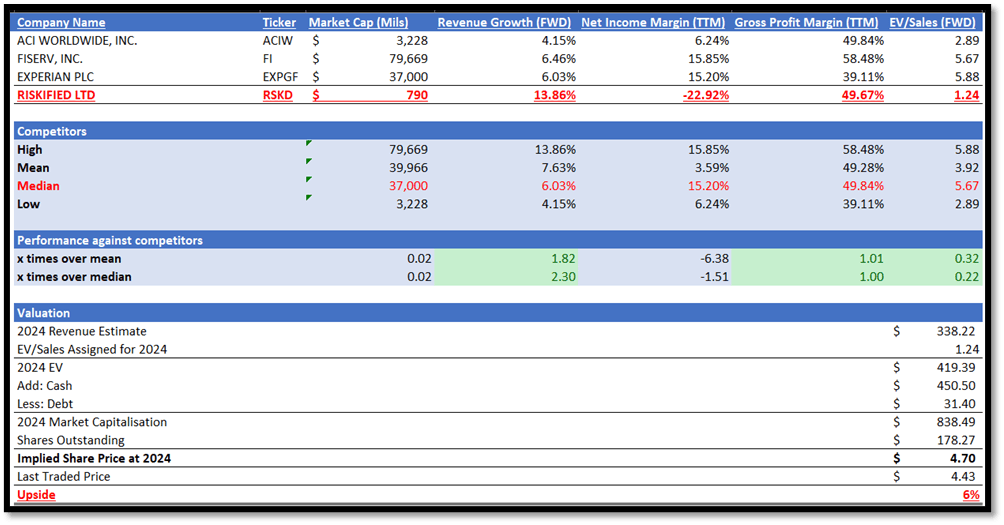

Before moving on, I want to clarify the comparable companies listed in my valuation model. While RSKD operates in the application software industry and specializes in fraud and chargeback prevention software technology, the three competitors I have identified also offer online transaction security, fraud detection, and risk management solutions, making them more suitable for comparison.

Right off the bat, it’s clear that RSKD is much smaller than its competitors. Its market capitalization is ~$790 million, while competitors’ median is ~$37 billion. In terms of size, RSKD is only 2% of competitors median. Despite its smaller size, its forward growth outlook is twice that of its competitors. RSKD’s growth outlook is ~13.86%, while competitors’ median is ~6.03%. However, it is quite common for smaller companies to grow faster due to easier comparable years, also known as the base effect.

When it comes to profitability, the narrative shifts. Among all the companies listed, RSKD is the only one reporting a net loss, the drivers of which have been discussed in depth earlier. However, in terms of gross profit margins, RSKD aligns with the median of its competitors.

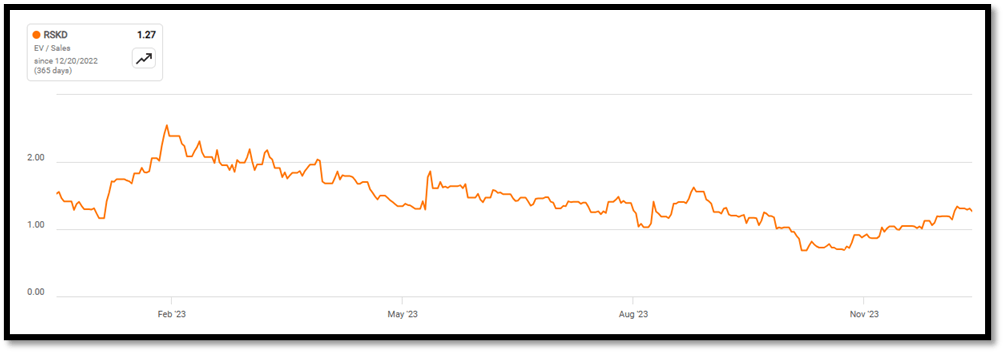

As a result of its net losses, RSKD is currently trading at 1.24x forward EV/Sales, while its competitors are trading at 5.67x. Looking at RSKD’s 1-year average EV/Sales, it is in line with its current forward EV/Sales. Therefore, I believe that there is a low risk that its current EV/Sales is over or undervalued. With these supporting factors, I believe that the EV/Sales market assigned to RSKD is fair and justified.

I applied its 1.24x forward EV/Sales to its 2024 market revenue estimate, and my target price for RSKD is ~$4.70, which represents a modest upside potential of ~6%, which in my opinion lacks margin of safety. Therefore, I am recommending a hold rating for RSKD.

{kind=link}

{kind=link}

{kind=link}

Upside Risk to My Hold Rating

In my opinion, I believe inflation might just be the catalyst for RSKD’s share price to appreciate. In my analysis of RSKD, I mentioned that its margins were in negative territory and that it was mainly driven by SG&A. If inflation cools even further, it will drive its SG&A expenses down, which ultimately leads to margin expansion. In addition, management is taking active steps to manage its current cost situation. In the event that margins were to be better than expected, its share price might appreciate.

Secondly, as discussed above, revenue guidance was updated due to uncertainty caused by inflation. Again, if inflation cools more than expected and upcoming revenue beats expectations, it will cause its share price to appreciate.

Conclusion

In conclusion, RSKD’s historical financial performance is mixed. Top-line revenue is growing robustly in the double-digit range, but I did notice a slowdown in 2022 due to management’s focus on profitability. It has also reported a net loss that is exacerbated by rising SG&A costs, but management has expressed its commitment to bolstering bottom-line margins. In 3Q23, RSKD continued to report strong revenue growth. At the same time, margins are improving through SG&A expense management.

Moving ahead, I expect the anticipated growth in the global e-commerce market will drive demand for RSKD’s solutions and thus support a positive growth outlook. In addition, global e-commerce fraud is rising in line with the growth of the e-commerce market. I believe this will also drive demand for RSKD’s products.

Although inflation has cooled from 2022’s peak, it is still above the central bank's target rates. Hence, it is casting doubt and uncertainty in the market. As a result, management has revised their 2023 revenue guidance downward to better reflect the current market outlook.

When I conducted my comparable valuation, it revealed that RSKD is trailing its competitors in terms of net income, but it has outperformed them in terms of growth outlook. Its current EV/Sales ratio is lower than the median of its competitors, reflecting its net loss situation. In addition, its current EV/Sales ratio is also in line with its historical average. Thus, these factors support my belief that its current valuation assigned by the general market is justified. With a lack of margin of safety in my target price, I am recommending a hold rating at this moment for RSKD.

For further details see:

Riskified: Strong Growth Outlook, Yet Negative Margins Remain A Concern