RISR - RISR: A Performing MBS Fund In A Highly Volatile Market

2023-07-10 13:16:19 ET

Summary

- The FolioBeyond Alternative Income and Interest Rate Hedge ETF (RISR) focuses on interest-only mortgage-backed securities (MBS IOs) and US Treasury bonds, with an active management strategy.

- RISR has performed well against relevant equity and bond indices since its inception in 2021, but reports a high volatility level and has a high expense ratio of 1%.

- Despite its potential, the fund's outlook is uncertain due to the volatility of MBS IOs and the broader agency MBS market, leading me to rate RISR a Hold.

The FolioBeyond Alternative Income and Interest Rate Hedge ETF ( RISR ) invests in fixed income markets in the United States. The fund primarily focuses on interest-only mortgage-backed securities (MBS IOs) and US Treasury bonds. RISR was launched and managed by Toroso Investments, LLC and employs an active management strategy with priorities in diversification, income generation, and interest rate risk mitigation. Moreover, RISR is a new and small fund, having launched in 2021 and only accumulating an AUM of slightly over $56 million. The fund employs a proprietary method in selecting and weighting its holdings, and it seeks to benchmark its performance against the ICE U.S. Treasury 7-10 Year Bond 1X Inverse Index and the Bloomberg US Aggregate Bond Index.

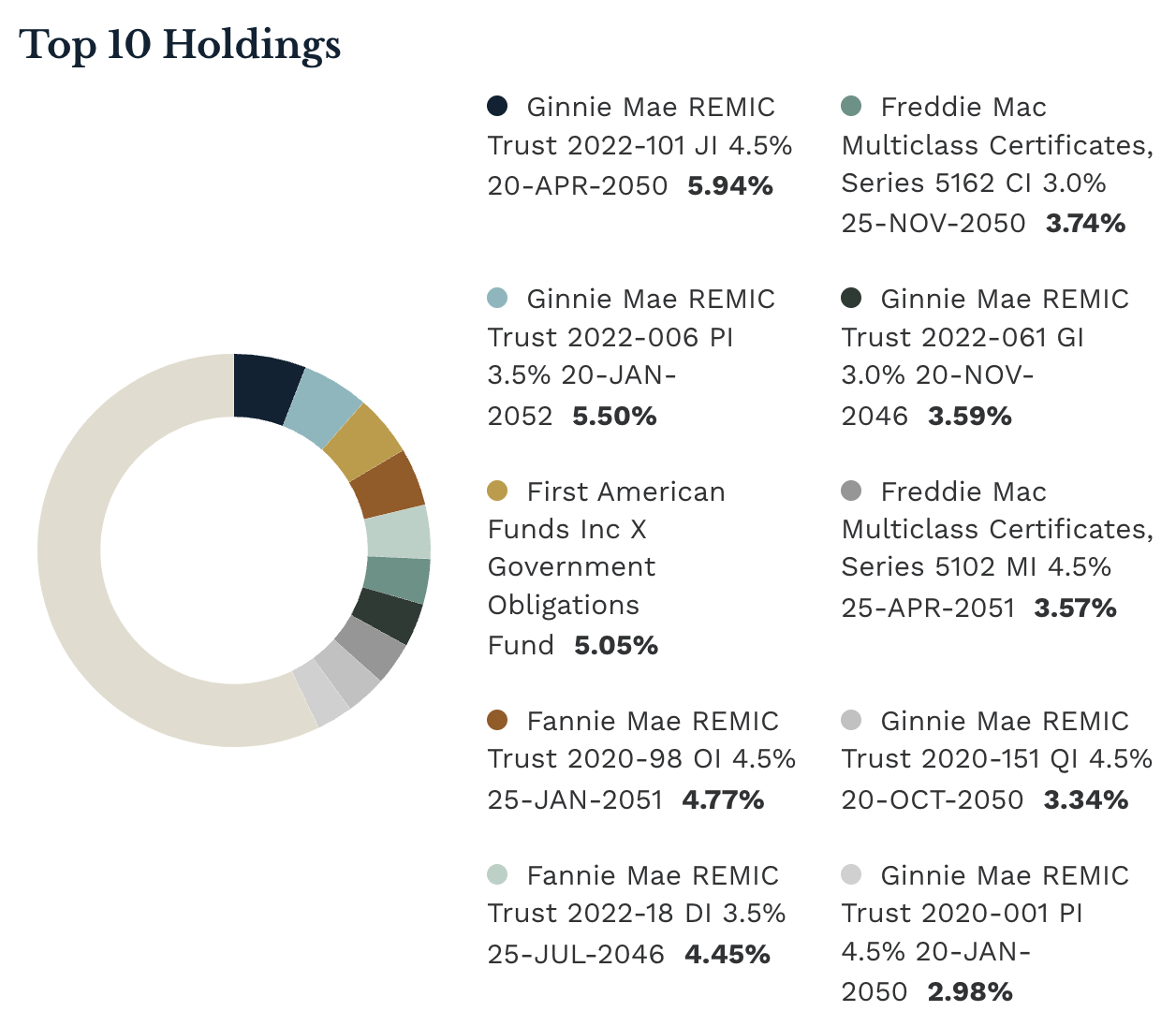

Holdings

While the fund invests primarily in mortgage-backed securities and US Treasury bonds, the fund also invests a considerable amount, 13%, in other ETFs and mutual funds. For instance, one such holding is the First American Funds Inc X Government Obligations Fund, with a weighting of 5%. RISR invests in a total of 56 holdings, and it allocates over 43% of its portfolio to the top 10 holdings. Moreover, the fund invests in 100% in AAA investment grade bonds with an effective duration of -7.65.

{kind=link}

Actively Managed Portfolio

RISR's main distinguishing strengths is its actively managed portfolio. The fund has 4 fund managers, 2 of which have over 25+ years of experienced in the fixed income and portfolio management spaces. In fact, among the fund's closest peer group of BND, AGG, BNDX, and BSV, RISR is the only interest only MBS and Treasury bond ETF to have an active management strategy. The other funds listed above all have passive management strategies. The fund employs this strategy with the goal of providing protection against rising interest rates while also generating income under stable interest rates. This is especially beneficial as the fund's managers can make timely decisions to buy and sell securities to capitalize on market trends.

The fund managers also employs a liquidity risk management program where it intends to manage the risk to prevent the value of their shares from decreasing. The program will assess liquidity risk under both normal and potential tougher market conditions in the near future. The risk is managed by monitoring the liquidity of a security within the fund, where it limits the amount of investments that are do not meet liquidity benchmarks. Because of this extensive strategy, the fund has an exceptionally high expense ratio of 1%, which is double that of the median of all ETFs.

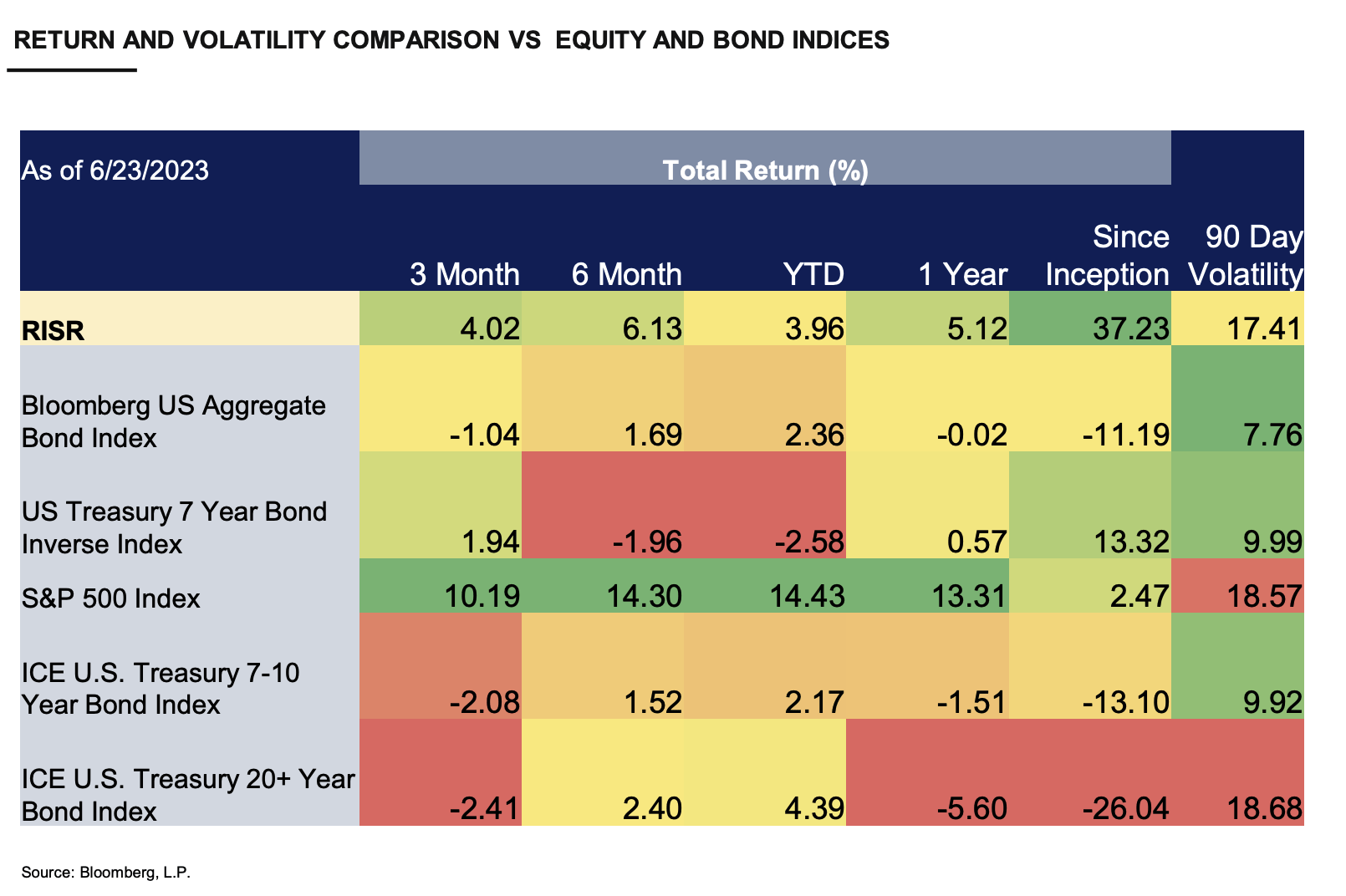

Performance Analysis Among Equity/Bond Indices

In terms of capital appreciation, RISR has performed exceptionally well against several relevant equity and bond indices over a variety of time frames, from '3 months' to 'since inception'. The Bloomberg US Aggregate Bond Index and the US Treasury 7 Year Bond Inverse Index are included in this comparison since these are the two indices that RISR seeks to benchmark its performance against. RISR has significantly outperformed these two indices in all time frames. While RISR has reported a total return rate of over 37% since its inception, the fund does report a 90-day volatility level of over 17% that is substantially larger than the two indices the fund seeks to benchmark. Moreover, the fund only falls short of the S&P 500, but this is pretty standard for all bonds in the nation's current economic environment of rising interest rates.

{kind=link}

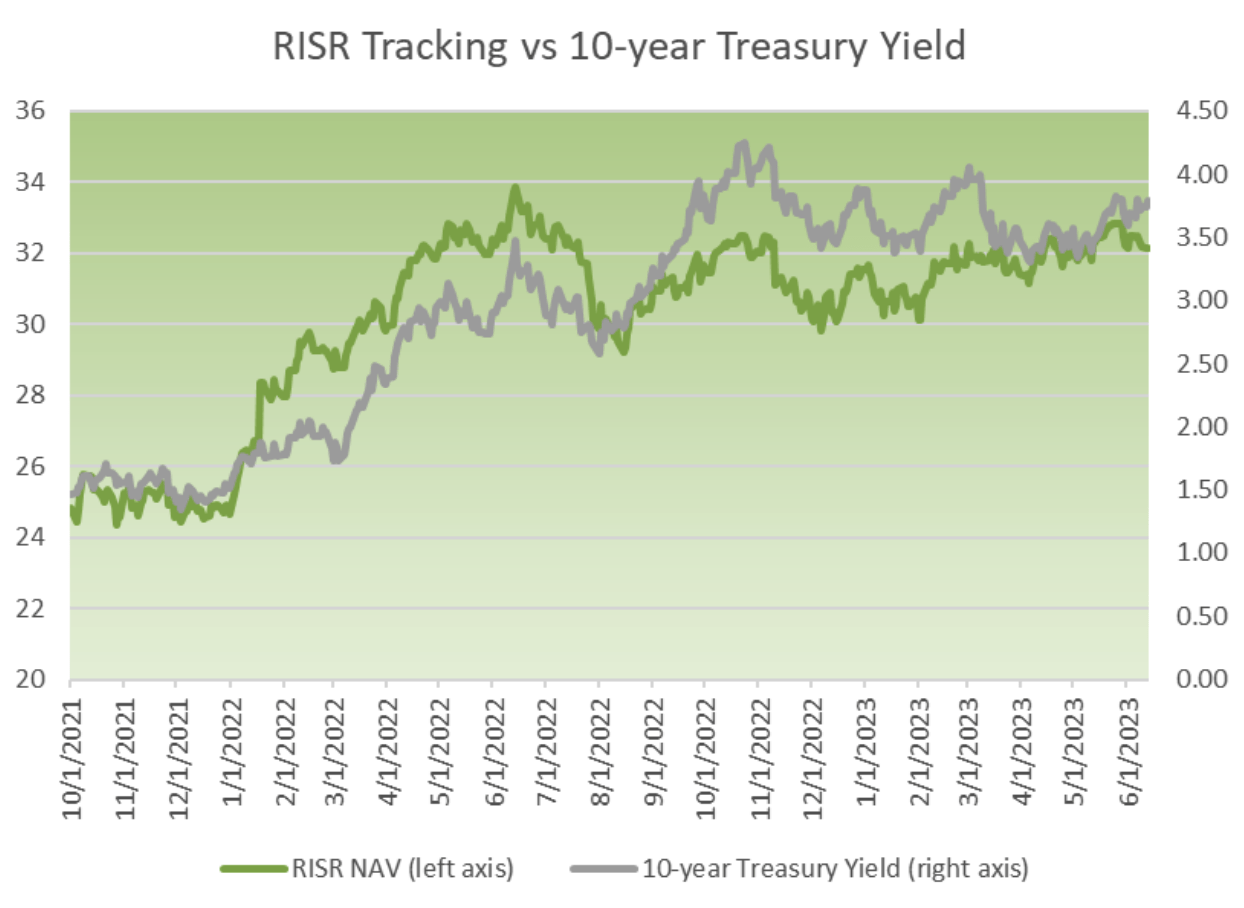

If we look at the Net Asset Value of RISR since its inception and compare it to the 10-year Treasury yield since the fund's inception, it seems that the yields and prices have similar peaks and troughs. RISR outperformed the 10-year Treasury yield at the onset of 2022 for a few months, but a slight crash in August 2022 has caused the fund to trail the Treasury yield since. However, this comparison provides an outlook of less than 2 years, and it should not be used to make any concrete conclusions on the patterns and behaviors of the fund against the 10-year Treasury yield.

{kind=link}

MBS Market Outlook

The MBS market is the second-largest debt market in the US, behind the US Treasury. Mortgage-backed securities are securitized through the agency MBS market, and Agency MBS returns were extremely volatile in 2022 as banks were limiting purchases of mortgage securities due to a decrease in deposits and consumer confidence in the banking sector. These securities were so volatile that they actually exceeded similar duration investment grade corporate bonds, which is historically very unusual for government guaranteed securities like agency MBS to have higher volatility than corporate bonds with default risk. BMO Capital Markets predicts that the total sales of fixed-rate mortgage bonds by government entities will nearly halve by the end of 2023 to $300 billion from an initial estimate of $550 billion in 2022. These securities depend very heavily on the performance of the housing market, a sector that experienced similar headwinds that the MBS market faced. With interest rates continuing to rise and a recession seeming more likely by the day, I am not bullish on residential real estate, let alone commercial real estate.

Final Thoughts

Overall, RISR is an extremely new and small ETF that I would not count off as an interesting opportunity for investors. The fund is distinguished in that it has great potential to capitalize on industry trends with its active management strategy, and it has also consistently outperformed its relevant broader indices that it seeks to benchmark given the time since its inception. However, given it was only launched in 2021, I will refrain from making concrete judgements based on its past performance.

I do not have a positive outlook for MBS at the time being. Interest only MBS are extremely more volatile than other mortgage-related securities, and this is also demonstrated by its high volatility levels compared to its relevant indices. Moreover, the broader agency MBS market is just as volatile and projections for the rest of 2023 do not seem favorable. I rate RISR a Hold.

For further details see:

RISR: A Performing MBS Fund In A Highly Volatile Market