RSP - RIV: This 13.73%-Yielding CEF Has Unique Qualities But Be Careful Of Leverage

2023-08-17 18:06:32 ET

Summary

- High inflation is a major problem in the U.S., pushing up the cost of living and putting pressure on household budgets.

- Investors can earn income by purchasing shares of closed-end funds like the RiverNorth Opportunities Fund.

- The RIV closed-end fund uses leverage and a unique strategy to boost its effective yield, but it comes with higher risk and uncertain distribution sustainability.

- The fund has an attractive 13.73% distribution yield, but it is uncertain whether or not it can sustain it. It failed to cover its distribution during the most recent six-month period.

- The fund is currently trading at a reasonable discount to the net asset value, so the price is currently acceptable.

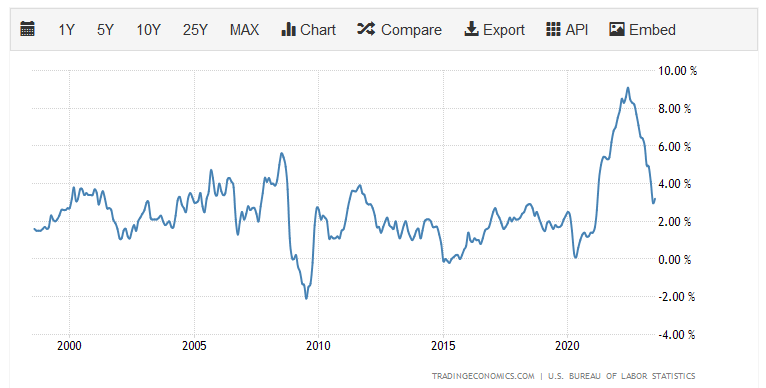

There can be little doubt that one of the biggest problems facing the average American today is the incredibly high inflation that has been ravaging the economy. This has pushed up the cost of everything that we buy or consume in our daily lives, which naturally makes it much more expensive to go from day to day than it used to be. We can see the extent of this problem by looking at the consumer price index, which claims to track the price of a basket of goods that is regularly purchased by the average person. This chart shows the annual rate of change in this index during every month over the past twenty-five years:

{kind=link}

In January 2021, the basket of goods measured by the consumer price index cost $261.50 but today it costs $305.70. That is a 16.90% increase over the thirty-one-month period that roughly corresponds to the time that it has been since the panic surrounding the COVID-19 pandemic has wound down. This is important because it was the government spending in response to this pandemic that caused the inflation that is now ravaging the economy.

As I pointed out back in June 2020, the Federal government embarked on an unprecedented spending spree consisting of various economic support programs in response to the pandemic and the resultant lockdowns. This was financed by the Federal Reserve printing new money, ultimately increasing the M2 money supply by 40% in aggregate. The productive capacity of the economy obviously did not increase by anything approaching this, and so we had a situation in which an increased number of currency units were attempting to purchase each unit of economic production. That is the root cause of inflation, as has been seen in Weimar Germany, Hungary, Zimbabwe, and various other places over the past century. Unfortunately, the cost of living in the United States has been growing more rapidly than wages, which is pressuring the budgets of numerous households. After all, approximately 64% of Americans live paycheck-to-paycheck , so when prices increase faster than wages sacrifices have to be made. This has forced people to begin resorting to alternative methods to obtain extra income to support themselves.

As investors, we are certainly not immune to this. After all, we require food to sustain ourselves and energy to heat our homes and businesses. We might also want to enjoy an occasional luxury from time to time. All of these things cost considerably more money than they did two years ago, so we need more income if we are to maintain our lifestyles. Fortunately, we have other methods that we can employ to obtain the money that we need to sustain ourselves and do not have to resort to things such as taking on a second job. After all, we have the ability to put our money to work for us to earn an income.

One of the best ways to do this is to purchase shares of a closed-end fund aka CEF that specializes in the generation of income.

These funds are unfortunately not very well followed by the financial media and many investment advisors are unfamiliar with them so it can be difficult to obtain the information that we would really like to have in order to make an informed investment decision. This is a shame because these funds offer a number of advantages over ordinary open-ended and exchange-traded funds. In particular, a closed-end fund is able to use certain strategies that have the effect of boosting their effective yields well beyond that of any of the underlying assets or indeed pretty much anything else in the market.

In this article, we will discuss the RiverNorth Opportunities Fund ( RIV ), which is one fund that investors can use to earn a high level of income from their portfolios. This is clearly apparent in the fact that the fund boasts a whopping 13.73% yield at the current price. While certainly attractive, any time a fund's yield reaches such a high level, it is a sign that the market expects that the distribution will have to be cut. We will want to pay special attention to that over the course of this article. I have discussed this fund before, but a few months have passed since that time so naturally some things have changed. This article will therefore focus specifically on those changes as well as provide an updated analysis of the fund's financial condition.

About The Fund

According to the fund's webpage , the RiverNorth Opportunities Fund has the objective of providing its investors with a high level of total return. This is a reasonable objective for a fund that invests in either common stocks exclusively or in a portfolio that consists of both stocks and bonds. This fund is the latter, as its portfolio currently consists of a combination of common stocks, preferred stocks, and bonds:

CEF Connect

One thing that we note here is that the fund has a negative allocation to cash. This is due to the fact that this fund employs leverage as a way to boost its overall returns. We will discuss that in more detail later in this article. The fact that the fund is focusing on total return is the only objective that makes sense here. After all, common stocks will deliver their returns through either dividends or capital gains. The fixed-income securities deliver their return primarily through direct payments to the investors, although it is sometimes possible to make a profit due to the fact that the price of fixed-income securities varies due to interest rates. They do not provide any net capital gains due to the fact that they have no connection to the growth and prosperity of the issuing entity. I discussed that in multiple previous articles. Overall, though, the fund is aiming to achieve both capital gains and current income, which is the definition of total return.

As I pointed out in my last article on this fund, the RiverNorth Opportunities Fund uses a very unique strategy to achieve its investment objective. This is described on the webpage:

"The fund employs a tactical asset allocation strategy primarily comprised of closed-end funds, exchange-traded funds, special purpose acquisition companies, and business development companies. RiverNorth implements an opportunistic investment strategy designed to capitalize on the inefficiencies in the closed-end fund space while simultaneously providing diversified exposure to several asset classes."

This might make the above asset allocation chart seem a little strange. The fund does not explicitly list fixed-income securities at all in its strategy description. The way that this fund is gaining its fixed-income exposure is by purchasing shares of closed-end funds that invest in the fixed-income space. We have discussed several of these funds in past articles. In short, the way they work is by buying bonds, floating-rate debt securities, preferred stocks, and similar assets and then applying leverage to boost their effective yields. The fact that they are using leverage is pretty much necessary since bonds are still offering rather terrible returns. After all, the ten-year Treasury is at 4.25% right now, which is less than a money market fund. As bonds offer no net capital gains over their lifetime, that is the total return that a bond investor who holds a bond over its lifetime will receive.

I very much doubt that too many people will be willing to accept a total return of 4.25% when trying to save up for retirement (although a retiree with a sufficiently large portfolio might be okay with that if it is enough to support their desired lifestyle). A closed-end fund that invests in fixed-income securities can frequently yield 10% or higher, which is much closer to the return that many investors desire.

The usual way for a closed-end fund to distribute its returns to investors is to pay out all of its investment returns to investors in the form of distributions. Basically, the fund tries to keep a relatively stable asset base and distribute all of the surplus. When we consider that indices like the S&P 500 (SP500) deliver an average return that is somewhere around 10% annually, we can see how this basic model can result in closed-end funds having incredibly large distribution yields. The funds in which this fund is invested are no exception. Here are the largest holdings of the fund and their yields:

| Asset |

| Weighting |

| Current Yield |

| BlackRock ESG Capital Allocation Term Trust ( ECAT ) |

| 10.16% |

| 9.06% |

| BlackRock Capital Allocation Term Trust ( BCAT ) |

| 9.26% |

| 10.23% |

| Pershing Square Holdings ( PSHZF ) |

| 7.24% |

| 1.38% |

| Saba Capital Income & Opportunities ( BRW ) |

| 3.88% |

| 13.16% |

| United States T-Bills 0% |

| 3.74% |

| N/A |

| Virtus Total Return Fund ( ZTR ) |

| 3.65% |

| 16.81% |

| PIMCO Energy & Tactical Credit Opportunities ( NRGX ) |

| 3.56% |

| 5.23% |

| Western Asset Inflation-Linked Opportunities and Income Fund ( WIW ) |

| 3.55% |

| 8.33% |

| Nuveen Preferred and Income Securities Fund ( JPS ) |

| 3.49% |

| 7.26% |

| Invesco S&P 500 Equal Weight ETF ( RSP ) |

| -12.60% |

| 1.72% |

We can clearly see that the closed-end funds here all boast reasonably attractive yields. Pershing Square Holdings is not a closed-end fund and of course, the U.S. T-Bills also are not closed-end funds. Overall, the worst yield here is the PIMCO Energy & Tactical Credit Opportunities Fund, and even that has a substantially better yield than the S&P 500 Index or U.S. Treasury Bonds right now. Thus, in some ways, the RiverNorth Opportunities Fund is a fund of funds, as 54% of its portfolio consists of closed-end funds. This fund simply collects the distributions paid out by all of these funds and distributes them to its own investors.

However, it also does more than that. One of the characteristics that sets closed-end funds apart from open-ended or exchange-traded funds is that the share price of closed-end funds does not always directly match the price of their assets. This is because these entities are not constantly issuing or redeeming shares, as the other funds do. As such, it is sometimes possible to purchase shares of a closed-end fund at a price that is substantially less than the per-share value of the underlying portfolio. What this fund attempts to do is exploits this by purchasing funds trading for significantly less than their net asset value per share with the intent of earning capital gains as the share price adjusts to match the market value of the assets in the portfolio.

This strategy, unfortunately, necessitates that the fund engages in a great deal of trading. This is one reason why the RiverNorth Opportunities Fund had an annual turnover of 119% as of the end of July 2023.

The reason why the fund's annual turnover is important is that it costs money to trade assets. These expenses are billed directly to the fund's shareholders, which creates a drag on the performance of the fund. It also makes management's job much more difficult. After all, the fund's managers have to earn a sufficient return to cover the added expenses from the trading activity and still have enough left over to satisfy the shareholders' demands for a return. This is a very difficult task that very few management teams are able to accomplish on a regular basis. This is one reason why actively managed funds frequently end up underperforming their benchmark indices. This fund does not appear to be an exception to this rule.

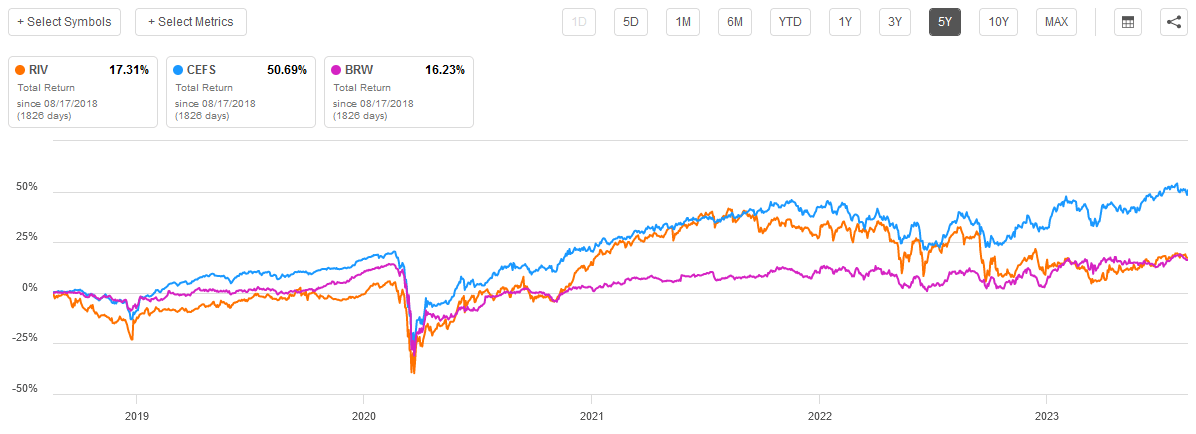

Unfortunately, there is no perfect benchmark for this fund, so I have had to choose a few that are close in order to deliver a total return comparison. Here is the fund's five-year total return performance compared to the Saba Closed-End Fund ETF ( CEFS ) and the Saba Capital Income & Opportunities Fund ((BRW)), which is a closed-end fund that uses a similar strategy to the RiverNorth fund:

{kind=link}

As we can see, the Saba Closed-End Fund ETF does beat the RiverNorth fund pretty handily. However, the RiverNorth Opportunities Fund did beat the Saba Capital & Income Fund. This actually surprised me, since Saba has a reputation for taking over underperforming closed-end funds and turning them around. It is one of the best closed-end fund managers around, so the fact that the RiverNorth fund outperformed it is a very good sign. It is worth noting though that none of these products are actual index funds, as even the exchange-traded fund is an actively managed one.

The biggest reason for the exchange-traded fund's outperformance though appears to have been in late 2022, so it is possible that either the exchange-traded fund's lack of leverage or the fact that the exchange-traded fund does not invest in special-purpose acquisition companies (which basically lost a lot of their appeal once rates started to rise) helped it along. As is always the case though, past performance does not guarantee future results so there is no guarantee that the RiverNorth fund will underperform the exchange-traded fund forever.

Leverage

In the introduction to this article, I stated that closed-end funds like the RiverNorth Opportunities Fund have the ability to employ certain strategies that can boost their effective yields well beyond that of any of the underlying assets. One of these strategies is the use of leverage. In short, the fund is borrowing money and using those borrowed funds to purchase shares of closed-end funds, business development companies, and similar entities. As long as the purchased assets deliver a higher yield than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio.

This fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates, so this will usually be the case. It is important to note though that this strategy is not as effective today with rates at 6% as it was eighteen months ago when rates were effectively 0%. This is because the difference between the rate that the fund has to pay and the yield that it can get on the purchased assets is much narrower than it once was.

Unfortunately, the use of leverage in this fashion is a double-edged sword. This is because debt boosts both gains and losses. As such, we want to ensure that the fund is not employing too much leverage because that would expose us to too much risk. I generally do not like a fund's leverage to exceed a third as a percentage of its assets for this reason. Unfortunately, this fund does not satisfy that criterion.

As of the time of writing, the RiverNorth Opportunities Fund has levered assets comprising 35.70% of its portfolio. When we consider that many of the entities that make up its portfolio are also employing leverage to boost their own yields, we are talking about an enormously levered fund. As I suggested earlier in this article, this could have been one of the reasons why this fund's share price plummeted in late 2022. As such, it appears that this is something of a high-risk, high-reward fund.

Distribution Analysis

As mentioned earlier in this article, the primary investment objective of the RiverNorth Opportunities Fund is to earn a high level of total return. The fund is attempting to achieve that by investing in a portfolio of closed-end funds, business development companies, preferred stocks, and similar things that tend to have very high yields. The fund then applies a layer of leverage on top of this to artificially boost its yield beyond that of any of the assets in the portfolio. The fund then distributes the majority of its own investment returns to the shareholders.

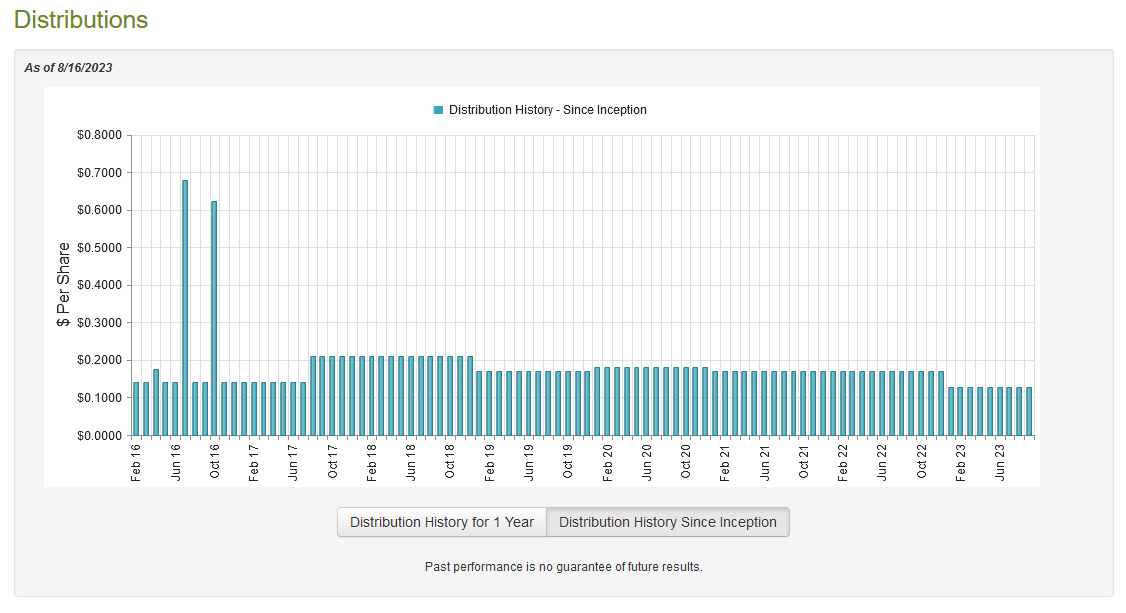

As such, we might expect that this fund would boast a very high yield itself. That is indeed the case as the RiverNorth Opportunities Fund pays a monthly distribution of $0.1278 per share ($1.5336 per share annually), which gives it a 13.73% yield at the current price. Unfortunately, this fund has not been particularly consistent with its distributions over the years. In fact, its distribution has varied quite a bit over time:

{kind=link}

The fact that the distribution has exhibited such considerable variation over the years is likely to be something of a turn-off to those investors that are seeking a safe and secure source of income to use to pay their bills or finance their lifestyles. The fact that the fund cut its distribution back at the start of this year is not likely to help this impression. As I have pointed out numerous times in the past though, the fund's past history is not really the most important thing for anyone considering a purchase today. This is because anybody buying the fund's shares today will receive the current distribution at the current yield and does not really have to worry about the fund's performance in the past, as it will not have a negative impact on them. The most important thing for anyone buying the fund today is how well it can sustain the distribution at the current level. Let us investigate that.

Unfortunately, we do not have an especially recent document that we can consult for the purposes of our analysis. As of the time of writing, the fund's most recent financial report corresponds to the six-month period that ended on January 31, 2023. As such, it will not include any information about the fund's performance over the past six or seven months. However, it will still provide some insight into the events that led to the fund's distribution cut back at the start of this year. That could be quite valuable as we investigate the sustainability of the fund's distribution.

Perhaps the biggest disappointment, though, is that the first half of this year gave us a much stronger market environment overall that could have allowed the fund to earn some capital gains. This will not be reflected in this document.

During the six-month period, the RiverNorth Opportunities Fund received $9,875,118 in dividends and $1,461,809 in interest from the investments in its portfolio. This gives it a total investment income of $11,336,927 during the period. The fund paid its expenses out of this amount, which left it with $8,555,452 available for shareholders. As might be expected, this was nowhere close to enough to cover the $19,528,379 that the fund actually paid out in distributions over the six-month period. At first glance, this is likely to be quite concerning, as we usually like a fund to be able to cover its distributions out of net investment income.

However, this fund does have other methods through which it can obtain the money that it needs to cover its distributions. For example, some of the funds in its portfolio may have made a return of capital distribution, which is not included in net investment income but still represent money coming into the fund. In addition, the fund might have been able to earn some capital gains itself that can be paid out to the investors. Fortunately, the fund was successful at this task, but not as successful as it needed to be.

During the six-month period, the fund reported net realized losses of $8,163,443 but this was fully offset by $9,259,939 net unrealized gains. Overall, the fund's assets did increase by $26,062,677 after accounting for all inflows and outflows during the period, but this was only because it did a capital raise that brought in $38,034,976. The fund basically used some of the money from new investors to cover its distributions, which is not sustainable over any sort of extended period.

As the fund failed to cover the distribution through its investment performance, it explains the distribution cut. It remains to be seen how sustainable this new distribution will be, although I am optimistic at the moment due to the strength of the market year-to-date.

Valuation

It is always critical that we do not overpay for any assets in our portfolios. This is because overpaying for any asset is a surefire way to earn a suboptimal return on that asset. In the case of a closed-end fund like the RiverNorth Opportunities Fund, the usual way to value it is by looking at the fund's net asset value. The net asset value of a fund is the total current market value of the fund's assets minus any outstanding debt. It is therefore the amount that the shareholders would receive if the fund were immediately shut down and liquidated.

Ideally, we want to purchase shares of a closed-end fund when we can obtain them at a price that is less than the net asset value. This is because such a scenario implies that we are acquiring the fund's assets for less than they are actually worth. That is, fortunately, the case with this fund today. As of August 16, 2023 (the most recent date for which data is available as of the time of writing), the RiverNorth Opportunities Fund has a net asset value of $12.01 per share but the shares only trade for $11.16 per share. This gives the fund's shares a 7.08% discount on net asset value at the current price. This is a bit better than the 6.66% discount that the shares have had on average over the past month, so the price certainly looks acceptable today.

Conclusion

In conclusion, the RiverNorth Opportunities Fund is a rather unique fund in the closed-end fund space. It acts something like a fund of funds, except that it includes other high-yielding assets beyond closed-end funds. This allows it to provide access to certain assets that may otherwise be difficult to include in a diversified portfolio. Risk-averse investors may not like the leverage here, though, as the fund is employing a significant amount of leverage to purchase assets that are themselves leveraged. It is also uncertain how sustainable the distribution is, as generally speaking the market will not allow most things to enjoy a 13.73% yield for very long unless there is a risk of a distribution cut. Fortunately, the fund's valuation is reasonable right now.

For further details see:

RIV: This 13.73%-Yielding CEF Has Unique Qualities, But Be Careful Of Leverage