RIV - RIV: Fund Of Funds 15% Yield

2023-10-25 08:49:58 ET

Summary

- RIV is a "fund of funds," meaning it invests in other closed-end funds (CEFs), business development company (BDC) debt, exchange-traded funds (ETFs), and special purpose acquisition companies (SPACs).

- RIV's performance has been influenced by interest rates, and it tends to perform poorly in years when rates are rising. It aims to benchmark itself against the S&P 500.

- The fund's largest allocation is in CEFs (59%), followed by 14% in BDC debt and equity, 10% in SPACs, and it also has a short position in the S&P 500.

- RIV is currently trading at a large discount to net asset value and is utilizing a significant amount of return of capital (ROC) in its distributions.

Thesis

RiverNorth Opportunities Fund, Inc. (RIV) is a closed-end fund. The vehicle is a 'fund of funds', aggregating in its portfolio other CEFs, BDC debt, ETFs and SPACs. RIV seeks a total return consisting of capital appreciation and current income. As per its literature, the fund:

implements an opportunistic investment strategy designed to capitalize on the inefficiencies in the closed-end fund space while simultaneously providing diversified exposure to several asset classes.

As a CEF itself, RIV employs leverage, which currently stands at 28%. The best way for a retail investor to think about RiverNorth is as a very 'risk-on' fund with a high degree of embedded leverage. Outside the outright debt the fund has, its holdings themselves are highly leveraged (think that each CEF in the fund's portfolio has its own leverage ratio).

The fund is down this year (-12% on a total return basis), although it aims to benchmark itself against the S&P 500. The S&P 500 is up significantly in 2023 thanks to the ' Magnificent 7 ' solely. We would have expected a fund benchmarked against the S&P 500 to have at least a positive performance. However, when drilling into the collateral pool for RiverNorth, the year-to-date performance is not surprising anymore:

{kind=link}

The CEF is overweight fixed income via CEFs and outright BDC bonds, and underweight equities. Fixed income has done extremely poorly this year again, on the back of higher rates. We are going to expand further regarding the individual names in the portfolio in the 'Holdings' section, but view RIV as an investment vehicle with overweight investment grade credits.

The main risk factor for RIV is represented by rates, and we see that from the fund's performance as well. The name posted negative performances only in the years when rates went up, namely 2018, 2022, and now 2023. RIV will become a palatable, interesting investment when the Fed starts cutting rates.

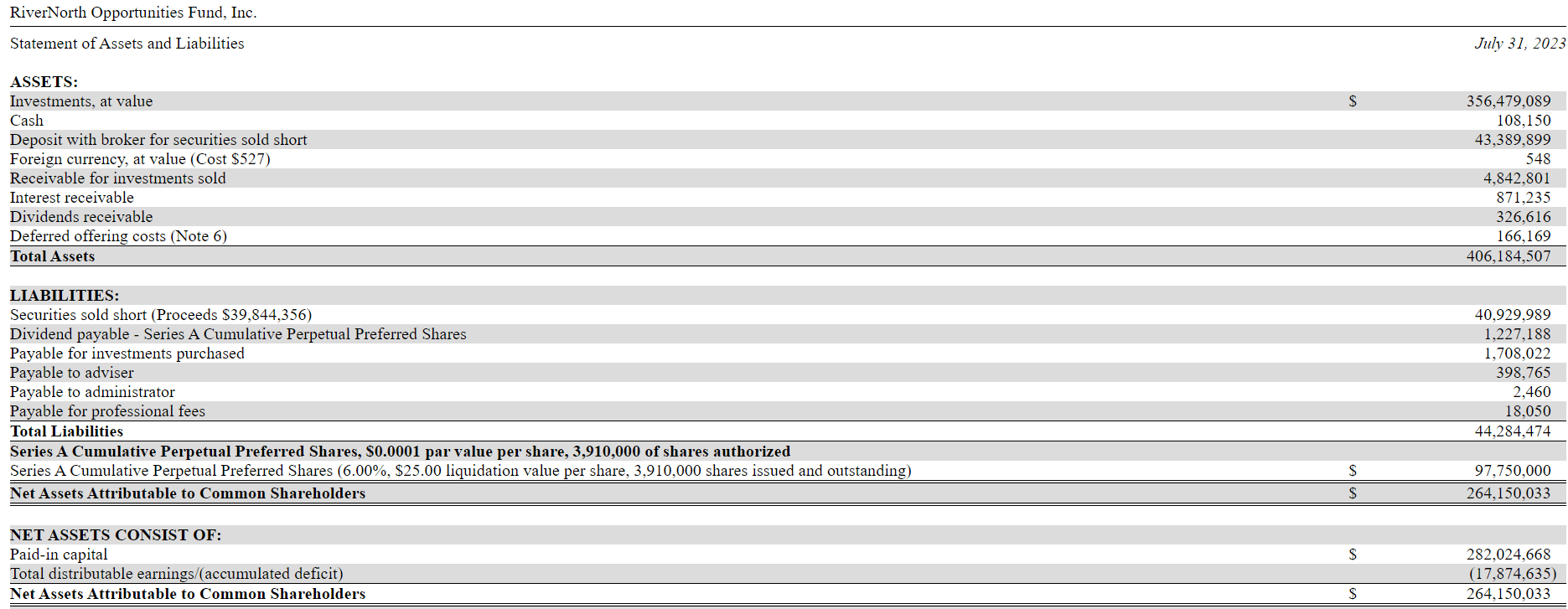

Leverage

RIV is one of those rare CEFs that has embedded leverage via preferred shares solely:

{kind=link}

If we look at the 'Liabilities' section of the balance sheet we can notice that outside the preferred shares, we only have the 'payables' lines and the shorted securities accounting line. There is no Repo facility for this name.

This liabilities structure basically translates into a stable cost of funds, which has helped this CEF in a rising rates environment, when compared to funds with Repo structures.

Historic Performance

The fund's performance has been mainly driven by rates:

{kind=link}

The CEF posted negative annual returns only in the years with rising interest rates, namely 2018, 2022 and 2023. Expect this correlation to persist in the future, with the fund set to post a positive performance when the Fed starts cutting rates.

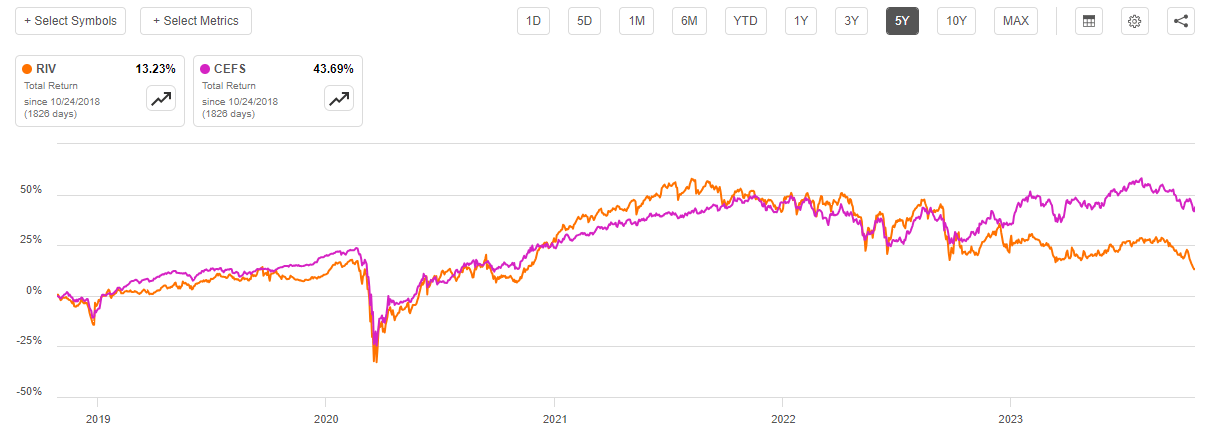

It is also worth noting that until recently, RIV has managed to closely match the return performance of one of the stalwarts in the sector, namely the Saba Closed-End Funds ETF ( CEFS ):

{kind=link}

The recent divergence has all to do with the fixed income versus equity allocation between the two vehicles, with CEFS having a larger allocation to large-cap equities when compared to RIV.

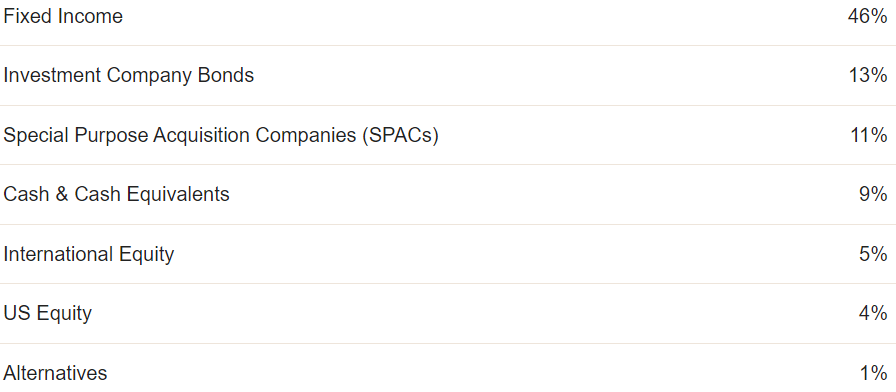

Holdings

The fund has its largest allocation placed with CEFs:

Allocation (Fund Website)

59% of the portfolio sits with CEFs, followed by 14% of the allocation invested in BDC debt and equity, while 10% is put into SPACs. Interesting to note the short ETF position the fund has. When drilling into the details we see the fund shorting the equal weight S&P 500 ETF:

{kind=link}

The CEF is short both the Invesco S&P 500 Equal Weight ETF (RSP), as well as the SPDR S&P 500 ETF (SPY). $34mm of the $40mm short is via RSP though. We view this as a portfolio hedge, although the fund runs a significant basis here. For example, the SPY short has not worked this year. It has actually been a double drag - on one side the SPY short has produced negative results, while the actual portfolio (mostly fixed income) has posted negative figures as well.

From a sectoral standpoint, municipals make up the largest allocation in the underlying portfolio:

Sectors (Fund Fact Sheet)

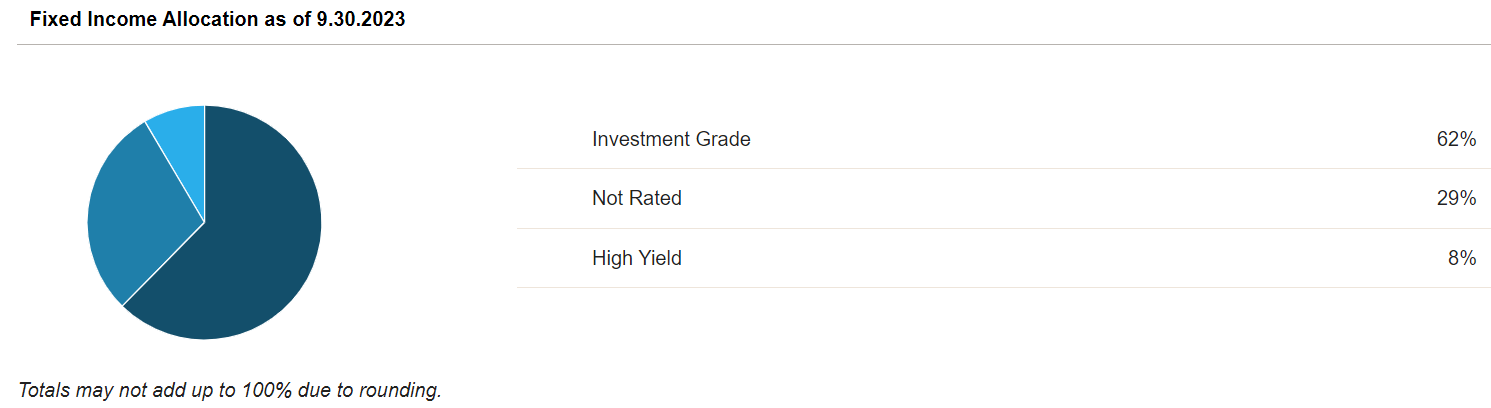

Municipals are followed by investment-grade bonds and treasuries. The CEF has a very low overall allocation to equities. On the fixed-income side the fund has its largest aggregate allocation to investment-grade credits:

{kind=link}

The parsing explains quite well the fund's sensitivity to interest rates, its largest risk factor.

Premium/Discount to NAV

The fund is currently trading at a large discount to net asset value:

The CEF was trading almost flat to NAV for a long period of time, and only moved to a large premium on the back of the zero rates environment observed in 2020/2021.

As rates rose, the CEF moved to a discount, which has widened as of late. Expect this beta to interest rates to persist, with the CEF moving to a narrower discount only when the Fed starts cutting rates again.

Distributions

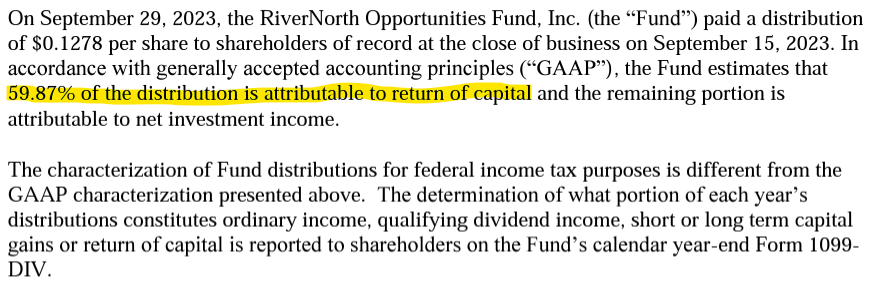

Despite its large 15% dividend yield, the CEF is utilizing a very large amount of ROC to support that figure:

{kind=link}

As of the September 2023 Section 19 notice, the fund is using 60% ROC in its distribution. That is an enormous amount, and will eventually result in the fund's underperformance via NAV erosion. We would prefer to see the CEF cut its distribution to say 10%, which would still have the vehicle pay out a large dividend, but at the same time utilize less ROC.

We understand why the CEF is doing this, namely to support its market price as a factor to its NAV (the CEF is currently trading at a -13% discount to NAV), but we feel a lower dividend yield will have the same supportive impact.

As a rule of thumb, any CEF with ROC figures above 30% will eventually result in fund underperformance. ROC is useful as a temporary tool and in small quantities. Especially when talking about a fixed-income CEF, which generally generates a substantial amount of interest income.

Conclusion

RIV is a 'fund of funds' structured as a CEF. The vehicle holds other CEFs, BDC debt and equity, SPACs and ETFs. The fund is a 'risk-on' vehicle with a 28% leverage ratio and further leverage embedded in each of its holdings.

RIV is mainly a fixed-income vehicle, with investment-grade debt as its largest sectoral allocation. The fund's historical performance is reflective of that, with the CEF down in the years when rates moved higher, namely 2018, 2022 and 2023. The CEF is now trading at a -13% discount to NAV, a discount which has opened up on the back of higher rates. Expect this discount to persist until the Fed starts cutting rates and the CEF starts outperforming.

RiverNorth has been able to post an impressive historical track record, closely matching the Saba CEFS performance until earlier this year. The fund has been dragged down in 2023 by its overweight fixed-income allocation and short positioning in RSP and SPY. The CEF is however well set up for a gap-down in the markets via this portfolio hedge.

Even though RiverNorth has a large 15% dividend distribution, it is not supported, with 60% of it being ROC. We would like to see the fund cut the distribution in order to improve its long-term NAV performance.

RIV is a very robust 'fund of funds' but it will only start performing once the Fed starts cutting rates. That is when we see its discount to NAV narrowing as well. If you already own this CEF then Hold it for the dividend, while new capital should wait until the Fed cuts rates to enter the name.

For further details see:

RIV: Fund Of Funds, 15% Yield