RAD - Rite Aid May Be Forced Into Ch.11 Bankruptcy To Resolve Opioid Liabilities

2023-07-10 08:50:39 ET

Summary

- Rite Aid's stock is being downgraded from "Hold" to "Sell" due to the opioid lawsuit, ongoing financial losses, and ineffective management.

- Rite Aid reported a $(5.56) net loss per share for 1Q.

- Elixir will discontinue their Medicare Part D program for individuals starting next year.

- The stock is effectively trading at only about $0.08 after adjusting for the 1-20 reverse stock split a few years ago.

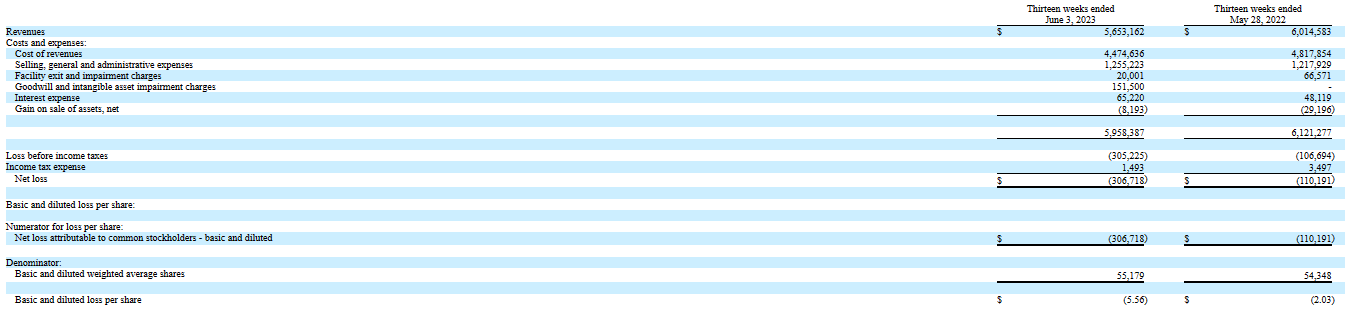

Shareholders of Rite Aid ( RAD ) most likely have been frequent customers of this pharmacy chain buying drugs to reduce their anxiety and depression because RAD stock price continues to plunge, and management seems that it is incapable of turning it around. Rite Aid continues to report massive losses. It reported a net loss per share of $(5.56) for 1Q compared to a RAD stock price of only $1.65. The federal opioid lawsuit could eventually force them into Ch.11 bankruptcy. Because of reasons stated in this article, I am downgrading RAD stock from a "Hold" to "Sell".

Management Has Not Been Effective

A major reason for the downgrade to "sell" is management. My prior "hold" recommendations were partially based on the potential to enact plans by management to keep them out of bankruptcy court. Management, however, is doing nothing. While the prior CEO is gone, the new one does not seem to be doing enough, in my opinion. As I wrote in my prior article , I expected that management would be able to raise a modest amount of cash via stock sales and also seek shareholder approval to increase the number of authorized RAD stock from the current limit of 75 million. Nothing so far.

The board of directors does not have even one member with expertise in restructuring. This is, in my opinion, totally unacceptable. Many companies that are financially distressed have at least one financial expert on their board. To make matters even worse, current board members own almost no RAD stock that they purchased in the market. The few RAD shares that they do own are just via some management payment program. They need some "skin" in the game besides their annual retainers to be aggressive and creative in developing an effective plan to keep this company out of bankruptcy. For example, board chairman Bruce Bodaken only owns 74,920 stock units that have vested or will vest before August 26, 2023. That is barely $100k. Many other board members own even less.

1Q Results and Updated Guidance Numbers Are Weak

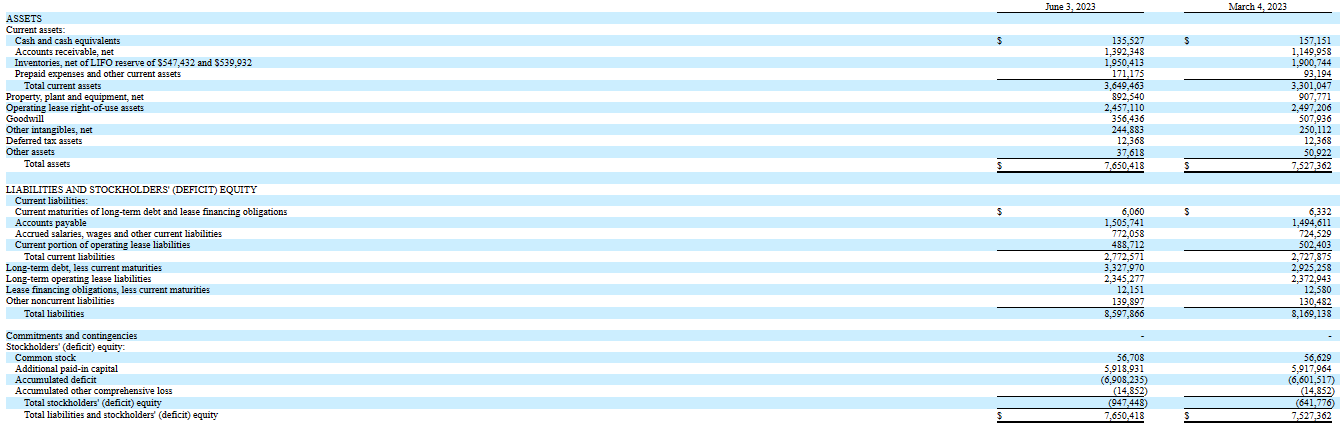

I have a few comments on their recent 1Q results and updated guidance numbers. At first glance the $400 million additional draw on their revolver and their $242 million increase in accounts receivable looks terrible, but it is not as bad as it seems. Bank of America ( BAC ) has an established program of periodically purchasing Rite Aid's accounts receivable. For example, BAC purchased $278.4 million accounts receivable last February at a 6% discount. I would expect future transactions in the near future that would generate cash to pay down part of the revolver. While the numbers are bad - they are not as bad as some have asserted.

First Quarter Balance Sheet

{kind=link}

sec.gov

First Quarter Income Statement

{kind=link}

sec.gov

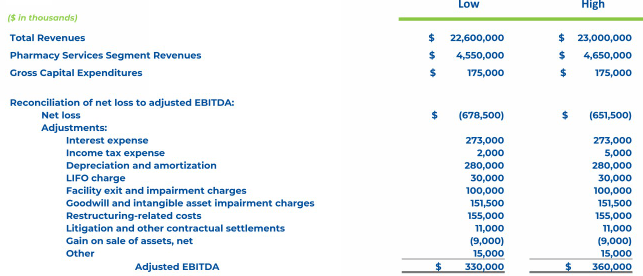

Their adjusted EBITDA guidance of $330 million - $360 million for this fiscal year is much lower than their actual $429 million EBITDA last year. Last year at this time they guided for $460 million - $500 million for the year ending in March 2023. I think that their current guidance numbers may again be too optimistic. Given that their interest expense guidance is $273 million, which is much higher than actual interest expense of $224 million last year, they are getting closer to not covering interest expenses from adjusted EBITDA, especially if interest rates continue to increase this year and their actual operating results are worse than forecasted. Using their low EBITDA guidance of $330 million and interest expense guidance of $273 million, the interest coverage is only 1.21x compared to 1.91x last year. In addition, debt is almost 10x EBITDA guidance. If vendors become stricter in their terms because they worry about Rite Aid's financial condition, Rite Aid may have to increase their borrowing on their revolver to support needed inventories, which would further increase interest expenses.

Fiscal Year 2024 Guidance

{kind=link}

sec.gov

Elixir Discontinuing Medicare Part D for Individuals

Management stated during the recent conference call that after January 1 2024 Elixir would longer offer Medicare Part D for individuals, but it will still offer Part D under group plans. Letters to individuals will be sent in September or October informing the individuals that Elixir will no longer offer Part D and that they will have to select a different provider during the annual enrollment period. They were already moving away from the individual Part D market over the last 3 years, and they were expecting some new regulations that could have a negative impact. I think there is some P.R. risk here. Current customers might become annoyed by being dropped and that any press reports on Rite Aid dropping individuals could be negative. Rite Aid does not need any more negative press. It is already having negative press about how they handle shoplifting.

Rite Aid purchased EnvisionRx (name was changed to Elixir) in 2015 for $2.0 billion ($1.8 billion cash and about $200 million RAD stock), which seems to have been a major mistake. The results have been very disappointing and last year Rite Aid had a $229 million impairment charge related to Elixir.

Federal Opioid Lawsuit

The opioid lawsuit against Rite Aid could be the catalyst that sends them into Ch.11, which would most likely wipeout investors. This opioid liability risk has been hanging over Rite Aid for the last few years as other companies have agreed to pay billions under settlements.

On March 13, 2023, the U.S. filed a complaint ( copy of the 75-page complaint docket 38 ) against Rite Aid [U.S. ex rel. White et al. v. Rite Aid Corp., et al., No. 1:21-cv-1239 (N.D. Ohio)]. The complaint asserts five counts:

1) False Claims Act: Submission of False Claims: 31 U.S.C. § 3729(a)(1A)2) False Claims Act: False Records or Statements: 31 U.S.C. § 3729(a)(1B)3) Unlawful Dispensing of Controlled Substances 21 U.S.C . §§ 829, 842(a)(1), 842(c)(1A), and 21 C.F.R. § 1306.04 4) Payment by Mistake of Fact5) Unjust Enrichment

No specific amount was mentioned in the complaint, but other pharmacy chains have settled for billions. CVS Health ( CVS ) settled for about $5 billion payable over 10 years and Walgreens Boots Alliance ( WBA ) settled for $5.7 billion payable over 15 years. These companies are relatively strong financially, but Rite Aid has no cash or even expected future cash flow that could be used for a settlement or judgment. They spend $273 million annually (fiscal 2024 guidance number) to pay interest on debt that could be partially used for annual cash settlement payments - assuming Rite Aid had no or little debt. The reality is their operations do not generate enough cash to pay both interest expenses and potential opioid settlement payments. Ch.11 bankruptcy could cancel all their debt. For example, Mallinckrodt plc ( MNK ) used Ch.11 bankruptcy process (reorganization plan docket 7670 ) to help resolve their opioid liabilities.

Some investors may counter that I am too pessimistic. They assert that Rite Aid could fight this in court and win. That, however, takes a lot of cash to pay legal fees, which Rite Aid does not have. If one actually reads the complaint, it seems that the government has a very strong case. These investors further assert that even if there is a judgment against the company it could then file for Ch.11 and the automatic stay section 362 would prevent the government from seizing assets for judgment payments. They additionally assert that the judgment might be classified just as an unsecured claim, a fairly low priority claim, which would, in theory, mean holders of 1lien and 2lien debt would get recoveries before the government under a Ch.11 reorganization plan. Interesting. This all ignores the fact that over 38% of Rite Aid prescription sales are from Medicare Part D. If the reorganization plan allows for just a token payment for the government's judgment claim could the government then disallow payments to Rite Aid for Medicare Part D prescriptions? This clearly gets very complicated and very expensive paying huge legal fees.

I am expecting a rather difficult bankruptcy process because not only will they have to negotiate typical restructuring but negotiate acceptable settlements with various parties over asserted opioid liabilities. If Elixir Insurance is included in the bankruptcy filing, they would have additional complex issues associated with an insurance company bankruptcy. The only "winners" will most likely be lawyers. I would expect that RAD shareholders and unsecured noteholders would receive no recovery with 1lien debt holders getting the equity of the new reorganized Rite Aid under a Ch.11 reorganization plan. It seems unclear what, if any, 2lien debt holders would get and that could be a major hurdle negotiating a plan because 34% of their debt is 2lien.

I would expect that an opioid trust would be created under a Ch.11 reorganization plan that receives significant payments (over $100 million per year) over a 10–15-year period from the new Rite Aid. Because all or almost all of their debt (over $3.3 billion) most likely would be cancelled in bankruptcy, they would be able to afford to make timely payments into the opioid trust instead of making interest payments. The biggest hurdle, of course, is negotiating the specific amount of an opioid settlement.

Long-Term Debt

sec.gov

It is unclear if they will be in violation of any debt covenants in the near future and there is no debt maturing until July 2025. Rite Aid's finances, however, continue to get worse. If the opioid lawsuit does not force them into Ch11, their debt maturities starting in 2025 will, in my opinion, be very difficult to roll-over, which could force an in-court restructuring.

Why I Am Downgrading from Hold to Sell

Rite Aid stock is down about 92% since I recommended selling it in early 2021. Some of my more recent articles I had "hold" recommendations because I expected that management might be able to enact an effective turnaround. The reality to many long-term RAD shareholders is that the stock is selling at only about $0.08 per share after adjusting for a 1-20 reverse stock split a few years ago and they effectively have $59.29 long-term debt per RAD share. I am again recommending selling RAD for the following reasons:

1) Management is not doing enough to avoid bankruptcy.

2) Recent results and updated guidance numbers reflect a continued downward path.

3) The opioid lawsuit could force them into Ch.11 bankruptcy.

4) The July 2025 maturity of 2lien notes is getting closer.

For further details see:

Rite Aid May Be Forced Into Ch.11 Bankruptcy To Resolve Opioid Liabilities