RMM - RMM: An Expensive Way To Access The Municipal Bond Sector

2023-11-08 17:41:16 ET

Summary

- RMM has seen a negative total return since my prior review years ago. Going forward, I'm reluctant to place a buy rating on it.

- The use of return of capital is extensive, suggesting a distribution cut will occur in 2024.

- Munis as a whole have merit given the historically high income streams (relative to their trading history). But RMM is not the best way to play it.

Main Thesis / Background

The purpose of this article is to evaluate the RiverNorth Managed Duration Municipal Income Fund ( RMM ) as an investment option at its current market price. This is a fund available to retail investors to access the municipal bond sector, with an objective "to provide current income exempt from regular U.S. federal income taxes with a secondary objective of total return".

As my followers know, I regularly cover the muni bond sector and often suggest it as a reasonable choice for high income investors. Despite that, it has been a while since I last covered RMM in particular. Roughly three years ago I advised readers to approach this fund carefully and I was absolutely right with that outlook in hindsight:

Fund Performance (Seeking Alpha)

With the recent Fed announcement last week and the broader volatility in the equity market, I figured it was timely to take another look at RMM as an option. Going in to 2024, I am more bullish on bonds as a whole - including munis - than I was when 2023 got underway. Yet, despite that outlook, I remain unconvinced that RMM is a wise choice for investors. I see a fund designed with above average expenses and lackluster performance. For this reason, among others, I would hesitate to recommend this product, and I will explain why in detail below.

Leverage, Expenses Are Red Flags

To begin this review I will highlight some of the major issues I have with this fund at this moment in time. There are two attributes here, but they are related so I will tackle them together. These are leverage and expenses, both of which clock-in at above-average levels - even for the land of muni CEFs.

Specifically, RMM uses roughly 40% leverage. This is on the high end. While other funds use similar amounts, I have seen other leveraged CEFs (in the muni space) range between 25% - 35% as well. So 40% is high:

RMM's Stats (RiverNorth)

What sets RMM apart to an even greater degree, however, is that this fund is partially a "fund of funds". When I say partially, this is because RMM does own individual muni issues. But in addition to those securities directly, RMM's strategy allows it to buy other CEFs on the open market. This is not inherently "bad", as management will use its judgement to find under-valued CEFs (often due to excessive discounts to NAV) in an attempt to amplify the fund's returns. But the net result is that RMM has 40% direct leverage and additional leverage through those funds it is buying.

That means the 40% figure is a bit of an understatement in how exposed investors really are to this space. The footnote within RMM's fact sheet regarding leverage reads as follows:

Leverage is based on the use of proceeds received from tender option bonds transactions, issuing Preferred Shares, or funds borrowed from banks or other institutions, expressed as a percentage of “Managed Assets"

Source: RiverNorth

As you can see, the fund's stated leverage percentage does not take in to account the leverage utilized by the underlying CEFs the fund owns. So this in reality amplifies the leverage (and therefore the risk) that investors face when purchasing this type of fund.

While this may not seem like a big deal, remember that a fundamental aspect of RMM's strategy is to buy leveraged CEFs and bundle them together. That does have merit and potential upsides, but I am emphasizing it because it is a big part of the broader portfolio. In fact, a rival CEF is actually one of RMM's top holdings right now:

RMM's Top Holdings (RiverNorth)

I use this exhibit why I am so cautious on this type of strategy. I am not saying this is fundamentally "bad" and that the management team is doing anything wrong. But what I am saying is that investors who buy this type of fund - as opposed to other muni CEFs - actually have more leverage and risk perhaps unknowingly. Is there the potential for more upside / higher returns? Absolutely - I am not suggesting otherwise. But when we are starting with 40% leverage ranges already, I personally don't see the need to amplify that number even more on the chance of additional returns.

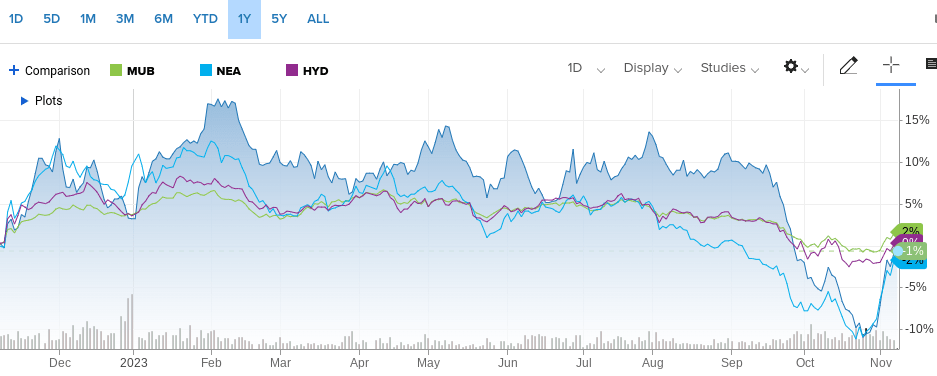

For support of my opinion, let us look at 1-year returns. When I compare RMM's performance against the Nuveen AMT-Free Quality Muni Fund ( NEA ) (the CEF listed above as a top holding) and two passive muni ETFs: the iShares National Muni Bond ETF ( MUB ) and the VanEck High Yield Muni ETF ( HYD ), I don't see a lot to get excited about:

{kind=link}

As you can see, market price returns are quite similar. Yes, RMM would have a higher yield than both MUB and HYD, but its yield compared to NEA would be similar. This suggests to me that taking on the extra risk isn't really paying dividends, so to speak, for retail investors.

This begs the question - why would that be the case? While we cannot always justify market moves, especially over short time periods, expenses have got to play a part of this role. RMM - due to its strategy and leverage - charges quite a bit for the privilege of owning it:

Expenses and Investment Income (RiverNorth)

This is quite telling. Management is getting a high level of fees from this fund while investors are not reaping many benefits (as noted in the negative return since my last review three years ago). I can't see how one could get overly excited about owning this fund when a substantial portion of the investment income is siphoned off via fees and expenses. This is a major red flag for me - and one I don't see changing any time soon. This completely supports my caution.

Income Is High - But Sustainable?

In fairness, a lot of investors do not invest in muni CEFs, including RMM, with a primary focus on total return. While I would emphasize its importance, many investors are solely focused on yield. If so, RMM may look attractive on the surface given its high payout ratio at the moment:

RMM's Distribution Schedule (Seeking Alpha)

{kind=link}

Looks good, right?

Well, maybe in the short-term. But in the long-term I have some major concerns. I would urge my followers not to be blinded by the high yield on the surface. It hasn't worked out for RMM holders in the past, and it is unlikely to now.

Yes, a double-digit yield after tax adjustments would certainly draw in buyers. But we have to consider its sustainability . The simple truth is that this just isn't sustainable in my opinion. To see why, let's look at the most recent Section 19a disclosure for the fund. It shows the vast majority of the distribution is being paid out by return of capital:

{kind=link}

This is a stunning metric and is much worse than where it sat back in 2020 in my prior article. The fund is pumping out a high yield, but not through investment income. I am surprised they have not had to cut the distribution yet with this metric in hand, but I imagine that will be coming in early 2024. With that as a headwind, I cannot get behind positions in this fund.

But The Discount Is Attractive, Right?

This article has had a fairly bearish tone and I stand by that. But it isn't meant to suggest RMM is the worst of the worst out there. I don't love it as an investment at these levels, but to present a balanced take we have to consider some of the positives. One in particular is the discount to NAV. At over 8%, this should limit downside risk going forward - even if bad news like a distribution cut occurs:

Current Data (RMM) (RiverNorth)

The fact is this is a reasonably positive attribute to consider. I love CEFs - especially quality CEFs - at discount prices. RMM offers the discount, but I'm not completely sold on the "quality" of the strategy it employs. So that presents a balancing act.

Further, this isn't really "cheap" on a historical basis. During my last review of RMM the fund sat with a discount in excess of 10%. So the discount has actually narrowed over time, despite posting a negative total return. This isn't meant to be alarmist, but it reinforces that a discount to NAV does not automatically translate to positive future returns. It hasn't worked out that way for RMM in the last few years, so this clouds how attractive the discount is right now.

Munis Are Offering Historically High Income

I will now shift to a macro-outlook on why readers should be considering the muni sector at this time. This could extend to RMM for some, but is really relevant for any quality muni security (or fund that holds them).

The primary metric to focus on (in my opinion) is the current yield. This is a stat that has reclaimed a level not seen for roughly 15 years - with the broader index offering 4.5% and climbing:

Yield for Muni Index (Bloomberg)

{kind=link}

To be fair, investors can earn more elsewhere. This is especially true for those in lower income tax brackets. But for those in high income brackets (35-50% range), this yield is very competitive given the quality of the IG-rated issues. Munis rarely default and, when they do, they tend to be concentrated in below-IG issues. So CEFs with IG-rated holdings look attractive historically.

The takeaway for me is that now is a good time to lock-in yields across the muni sector. But to tie this back to RMM, yields aren't high enough to make this particular fund the right play. Remember what I said about expenses - running in around 4.5%. Well, look at the muni yield curve. It is too similar for my liking. RMM management is borrowing and charging a rate similar to what it will earn in yield on the muni curve - so how are retail investors going to come out ahead? It will be difficult to do so, and that is not the type of backdrop I want for any investment.

Equities Look Expensive, Making Hedges Relevant

My final thought is another reason why considering the muni market at the time being could be relevant. Simply put, this sector remains an effective long-term hedge against equity volatility and I do expect that to continue. At time of writing, US stocks (large-cap) are expensive. This is true both in isolation and compared to other developed markets, as shown below:

Forward P/E Ratio (By Region) (FactSet)

This doesn't mean flee stocks. Far from it. The reality is that US stocks often out-perform and generally have higher P/E ratios than Europe and/or Asian indices. So this in and of itself is not a "sell" signal. But it does show that forward returns may be challenging to come by starting with today as Day 1 because stocks are not historically cheap or a real bargain. That suggests heightened chances of volatility ahead, and munis are one way to ride out the storm in the hope I can get in to equities at better prices in the months to come.

Bottom Line

RMM has been off my radar for a while and I'm better off for it. While the fund does have some positive attributes, such as a high income stream and a discount to NAV, there are headwinds that make me reluctant to take a chance on it.

Leverage costs and other expenses are sky-high, making total returns tough to come by. Furthermore, the amount of return of capital being utilized to pay the distribution is a huge red flag. If a cut occurs, it is very likely the market price will take a hit. Add this up, and RMM remains on hold for me, and I'd caution my followers to approach it very selectively.

For further details see:

RMM: An Expensive Way To Access The Municipal Bond Sector