SCU - Rithm Capital: Caught In A Sculptor Bidding War With Bill Ackman (Rating Downgrade)

2023-08-24 08:16:18 ET

Summary

- Rithm Capital is engaged in a bidding war with a hedge fund consortium over the acquisition of asset manager Sculptor Capital.

- The market's reaction to the merger announcement has been muted, with the stock price not significantly impacted.

- The likelihood of the merger going through is uncertain, but the hedge fund consortium's higher bid is expected to be the winner.

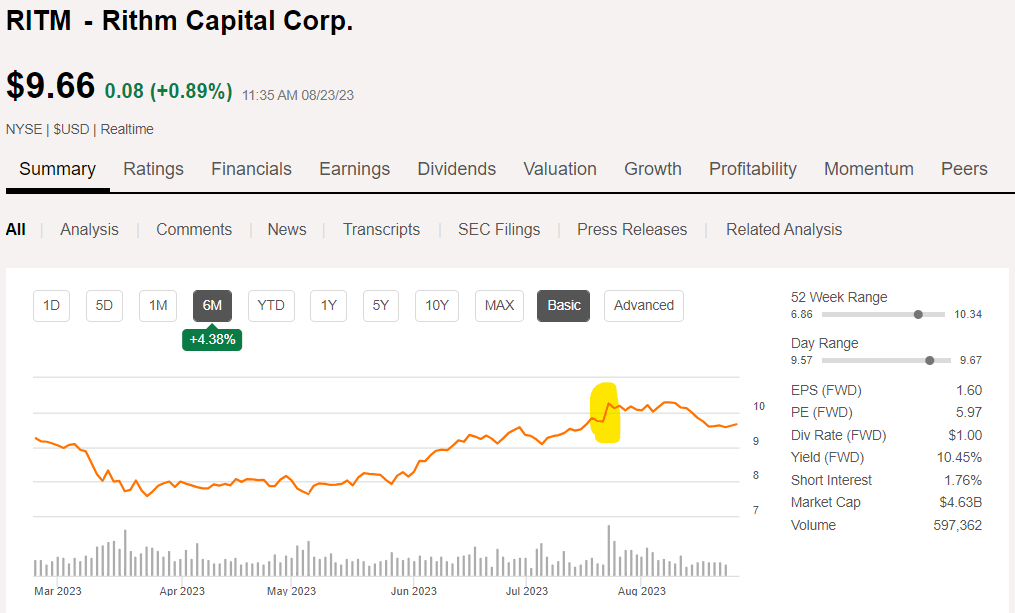

Rithm Capital (RITM) is a $4.6B market cap mREIT with many different lines of business ranging from mortgage servicing rights (MSRs) to direct ownership of single family rental properties. This midcap has been elevated to national news as it has gotten into a bidding war with a consortium of hedge fund managers including Bill Ackman, Marc Lasry and Boaz Weinstein over an asset manager called Sculptor Capital (SCU).

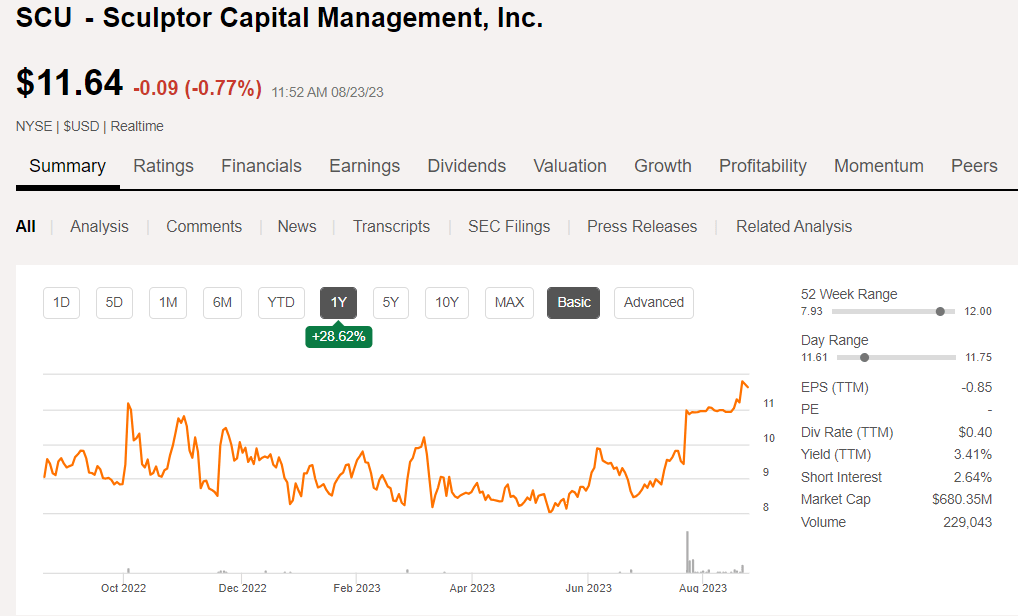

RITM has already inked the acquisition with an agreement to buy SCU for $11.15 per share. The hedge fund consortium is trying to overturn that agreement by offering a higher $12.00 per share to buy SCU.

This article will discuss likely outcomes of the bidding war and its implications for Rithm Capital. Specifically, I think RITM will lose the bidding war and shares will increase as a result.

Market Reaction

So far, the market's reaction appears to be muted. There was a slight bump up on the announcement highlighted in yellow below, but that has since been removed.

{kind=link}

I think the bump up gives the false impression that the market likes the Sculptor deal and wants it to go through.

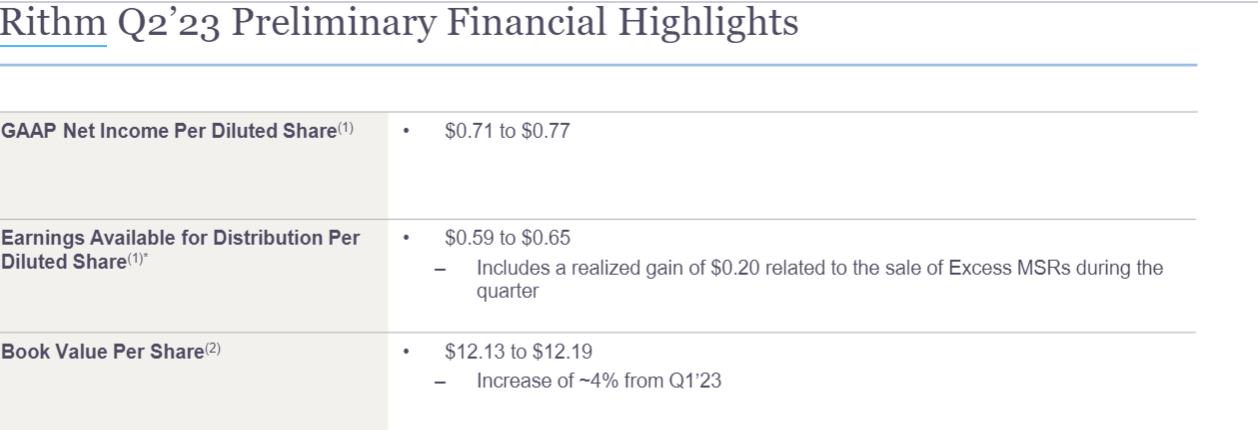

See, the deal was announced concurrently with a pre-announcement of 2Q23 operating results. These results were phenomenal.

{kind=link}

This was a beat of $0.26 per share and a revenue beat of $185 million.

RITM's mortgage servicing rights portfolio performed well through the rising interest rate environment of 2Q23.

The way MSRs work is that RITM pays up front to buy the right to service them which generates a cash flow over the life of the asset. At the time RITM bought these MSRs, prepayment speeds were quite high which meant the expected life was fairly short. However, with mortgage rates rising so rapidly nobody wants to lose their existing low cost mortgage so prepayments have plummeted. This extends the life of the MSRs allowing RITM to collect a longer stream of cashflows than initially underwritten. This portfolio has appreciated substantially.

I believe it was the preannouncement of very strong operating results that caused the stock to go up on the day of the merger announcement. In fact, I think the stock would have gone up significantly more if not for the merger.

The merger with SCU, merits and demerits

With a consortium of sophisticated hedge funds offering a higher bid it would appear RITM got a reasonably good price for SCU. The deal is expected to be near term neutral to earnings and long term accretive. Financially speaking, it is a fine deal.

Strategically, however, I don't think it makes much sense. It is an entirely new business line for RITM with virtually no synergy with existing business. In any merger presentation there is always a synergy slide, but this is one of the weakest I have ever seen.

RITM

The first bullet is a fluff sentence that says nothing.

The 2nd and 3rd bullets are intentions of how to manage SCU as a standalone business under the RITM umbrella. These might be good initiatives, but that is not synergy.

RITM does have a strong history of making mergers work so they might be able to grow this as intended and make it quite accretive to shareholders.

It just strikes me as unnecessary as RITM's existing business lines are so well positioned. It would be a shame to dilute the exposure to MSRs and single family rentals.

I think the market agrees and RITM stock will rise if the merger gets broken up by higher bids.

Chance of merger going through

RITM's bid is at $11.15 and the hedge fund consortium has bid $12.00 per share.

SCU is trading near the middle of this range indicating the market is about 50/50 on what happens.

{kind=link}

I think there will be a bit of a back and forth but ultimately the hedge fund investors will win the bid.

Why?

Frankly, SCUs rejection of the $12 bid has no merit.

With mergers there is usually a "go-shop" period in which the target will review competing bids and have a review board look at them in a process that is meant to be aligned with shareholders to maximize shareholder value.

I would imagine that shareholders of SCU would universally prefer the $12 bid by the hedgefunds to the $11.15 bid from RITM. So to reject the significantly higher bid there should be some fairly substantial reason.

Well, the SCU special committee looked at the $12 bid and rejected it for the following reason:

"We have received an unsolicited proposal from a third party that had participated in the strategic alternatives process. This bidder has not demonstrated adequate committed funding for any of its bids."

Let's just marinate on that for a second.

They are claiming that a consortium including Bill Ackman, Marc Lasry and Boaz Weinstein has not demonstrated the ability to fund the acquisition.

SCU is a small cap. This would be a bitesize acquisition for any of those guys individually so the idea that they as a group cannot fund the acquisition is just laughable.

So why did SCU reject the $12 bid?

In brief, management greed.

Since RITM does not have an existing asset management platform of this scale, they will leave current SCU management in place.

They want to keep their comfy and ridiculously high paying jobs ($30 million salary to Levin).

In contrast the hedge fund bidders already have sophisticated asset management platforms of their own and have no need to keep management.

SCU's special committee set up to review the M&A has a fiduciary duty to maximize shareholder value. Shareholders do not care whether management keeps their jobs. Shareholders obviously would prefer the $12 bid.

As more light gets shed on this matter, I think it will be very difficult for this committee to maintain its position.

Therefore, I believe the $12 bid from the hedge funds to be the likely winner of the bidding war.

How to play it

Buying SCU would be one way to play it, but I don't think the upside is enough to be worth the risk and the wait. At current pricing it is only about 3% below the $12 bid and even if that bid eventually wins it could be a few quarters time for closing.

That is a long wait for 3% and in my opinion not worth the risk.

I see RITM as the better way to play it. RITM benefits from losing this bidding war in 2 ways:

- RITM receives a $16.5 million breakup fee

- The operational excellence of 2Q23 finally gets to price in to RITM stock

From the Sculptor Capital Proxy:

"Under the Merger Agreement, the Company will be required to pay a termination fee in the amount of $16,576,819, net of Parent Expenses.

For clarity, the word "parent" in the proxy statement refers to RITM as per the proxy:

""Parent" or "Rithm" means Rithm Capital Corp., a Delaware corporation"

So, termination of the deal is a net profit of $16.5 million to RITM. It is not huge given RITM's size, but profitable nonetheless.

The bigger deal to me is that it unclouds RITM's story. Rather the looming question of whether they can grow their new asset management business shareholders will be able to focus on the MSRs and the SFR, both of which are fundamentally well positioned.

RITM going forward

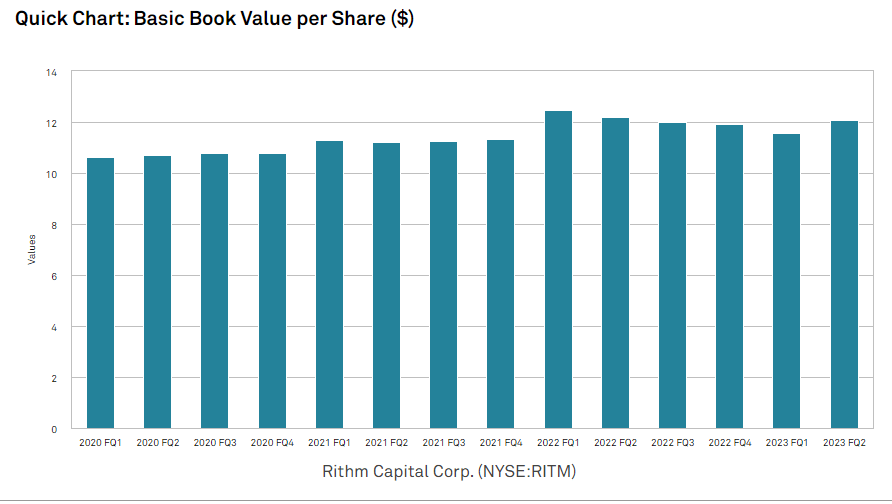

Rithm is significantly undervalued trading at 6X forward earnings and 80% of book value. That valuation implies substantial risk which I think is incorrect as RITM's main business lines just aren't that risky.

Since their MSRs have exceedingly low coupons, prepayment would only be likely to rise substantially if mortgage rates fell maybe 300-400 basis points.

RITM has also set up a nice internal buffer in that its origination business benefits when interest rates drop. This internal offset with MSRs liking higher rates and origination liking lower rates cushioned RITM in the meteoric Fed hike cycle allowing it to be one of few mREITs to actually grow its book value.

S&P Global Market Intelligence

{kind=link}

Given the valuation and strong businesses, I think RITM could be a reasonable stock to own here.

That said, I think the preferreds remain the better way to play it.

Preferreds with significant upside to par

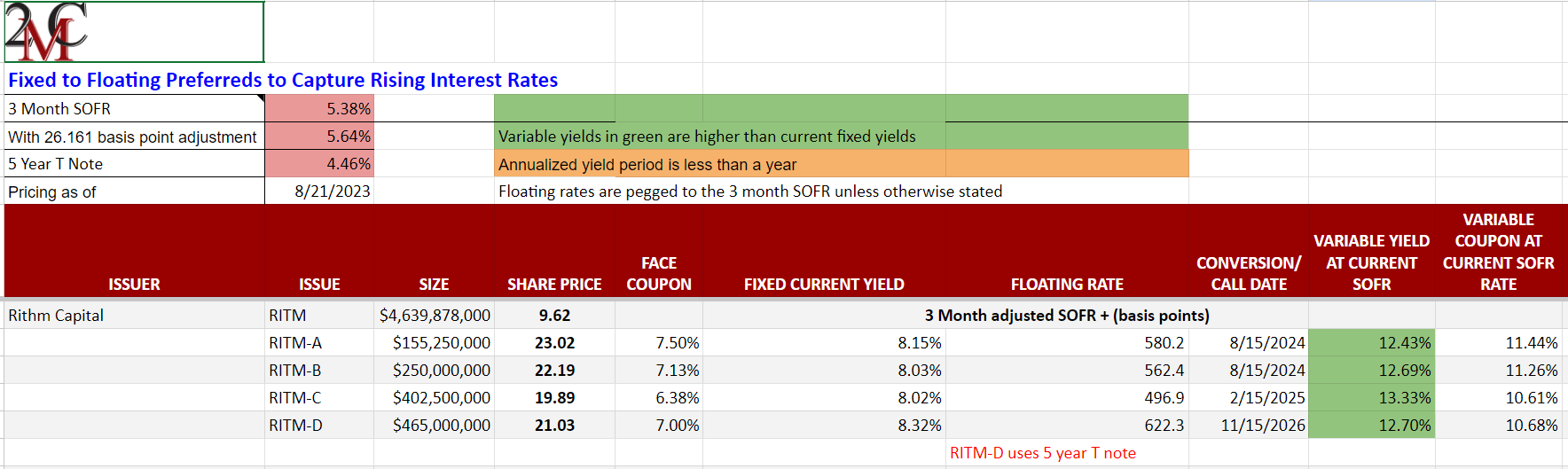

Rithm has series A through D preferreds which are each currently fixed rate but move to floating rate on their respective conversion dates detailed below.

Portfolio Income Solutions Fixed to Floating Preferred Tracker Spreadsheet

{kind=link}

The rates they offer upon conversion were designed during a low interest rate environment so SOFR plus 500 basis points did not seem like a huge payout. But SOFR has moved up an incredible amount resulting in some juicy yields.

Within the preferred stock, each has certain advantages.

The A and B series, (RITM.PA) and (RITM.PB), have the soonest conversion to floating rate on 8/15/24. If SOFR remains where it is today that would take them to yields against current market price of 12.43% and 12.6%, respectively. As the call date approaches we have noticed a tendency for these fixed to floating preferreds to trade up closer to $25 par value. Companies are incented to redeem the shared at the call date because they don't want to pay 12%+.

As such, there is an opportunity to collect significant capital appreciation in addition to the dividends obtained in the interim. The combined capital gains and dividend suggest annual total return between 16% and 25% for the RITM preferreds if called upon conversion.

The C series (RITM.PC) is on the 25% end due to its extreme discount to par.

Series D (RITM.PD) is also quite interesting because it uses a 5 year Treasury yield as the base for its floating rate instead of SOFR. Presently, SOFR is higher because the yield curve is inverted, but if history is a guide the 5 year Treasury yield is typically higher. I suspect it will be higher in November of 2026 when this thing converts.

The Series D also has the best spread with a floating yield of 622 basis points over the 5 year. That looks like a high yield in any environment. At the present moment I think any of these are a viable way to play it.

There might be opportunities to double or triple dip by buying in succession as they convert. We will continue to monitor the relative pricing and opportunity.

The preferred dividends are well covered whether the SCU acquisition goes through or not, but I think they are slightly better positioned if the deal does not go through because the asset management business introduces a new source of volatility.

For further details see:

Rithm Capital: Caught In A Sculptor Bidding War With Bill Ackman (Rating Downgrade)