PLDGP - Risks Are Real And REITs Are A Steal (How We Play The Sector)

2023-09-17 07:00:00 ET

Summary

- Commercial real estate market is experiencing declining property values, rising vacancy rates, and shifting demand across various sectors.

- Softening fundamentals and surging energy prices may keep interest rates high, impacting the market further.

- Lending standards have tightened, impacting credit availability, and maturing debt is becoming a growing concern.

This article was co-produced with Leo Nelissen.

On September 12, we published an article titled, What If Inflation Remains High? Two REITs That Could Outperform .

In that article, we discussed the high likelihood of a new and lasting market environment consisting of sticky, above-average inflation, and higher rates.

We presented two stocks that would do relatively well due to excellent business models, stellar balance sheets, high yields, consistent dividend growth, and the ability to deal with elevated inflation.

This is also a macro-focused article, as we believe that it is important to take a step back to look at the bigger picture.

In this article, we will guide you through the most recent advancements in commercial real estate.

We will discuss the current vacancy rates, rent growth, debt quality, and other essential factors.

Additionally, we will provide a comprehensive overview of various real estate sectors across multiple industries.

So, let’s get to it!

The Bigger Picture – Cracks Are Starting To Appear

Earlier this week, Wells Fargo ( WFC ) published its new Commercial Real Estate ('CRE') chartbook. The bank, which has been on top of all major developments in CRE over the past few years, noted that the U.S. economy remains robust, supported by a robust labor market and controlled inflation.

As a result, Wells Fargo predicts a short and mild recession in the first half of 2024 as its base case scenario , though a soft landing seems increasingly likely due to the strong labor market, which continues to fuel income growth and consumer spending.

The bank does not expect further rate hikes.

Personally, we disagree with the bank when it comes to the soft landing. The latest inflation numbers showed the second-consecutive increase in year-on-year inflation.

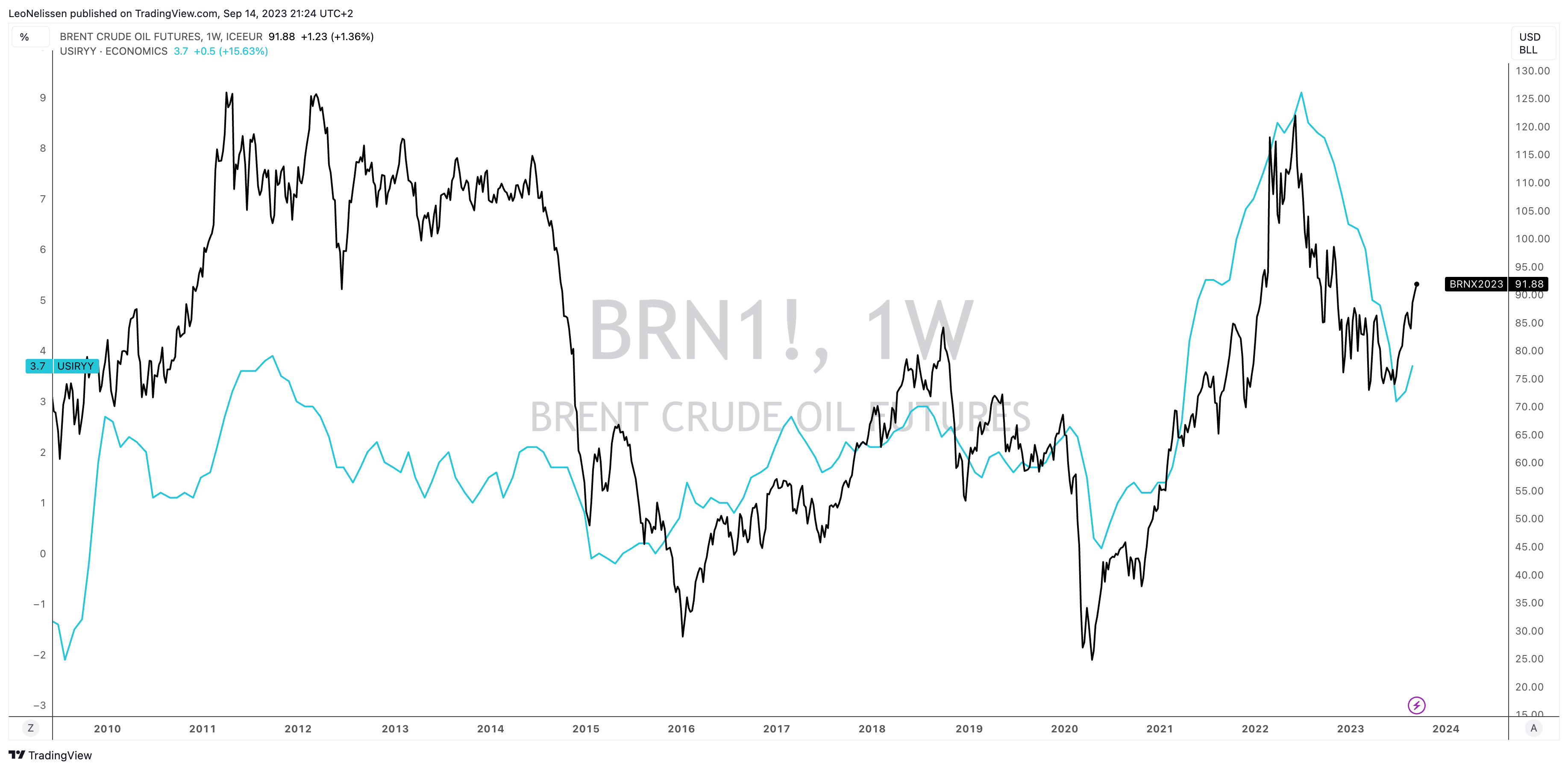

Looking at the chart below, we see the correlation between Brent crude oil and year-on-year inflation (all items). Although energy was the main driver, the problem is that energy works its way through the system. It could quickly put a halt to the decline in core inflation and make sure that the Fed keeps rates elevated for longer.

{kind=link}

Having said that, the reason why energy is so hot is slowing supply growth. The shale revolution in the U.S. is over, OPEC is cutting output, and demand remains stronger than expected.

This is an issue, as Wells Fargo noted that despite its somewhat rosy outlook, CRE is struggling.

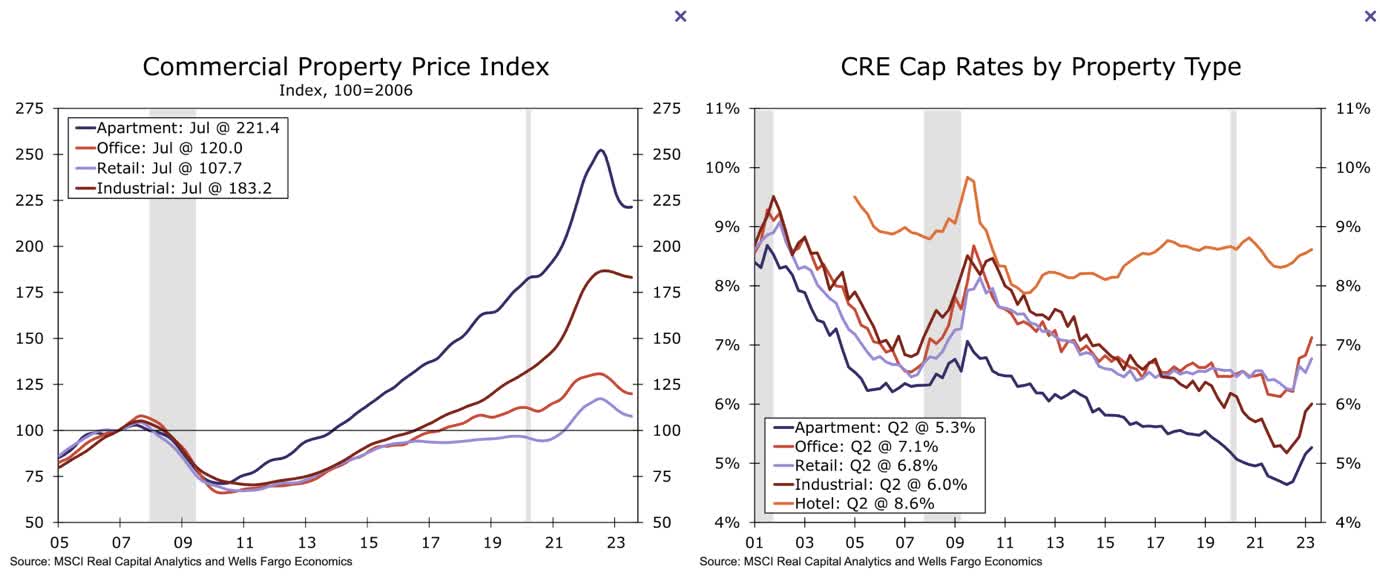

Rising Treasury yields have led to higher capitalization rates (cap rates) and declining property valuations. The CRE transaction volumes have plummeted , with differences in valuations between buyers and sellers further dampening sales activity.

The charts below display CRE prices and cap rates.

{kind=link}

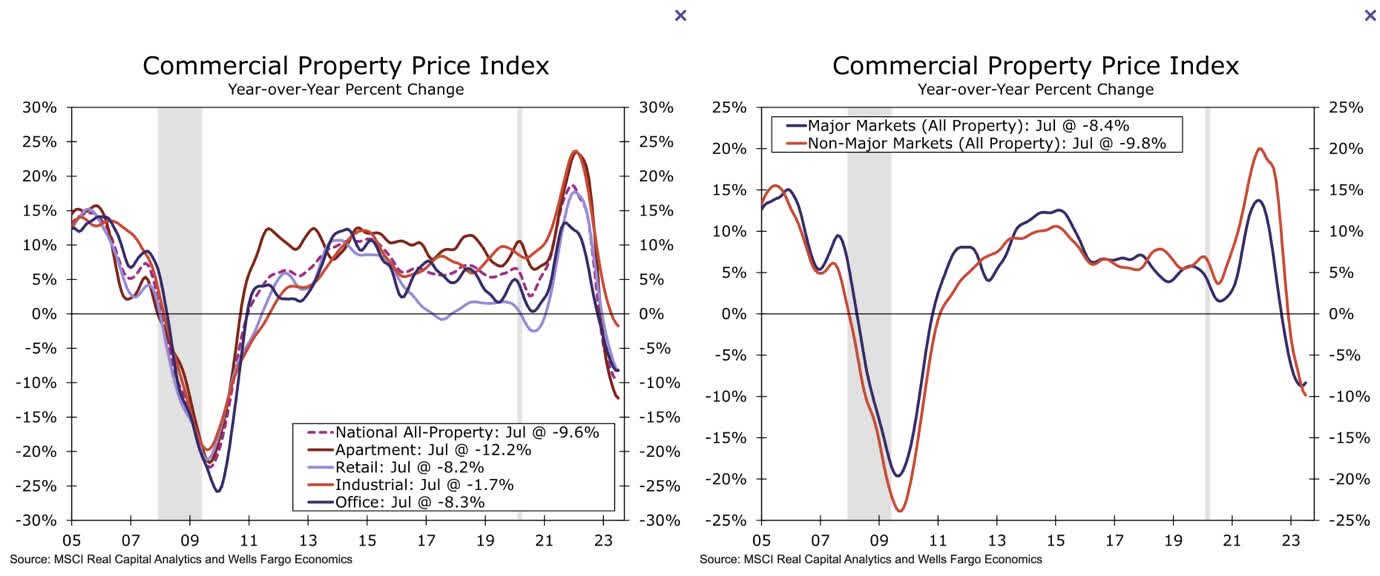

As we can see below, all property sectors are now seeing year-on-year price weakness, led by apartments.

{kind=link}

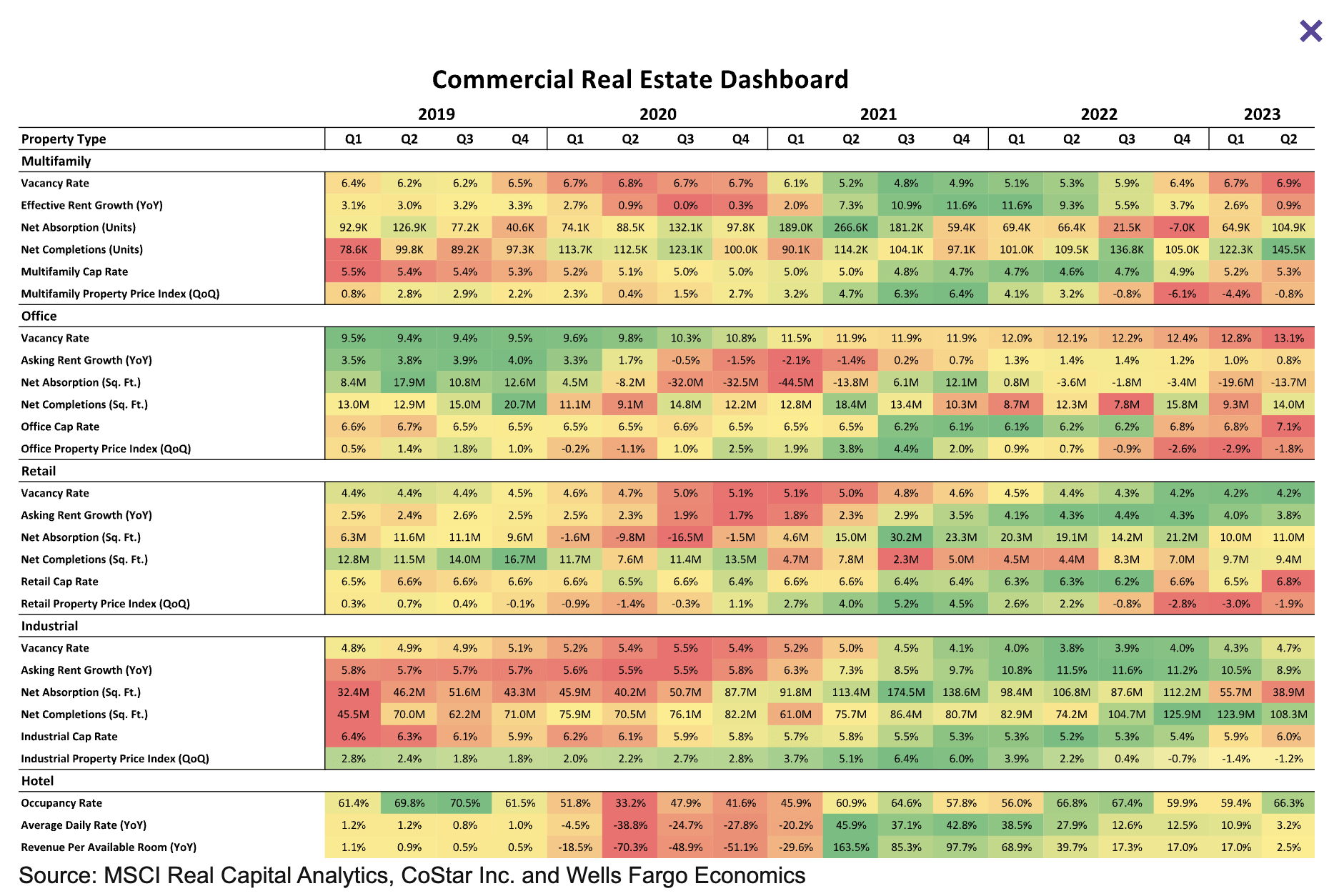

Fundamental conditions in the CRE market are softening, with vacancy rates either stable or rising and rent growth slowing.

Yet, the resilient economy continues to support demand for space, particularly in the apartment market, where net absorption has improved.

- In the retail sector , demand remains steady, but the shift from goods to services spending and limited available space impact leasing activity.

- The industrial sector , which initially thrived during the pandemic, is now dealing with moderating demand due to normalized trade flows and an uncertain consumer outlook.

The overview below (it’s a great cheat sheet we’ll use in future articles as well) confirms these comments. New supply has increased the vacancy rate in multifamily residential real estate.

The office segment saw a new multi-year high in its vacancy rate (13.1%). Asking rent growth fell below 1.0% again, as the cap rate now exceeds 7.0%.

The office market is undergoing a transformation with the rise of hybrid work models. While there's a push to get workers back post-pandemic, office occupancy remains at around 50-60% of pre-pandemic levels .

Many companies are downsizing, leading to increased vacancy rates and putting downward pressure on rent growth.

Case in point, my publishing business (Wide Moat Research / Legacy Research) occupies 25% of our corporate office space in Delray Beach, Florida.

Retail did well.

The other day, we wrote an article mentioning that more than 1,000 net new stores are opening in the U.S. This is reflected in these numbers.

Despite a weak consumer, retail remains strong . Asking rent growth remains close to 4.0%. The vacancy rate has been unchanged since 4Q22 and in a downtrend since 4Q20.

As aforementioned, industrial demand is weakening , pushing the vacancy rate to 4.7%. However, rent growth remains robust at 8.9%, albeit below the double-digit rates of the past five quarters.

The hotel sector faces challenges with softening demand, reflecting changes in remote work and sluggish business travel recovery. Average daily rates and revenue per available room growth have also cooled, although they remain positive.

{kind=link}

So, what about credit quality?

On September 9, we wrote that we’re closer to a debt doom loop.

" However, unless the Fed lowers rates soon, we could be looking at a doom loop. Prices are falling, and nobody is buying and selling. No new debt is fueling a debt-fueled boom.

This could end in much lower prices before buyers return.“

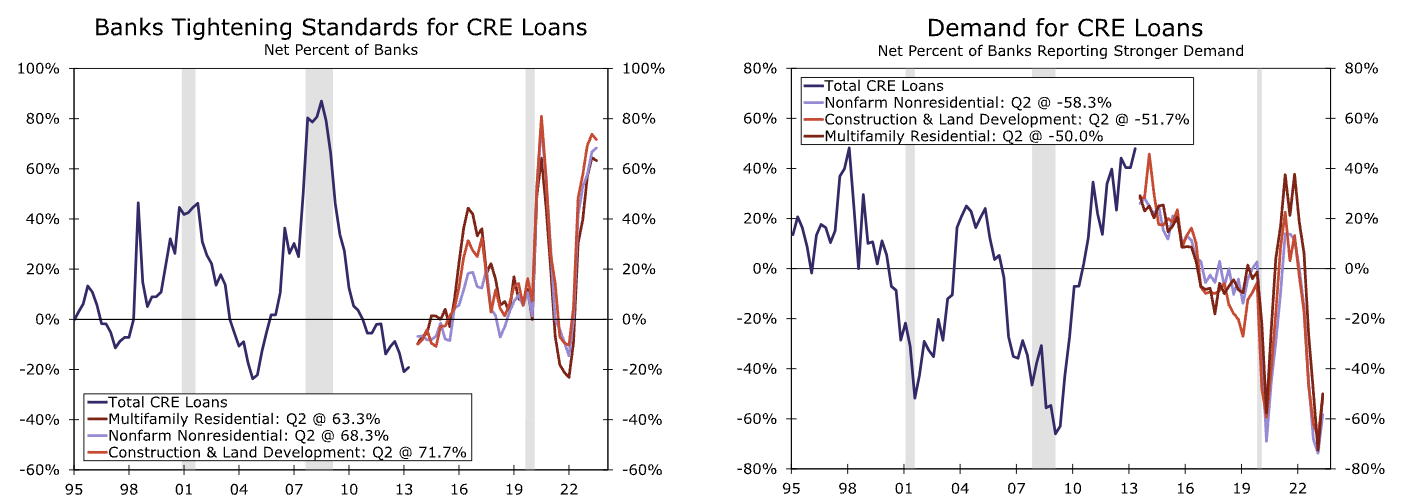

Commercial real estate has been affected by tighter lending standards.

According to the Federal Reserve's Q2 Senior Loan Officer Opinion Survey, a significant percentage of banks reported tightening lending standards for construction and land development loans, as well as nonfarm nonresidential loans.

This tightening indicates a more cautious approach by lenders in extending credit to CRE projects.

{kind=link}

As we can see in the chart above, the tightening of lending standards has been accompanied by a decrease in demand for CRE loans.

While there was a marginal improvement in the net share of banks reporting stronger demand for CRE loans in the second quarter, over half of senior loan officers still reported weaker demand for CRE loans in 2Q compared to 1Q.

This decline in demand reflects the challenges faced by borrowers in accessing financing for CRE projects.

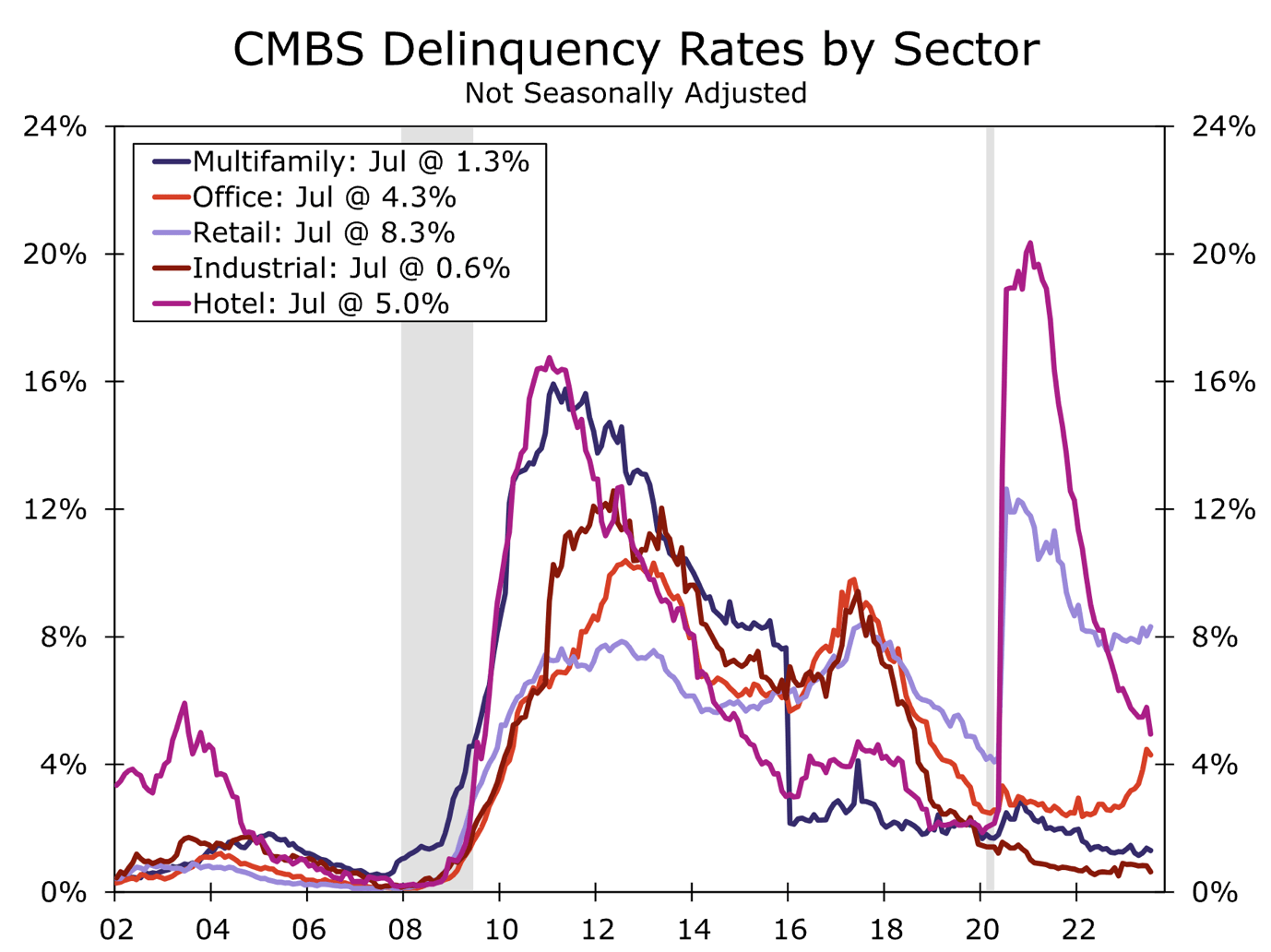

CMBS delinquency rates have also played a role in influencing credit availability and lending.

Office and retail segments have experienced significant increases in delinquencies, which can further tighten credit availability in these sectors as lenders become more risk-averse.

This confirms what we have discussed in prior articles as well.

{kind=link}

Overall, credit availability and lending in the commercial real estate market have been characterized by tighter lending standards, reduced demand for CRE loans, and varying impacts of CMBS delinquencies on different property types.

These dynamics reflect the cautious approach of lenders and the challenges faced by borrowers in securing financing for CRE projects.

This is what the Wall Street Journal reported in this the other day:

“Even the biggest banks are feeling the pressure. Bank of America said that, at higher required capital levels, it would have to evaluate things such as how many unused credit lines it can offer.

JPMorgan Chase Chief Executive Jamie Dimon said the new set of capital proposals by the Fed implies that “certain things should not be held in the banking system. That’s what it means. Almost all loans are bad.” The proposal includes higher risk-weightings for loans such as certain types of mortgages.”

Unless Rates Fall, There’s More Downside For Prices

So, how bad are things really?

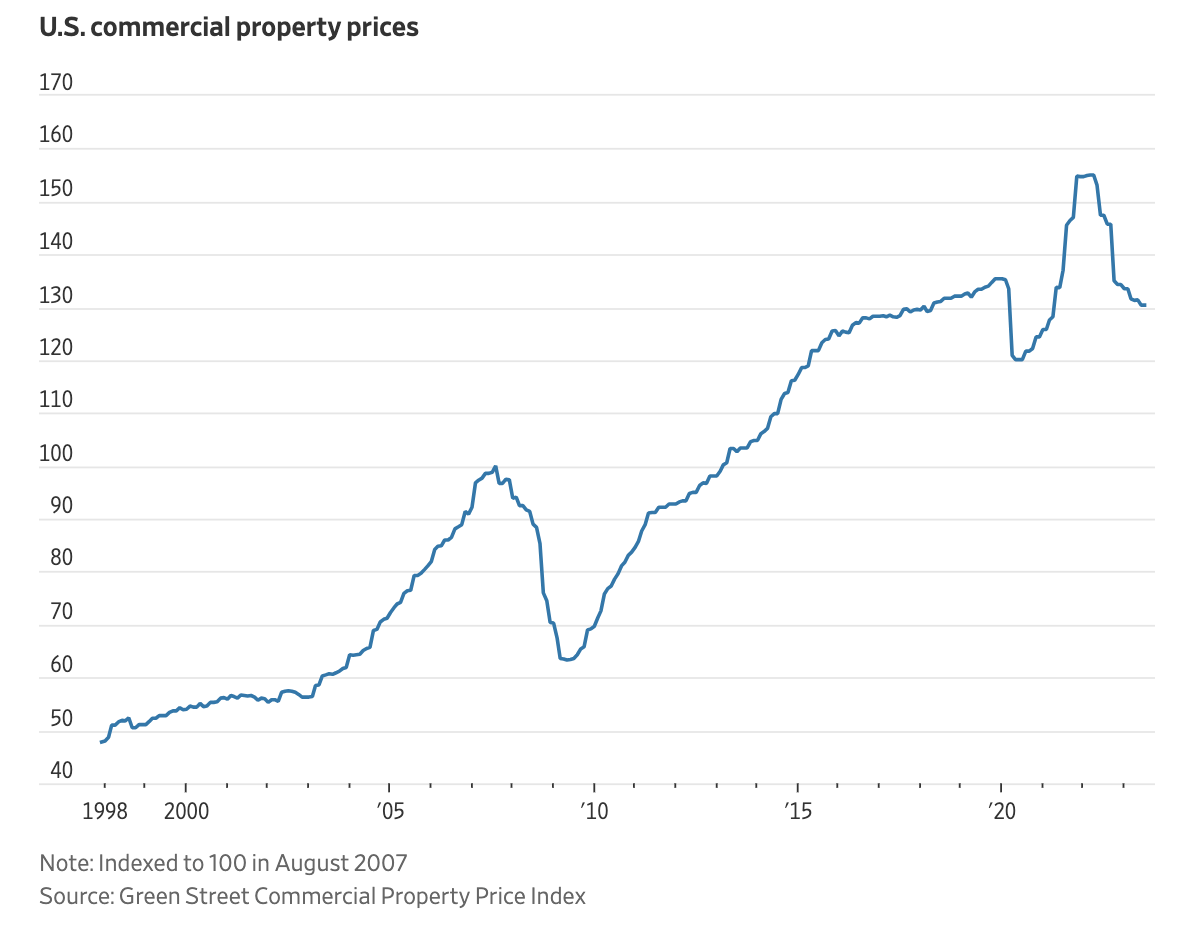

On August 30, the Wall Street Journal wrote an article titled How to Play the Property Meltdown in Five Charts .

First of all, calling it a meltdown at this stage is quite interesting. Cracks are appearing, but is it really a meltdown?

According to the paper, since March 2022, U.S. commercial property prices have already seen a substantial 16% decline on average. That’s bad, but it’s nothing more than a normalization at this point. After all, we can argue that the post-2020 surge wasn’t sustainable.

{kind=link}

Unlike the 2008 financial crisis, the impact varies significantly across property types. Offices, for instance, have taken the hardest hit, experiencing a 31% drop in value due to the shift towards remote work.

Nonetheless, this discount might not be as appealing, as many office buildings require substantial investments to attract tenants or undergo redevelopment .

In contrast, the prospects of obtaining discounted e-commerce warehouses appear slim, as warehouse values have only declined by 8%, reflecting higher financing costs.

According to the paper, for those interested in distressed assets, multifamily apartment buildings may present a better opportunity, with prices having fallen by 20% since March 2022.

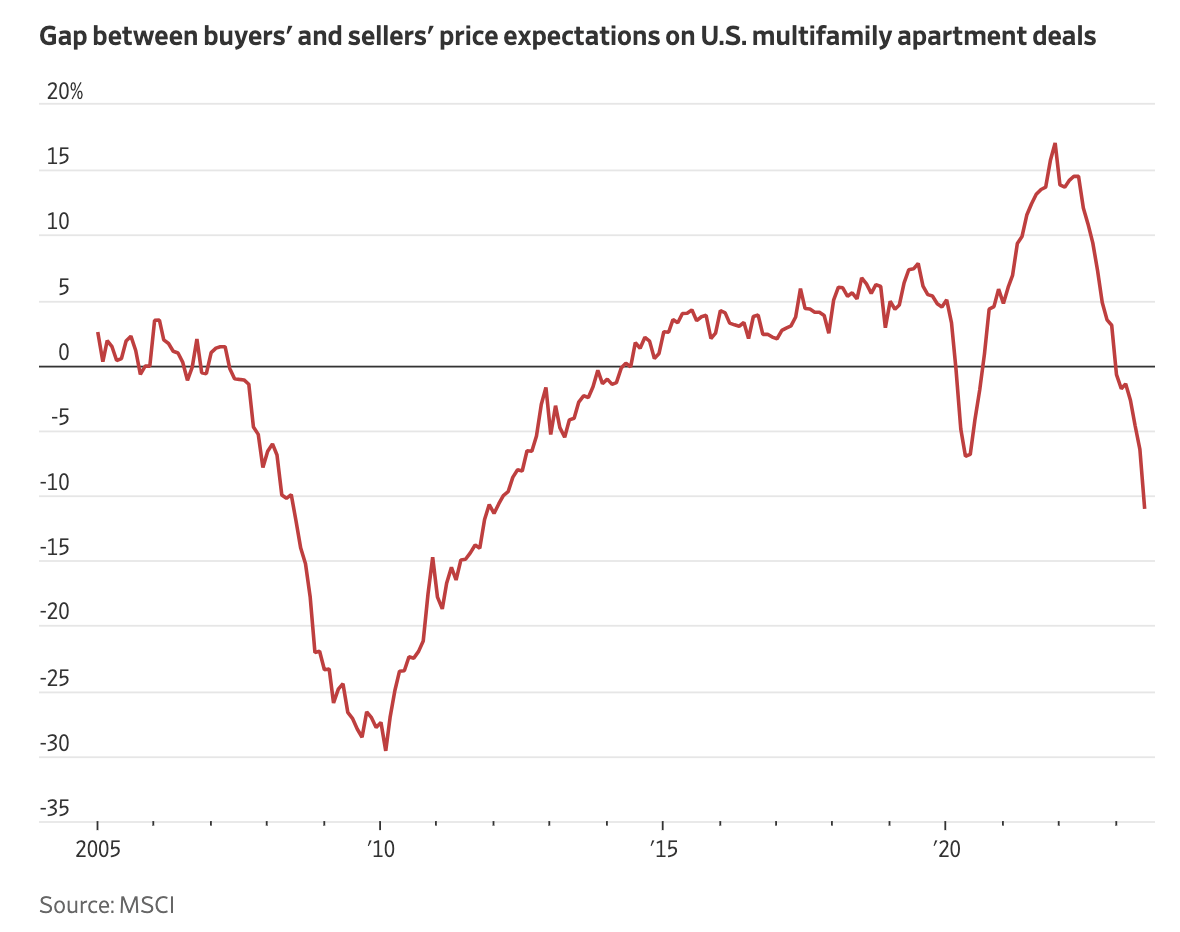

Some property owners who acquired assets during the pandemic using short-term, floating-rate debt may be forced to sell as mortgage repayments become unmanageable when interest rate hedges expire.

Furthermore, a significant challenge in the market is the gap between what sellers are demanding and what buyers are willing to pay. As of July, this gap reached 11% for multifamily apartments, the widest since early 2012.

Office and retail properties are experiencing a slightly narrower gap of around 8%, while industrial warehouses have the smallest disparity, with sellers seeking just 2% more than buyers are willing to pay.

We believe these numbers reflect the developments we discussed in the first part of this article.

However, it also shows what is going on in the market with regard to rates, as sellers are unwilling to sell unless they get a good price. Buyers need better deals as funding costs have risen.

{kind=link}

Hence, one of the biggest risks is maturing debt.

Maturing debt could lead to refinancing issues, forcing some sellers to accept lower prices.

This is one of the biggest risks that is unfolding very slowly at the moment. It can be stopped by rapidly declining rates, which seems to be unlikely at this point.

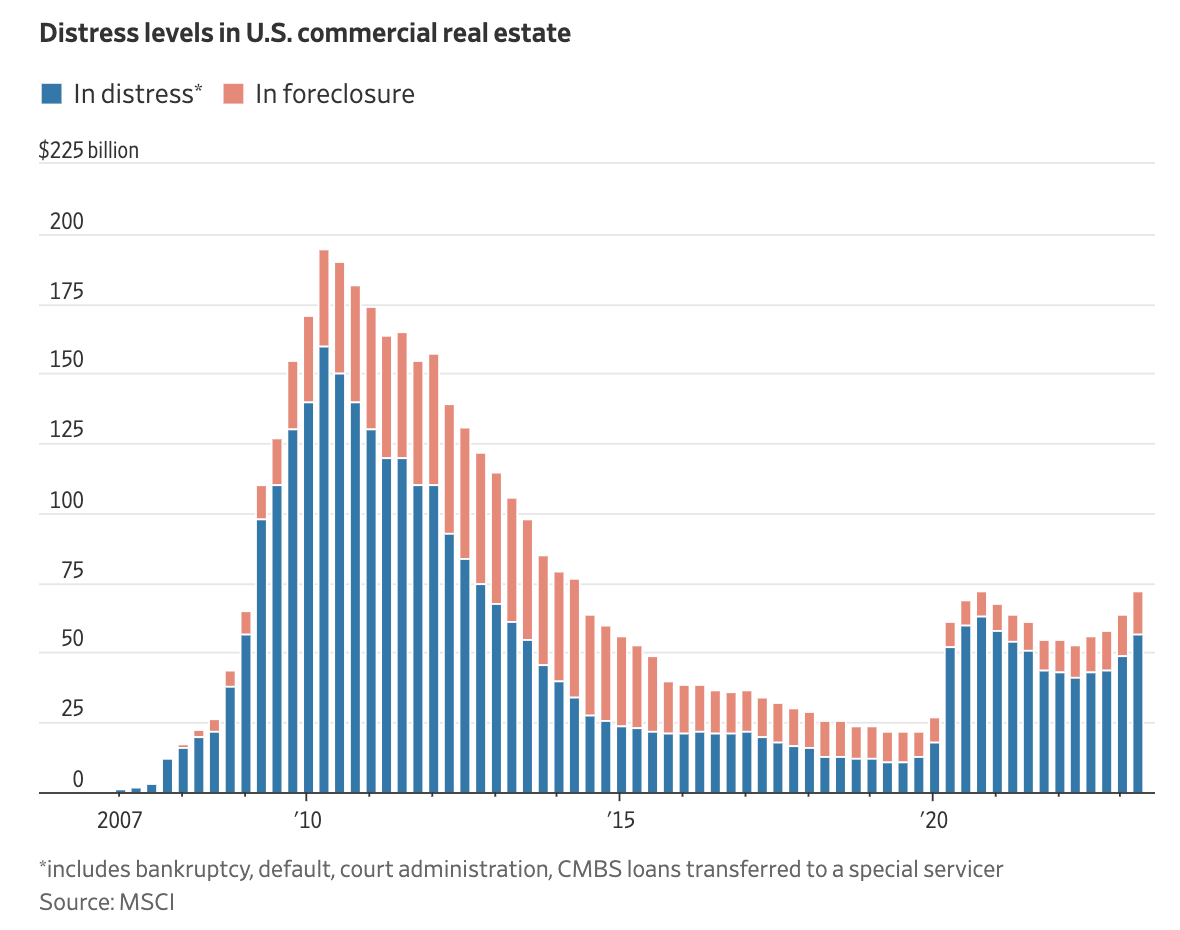

As a result, we’re seeing increasing defaults.

The value of distressed U.S. properties, including those in default or special servicing, is on the rise, with an additional $8 billion of assets falling into distress in the second quarter, bringing the total to $71.8 billion.

When considering properties at risk, the pool of potentially troubled assets is even larger.

{kind=link}

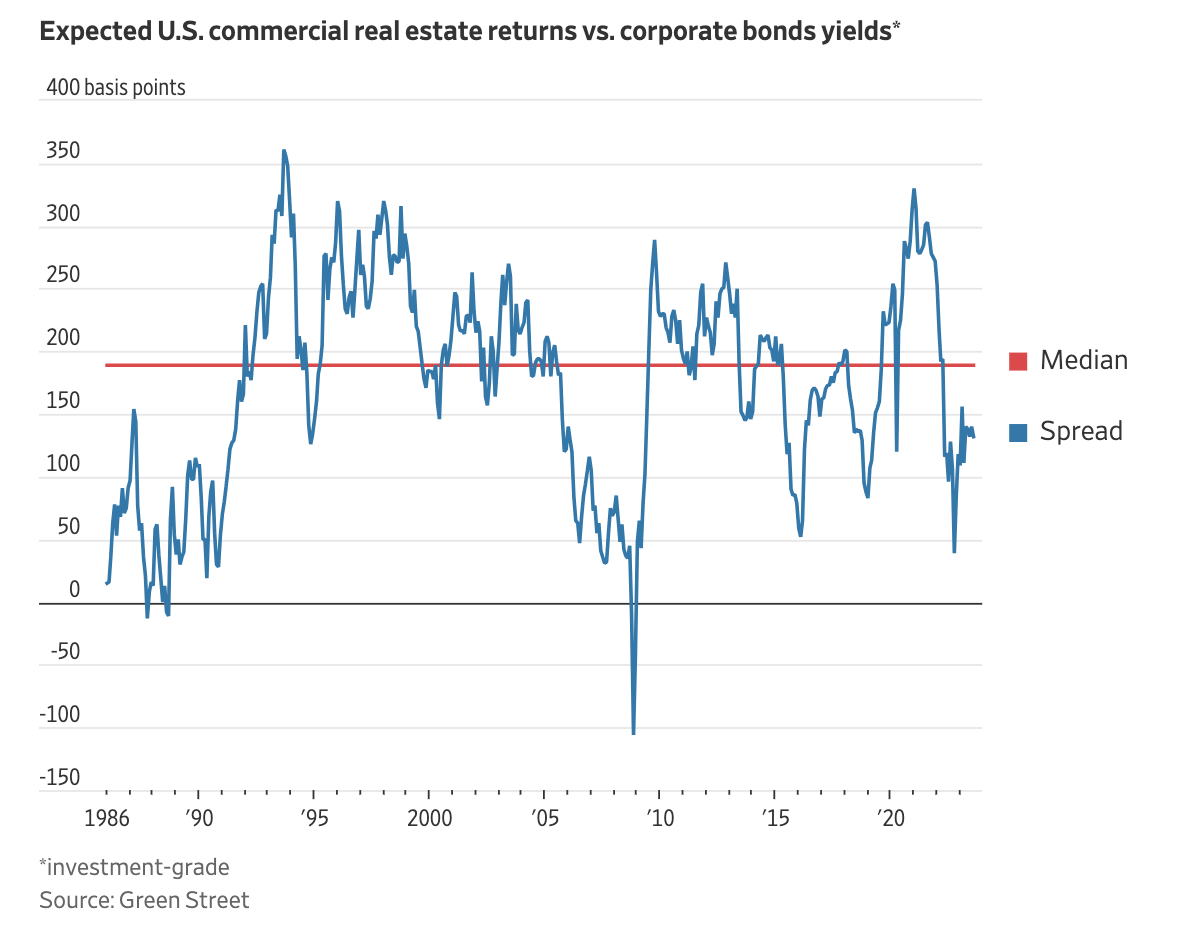

In order to gauge the future of the commercial real estate market, the Wall Street Journal makes the case that it's essential to monitor the relationship between U.S. real estate prices and investment-grade corporate bond yields.

Currently, the yield premium for real estate is lower than historical levels, indicating that U.S. real-estate prices need to drop an additional 10% to 15% to become more attractive to investors .

{kind=link}

So, does it mean we’re panic selling?

Our Gameplan

We have zero shorts.

We also haven’t sold a penny of investments (REITs and others).

Although there is no denying that the current situation is tricky (we’re all feeling the pain through falling REIT stock prices), the good news is that weakness comes with opportunities.

Over the past few quarters, we’ve discussed a wide number of opportunities as we believe that buying great stocks at great prices beats panicking during downturns.

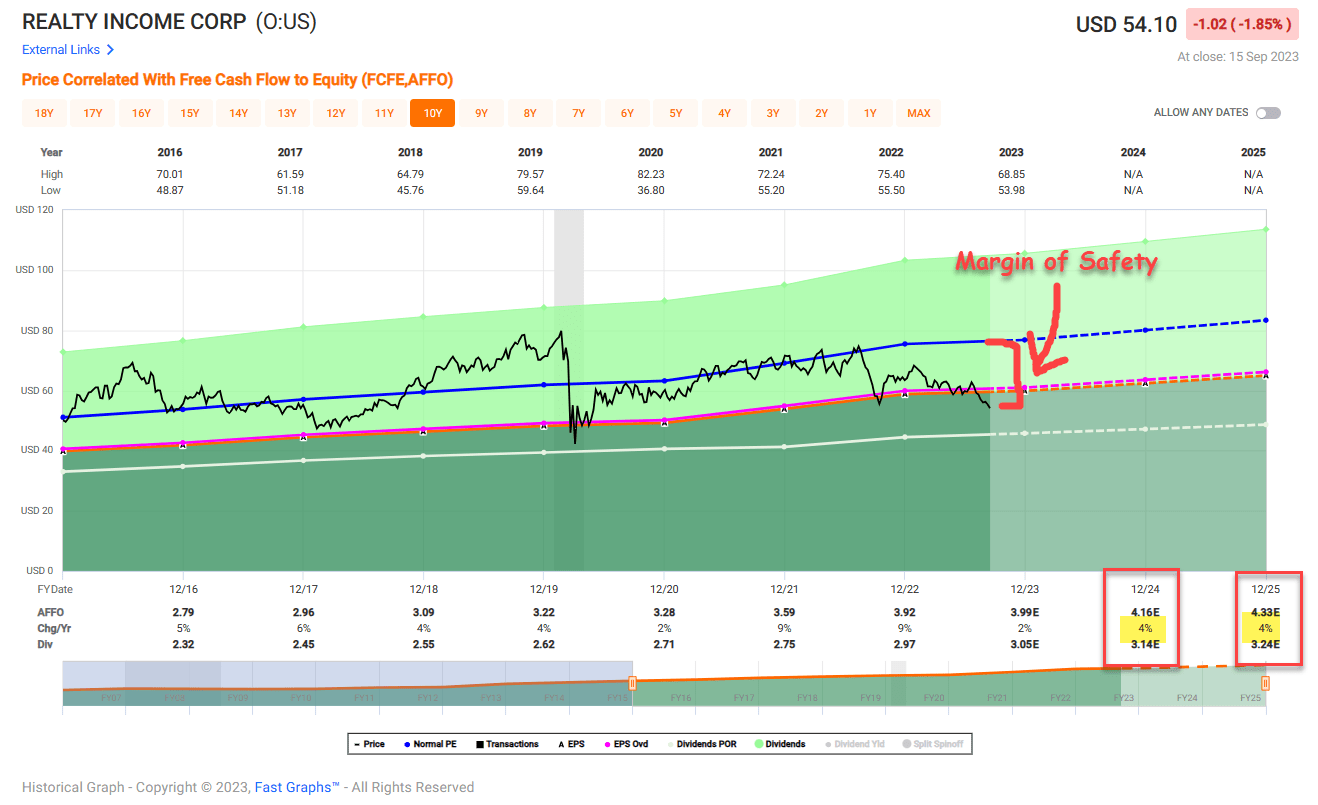

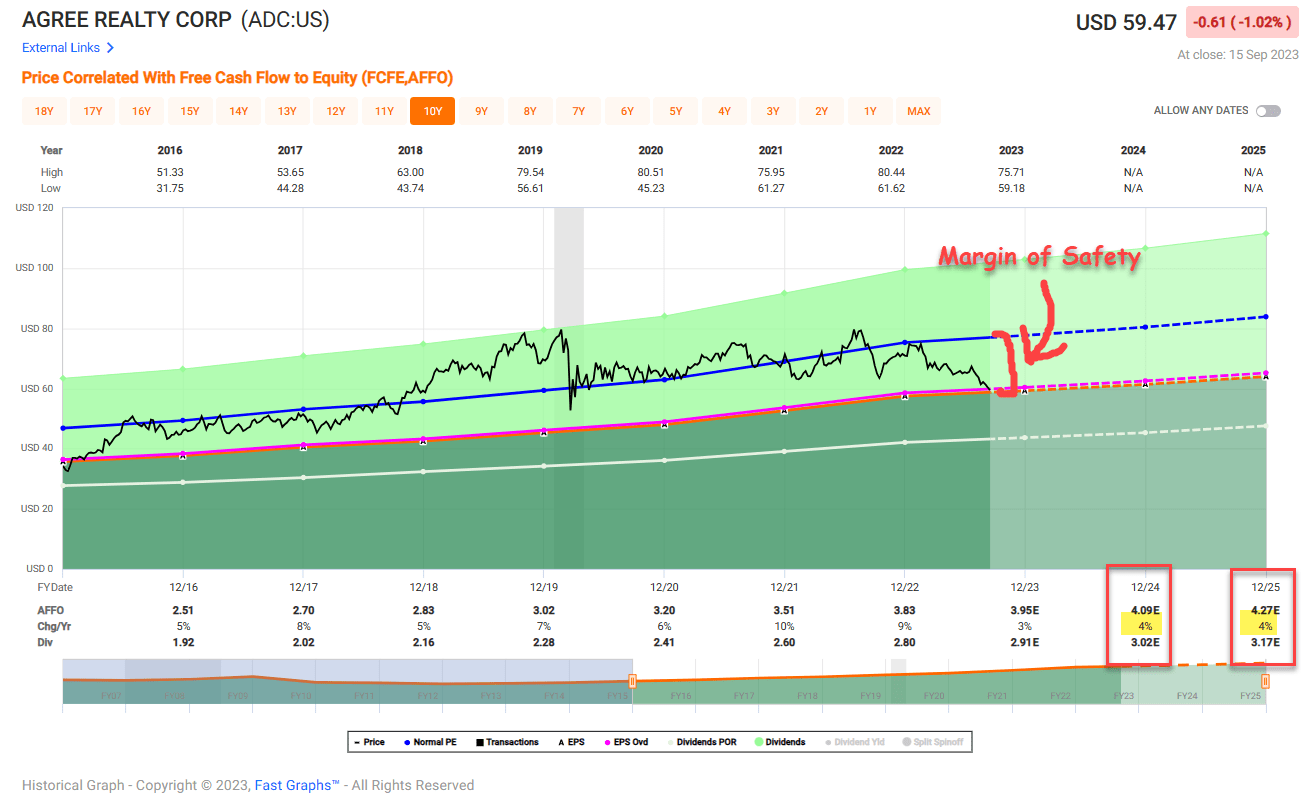

We have aggressively added to self-storage and net lease REITs like Realty Income ( O ) and Agree Realty ( ADC ).

Realty Income

{kind=link}

Agree Realty

{kind=link}

We prefer companies with healthy balance sheets, secular growth tailwinds, and the ability to maintain high long-term dividend growth to offset potentially sticky inflation.

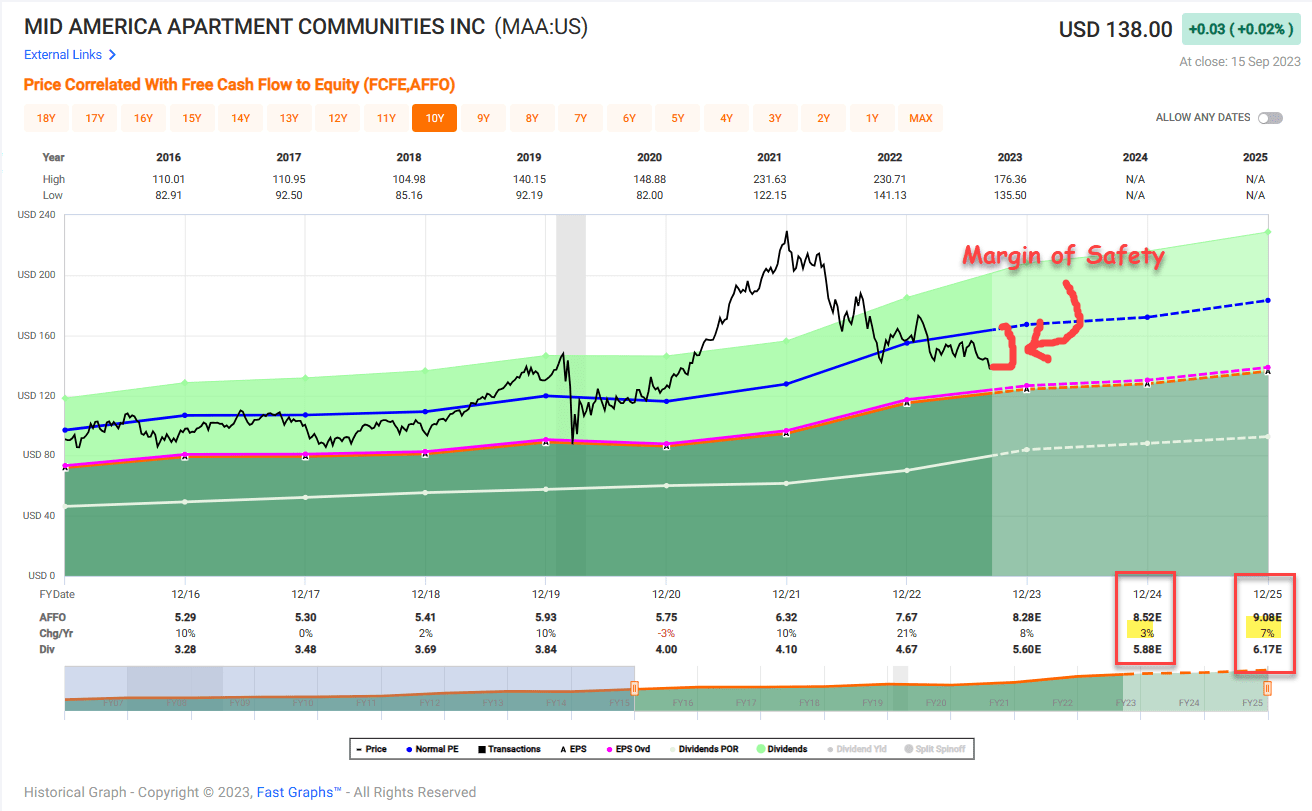

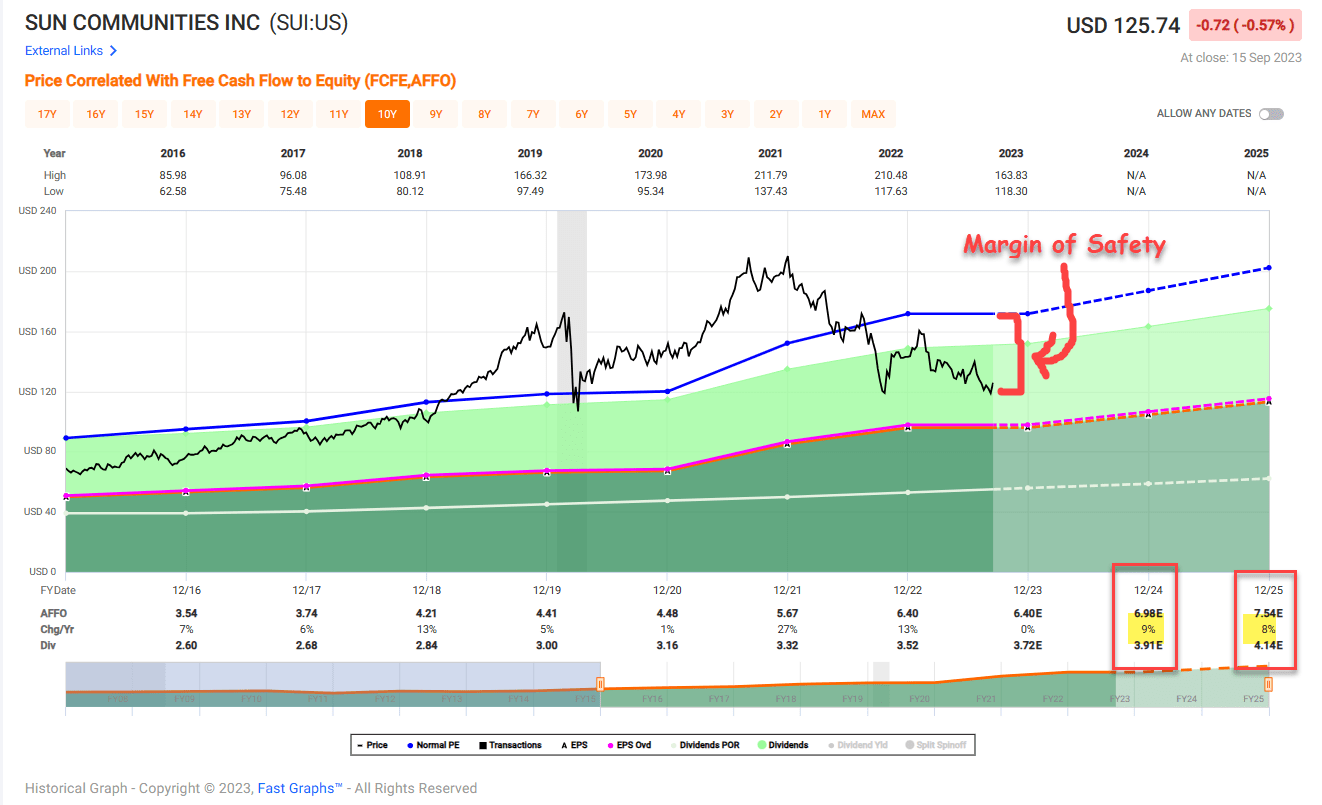

We're also looking for opportunities in the industrial REIT space and residential sector. Stocks on my radar include Rexford Industrial Realty ( REXR ), Mid-America Apartment Communities ( MAA ), Equity LifeStyle Properties ( ELS ), Sun Communities ( SUI ), Prologis ( PLD ), and others.

MidAmerica Communities

{kind=link}

Sun Communities

{kind=link}

However, we hold a slightly bigger cash position, and we have increased our savings rate and invested less in recent months. This way, we hope to capitalize a bit better on potential downside pressure on the market (and REITs).

Again, we're not predicting the Great Financial Crisis.

However, odds are we might encounter some better buying opportunities down the road.

Through owning top-tier REITs that can withstand any serious macro environment and slightly increasing my war chest, we believe we're protected against anything the market throws at us without sleeping badly at night.

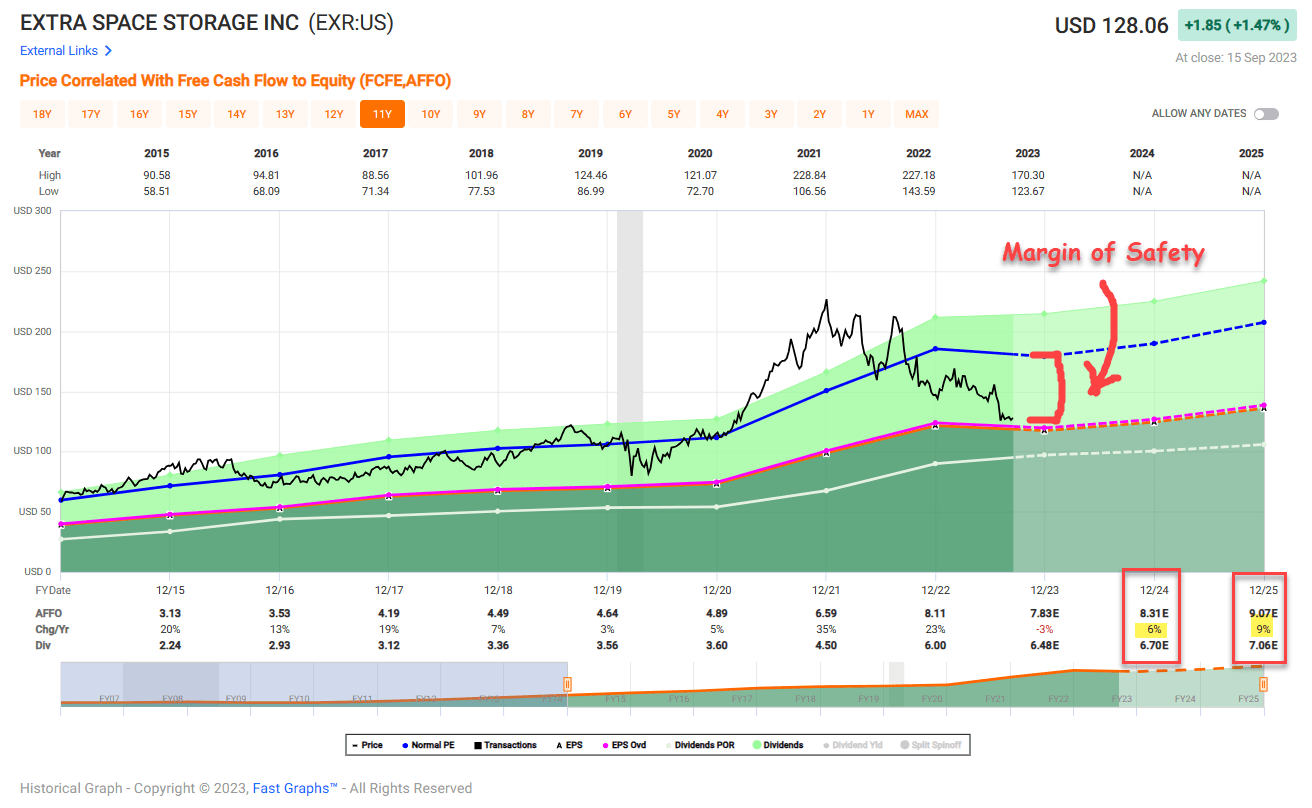

After all, my EXR position is currently down almost 18%, and I haven’t worried about it for a second, as I can add to this BBB+-rated gem at a yield of more than 5% - to give you an example of what I like about investing in this environment.

Extra Space Storage

{kind=link}

Needless to say, I and the entire team will spend the next few months and quarters finding great opportunities that will protect us in potentially tough times and attractive buying opportunities to put some of our hard-earned cash to work.

Takeaway

Cracks are appearing in the commercial real estate market, with declining property values, rising vacancy rates, and shifting demand across various sectors.

The softening fundamentals are a cause for concern, especially as energy prices continue to surge, potentially keeping interest rates high.

Lending standards have tightened, impacting credit availability, and maturing debt is becoming a growing concern. This slow-burning issue could lead to more defaults unless rates decline significantly, which appears unlikely.

However, amid these challenges, there are opportunities . The key is to focus on quality assets with strong balance sheets and potential for long-term dividend growth.

While uncertainties loom, maintaining a diversified portfolio and a cash buffer can provide some protection against market turbulence. So, while it's not time for panic, it's a time for vigilance and strategic planning.

As we navigate these market dynamics, we'll continue to seek out opportunities that offer both protection and growth potential.

Stay informed.

Stay adaptable.

Stay prepared.

And above all, don’t stress out...

Sleep Well at Night!

Note: Brad Thomas is a Wall Street writer, which means he's not always right with his predictions or recommendations. Since that also applies to his grammar, please excuse any typos you may find. Also, this article is free: Written and distributed to assist in research while providing a forum for second-level thinking.

For further details see:

Risks Are Real And REITs Are A Steal (How We Play The Sector)