RVSB - Riverview Bancorp: Depleting Deposits And Low Growth Overshadow Dividends

Summary

- RVSB’s high revenues, supported by increasing NII, are insufficient to meet the industry standards.

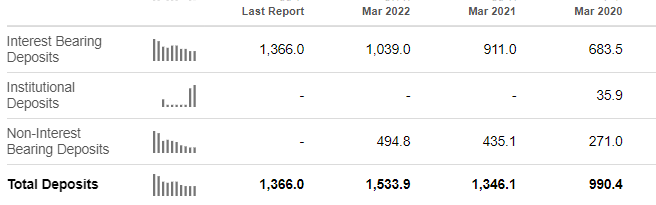

- Its deposits increased substantially during 2021 and 2022, but they seem to retreat to the 2020 level, making it a cause of concern for the management.

- It has been paying dividends consistently with the latest yield crossing 3.3% and having a CAGR of 19.2% since 2015.

- My current opinion on RVSB stock is a Hold.

Thesis & Introduction

Riverview Bancorp, Inc. ( RVSB ) has witnessed a commendable uptick in its net interest income ((NII)) for two consecutive quarters, Q2 2022 and Q3 2022. During Q2 2022, the NII stood at 3.3% and increased to 3.5% in Q3 2022. This development coincides with the possibility of the bank achieving its highest revenue and net income in the past decade. As of December 2022, its total revenue amounted to $64.5M, closely trailing its highest revenue of $65.5M a year earlier. With three more months left in its financial year (April to March), the bank's net income stands at $19.2M, with the potential to surpass the $21.8M net income achieved in 2022. Also, the bank has been able to maintain consistent growth in dividends with regular repurchase programs to reward its shareholders.

Despite its all-time high revenue, the latest quarter has brought troubling news for Riverview Bancorp, Inc. as its deposits experienced a significant decline of almost $124M . This drop is a cause for concern for the regional bank, especially considering the ongoing inflation and increasing impatience among depositors in managing their finances. To simplify further, the customers may make withdrawals in search of better yield or use their savings to meet their increased routine expenses.

Riverview Bancorp, Inc. is a bank holding company that oversees Riverview Community Bank. It caters to small and medium-sized businesses, professionals, and individuals looking to build wealth. The institution offers a variety of deposit products and lending services, including commercial business, real estate, and consumer loans. It also provides mortgage brokerage and loan servicing activities, as well as asset management services such as trust, estate planning, and investment management.

Disappointing growth rates

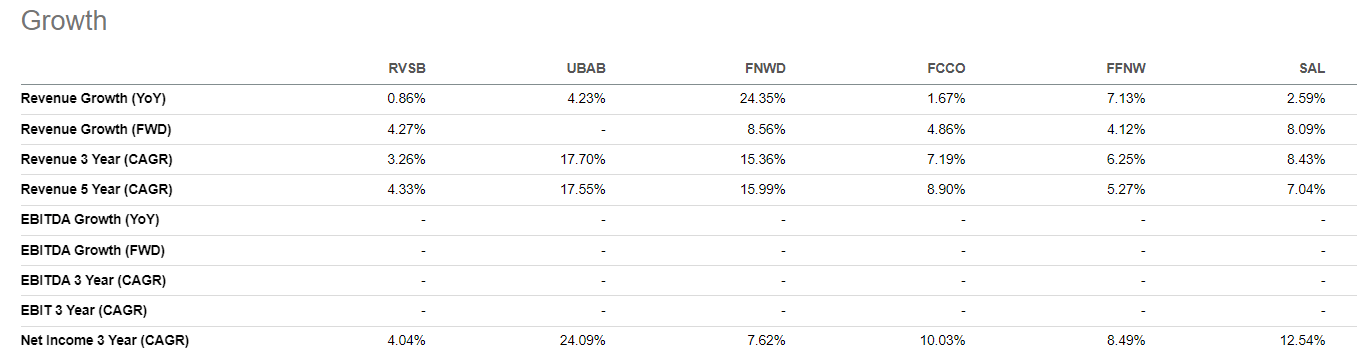

RVSB is performing exceptionally when evaluated in isolation, but amongst its peers, it has seen the lowest revenue growth at the 3Y and 5Y mark. Compared to the industry average of 11.6%, its 3Y revenue growth stands at only 3.26%. The same can be said for its net income growth as well which is the lowest at 4.04%, well below the industry growth rate of 15.69%.

{kind=link}

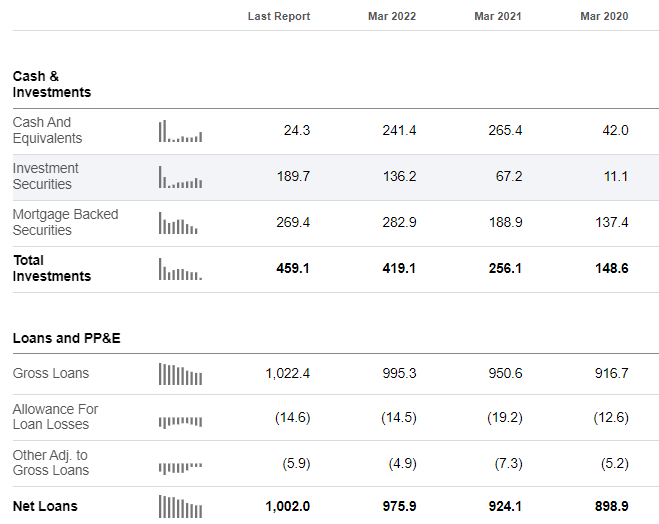

Such a stark difference can be attributed to its incapability to acquire new loans despite having record cash and deposit levels and resorting to investing them in mortgage-backed securities and other investments. From 2020 to 2022, when its deposits increased by 35%, its gross loans increased by only 11.5%. This became more concerning when it added only $5M in Q3 2022 and observed a decrease of $1.5M in the quarter before that.

{kind=link}

{kind=link}

Growing dividends, repurchases, and improving asset quality

RVSB halted the dividends after the events that unfolded in 2008. That halt was finally lifted after seven years in 2015, and since then, the bank has been able to raise dividends consistently. In this period, its dividend has achieved compounded annual growth rate ((CAGR)) of 19.2% and a dividend yield trailing 12 months ((TTM)) of 3.3%. This trend might continue as the bank has a steady flow of income and no expansion plans for now.

To add to the dividends, RVSB launches share repurchase programs frequently. In November 2022, it announced a repurchase program for six months, and as per its Q3 2022 report, it repurchased 10,797 shares at a total cost of $81,000 under the November 2022 repurchase program at an average price of $7.51 per share.

Bank has also done exceptionally well in taking its nonperforming loans to total assets ratio as low as 0.8% per the latest 10-Q . Almost 100% of these loans are guaranteed by the Small Business Administration ((SBA)) and the United States Department of Agriculture ((USDA)). During the financial years 2022 and 2023, Riverview has overturned provisions for loan losses by more than $5M of which $0.7M belongs to the current fiscal. The bank has also maintained a comfortable risk-based capital ratio (tier 2 ratio) of 16.7% and a tier 1 ratio of 10.1%. This exemplifies its financial strength.

Depleting deposits in the last two quarters

In Q3 2022, Riverview Bancorp, Inc. experienced a significant 8.3% drop in deposits, bringing it back to 2021 levels of $1.4 billion. Management attributes the decrease to deposit pricing pressures and customers seeking higher-yielding investment alternatives, such as money market accounts offered by Riverview Trust Company. This is the second consecutive drop in deposits, the previous being only around $6 million, causing concern for management.

Most of the deposits received by the bank in the past two years were allocated more toward investments and less towards loans. Further, the bank currently only has $24.3 million in cash and equivalents, and if withdrawals continue, it may be forced to liquidate its investments, which could impact its income statement as well as its balance sheet.

Valuation

Small banking and insurance firms tend to have fair values within plus or minus 25% of their book values due to limited growth prospects or challenging expansion opportunities. Also, the majority of their assets and liabilities are reflected at fair value. But, valuing RVSB using book value could be misleading because of the presence of intangible assets, which create a difference of almost 20% between the book value per share and the tangible book value per share.

Hence, I value it based on the price-to-earnings (P/E) ratio. The median P/E ((TTM)) of the industry stands at 10x while the normalized net income ((TTM)) for Riverview is $15.6M. Currently, it has 21.5M outstanding shares. Hence, the intrinsic value is as follows:

| Particulars |

| Value |

| Normalized net income ((TTM)) |

| $15.6 |

| P/E GAAP ((TTM)) |

| 10.0x |

| Value of equity |

| $155.9 |

| Number of outstanding shares |

| 21.5 |

| Intrinsic value |

| $7.3 |

The intrinsic value of $7.3 is a tad above the current price of $7.18 making it almost correctly valued by the market.

Conclusion

Stock Tracking Opinion

Riverview increased its deposits in 2021 and 2022, but it looks like they were the two exception years in its slow growth of deposits, loans, and revenues. The bank hasn’t been able to deploy its resources at full potential and the way the last two quarters have unfolded and the macroeconomic outlook becoming bleaker with each day passing the road to high revenue and net income growth is only going to get tougher. Considering these, I will keep RVSB on my watchlist and wait to see changes in the deposits and revenue growth.

Investment Opinion

In consensus with Quant rating on Seeking Alpha, my current rating on the stock is a Hold.

For further details see:

Riverview Bancorp: Depleting Deposits And Low Growth Overshadow Dividends