ECAT - RIV: A Tempting Discount

2023-06-14 10:38:06 ET

Summary

- RiverNorth Opportunities Fund is trading at an attractive discount, with a diverse portfolio and exposure to fixed income, SPACs, investment company bonds, and equity.

- The fund's discount and underlying CEFs' discounts provide potential upside, but leverage increases risks and adds volatility.

- RIV is not a set-and-forget investment but should be traded around between its discounts/premiums and rights offerings.

Written by Nick Ackerman, co-produced by Stanford Chemist. This article was originally published to members of the CEF/ETF Income Laboratory on June 1st, 2023.

RiverNorth Opportunities Fund ( RIV ) continues to trade at an attractive discount. The fund's portfolio is fairly diverse, with most of its exposure to fixed income. However, they aren't limited to investing in any specific area as the fund also invests in special purpose acquisition companies or SPACs, as well as investment company bonds and equity, and it even has a touch of exposure to business development companies or BDCs. They gain most of their exposure through investing in other closed-end funds.

The fund has fairly frequently traded at premiums, so the latest discount makes it an interesting consideration. One of the driving factors for the fund's premium seems to be the high managed distribution plan of 12.5% of NAV that resets annually.

In our last update , I noted that RIV could be swapped in favor of the RiverNorth/DoubleLine Strategic Opportunity Fund ( OPP ). The simple premise was that these funds conduct rights offerings, and OPP was going through their RO while RIV was next on deck to conduct one. In that previous update, RIV's premium stood at 10.54%. So the swing down to a near 9% discount at present was a pretty large shift.

Since that update, RIV has outperformed OPP significantly on a total NAV return basis. Yet, RIV had underperformed a bit on a total share price return basis.

YCharts

Therefore, the suggestion to swap worked out. At this point, the difference wasn't massive, but at one point, the divergence was a bit wider. The RO for RIV was announced in October and completed in November 2022.

The Basics

- 1-Year Z-score: -098

- Discount: -7.63%

- Distribution Yield: 13.89%

- Expense Ratio: 2.18% (including leverage expenses)

- Leverage: 27.76%

- Managed Assets: $256 million

- Structure: Perpetual

RIV has an investment objective of "total return consisting of capital appreciation and current income."

To achieve the objective, RIV "employs a tactical asset allocation strategy primarily comprised of both closed-end funds and exchange-traded funds. RiverNorth implements an opportunistic investment strategy designed to capitalize on the inefficiencies in the closed-end fund space while simultaneously providing diversified exposure to several asset classes."

Around half of the underlying portfolio is exposed to other closed-end funds. While that can mean discounts on discounts, it also means expenses on expenses. The fund's own expense ratio comes to 2.18%, with its underlying CEF positions having their own 1 to 2% expense ratios as well.

The fund issued a preferred 6% ( RIV.PA ) that's publicly traded, and it currently yields 6.56%. This isn't callable until after May 15th, 2027, and it could trade perpetually. By having preferred, they haven't been impacted by the rising costs of borrowings that other CEFs had experienced as interest rates have risen. However, they do have the flexibility to draw on a credit facility at up to $65 million. Those borrowings would be paid at OBFR plus 0.85%/

Performance - Discount Remaining Wide

The fund conducts rights offerings every year, and every year it leads to the dilution of the fund. So the fund has to outearn this dilution and the expenses on expenses, which can be a fairly difficult thing to do. The dilution on a per share basis is located in their financial highlights in their last semi-annual report . The hit to NAV per share was a decline of $0.10, $0.13, $0.08, $0.21, $0.26 and $0.32 in years 2023, 2022, 2021, 2020, 2019 and 2018, respectively.

Considering how difficult that can be to accomplish, it's almost surprising they have positive results at all. They provide performance against the S&P 500 Index, which is interesting considering that half of the fund is fixed-income. I wouldn't necessarily expect the fund ever to outperform the large-cap equity market going forward.

{kind=link}

RIV Annualized Performance (RiverNorth)

However, where an investor can outperform other multi-asset investments is by potentially taking advantage of instances where the fund is trading at a discount. With the fund's current discount being fairly attractive, it could suggest some upside. That would be if the fund can return to trading at a premium, which will lift up the results of the fund materially. Since our last update, the fund was at a ~10% premium and now trades around a 7.6% discount. That was a massive swing.

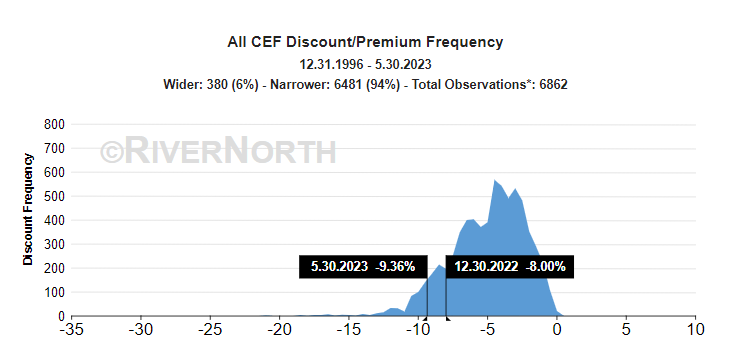

In addition to RIV's discount, being that the fund is comprised of around 50% of other CEFs, overall CEF discounts are important to consider too. At this present time, discounts across the board are exceptionally large relative to history.

{kind=link}

Closed-end Fund Discounts/Premiums (RiverNorth)

Discount tightening on the fund and discount tightening on the fund's underlying portfolio could provide an added lift. RIV noted that at the end of March 31st, 2023, they're underlying CEF discounts averaged -11.3%. Suggesting that they had invested in discounts that are wider than what we are seeing across the board. Of course, the caveat is that discounts can remain wide for considerable periods of time. Given the fund's drop to a substantial discount, it remains to be seen if they'll conduct an RO this year. The deeper the shares are discounted when an RO is conducted, the larger the NAV dilution.

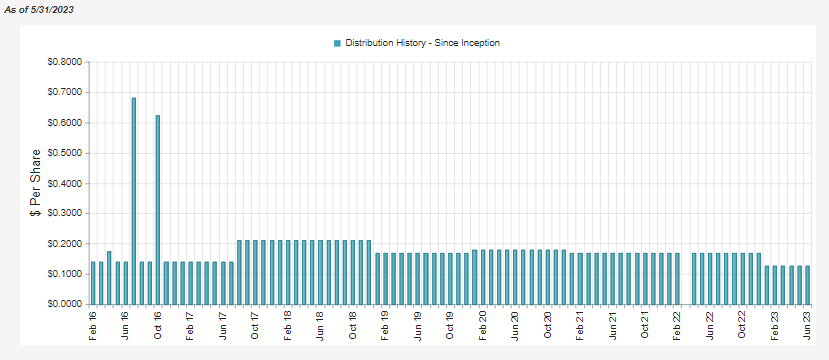

Distribution - 12.5% Managed Plan

No matter what the fund is earning or returning to investors, one thing is going to be guaranteed in its distribution. That is, it will always be a high yield because of the 12.5% plan that resets annually. Thanks to the fund's discount, that would mean investors are actually collecting 13.89% currently. The fund's NAV has also declined a bit on a YTD basis, meaning that the NAV rate is now up to 12.64%.

{kind=link}

RIV Distribution History (CEFConnect)

Generally speaking, the fund won't return 12.5% + the expense ratio, meaning that the NAV should decline over time. Throughout 2019 and 2022, the strong bull market run meant that we didn't see substantial declines. Covid was a brief drop in 2020 that never really impacted the fund either since the distribution is set for the entire following year.

However, with 2022 being a particularly tough year, the cut heading into 2023 was material. Generally speaking, we should see a decline in most years as the NAV should decline in most years as they pay out more than can be earned.

In their last semi-annual report, net investment income jumped materially. It went from $0.18 for all of fiscal 2022 to $0.43 for the six months ended January 31st, 2023. With more NII, the fund could have a better chance of more predictability in their income generation. That could lead to a potentially slower decline in terms of cuts for the distribution.

RIV's Portfolio

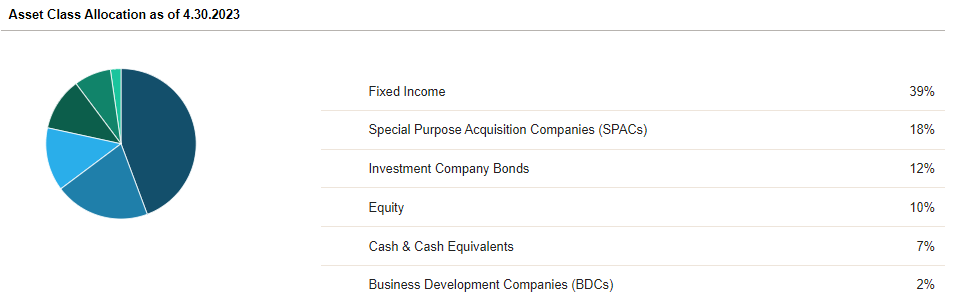

Helping to drive higher NII would seem to be added exposure to fixed-income investments. Last year, the fund was invested in around 32% fixed income with around a 22% allocation of equities, with a substantial ~34% allocated to SPACs.

Fixed income exposure comes in at 39%, but they also list another 12% allocated to investment company bonds. Those are also fixed-income investments. The allocations to SPACs have declined materially, but for the most part, those could even be considered fixed-income investments as they are essentially invested in short-term Treasuries for the most part until they de-SPAC.

{kind=link}

RIV Asset Breakdown (RiverNorth)

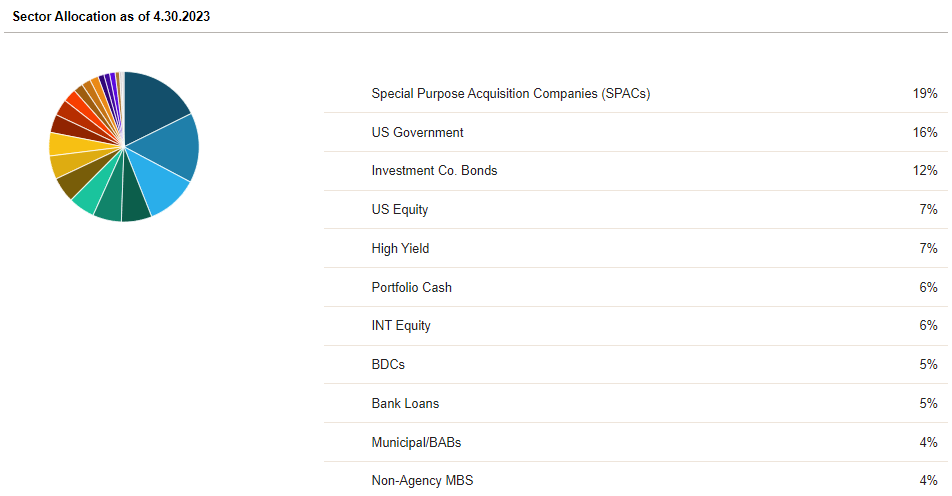

In particular, investment grade exposure more recently came in the form of U.S. Government securities which has seen a noticeable uptick. At the end of January 31st, 2023, U.S. debt securities accounted for 16.36% of the fund's assets and another 5.63% was allocated to a money market fund with a yield of 4.169%. The fund's U.S. debt investments had yields of 3-4.61%. SPAC exposure at that time was 28.64%, which, again, is mostly short-term U.S. Treasury securities until they find a company to merge with.

Here's a look at some of the top asset class allocations.

{kind=link}

RIV Asset Class Allocation (RiverNorth)

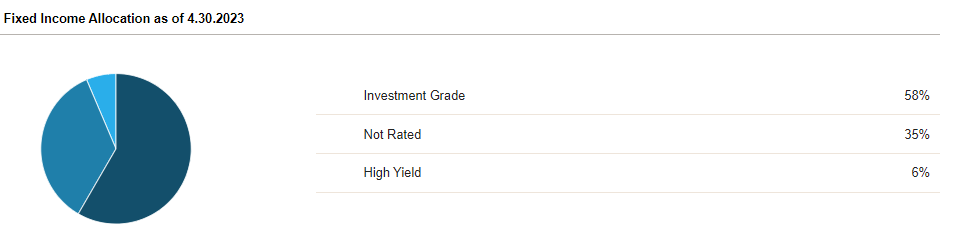

Here's the breakdown of the fund's fixed income allocation divided up amongst investment, non-investment or not rated grades. Previously, the high yield was 22.77% of the fund, 26.89% was in investment grade and not rated was the largest at a 50.34% allocation.

{kind=link}

RIV Credit Quality Allocation (RiverNorth)

While yields on these risk-free debts have been rising to more attractive levels, it also nearly guarantees the decline in NAV as they pay out above these yields. Where that might not happen is if rates are cut. That would see the value of these investments rise, and the capital gains could offset the over-distribution.

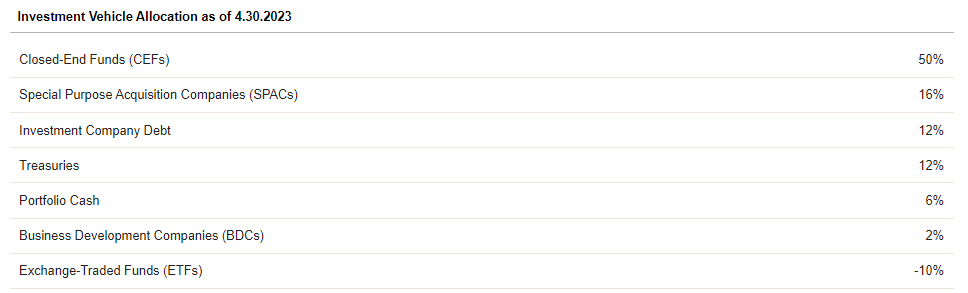

CEFs make up around 50% of the fund.

{kind=link}

RIV Asset Breakdown (RiverNorth)

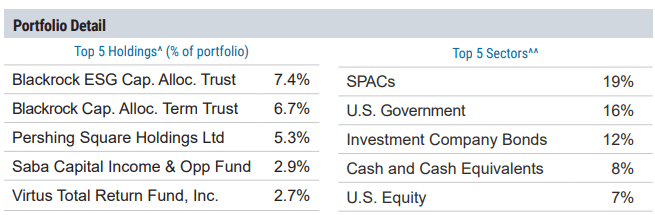

They don't list the top holdings as of the same breakdowns listed above for the period ending April 30th, 2023. However, we can see the breakdown as of the end of March 31st, 2023, which is provided in the fund's latest fact sheet.

{kind=link}

RIV Top Exposure (RiverNorth)

The two largest positions are BlackRock ESG Capital Allocation Term Trust ( ECAT ) and BlackRock Capital Allocation Term Trust ( BCAT ). These funds are both multi-asset CEFs that invest with tons of flexibility. I've covered BCAT more recently, and the fund's substantial discount of nearly 12% is particularly attractive. Despite ECAT having "ESG" in its name, you'll still see investments in similar holdings as BCAT. ECAT is also carrying a meaningful discount of 11.25%.

Saba is invested in both of these funds, but they are being more aggressive with ECAT. They are looking to fill some seats on the Board. They had also indicated they'd be interested in seeing the fund switch to an open-ended structure. That would eliminate the discount/premiums as investors would be allowed to invest or redeem at NAV daily.

Conclusion

Given RIV's discount remains wide after the fund's previous rights offering, it would appear a decent time to consider RIV. Besides the fund's discount remaining relatively attractive if we can get some mean reversion, the fund's underlying CEFs representing ~50% of the portfolio are also attractively discounted. The fund's leverage does increase risks and adds volatility. However, it's also at a fixed-rate cost, so we haven't seen borrowing costs rise substantially as we've seen from other leveraged CEFs.

RIV is a bit more of an unusual fund, and it isn't necessarily a set-and-forget style that some investors like to invest in. Instead, I believe that RIV should be traded around between its discounts/premiums and rights offerings.

For further details see:

RIV: A Tempting Discount