SCU - Rithm Capital: This 9.8% Yielding Mortgage Trust Now Has A Catalyst

2023-07-27 03:11:12 ET

Summary

- Rithm Capital has announced the acquisition of Sculptor Capital Management, paying an 18% premium on the company's closing stock price.

- The acquisition is part of Rithm's strategic plan to develop a third-party asset management business, diversifying its investment focus beyond real estate and mortgage markets.

- RITM stock and its 9.8% yield remain attractive for passive income investors, particularly as the trust may declare a special dividend related to Mortgage Servicing Rights sales.

Rithm Capital Corp. ( RITM ) , the mortgage real estate investment trust that I recommended aggressively after the trust presented 1Q-23 results due to its excellent dividend coverage, Mortgage Servicing Rights investments, and a low valuation based on book value, now also has a catalyst.

The trust announced the acquisition of Sculptor Capital Management, Inc. ( SCU ) on Monday and said that it will pay an 18% premium to the company's closing stock price on Friday.

By acquiring Sculptor Capital Management, Rithm Capital advances its strategic plan to develop a third-party asset management business that could add to the trust's core earnings growth moving forward. Because Rithm Capital is cheap, based on book value, and the trust might declare a special dividend related to MSR sales, I think the stock and its 9.8% yield remain highly compelling for passive income investors.

New Acquisition Equals New Revenue Stream, Scale, And Improved Diversification

Rithm Capital has large investments in mortgage assets and Mortgage Servicing Rights. Mortgage Servicing Rights (MSRs) are rate-sensitive and, therefore, extremely attractive to own during periods of rising interest rates . With that said, the trust has tried to broaden its investment focus in recent years.

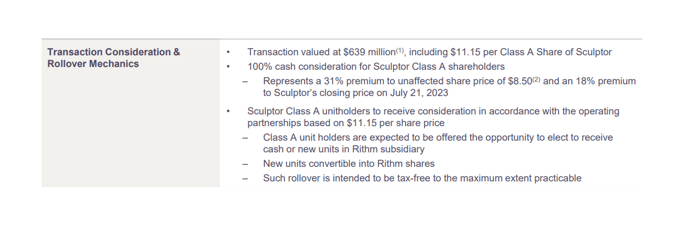

In a move to further diversify the company, Rithm Capital said on Monday that it was acquiring alternative asset manager Sculptor Capital Management for $639 million, or $11.15 per Class A share. The transaction details, which I represent below, require the mortgage REIT to pay for the company all cash. Acquirers typically offer a full cash consideration if they believe the transaction will benefit their shareholders in terms of synergy, cost, and revenue potential.

Rithm Capital plans to finance the transaction with available cash (no transaction-related funding will be required) and the deal is expected to close in the fourth quarter.

{kind=link}

The acquisition of Sculptor Capital Management creates a path for Rithm Capital into the asset management business which the trust said it wants to develop in order to diversify its investment business that has so far been concentrated on the real estate and mortgage markets.

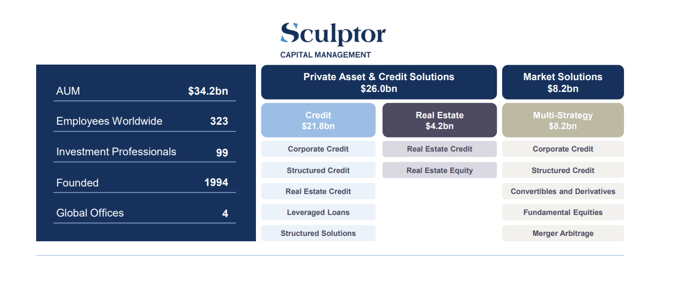

By acquiring Sculptor Capital Management, Rithm Capital gets access to $34 billion in assets under management, with the majority of those funds invested in non-real estate related investment products.

From a diversification perspective, the deal makes sense for Rithm Capital because the alternative asset manager moves into the third-party capital management sphere which creates a new revenue stream for the trust. At the same time, the transaction provides Rithm Capital with immediate scale.

Sculptor Assets Under Management (Sculptor Capital Management)

{kind=link}

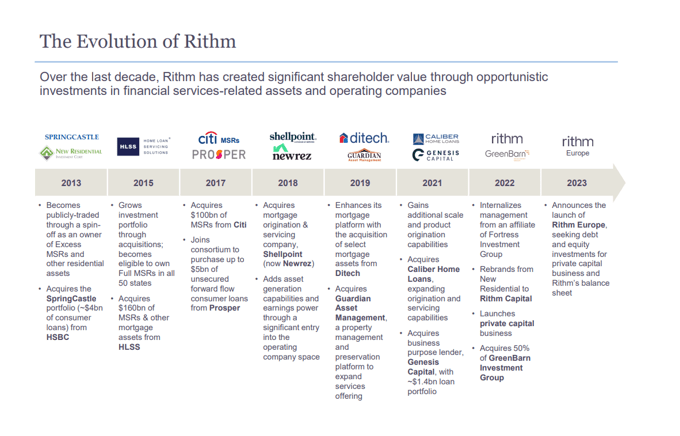

Rithm Capital has been a busy acquirer of companies in the last decade. The trust acquired mortgage servicing, origination, and investment capabilities steadily since 2013 and is moving slowly towards becoming a multi-line, full-service alternative asset manager. Moving forward, I can even see Rithm Capital dip its toes into the business lending market or raise capital for a private equity fund.

{kind=link}

Preliminary 2Q-23 Results, Special Dividend Potential

As part of the transaction announcement, Rithm Capital released its estimates for its 2Q-23 book value and core earnings which I incorporated into the chart below. In the second quarter, Rithm Capital produced an unusually high $0.59-0.65 per share in distributable earnings, which includes a $0.20 per share extraordinary gain from the sale of MSRs during the quarter.

As a result, the trust's payout ratio is set to drop from 71% in 1Q-23 to ~40% in 2Q-23. With excess portfolio income generated in 2Q-23, I can see how management (I am speculating) could declare a special dividend for the second quarter.

Dividend (Author Created Table Using Trust Information)

Rithm Capital: Why Should It Trade At A 13% Discount To Book Value?

Rithm Capital remains a steal from a valuation perspective. Passive income investors can buy the trust's total portfolio at a 13% discount to book value which seems rather undeserved when taking into account that Rithm Capital has a solid record of covering its dividend with distributable earnings.

In 1Q-23, Rithm Capital had a 71% LTM dividend payout ratio and the trust has consistently covered its dividend with distributable income in the last year. Other mortgage REITs, though much less diversified and having much riskier dividends, sell near 1.0x book value multiples.

How Does The Risk Situation Look Like?

Rithm Capital is trading at a book value of 0.87x which takes a lot of risk out of the equation, in my view. A decrease in interest rates would probably negatively impact the trust's large MSR portfolio (MSR values are negatively correlated with interest rates), but Rithm Capital appears, based on its transaction announcement, to reduce its exposure to the MSR sector right now.

My Conclusion

A new revenue driver is starting to emerge in Rithm Capital's investment portfolio.

By acquiring an alternative asset manager, Rithm Capital is also acquiring a new revenue stream that is set to make the mortgage REIT less dependent on the mortgage/real estate industries which, in turn, results in a more diversified portfolio and less core earnings risk for passive income investors.

Rithm Capital is the best mortgage trust, from a diversification perspective, in my opinion, and I consider the trust to be undervalued based on book value.

Furthermore, due to a realized gain related to MSR sales, resulting in way above run-rate core earnings, I think Rithm Capital might declare a special dividend for the third quarter.

For further details see:

Rithm Capital: This 9.8% Yielding Mortgage Trust Now Has A Catalyst