IBKR - Robinhood: Skewed Risk/Reward To The Downside

2023-04-19 07:45:00 ET

Summary

- Robinhood has experienced a slowdown in retail trading activity in the last sixteen months after a period of rapid growth in 2021.

- Robinhood's customer base, consisting of younger and lower-income individuals, is more vulnerable to the effects of inflation and a possible recession.

- The company faces the greatest potential headline and regulatory risk compared to other brokers due to its reliance on PFOF.

- The challenging macro environment may prolong the process of successfully cross-selling new products to Robinhood's current customer base.

Thesis

Robinhood Markets, Inc. ( HOOD ) has been adversely affected by a slowdown in retail trading activity over the past sixteen months after a period of rapid growth in 2021. Robinhood's profitability could be improved by rising rates and cost-cutting measures, in my view. However, the company's younger and lower-income customer base is expected to face the greatest impact from ongoing inflation and the possibility of a recession. I also see the greatest potential headline and regulatory risk for Robinhood vs. the other brokers, given the reliance on order flow revenues, among other factors. Moreover, HOOD's customer base is positioned to be disproportionately impacted by a challenging macro environment, and I believe it would become difficult for the company to cross-sell new products.

Net interest income continues to be a tailwind for brokers

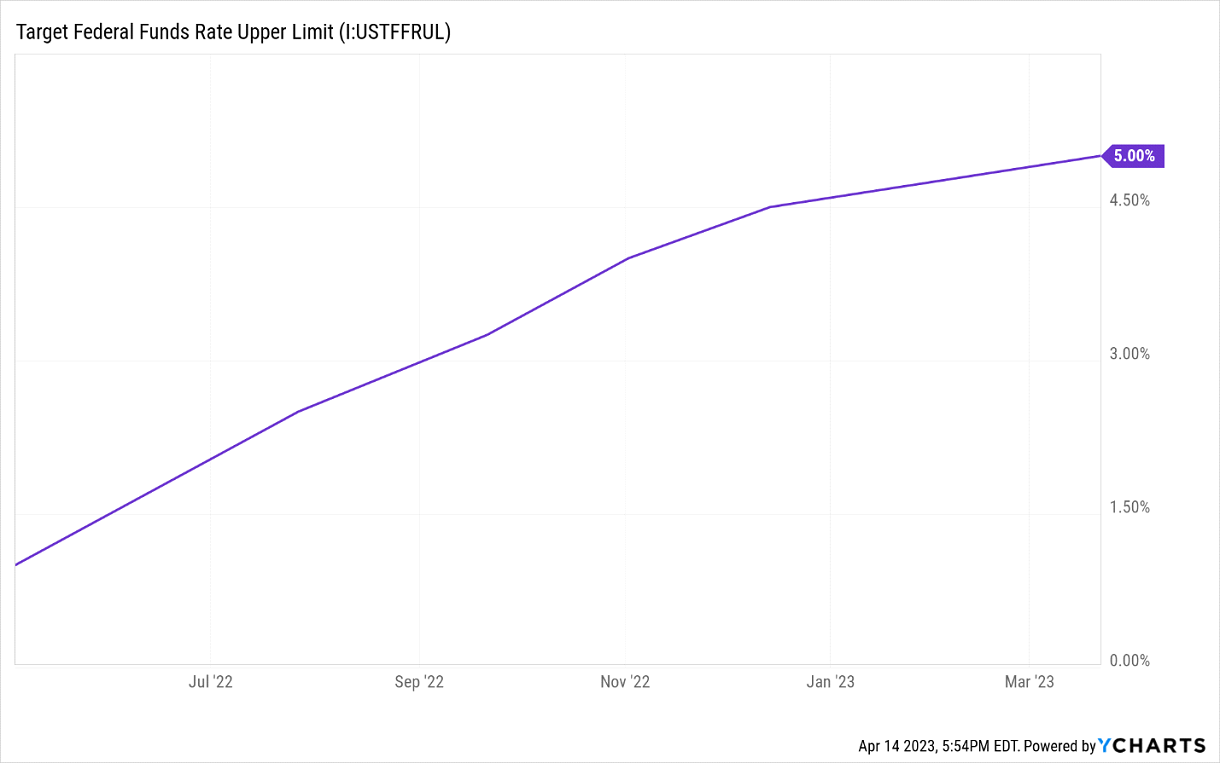

The Federal Reserve has raised the upper bound target rate to 5%, causing rates in the US to continue to rise. In Q4, the average effective Fed Funds Rate was 3.65%, which is almost 150 basis points higher than the Q3 average of 2.18%. The fed funds futures curve predicts that rates will peak near 5.25% , which is expected to support interest income for all brokers through at least the first half of 2023. Higher rates have boosted topline interest income for brokers, but there has been a slight offset due to declines in margin balances across monthly metrics. This trend may continue as the Fed funds rate keeps climbing. Robinhood has seen an increase in customer deposits due to the Gold cash sweep program , which offers a high-interest rate of 4.4% for deposits in Gold sweep accounts and 1.5% for non-Gold sweep accounts.

{kind=link}

A Challenging Macro Environment & Declining Engagement to Impact HOOD

Robinhood's monthly active users (MAUs) and overall trading activity peaked in 2021 during market volatility and have been declining ever since across all product categories. Per-MAU activity peaked in Q4 2020, Q1 2021, and Q2 2021 for options, equities, and crypto, respectively. Given Robinhood's customer demographic, which consists largely of younger and lower-income individuals, it may take some time for activity to resume. Additionally, this demographic is more likely to be negatively impacted by high levels of inflation and a potential recession compared to the customer bases of competitors. Management has noted that younger customers facing a recession for the first time, coupled with higher inflation, higher rates, a bear market in equities, and a "crypto winter," will have less money to save and invest.

To reverse the trend of falling MAUs and trading activity, Robinhood needs more constructive markets. A worsening of economic conditions could lead to even lower figures as customers divert funds to essentials instead of discretionary investment. This is particularly true for Robinhood's customer mix, although a significant improvement in market sentiment could potentially lead to a swift increase in trading volume. The decline in engagement since late 2021 has reversed most of the gains made in 2020-21, with Q4 2022 MAUs of 11.4 million being 34% lower than Q4 2021 MAUs of 17.3 million .

Competition remains intense in the US

Robinhood faces competition from a wide range of players, including traditional brokers, fintechs, and crypto-native companies. While there are differences in the user bases of Robinhood and traditional brokers like The Charles Schwab Corporation ( SCHW ) and Interactive Brokers Group, Inc. ( IBKR ), Schwab has indicated that over 50% of its net new assets in a recent quarter came from customers under 40 years old. The transfer of accounts ((TOA)) ratio, which measures assets rather than total accounts, suggests that the average account size of a fintech customer moving assets to Schwab is significantly larger than that of a customer leaving Schwab for a fintech. Interactive Brokers has also noted that accounts coming from Robinhood have an average size of approximately $75k, which is much larger than Robinhood's average account size of $3-4k. This suggests that Robinhood may be losing larger accounts to traditional brokers.

Financial Times

Several fintech competitors are expanding their stock trading businesses. FTX launched a stock trading offering in beta earlier this year and expanded it in July. FTX's combined offering of stocks and crypto may appeal to a similar demographic as Robinhood. Cash App has also expanded its equities offering and launched a Round Ups feature in June 2022, similar to Robinhood.

Robinhood Has Bigger Risk from PFOF Regulation vs. Peers

Robinhood's transaction-based revenue decline highlights its risk from turbulent retail-trading activity, with crypto adding volatility. Market sentiment drives activity, and reliance on such revenue means it's suffering more than peers from the pullback and would from any SEC-proposed changes to the existing payment-for-order flow (PFOF) ecosystem. Proposed market-structure changes could hurt online retail brokers via cuts to payment for order flow (PFOF), but the effects would be felt unevenly due to the business mix.

Robinhood faces the greatest risk due to its business model. Any changes to the options-market structure would be much more punitive. More broadly, if a worst-case scenario occurred, the fallout could prompt questions about widespread commission-free trading. Though I view a return to equity commissions as unlikely, companies that are reliant on PFOF could be forced to tweak their business models over time, while those that are more insulated might benefit via customer acquisition.

Valuation

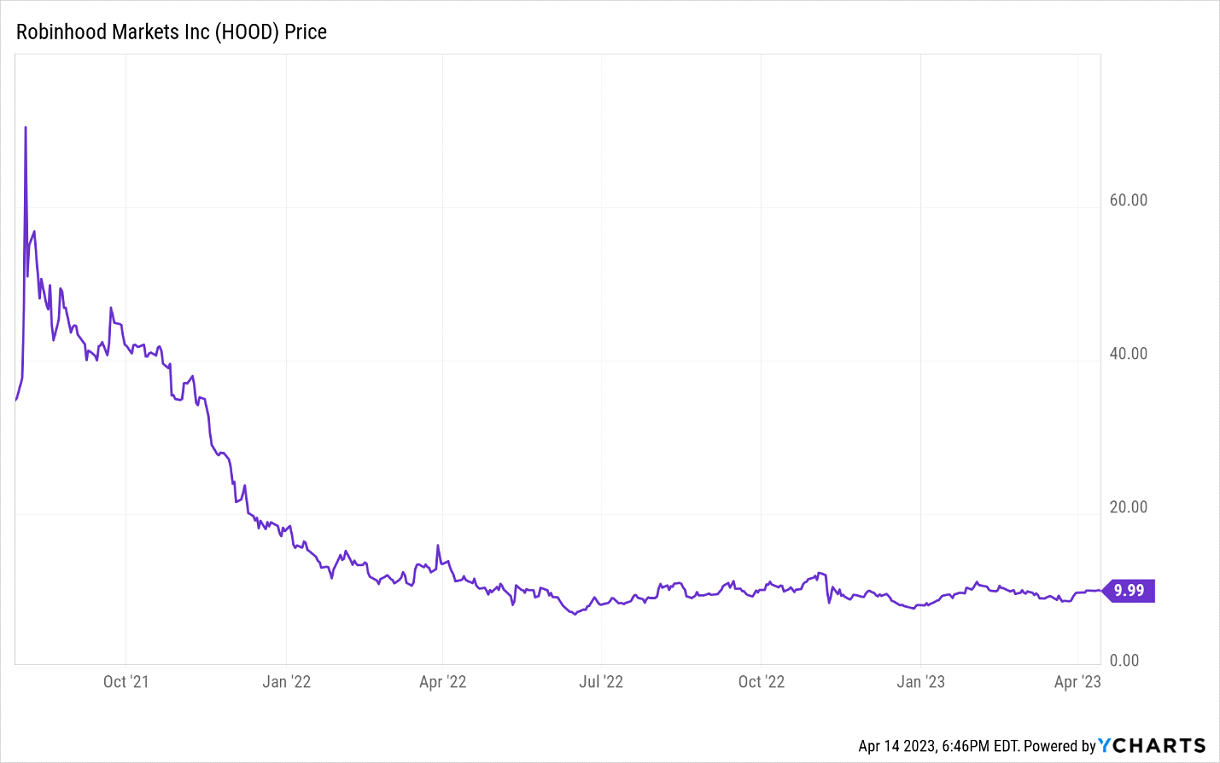

Robinhood's stock is 74% below its July 2021 IPO price. The significant underperformance stems from the sharp downward revision in trading expectations that's come as markets turned, curtailing retail investor enthusiasm, I believe. Additionally, the impending threat and ultimate proposals from the SEC regarding changes in equity-market structure have been more punitive to Robinhood's shares.

Robinhood's valuation paradigm poses a challenge for investors due to changing fintech narratives and valuation methodologies over the years, which differ from traditional brokers that tend to trade on P/E multiples. Additionally, the company's current profitability and longer-term growth expectations add to the challenge. Robinhood's exposure to declining retail-trading trends may continue to impact sentiment, especially with SEC proposals on payment for order flow (PFOF) raising concerns about top-line prospects.

I currently maintain a sell rating on the stock without a price target as I believe that HOOD's customer base will continue to be disproportionately impacted by a challenging macro environment and that it will take more time than expected to successfully cross-sell new products to the current customer base.

HOOD stock price movement YTD (Ycharts)

{kind=link}

Final Thoughts

HOOD has been facing a decline in retail trading activity after a period of rapid growth in 2021. Although the company may achieve profitability in the near future through cost-cutting and rising rates, Robinhood's customer base, comprising young and low-income individuals, may be adversely affected by ongoing inflation and a possible recession. Robinhood also faces potential regulatory and headline risks due to its reliance on payment for order flow revenues. While there may be improvements in revenue growth and profitability, the challenging macro environment may disproportionately affect Robinhood's customer base, making it harder to cross-sell new products. I currently maintain a sell rating on the stock until the risks start to subside.

For further details see:

Robinhood: Skewed Risk/Reward To The Downside