RLTY - RLTY: REIT Exposure At A Discount With A Strong Distribution Yield

2023-12-29 11:57:06 ET

Summary

- RLTY is a strong candidate for investment due to the potential for three interest rate cuts next year and its deep discount.

- The fund's performance has been market-beating and its discount has widened, indicating even better underlying performance.

- RLTY's underlying portfolio includes REIT investments and preferred securities, making it attractive in a lower interest rate environment.

Written by Nick Ackerman, co-produced by Stanford Chemist.

We last covered Cohen & Steers Real Estate Opportunities and Income Fund ( RLTY ) earlier this year. It was just as the risk-free Treasury Rates were beginning to surge. Interestingly enough, similar to how they did in 2022, they ended up peaking sometime in October. That said, with the latest news from the Fed suggesting that there could be three interest rate cuts next year, RLTY is looking like a strong candidate with a deep discount. The party seems to be just getting started as the recovery takes hold in the real estate investment trust area of the market.

The performance of RLTY was market-beating on a total return basis during this fairly short period of time as rates began to falter, allowing for a recovery to start to take hold. Since our last coverage, the discount had actually widened a touch in this period as well, meaning that underlying performance would have been even better in the portfolio.

RLTY Performance Since Last Update (Seeking Alpha)

With the FOMC meeting and new Fed projections being released, yields were sent spiraling lower after already coming down meaningfully through November. We saw the market rally higher, but, in particular, the interest rate-sensitive sectors, such as REITs, surged higher; the utility sector is also included in this category.

RLTY Basics

- 1-Year Z-score: -0.78

- Discount: -13.52%

- Distribution Yield: 9.38%

- Expense Ratio: 1.81%

- Leverage: 35.59%

- Managed Assets: $411.2 million

- Structure: Term (anticipated liquidation date February 23, 2034)

RLTY's investment objective is "high current income." The secondary objective is for "capital appreciation." To achieve this, the fund will invest "at least 80% of its managed assets in (i) real estate-related investments, and (ii) preferred and other income securities." This is pretty straightforward and quite similar to Cohen & Steers' other real estate-focused funds.

The fund's expense ratio is on the high end, and it actually increased from the 1.74% operating expenses we saw at the end of its reporting for 2022. With the leverage expense included, the total expense ratio climbed to 4.98% from 3.14%. Of course, the primary driver during this period was the higher costs of the leverage - of which they are on the high side they employ.

However, they were making up some of these higher costs through having interest rate swaps. In effect, where they were taking a hit on the income side of the equation and seeing higher costs, they were making up for the value of their swaps on a majority of their leverage.

RLTY Leverage Facts (Cohen & Steers)

Performance - Set For Recovery And Attractively Priced

Included in RLTY's portfolio aren't only REIT investments that can benefit from a lower interest rate environment, but the fund also carries a sleeve of preferred securities. As rates ease, those investments become more attractive in terms of what yields they offer and can be bid up by investors. It also adds a little bit more of a conservative tilt to the fund being higher up in the capital stack. That didn't treat the fund well when it was going through the higher rate environment and the banking crisis earlier in 2023, but it could be set to rebound moving forward .

On a YTD basis, we can see pretty clearly what was driving RLTY's price and NAV results throughout this year when compared to the 10-Year Treasury Rate. In particular, in the last few months, the fund was heavily influenced by the changes in this risk-free rate.

Despite what has already been a solid recovery from the lows, in my opinion, this fund still remains attractively priced. While it isn't necessarily the oldest fund, it is the fund with the largest discount when compared to its sister funds, Cohen & Steers Quality Income Realty Fund ( RQI ) and Cohen & Steers REIT and Preferred Income Fund ( RNP ).

Of course, history can have an influence on the valuation that investors are willing to assign for a position. Additionally, the other caveat is that RLTY is more of the 'middle' sister in that RNP carries around 50/50 between equity and preferred, and RQI is at around an 80/20 split, respectively. RLTY is at a roughly 67/33 split between the two asset types.

An absolute basis also isn't always that informative; often, we want to look at a fund's relative discount compared to its historical levels. With RLTY being new, we don't really have a great range to look back at just yet. That's why I believe that comparing it to its peers, in this case, makes a lot of sense to consider where a relative value would be appropriate for RLTY. The fund is also a term fund, but if successful could easily become a perpetual fund if the Board decides to pursue that course.

Distribution Juiced Up

Speaking of the fund's discount, that works in favor of a CEF investor in that it also means they receive a higher juiced-up distribution yield relative to what the fund has to earn. That is, more specifically, the fund's NAV distribution rate comes to 8.11% while investors receive a 9.38% rate based on buying at today's price.

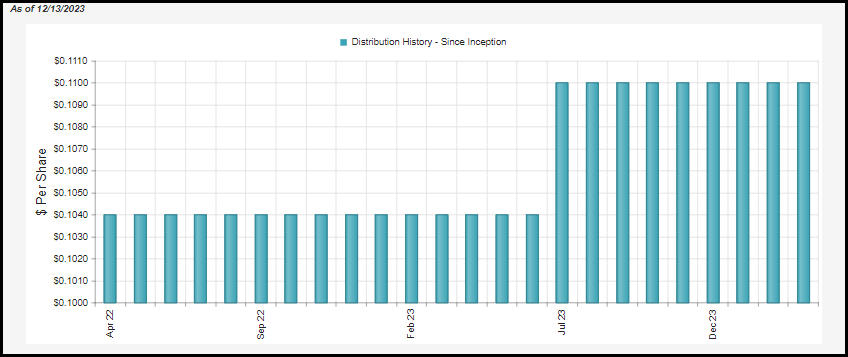

Additionally, they juiced up the rate they were paying out earlier this year when they bumped it up to an even $0.11 per month from the $0.1040 monthly rate.

{kind=link}

RLTY Distribution History (CEFConnect)

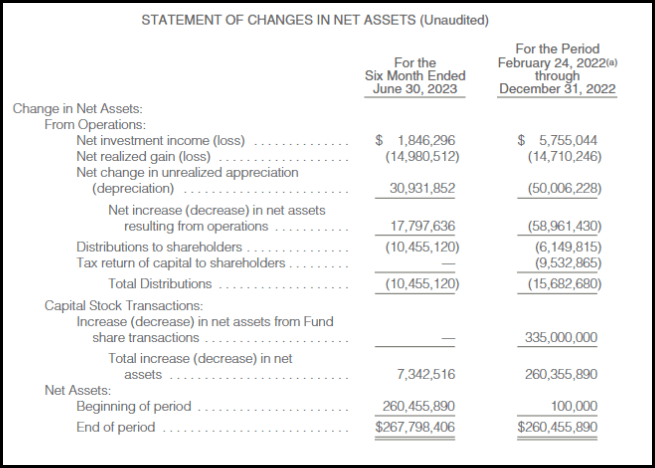

Given the funds raised in the distribution, I suspect that they are more than comfortable with leaving the payout where it is. That said, we can still give the latest numbers a look. During their latest semi-annual report, NII coverage came in at around 17.7%.

{kind=link}

RLTY Semi-Annual Report (Cohen & Steers)

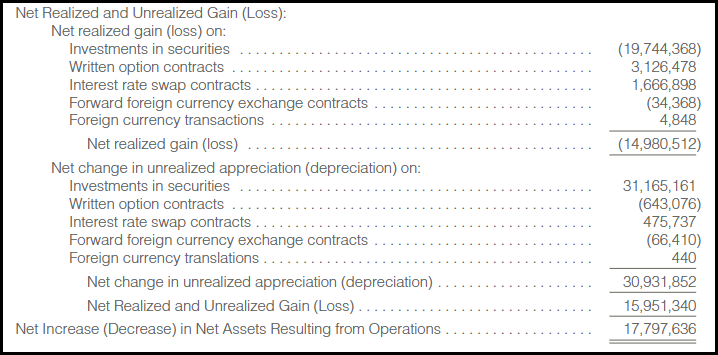

On a per-share basis, over the six-month period, it worked out to $0.11 - which is right at what they pay out in a single month. However, as we noted above, the interest rate swaps were kicking in and providing some capital gains.

{kind=link}

RLTY Realized/Unrealized Gains/Losses (Cohen & Steers)

Like the vast majority of CEFs that invest heavily in equities, they rely significantly on capital gains to fund their payouts. That's one of the main reasons their distribution rates are so high in the first place. On top of this, the Cohen & Steers REIT funds tend to invest in relatively lower-yielding investments and have more of a growth tilt.

Another common comment that comes up about RLTY is that it is paying return of capital distributions when its older peers aren't and are showing distribution tax classifications of capital gains instead. That is quite true.

C&S CEF Distribution Tax Classifications (Cohen & Steers (highlights from author))

They are estimating that a portion of 2023's distributions will be the same, including return of capital. However, in the end, the main argument is that whether the tax classification is return of capital or capital gains, assets are still coming out of the fund to pay investors during a time when the whole sector is facing pressure. Simply put, RQI and RNP have been around longer and have these embedded capital gains that they can fall back on.

RLTY, being a newer fund launching at a time when the REIT space got slammed by higher rates, just didn't have that advantage. In the end, the total NAV returns of the leveraged C&S CEF trio have been virtually the same.

YCharts

This is a good reminder that the tax classification isn't a performance metric but simply what it is, and that is a tax classification that is important for taxes and not whether a fund is performing poorly relative to another.

RLTY's Portfolio

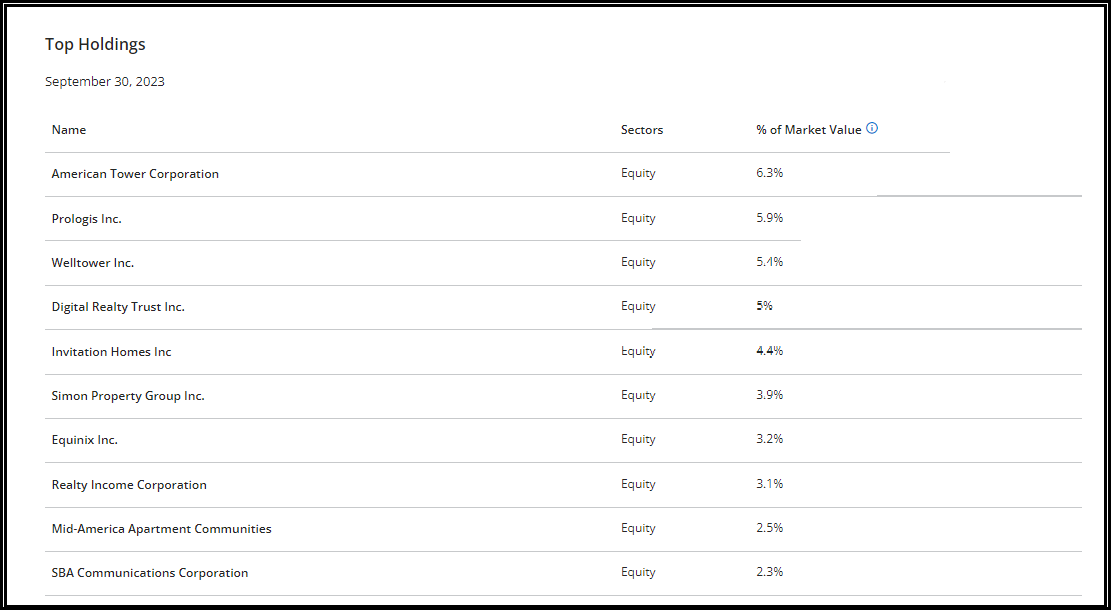

In looking at the fund's portfolio, we notice quite a bit of overlap with its older sister funds. That should be expected and would be why we see such similar performance despite the differences in terms of their weightings to equity/preferreds. RLTY lists 173 holdings, but the top ten make up a meaningful allocation of the fund overall at 42%. These are all equity positions, as noted in the breakdown as well, so relatively speaking, the preferred positions make up smaller positions.

The fund hasn't seen any drastic changes in the top holdings since our last update. SBA Communications ( SBAC ) made its way to the top ten, while Crown Castle ( CCI ) slipped outside of the top ten holdings. However, it still remains a position; it just became a bit smaller.

{kind=link}

RLTY Top Ten Holdings (Cohen & Steers)

Interestingly, as I was writing this, American Tower Corp ( AMT ) just announced a fairly sizeable bump in their quarterly dividend. It's interesting but perhaps not surprising, as this is a common feature of those positions. AMT often raises every quarter, at least historically, though they missed a bump higher earlier this year. That's why the 4.9% increase might not seem like a lot at first, but when they raise most every quarter, those increases really start to add up.

AMT was one of those positions that was deeply beaten down during October's peak risk-free rate, but it has been rebounding significantly. Even with this latest bump now to an annualized $6.80, we are looking at a yield of around 3.1% as of the latest closing price. Of course, as prices rise, the yield drops, like a bond assuming the equity position holds its payout steady. In this case, that meant that AMT's dividend yield was still lower than where it was just a short couple of months ago.

YCharts

Even with the latest increase in the share price rocketing higher, it isn't as if AMT is overly expensive based on its historical average. While the argument would be that the historical average is less helpful here because of the now higher rate environment, I think it still provides some good context overall. Also, if rates are set to go lower next year, then that historical valuation range becomes even more relevant.

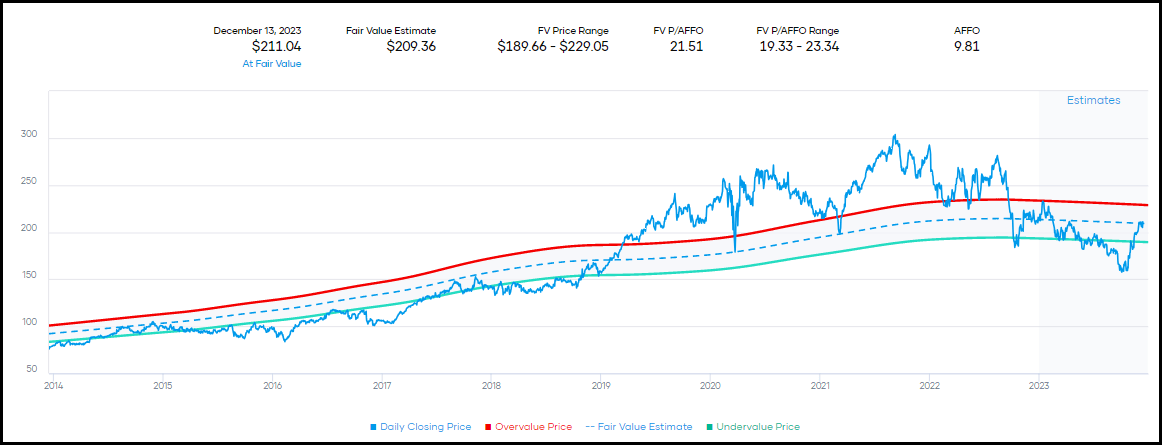

{kind=link}

AMT Fair Value Range (Portfolio Insight)

Conclusion

RLTY is poised to perform strongly as the REIT space continues on its recovery. With the Fed acknowledging that inflation is coming down, rate cuts are now nearer than originally forecasted. That can help propel the space higher, and with RLTY trading at a deep discount, that's an additional catalyst for upside. At the same time, the fund pays out a healthy distribution to investors while waiting for potential capital appreciation.

For further details see:

RLTY: REIT Exposure At A Discount With A Strong Distribution Yield