RIV - RIV: Unique Strategy And Beats The Market But Concern About The Distribution

2023-03-13 08:43:33 ET

Summary

- RIV invests in a portfolio of CEFs, BDCs, and other very high-yielding assets to try and give investors an outsized yield.

- The fund's mix of bonds and common equity would have been an advantage in years past but that is not the case today.

- The fund has been outperforming the market over the past year or so, which could make it an attractive holding for as long as the market remains weak.

- RIV appears to be financing its distribution by raising new money from investors right now, which is not sustainable long term.

- The fund is currently trading at a reasonably attractive discount to the net asset value.

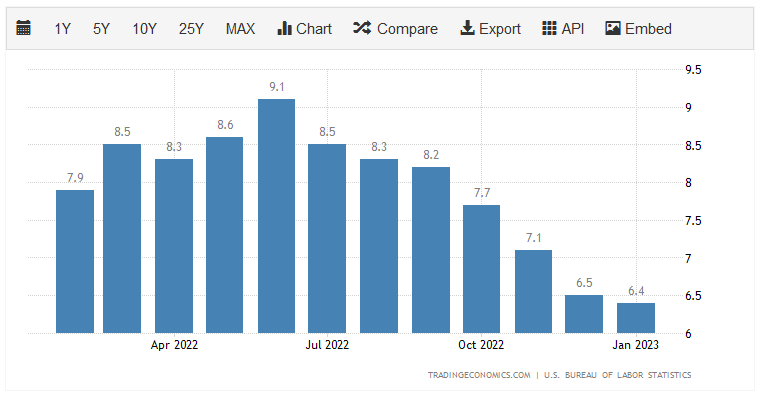

It almost seems that we cannot go a single day without hearing about a problem with the economy. The Federal Reserve's monetary tightening policy is certainly having an impact on everything, which we clearly saw last week with the collapse of Silicon Valley Bank. The reason for its policy was to combat another problem that was causing serious problems for Americans, which is the incredibly high inflation rate. Over the past twelve months, there has not been a single instance of the consumer price index appreciating less than 6.4% year-over-year:

{kind=link}

This has been causing havoc among those of lesser means, as it has greatly increased the cost of food and energy at a time when many people do not have sufficient room in their budgets to absorb the increase. This has led to an uptick in the number of people that are being forced to seek out second jobs or enter the gig economy just to obtain the money that they need to survive. I discussed this in a recent blog post .

Fortunately, as investors, we have other methods that we can employ to get the extra money that we need to cover the rising cost of living. After all, we have the ability to put our money to work for us. One of the best ways in which we can do that is by purchasing shares of a closed-end fund that specializes in the generation of income. Admittedly, closed-end funds is not an asset class that is actively followed by many investors. This is a shame, really, as they offer an excellent way to easily acquire a diversified portfolio of assets that can usually deliver a higher yield than pretty much anything else in the market.

In this article, we will discuss the RiverNorth Opportunities Fund ( RIV ), which is one fund that has proven attractive among income-seeking investors recently. This is hardly surprising as its 13.46% current yield seems almost too good to be true. As regular readers may recall, I have discussed this fund before, but a few months have passed since that time so naturally, a few things have changed. This article will focus specifically on these changes as well as continue our discussion about the sustainability of the fund's incredibly large distribution.

About The Fund

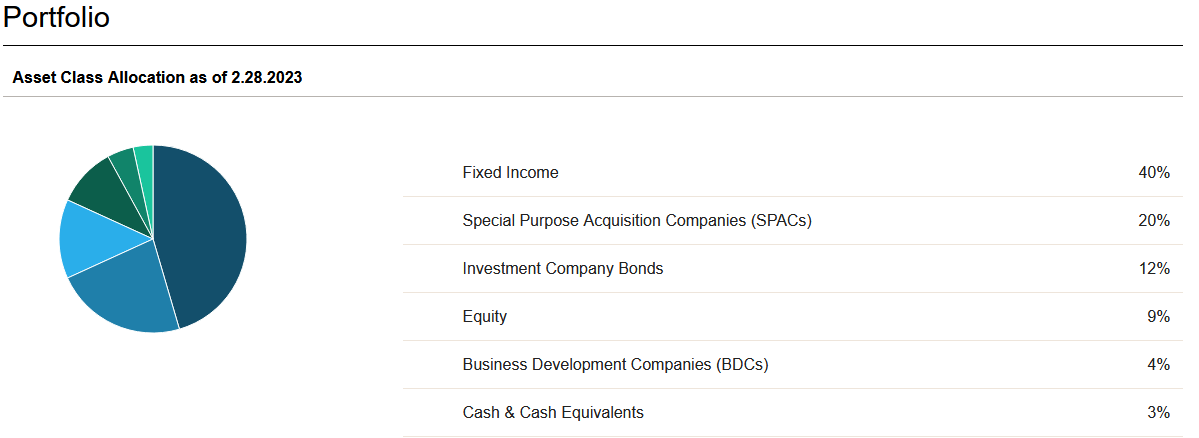

According to the fund's webpage , the RiverNorth Opportunities Fund has the stated objective of providing its investors with a high level of total return. This is not surprising considering that the fund describes its strategies as very open-ended. The fund invests in a combination of closed-end funds, exchange-traded funds, special purpose acquisition companies, and business development companies in order to achieve its objective. These entities themselves may engage in either debt or equity financing. After all, closed-end funds, exchange-traded funds, and business development companies will frequently own both common equities and bonds. Special purpose acquisition companies are different, and they have lost a lot of their former popularity over the past year, so they probably are not going to be particularly important to this fund going forward. However, currently, about 20% of the fund's assets are invested in special-purpose acquisition companies:

{kind=link}

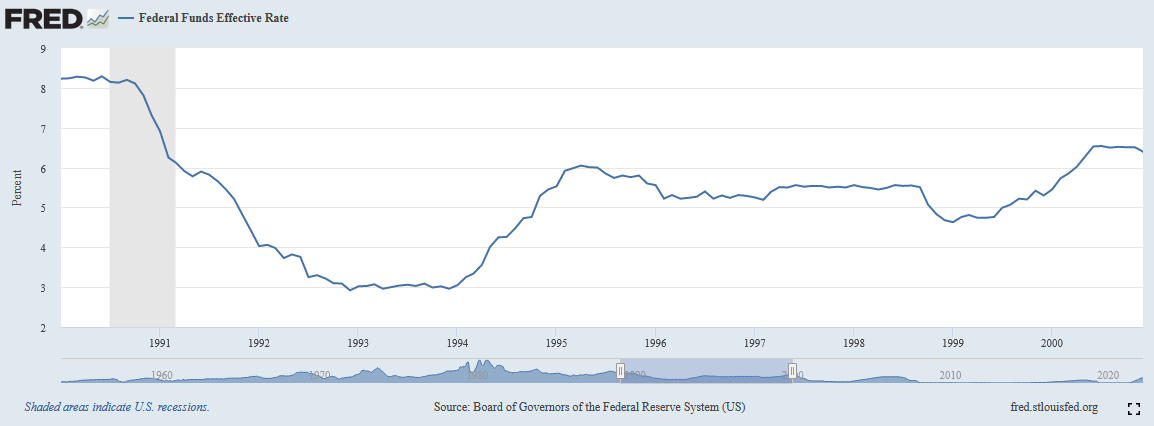

Overall, this does give the company an interesting amount of diversity as bonds and equity have generally different fundamentals. In fact, in the past, the two usually moved opposite each other. For example, when stocks went up, interest rates also were usually going up as the Federal Reserve tried to cool down the economy, which caused bond prices to decline. This was the case in the late 1990s technology bubble. We can see that quite clearly here as the Federal Reserve increased the federal funds rate significantly in 1994 and again in 1999 and 2000:

{kind=link}

While rising interest rates did definitely have a negative impact on bond prices during those years, anyone that can remember 1999 and 2000 certainly knows that stocks did not go down! Unfortunately, this inverse correlation between stocks and bonds appears to be broken today because of the Federal Reserve's longstanding "free money" policy. Thus, the protection and stability that the RiverNorth Opportunities Fund may once have provided with its diverse portfolio that includes both asset types is no longer as attractive as it would have been twenty years ago.

The fact that this fund can invest in closed-end funds could provide an opportunity, though. The fund points this opportunity out on its webpage with the following statement:

While RiverNorth Capital Management, LLC believes markets are generally efficient, closed-end funds offer a unique structure whereby investors can purchase a diversified fund and potentially generate additional return through the change in the relationship between the closed-end fund's market price and Net Asset Value.

This is a reference to how closed-end funds will frequently deliver a different performance in the market than the underlying portfolio. That is not true with exchange-traded funds or ordinary open-ended funds, which perfectly track the performance of the fund's actual portfolio. For example, over the past year, midstream closed-end funds have performed much worse in the market than the actual portfolio. The fact that the RiverNorth Opportunities Fund can purchase shares of underperforming closed-end funds and wait for its market price to react appropriately could provide investors with a higher return than other funds may be able to offer. In addition, the fund can opportunistically switch between debt funds, equity funds, and even option-income funds at any time to react to emerging opportunities or changing market conditions. This gives it a certain flexibility that could prove to be beneficial for investors over the long term.

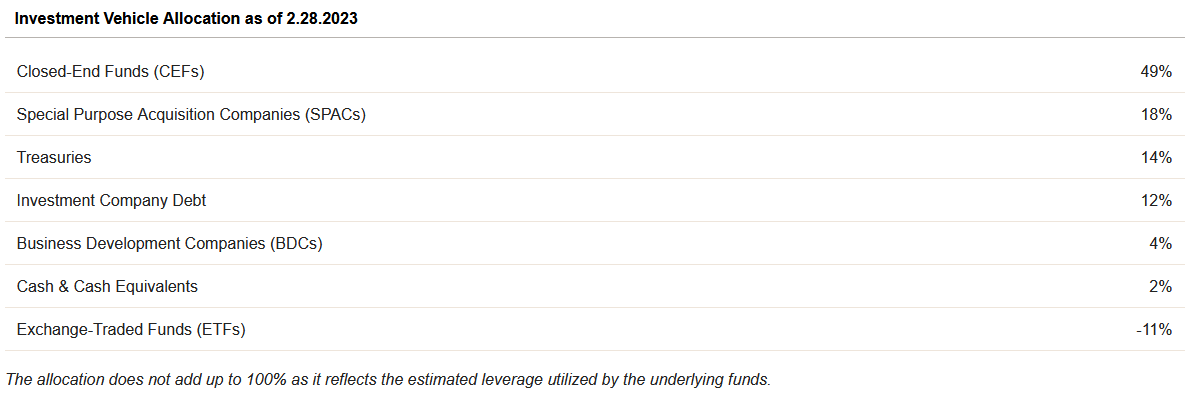

The fund certainly takes advantage of this flexibility. Currently, 49% of the fund's assets are invested in closed-end funds:

{kind=link}

These are obviously a combination of fixed-income and equity funds, per the earlier chart that shows that the fund's overall exposure to fixed-income assets is only 40%. One curious thing that we see above is that the fund currently has a negative allocation to exchange-traded funds. This means that the fund has actually been shorting these funds in order to raise money to purchase other assets. Unfortunately, we do not know what exchange-traded funds these are so we cannot be sure how risky these short positions are. In the fund's most recent financial report , it discloses three short positions:

RiverNorth

So, in effect, we see a short position in the S&P 500, a short position in a senior loan fund ( SRLN ), and a short position in junk bonds. I am not so sure that the senior loan short position is very smart in a time of rising interest rates since those are floating-rate loans that benefit from rising interest rates. The other two short positions make a lot of sense right now. However, the fund can easily purchase closed-end funds invested in similar asset classes to these funds as a hedge so these short positions may not be as big a risk as we might expect should the positions move against the fund. It is important to note though that the report that discloses this position is eight months old, so as I said earlier, we cannot be certain if these are indeed the exchange-traded funds that make up the short position that the fund had two weeks ago.

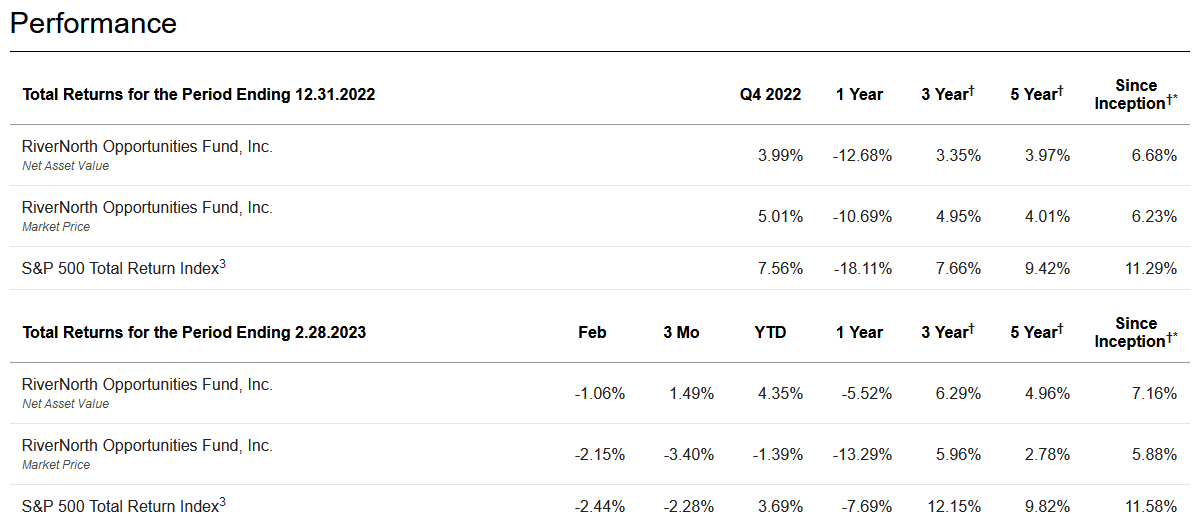

One unfortunate thing that we see with this fund is that the RiverNorth Opportunities Fund has an incredibly high annual turnover. The fund's turnover last year was 119.0%, which is well above the average for any closed-end fund. In fact, that is one of the highest annual turnovers that I have seen of any closed-end funds. The reason that this could be concerning is that it costs money to trade any asset, and these expenses are billed directly to the fund's stockholders. This creates a drag on the fund's performance that management must then work to overcome. That can be a very difficult task that few management teams manage to accomplish with any sort of consistency. This one has generally failed at that task, although it has managed to beat the S&P 500 Index during bear markets:

{kind=link}

We can see that the fund has generally been outperforming the S&P 500 during some of the more recent periods, at least when we look at the fund's net asset value performance. This chart clearly illustrates the performance differential that can exist between a closed-end fund's portfolio performance and its market price performance. We do see though that both have struggled to beat the index during periods of market strength, such as most of the past decade prior to 2022. Thus, this fund may make sense during times of market weakness like today, but it may not be the best choice during a strong bull market.

Leverage

As stated in the introduction, closed-end funds like the RiverNorth Opportunities Fund have the ability to deliver higher yields than pretty much anything else in the market. This fund actually manages to have a higher yield than the underlying assets possess. The way that it does this is through the use of leverage. In short, the fund borrows money and then uses that borrowed money to purchase shares of closed-end funds and other assets. As long as the purchased assets have a higher yield than the interest rate that the fund has to pay on the borrowed assets, this strategy works pretty well to boost the effective yield of the portfolio. As this fund is capable of borrowing at institutional rates, which are considerably lower than retail rates, this will usually be the case.

However, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that the fund is not employing too much debt since that will expose us to too much risk. I do not usually like to see a fund's leverage exceed a third as a percentage of its assets for this reason. The RiverNorth Opportunities Fund's levered assets currently comprise 33.84% of its assets, so it does slightly exceed this one-third limit. However, it is not higher by very much and when we consider that the largest asset class in the fund's portfolio is other closed-end funds then it is probably okay. After all, closed-end funds have a tendency to be at least somewhat stable relative to many other things over extended periods of time. The balance between risk and reward appears to be reasonably acceptable here.

Distribution Analysis

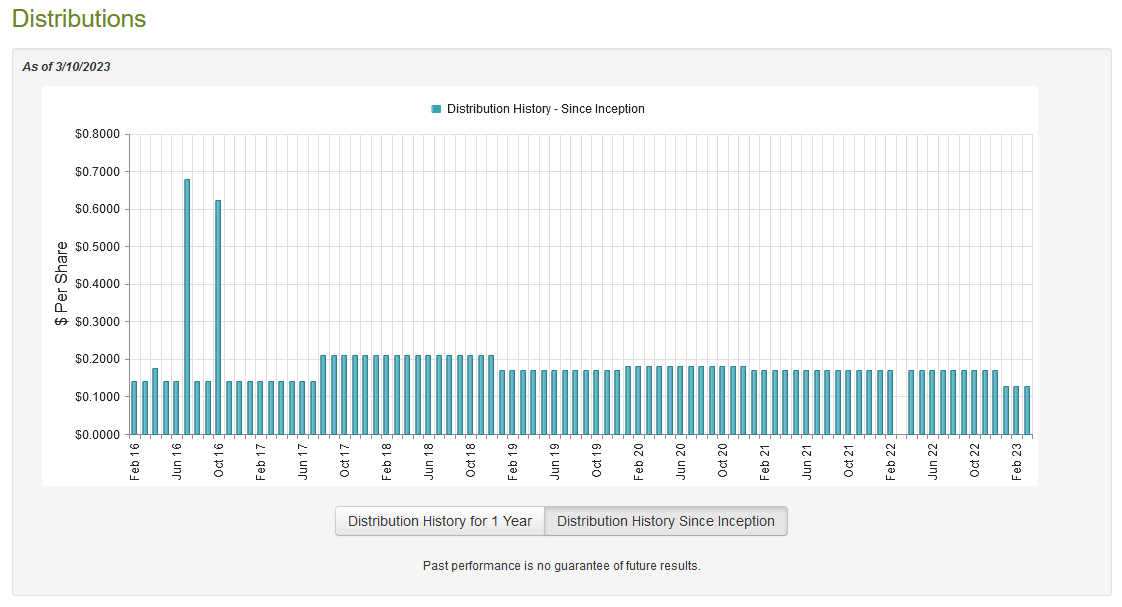

One of the biggest reasons why investors purchase the RiverNorth Opportunities Fund is because of its focus on generating a high total return through both current income and capital appreciation. In order to achieve this objective, it invests in a portfolio of closed-end funds, business development companies, and other entities that tend to have very high total returns. It then applies a layer of leverage to boost its yield further. Thus, we might assume that this fund would boast a very high distribution yield. That is certainly true as it pays out a monthly distribution of $0.1278 per share ($1.5336 per share annually), which gives it an incredible 13.46% yield at the current price. The fund's distribution has varied a bit over the years and unfortunately, it was forced to cut back in January:

{kind=link}

In my previous article on this fund, I predicted that its distribution would not be sustainable and indeed it cut the following month. This is likely to prove to be a bit of a turn-off to anyone that is looking for a stable and secure source of income to use to pay their bills, but apart from midstream funds and a handful of specialty debt funds, it is very hard to find any closed-end fund that was not forced to reduce its distribution in the past few months. The most important thing for anyone purchasing the fund today is how well it can sustain its current distribution. After all, someone buying today will receive the current distribution and does not really have to care about what past investors received.

Unfortunately, we do not have a particularly recent report that we can consult to analyze the distribution. The fund's most recent financial report (linked earlier) corresponds to the full-year period that ended on July 31, 2022. As such, it will not include any information about the fund's performance over the past several months. This is quite disappointing considering that market volatility was present in the second half of last year just as much as it was in the first half. During the full-year period, the fund received a total of $7,302,247 in dividends and another $577,127 in interest. That gives the fund a total income of $7,879,374 over the period. It paid its expenses out of this amount, which left it with $3,010,738 available for investors. As can probably be guessed, that was nowhere close to enough to cover the $38,234,643 that the fund actually paid out in distributions during the period. This is something that could prove quite concerning as clearly the fund did not have enough net investment income to cover the distribution.

The fund does have other methods to obtain the money that it needs to cover the distribution, however. For example, it could make up the difference through capital gains. As might be expected from the poor performance of nearly every asset class during 2022 though, it failed at this during the year. The fund reported net realized gains of $484,152 during the period but this was more than offset by $20,966,192 of net unrealized losses. The fund clearly did not manage to cover its distribution through its actual investment return. In fact, the net investment income plus net realized gains do not even come close to enough. The fund did, however, sell $98,018,703 of new shares during the period. The money that it received from that was enough to cause the fund's assets to increase by $36,978,477 after accounting for all inflows and outflows. However, the fund only managed to cover its distribution by bringing in new money, which is not sustainable over any sort of extended period. This could explain the distribution cut as the new shares increased the cost of an already unaffordable distribution. It remains to be determined though whether the fund manages to sustain the current distribution. We will want to watch its next two earnings reports very closely.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to generate a suboptimal return on that asset. In the case of a closed-end fund like the RiverNorth Opportunities Fund, the usual way to value it is by looking at the fund's net asset value. The net asset value of a fund is the total current market value of all the fund's assets minus any outstanding debt. It is therefore the amount that the shareholders would receive if the fund were immediately shut down and liquidated.

Ideally, we want to purchase shares of a fund when we can acquire them at a price that is less than the net asset value. This is because such a scenario implies that we are buying the fund's assets for less than they are actually worth. That is, fortunately, the case with this fund today. As of March 10, 2023 (the most recent date for which data is available as of the time of writing), the RiverNorth Opportunities Fund had a net asset value of $12.36 per share but the shares currently trade for $11.39 per share. That is a 7.85% discount on the net asset value. This is a much better price than the 5.42% discount to net asset value that the shares have traded for on average over the past month, so the price certainly seems reasonable right now.

Conclusion

In conclusion, the RiverNorth Opportunities Fund does not appear to be a bad fund to purchase today. The fund has been able to outperform the broader market during times of weakness, which is attractive as it appears unlikely that the current market weakness will fade anytime soon. The fund has a very unique strategy, which could allow it to add some diversification to a portfolio that is invested mostly in stocks and bonds. Unfortunately, the fact that the fund appears to be depending on raising money to maintain that distribution is concerning and it is something that we will want to check on in the next few financial reports. The price is right, but that concern about the distribution might make it worth sitting on the sidelines until the next financial report is released.

For further details see:

RIV: Unique Strategy And Beats The Market, But Concern About The Distribution