OPINL - RMR Brings Diversified Healthcare And Office Properties Together

2023-04-11 12:29:33 ET

Summary

- Diversified Healthcare Trust announced a definitive merger agreement with Office Properties Income Trust.

- The dividend goes up for Diversified Healthcare Trust, and Office Properties Income Trust takes a huge haircut.

- We examine the setup and tell you things you need to know to play this.

When we last covered Office Properties Income Trust ( OPI ) we raised our risk levels and told investors to follow metrics that matter. Specifically we warned:

The CAD payout ratio could be nearing 100% by the end of 2023. We think the risks have gone up and we have to give it one bump up (from low to moderate) on our Kenny Loggins Scale

Trapping Value

A moderate rating signifies a 20%-33% probability of a dividend cut within the next 12 months. We will stress here that the outlook pertains only to the next 12 months. If we were forecasting three years out, we would give OPI a less than 1% chance of sustaining the current dividend that far out.

Source: Don't Get Complacent On That 12.5% Yield

Well it has not been three years, heck it has not been three months, and OPI has cut its distribution. The stock is down almost 50% from that article.

Seeking Alpha

Let's look at what's happening here and how this plays into the thesis.

The Urge To Merge

Diversified Healthcare Trust ( DHC ) today announced that it has entered into a definitive merger agreement with OPI pursuant to which OPI will acquire all of the outstanding common shares of DHC in an all-share transaction.

Pursuant to the terms of the merger agreement, DHC shareholders will receive 0.147 shares of OPI for each common share of DHC based on a fixed exchange ratio, which represents an implied value of $1.70 per DHC common share and a 20% premium to the average closing price of DHC common shares for the 30 trading days ended on April 10, 2023, resulting in DHC shareholders owning approximately 42% of the combined company, and OPI shareholders owning approximately 58% of the combined company.

Upon the closing of the transaction, DHC shareholders will benefit from the combined company’s expected cash distribution of $0.25 per share per quarter, or $1.00 per year, which is a 267% increase on a pro rata basis from DHC’s current distribution level of $0.01 per share per quarter, or $0.04 per year.

This is definitely a first for us. OPI is radically cutting its distribution from $2.20 annually to $1.00 annually per share. But the press release focuses on how this delivers a dividend bump to DHC. Guess the marketing unit at The RMR Group Inc. ( RMR ), which manages both these REITs, certainly put in the overtime hours. Let's look at why the dividend was cut so drastically for OPI and where do we go from here.

The Rationale For DHC

The only thing OPI and DHC have in common is that they are both REITs that are managed by RMR. Both REITs have done poorly over longer timeframes, though OPI has more of an excuse than DHC, considering what's happening to all office REITs.

Merging these two together works to keep DHC out of troubled waters.

{kind=link}

DHC-OPI Combined Presentation

DHC had been granted relief on this, but the clock was ticking.

In October, we repaid a mortgage note on a life science property for approximately $10 million. And as Jennifer mentioned, in February, we announced an amendment to our credit facility. This amendment provides us with fixed charge coverage ratio covenant relief into 2024, while our SHOP segment recovers and allows us flexibility to continue investing in our portfolio to accelerate that recovery. The amendment also reduced the minimum liquidity requirement from $200 million to $100 million. In exchange, we have paid down the facility to $450 million, have agreed to a 40 basis point increase in the interest rate and no longer have the ability to reborrow.

Source: DHC Q4-2022 Conference Call Transcript

With rates headed higher quarter after quarter, DHC was getting more and more squeezed. The company finally bought the "higher for longer" narrative and that meant that it had to address this debt load quickly.

The Rationale For OPI

The combined entity will have a mishmash of assets across many different segments.

{kind=link}

DHC-OPI Combined Presentation

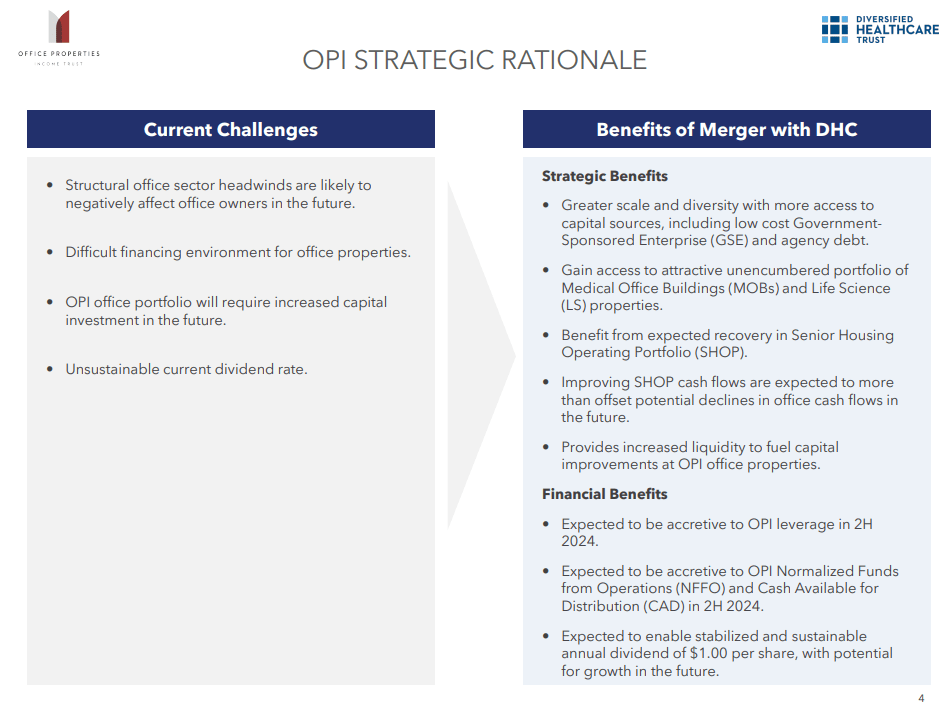

That said, we are hard pressed to find a reasonable positive here for OPI to create this large entity. Presumably, managing this portfolio will not be an issue as RMR already manages both sides. But we have two sets of assets with unique challenges here. Based on what we have seen by both these, we don't think they are equipped to deal with either one. According to the presentation, there are apparent benefits to this merger.

{kind=link}

DHC-OPI Combined Presentation

We don't see any of those listed as "benefits" as we think the only focal point will be try and survive over the next two years.

Can They Survive, Even If They Do Not Thrive?

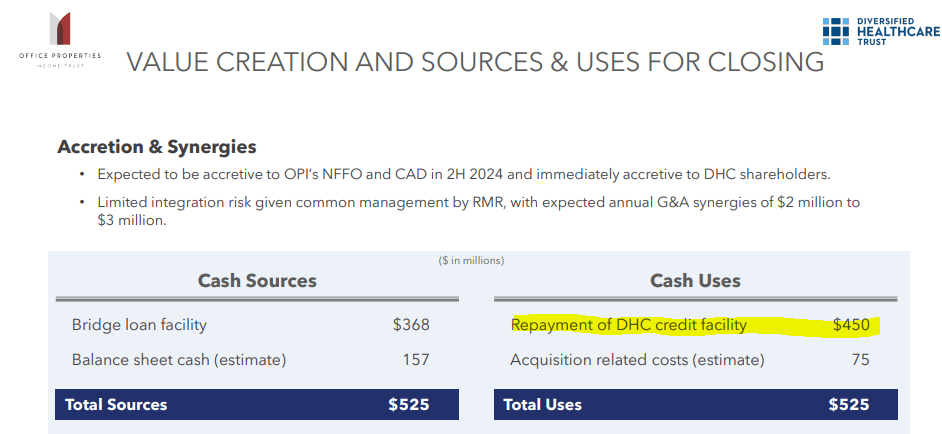

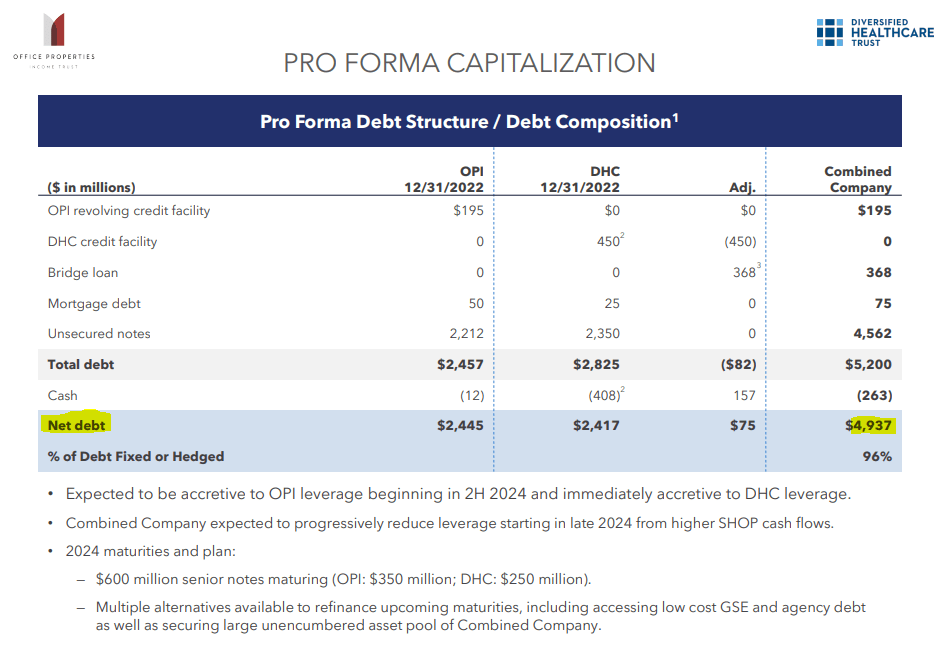

The combined entity will have almost $5.0 billion in net debt.

{kind=link}

DHC-OPI Combined Presentation

$5.0 billion may not sound like a lot, but investors should note that the combined market capitalization of our dynamic duo is under $800 million.

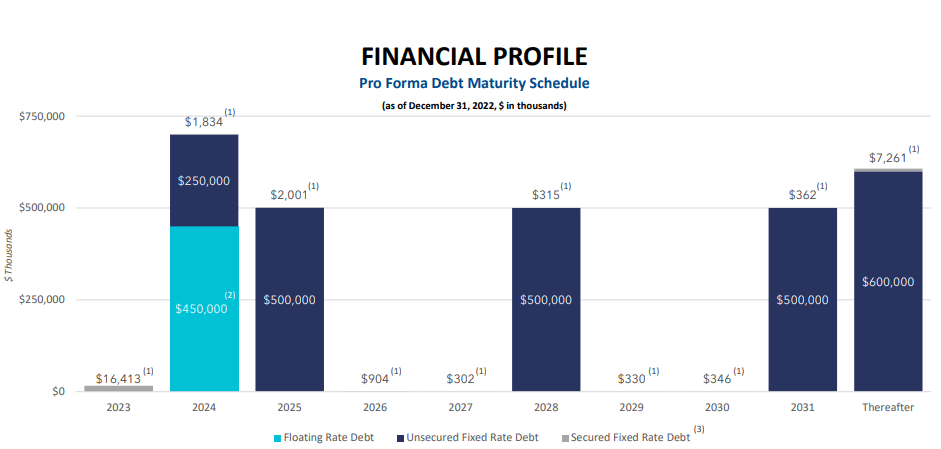

OPI had $1.2 billion due in the next 2.5 years.

OPI Presentation

DHC has another $1.2 billion of its own.

{kind=link}

DHC Presentation

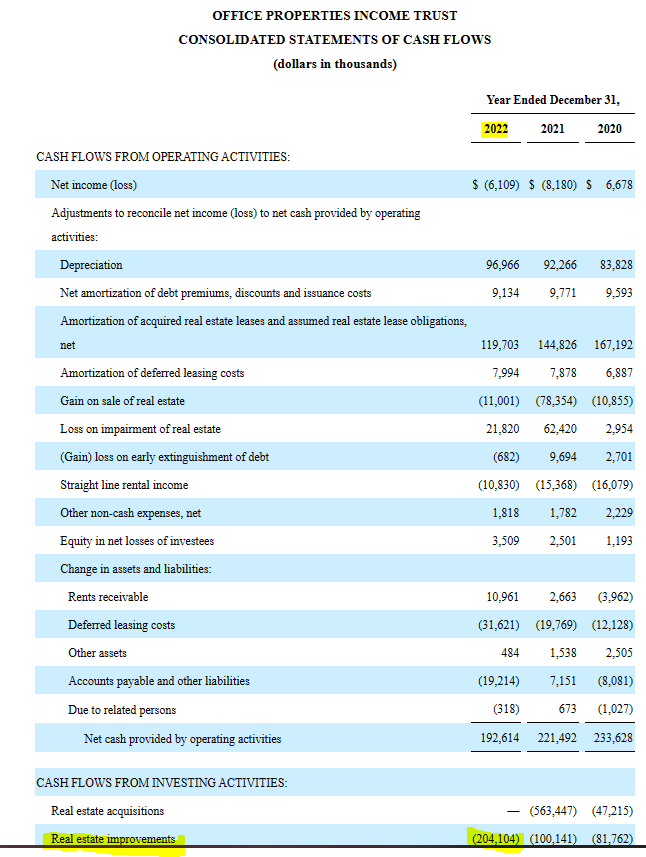

That debt load has to be addressed rather soon. The combined entity will produce close to $550 million in adjusted EBITDA. We're basing this on Q4 numbers from both side and reducing it slightly to account for continued office segment deterioration. So that puts our debt to adjusted EBITDA near 9.0X. On that $550 million, $300 million will be interest expense. So before we get to dividends/distributions, we have just $250 million left. The combined entities spent about $500 million in capex in 2022 . $200 million was spent by OPI.

{kind=link}

OPI 10-K

DHC splurged a bit more.

DHC 10-K

The bond market is acutely aware of this as well and the entire debt maturity curve for OPI is pricing in an average of 14% yield to maturities.

{kind=link}

Interactive Brokers April 11, 2023

So the challenges will be intense and unless the outlook for office properties improves significantly and rather rapidly, we're looking at a possible restructuring within three years.

Verdict

OK, so investors must be getting the picture here. We will need some massive real estate liquidations to get through the next few years. The combined gross assets (non depreciated book value) are substantial and worth over $12 billion. Fair value is extremely hard to ascertain as single tenant office properties are pretty binary. Either you get a great lease at the end of the term or you sell it for the value of the land. DHC's properties arguably have better staying power but ideally we should have seen far more deleveraging during the last two years. If those properties are valuable, where were the asset sales to realign the portfolio? After all, DHC's debt to gross assets ratio was extremely low. For whatever reason, those sales did not occur when things were relatively good in the capital markets. So having confidence in this asset sale going into a recession is a very tall ask. If we had to play it, we would look at the front end of the maturing debt structure. The Feb 2025 bonds offer 14% yield to maturity and possibly that is something that can work out. There are also some arbitrage opportunities in the capital structure. The DHC March 2031's are trading with a ridiculously low 8.8% yield to maturity.

{kind=link}

Interactive Brokers April 11, 2023

We would consider swapping that for OPI's June 2026 (shown above) at a 16% yield to maturity. The same logic can be extended to the baby bonds of both companies. Office Properties Income Trust 6.375% NT 50 ( OPINL ) for example matures in 2050. You can get better yield to maturities earlier in the structure and alongside that, a higher possibility of actually getting that return. For our part, we are looking Blackstone Mortgage Trust, Inc's. ( BXMT ) senior notes as possibly the only way we would play office today.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

RMR Brings Diversified Healthcare And Office Properties Together