CNS - RLTY And RNP: 2 Strong REIT Funds But RLTY The Better Value

2023-07-06 07:13:20 ET

Summary

- Cohen & Steers is the top REIT closed-end fund team that offers several choices for real estate exposure.

- RLTY and RNP are two funds that have provided similar results, but their valuations have been quite different, leading to a swap potential in the past.

- We are looking at how that swap played out and why RLTY is still the more favored choice today due to valuation.

Written by Nick Ackerman, co-produced by Stanford Chemist. A version of this article was originally published to members of the CEF/ETF Income Laboratory on June 21st, 2023.

In December of last year, I swapped Cohen & Steers REIT and Preferred Income Fund ( RNP ) to Cohen & Steers Real Estate Opportunities and Income Fund ( RLTY ). RLTY is the newest offering from the Cohen & Steers ( CNS ) team. Along with Cohen & Steers Quality Income Realty Fund ( RQI ) and Cohen & Steers Total Return Realty ( RFI ), all these funds have significant overlap but some worthwhile differences too.

RNP is fairly evenly split at 51/49% with equity positions and preferred & fixed-income investments. RLTY takes their allocation a bit heavier in the equity space with around a 67/33% split . So while the long-term results can diverge with different allocations, they'll still loosely correlate enough to exploit the discount/premiums in the funds.

I wanted to revisit to highlight why making this swap made sense but also that RNP is now trading at an attractive enough discount to make it worth considering. Albeit, RLTY is still trading at the heavier discount and would be my preferred selection if allocating new capital to the C&S funds.

RLTY Basics

- 1-Year Z-score: 0.15

- Discount: -12.26%

- Distribution Yield: 9.32%

- Expense Ratio: 1.74%

- Leverage: 36.66%

- Managed Assets: $401.02 million

- Structure: Term (anticipated liquidation date February 23rd, 2034)

RLTY's investment objective is "high current income." The secondary objective is for "capital appreciation." To achieve this, the fund will invest "at least 80% of its managed assets in (i) real estate-related investments, and (ii) preferred and other income securities." This is pretty straightforward and quite similar to Cohen & Steers' other real estate-focused funds.

RNP Basics

- 1-Year Z-score: -0.74

- Discount: -4.86%

- Distribution Yield: 8.51%

- Expense Ratio: 1.10%

- Leverage: 32.90%

- Managed Assets: $1.37 billion

- Structure: Perpetual

RNP's objective is "high current income" and a secondary objective of "capital appreciation." To achieve this, they invest just as their name would suggest; "investment in real estate and diversified preferred securities." They will invest in both U.S. and global positions. Most of the portfolio has been held in the U.S. or North American investments.

The Results

I discussed the swap in a previous article , and the exact day I made the swap was December 2nd, 2022. So we are roughly 7 months after that switch took place. Since then, neither fund has offered particularly attractive total return results. However, RLTY was the clear winner during this time, being able to produce slightly positive total return results on a share price basis rather than RNP's decline. Their total NAV return results were quite similar, which highlights why they can be worth exploiting the discount/premium feature in CEFs.

Even more interesting is that this swap could have worked out even better, but RLTY saw its discount widen further during this period too. It's off of the lows it touched recently, but it is still attractive. RNP recently bounced off its discount low that it was trading at.

RLTY's valuation wasn't anything like RNP, though, which began to trade at a significant premium. This premium was highly unusual as it was the highest in the fund's life. That's usually a good sign on its own that it's time to exit a fund and search elsewhere for a better deal.

The primary culprit for such a premium would have seemingly been the fund's large year-end special in 2022. The ex-div date on that was December 7th, so investors bid up the shares to this richly valued level. This highlights that large specials can also sometimes be exploited in CEFs without even having to hold through the ex-div date. By simply selling at the inflated price, the special was 'locked' in and then some.

RLTY Or RNP Today?

For the most part, RLTY still presents the best value out of all the C&S REIT funds. As the newest fund, it is likely to carry this discount for a while.

That's even if RLTY puts up almost virtually the same total NAV return results as it has done in the last year. Investors seem to overvalue a fund being around longer than a newer fund, even if one is giving the same results and is a much better valuation. Immediately buying a fund at launch has proven to be a terrible idea, but since RLTY is now at a massive discount already with over a year in, it's something that investors should probably consider now.

Ycharts

That being said, at the very least, RNP could be worth checking out at this time if you are looking for more of a preferred tilt. The discount present after dropping from the sharp premium is what makes it a consideration today.

The preferred sleeves of these portfolios took a substantial hit in March with the banking crisis. This is because these portfolios don't invest in REIT preferred and fixed-income, but they go into the financial space with bank and insurance exposure.

These make up the overwhelming majority of the preferred sleeve as banks are the largest issuer of preferreds to help meet regulations for capital requirements. These are perpetual non-cumulative to qualify for the banking regulation needs. That can make them relatively riskier, but for the most part, these are from the largest banks in the world, including JPMorgan ( JPM ), Citigroup ( C ), Wells Fargo ( WFC ) and Bank of America ( BAC ).

RLTY doesn't provide a breakdown of their preferred sleeve allocations by sector, but RNP does to give us some color of the exposure. The complete holding list shows a lot of the same banks preferred in RLTY as well.

RNP Preferred Allocation Breakdown (Cohen & Steers)

By having more preferred in the fund's portfolio, net investment income coverage should be better for RNP. NII provides a more predictable and steady distribution coverage compared to relying solely on capital gains. The regular distribution for RNP comes to $1.632 annually. NII in the last report came to $0.88, providing NII coverage of ~54%.

For RLTY, we are looking at $1.32 paid annually, but this was interesting just recently increased with the latest quarterly announcement. Their last report had NII at $0.40. That would put NII coverage at ~32% based on their previous distribution. However, this isn't an apples-to-apples comparison between these two funds either.

For RLTY's report, it is only an abbreviated period between its launch on February 24th, 2022, to December 31st, 2022. This would be anticipated to increase in the next report now that the portfolio is established. Which would be a positive as they now sport a higher payout with the recent boost.

We'll be able to compare directly, too, in the future, as both of these funds have the same fiscal year-end, which aligns with the calendar year-end. The good sign is that NII is mostly in line with each of the fund's preferred/fixed-income allocations.

Basically, it would be anticipated that RLTY will always require more capital gains to fund their distribution compared to RNP. This is simply how the portfolios are constructed. RQI's NII coverage comes to only around 31% because it carries even less preferred exposure at around 21% of its portfolio.

For the most part, REITs haven't been having a great time either. As they also have to contend with higher interest rates while the Fed bumps up rates. This makes financing new projects and acquisitions more expensive. Also, as income investments, investors can now receive a risk-free yield of ~5% or more.

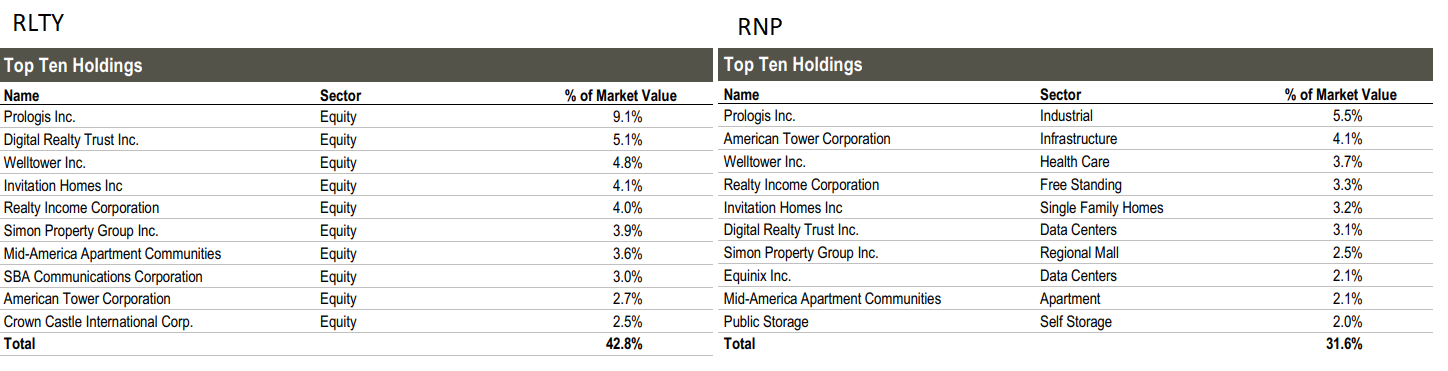

When looking at the top ten holdings, we can see where there is significant overlap. RLTY is more concentrated in the top ten compared to RNP. RLTY carries 168 total positions, and RNP is listed as having 291.

{kind=link}

However, they share overlap with Prologis ( PLD ) as both are their largest holding. Then it is a bit more mixed after that, but the only positions that aren't the same in the top ten are SBA Communications ( SBAC ) and Crown Castle ( CCI ), which are shown in RLTY's top ten. Instead, those are 'replaced' by Equinix ( EQIX ) and Public Storage ( PSA ) for RNP.

However, they are also on the complete holdings list at the end of the first quarter - meaning they are still exposed to these holdings, but they are presently at lower weightings. For RLTY, EQIX is position number 11, and PSA is the 14th largest.

Thus, exactly why we see such a high correlation even if the exact weightings are different in the positions. The majority of the largest allocations of the fund have significant overlap. It's really when you start getting into the much smaller allocations that you'd start to notice differences. This reinforces why the fund with the largest discount can make the most sense.

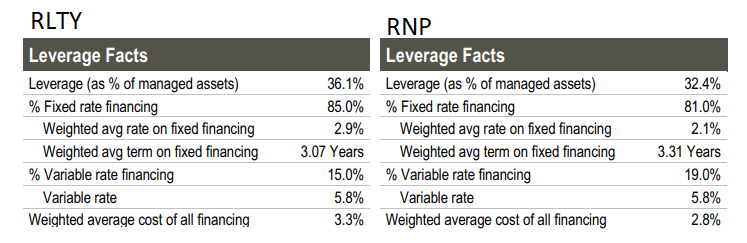

RLTY has a higher expense ratio, but that hasn't dented the results when compared to the other funds. Both funds are also leveraged, adding more volatility and risk. RLTY carries a bit more leverage with a 36.66% leverage ratio compared to RNP's 32.9%.

While leverage is a concern in the current environment due to rising costs, both of these funds have largely locked in their current rates for the next several years. This would make them less susceptible to the damage of higher leverage costs that we are seeing in other CEFs where leverage now doesn't really make sense as they can't produce returns high enough to get over the hurdle of the cost of said leverage.

{kind=link}

Conclusion

At the end of the last year, investors were presented with the opportunity to swap RNP for investment in RLTY. Both investments performed negatively during this time, but RLTY saw significantly less downside. Both the fund's underlying portfolios, as measured by total NAV returns, performed essentially flat during this time. This was as preferreds and REITs both have been dealing with higher interest rates and bank failures. Today, RLTY still presents the better valuation by far. However, RNP is at least back at a discount where it's getting interesting again.

For further details see:

RLTY And RNP: 2 Strong REIT Funds, But RLTY The Better Value