AOMR - Rocket Companies: In 2023 Mortgage Stocks May Be A Contrarian Buy

Summary

- Mortgage Origination is a cyclical business, dependent on stable interest rates.

- In 2022, the Federal Reserve hiked rates at a pace never seen before.

- Many mortgage companies are hovering near 52-week lows.

- Companies making NonQM mortgages during 2022 lost millions due to M2M accounting.

- In 2023, mortgage stocks including Rocket Companies, Inc. may rebound due to a more stable rate path.

In 2023, investors should consider mortgage originators, especially after seeing these companies' stock prices plummet in 2022. Companies like Rocket Companies, Inc. ( RKT ), loanDepot, Inc. ( LDI ), Finance Of America Companies Inc. ( FOA ), Angel Oak Mortgage, Inc. ( AOMR ), and Impac Mortgage Holdings, Inc. ( IMH ) are all trading at the bottom of their 52-week range. Many of these companies are also trading significantly below their recent IPO price.

As a whole, the mortgage origination sector is somewhat counter-cyclical in nature due to its unique position in the broader economy. During times of economic turmoil, when most sectors of the economy falter and there is a general lack of confidence in the equity markets, the mortgage origination sector is often the first to see a glimmer of hope. This is because the sector is highly sensitive to swings in interest rates. For better or worse, this creates tremendous cycles.

As we have seen in the past year, this sector has taken a large beating as rates have moved up at an unprecedented speed. Here’s a chart showing the speed and path of rate hikes in comparison to prior cycles. The pace of this rate hike cycle is unmatched by any other period.

Schwab

The resulting spike in rates has caused an adverse reaction in housing and mortgage finance. Not only has the refinance business nearly disappeared, but with mortgage rates topping 7%, purchase mortgage origination has hit multi-decade lows. This is reflected in these companies' earnings releases and stock prices.

yCharts

When the overall economy is weak, the mortgage origination sector takes on an increased role in providing liquidity and stability to the housing market mostly because the Federal Reserve and other central banks will often increase the money supply, bringing down interest rates. This increases mortgage activity due to lower rates and helps to stabilize the housing market, allowing existing homeowners to remain in their homes or upgrade to a larger home, refinance to a lower rate, or purchase a new home with cheaper financing.

In 2023, the rapid increase of interest rates may finally come to a halt. At that time, mortgage stocks may be positioned for a recovery. If a recession hits, like some economists have predicted, then rates may actually pull back slightly in 2023 (or 2024). In that case, the downward cycle in mortgage originations may actually reverse. This could be the biggest contrarian investor call of the year. Here are some stocks you may want to watch.

Rocket Mortgage

Rocket Mortgage is an online lender that has revolutionized the mortgage process by operating a massive call center refinance operation. It was one of the first lenders to offer a completely online mortgage application process, allowing many consumers to apply and get pre-approved for a mortgage in just a few minutes. Rocket also boasts a unique range of competitive advantages that set it apart from some other lenders.

Rocket prides itself on a simplified online application process that makes it easy for customers to apply for a mortgage loan. They also offer competitive rates and fees due to economies of scale that make it easy for customers to save money on their mortgage. Rocket Mortgage also offers 24/7 customer service to answer any questions customers may have and a nationwide marketing plan.

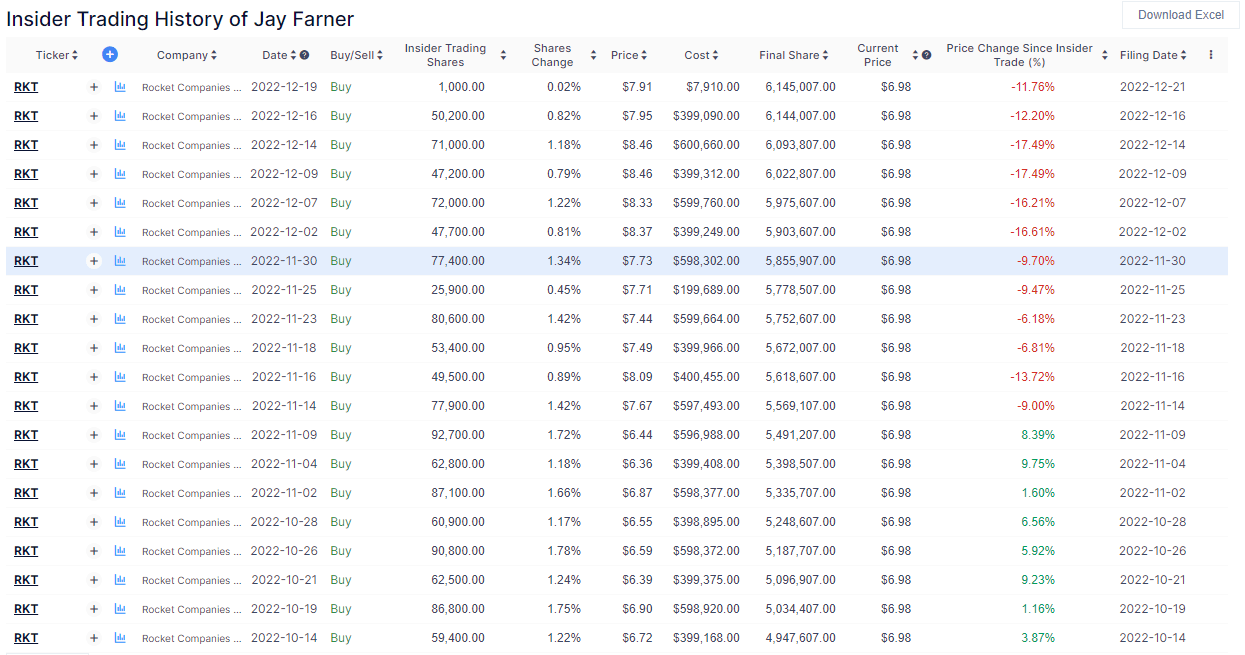

One of the interesting things about this year for Rocket has been that the founder, Jay Farner, announced a plan in early 2022 to personally buy $36 million in Rocket stock. He's done just that , as you can see below.

{kind=link}

Because Farner made a plan to purchase a certain amount of stock, with "no authority, influence or control over any purchase of the company's common shares," you can't really read into the price at which he has been buying. This is a stock purchase plan on autopilot. The brilliant part of this plan is that it allows Farner to engage in a systematic dollar-cost-averaging of his purchases over time. Farner has increased his position in the company from 1.7 million shares in March to 6.1 million shares today. For the average investor, it's a sign of confidence that the future will be brighter than 2022.

loanDepot

loanDepot is a mortgage lender that was founded in 2010 and is now one of the largest in the country. It has seen tremendous growth over the last several years and is now one of the most recognizable names in the mortgage finance industry. loanDepot's success can be attributed to its focus on customer service and reliance on technology. The company has invested heavily in customer service, which has enabled it to provide fast and accurate information to customers. It has also invested in technology, which has enabled it to streamline the loan process and provide customers access to their loan documents and other information online.

loanDepot has not been immune to the market weakness caused by rapid interest rate increases. They have launched a strategic path that they call Vision 2025, and this was discussed on a recent conference call (emphasis added):

Vision 2025 which we formerly launched in July has four pillars. Pillar number one focuses on transforming our originations business to drive purchase money transactions with an expanded emphasis on purpose driven lending. Pillar two calls for aggressively rightsizing our cost structure in line with current and anticipated market conditions and internally sets targets to achieve first quartile opting performance. Pillar three covers investing in profitable growth generating initiatives, which for this year focuses on launching our innovative digital HELOC solution . And finally, pillar four relates to optimizing our organizational structure.

In other words, loanDepot is shrinking their employee base, adding a home equity loan product, and trying to focus away from refinance activity. This outlook is consistent with a view that interest rates will remain elevated due to inflation.

New York Fed

Targeting the Home Equity Line of Credit market makes sense at this time. Borrowers seeking additional financing options for debt consolidation and other needs have previously had easy access to conventional refinance loans in the past decade. Today, with mortgage rates over 7%, it probably makes sense to keep the existing mortgage. HELOCs provide a flexible lending option that largely fell out of favor during the easy money, low rate period.

Impac Mortgage

Impac Mortgage Holdings has had its fair share of challenges the past few years. For instance, mortgage originations in 2022 pretty much dried up completely at the same time that the company was wrapping up a balance sheet restructuring that took years to negotiate. Timing of these events has taken a toll on the stock price which has fallen to the penny stock range.

According to George Mangiaracina (emphasis added):

“The company adopted a defensive risk-off posture in the fourth quarter of 2021 and remains measured and disciplined in its origination and capital markets activities. Layered risks cannot be effectively hedged in times of acute market dislocation and we have no visibility as to when such dislocation will abate and return the industry to normalized volumes and margins.”

At this time, it seems like Impac has basically ceased operations, but if the above statement is true, we all may actually look back on this period and say that the decision to take a "risk-off" approach was actually brilliant, given the low margins and risks associated with holding mortgages on your balance sheet during rapid interest rate hikes.

Going forward, a large value driver for Impac is the large deferred tax asset. At $257 million, the DTA is the largest asset that the company owns and it is completely unrecorded on the balance sheet. If the company reverses the valuation allowance on the DTA, this could add up to $7.52 per share in book value and EPS.

Impac IR

Impac’s Non-QM business is the area to watch in 2023. The mortgage market was difficult in 2022 due to rising rates, but the FOMC may actually pause rate hikes in early 2023 to avoid a recession. If that happens, we could find that the economy can support these higher rates. Further, homebuyers may be forced to buy homes with more expensive mortgages. In some cases, they may no longer qualify for the qualified mortgages and may have been pushed “outside the box.” Enter Impac and their offering of Non-QM products.

A few weeks ago, I wrote about the overall conditions of mortgage credit availability in my substack.

Today, housing and mortgage credit are in a really safe and sound place. In fact, the reigns of mortgage credit could be loosened. Mortgage credit availability never returned to a fraction of the levels seen before the last crisis.

(MBA)

Because credit availability in the mortgage market never really bounced back, certain product offerings like home equity loans and non-qualified mortgages have lots of room to grow. This is especially true when you consider that higher rates make the expansion of mortgage credit more profitable. It's much easier and more profitable to package a group of pristine NonQM mortgages into a AAA mortgage security when you are one of the few firms offering that product."

Firms like Impac could possibly serve a niche in 2023, if interest rates remain elevated. Impac provides borrowers with a few more options as they currently have five NonQM lending programs.

For self-employed borrowers, Impac offers a Bank Statement mortgage program . Mortgage borrowers under this program qualify with 12 months of bank statements instead of a W2. The loan to value ratios on these mortgages are currently capped at 60% and at 80% for cash-out refinance loans. Loans can be made up to $3 million in total value, and the minimum FICO score is above 600. They also have an interest only option with a minimum FICO of 700.

Another option for self-employed buyers or contractors is Impac’s Income 1099 program . These mortgage borrowers qualify with pay statements and a 1099 form documenting one year of non-payroll income. This program is similar to the bank statement program, but based on the borrower's 1099 reported income.

They also offer investor mortgage loans for “ positive cash flow properties. ” Borrowers in this program can utilize up to 75% loan-to-value for purchase or refinance loans on their investment properties. There is an interest-only option available and this program can be utilized for an unlimited number of properties.

Occasionally, a borrower may not be employed in a traditional sense, but has high liquid assets. The Asset Qualification program allows these mortgage borrowers, with FICOs above 660 to purchase or refinance loans up to $3 million and 90% loan-to-value, as long as they have verified liquid net assets.

Lastly, Impac offers an Agency Plus option , which closely mimics programs offered by Fannie, Freddie, and Ginnie. Under this lending program, borrowers just outside of qualified mortgage guidelines have an option to take out mortgage loans up to $3 million with interest-only as an option and debt-to-income up to 55%.

You may be asking why these programs didn't move the needle for Impac in 2022. The answer is that Impac pulled back out of the market strategically due to rising interest rates. Another Non-QM lender, Angel Oak, took $83.3 million in losses in Q3 2022, driven primarily by mark-to-market losses on mortgages held, as interest rates rapidly rose. This is after the firm reported $52.1 million and $43.5 million in losses in the prior two quarters. It should be noted that if interest rates swing the opposite direction, these M2M losses could become M2M gains .

Housing Market Fundamentals

The biggest concern among many investors looking at the mortgage sector is an expected housing market price collapse. The rapid increase in mortgage rates has definitely taken a hit to the market. Existing home sales have been depressed to levels seen during the COVID-19 shutdown, as well as the post-housing bubble recovery period.

Realtor.com

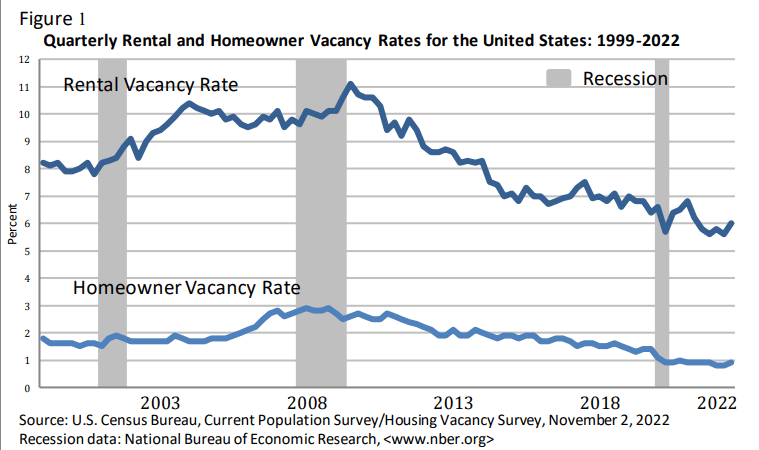

The depressed level of home sales has led investors to speculate that we are in for a repeat of the 2008 housing bubble crash. However anything could be further from the truth. There is simply a lack of housing supply which is causing home price inflation that won't be corrected by higher interest rates. Recent data from Census.gov shows that rental vacancy (6%) and homeowner vacancy rates (0.9%) are at multi-decade lows.

{kind=link}

Warren Buffett once joked in 2009 that the way to fix housing prices was to "blow up" all the extra homes. Well, the household formation rate and the lack of sufficient homebuilding over the past decade have taken care of the past housing inventory problem for us. Now, we have swung the opposite direction and we have a lack of affordable housing units.

According to Pew Research, 49% of Americans believe there is a shortage of affordable housing in the United States. Further, other groups estimate a shortage of 7 million housing units on the low-income side of the market. This is not a problem that can be fixed by hiking interest rates. Supply must be increased to meet demand and that means we need to have affordable mortgage options, including Non-QM.

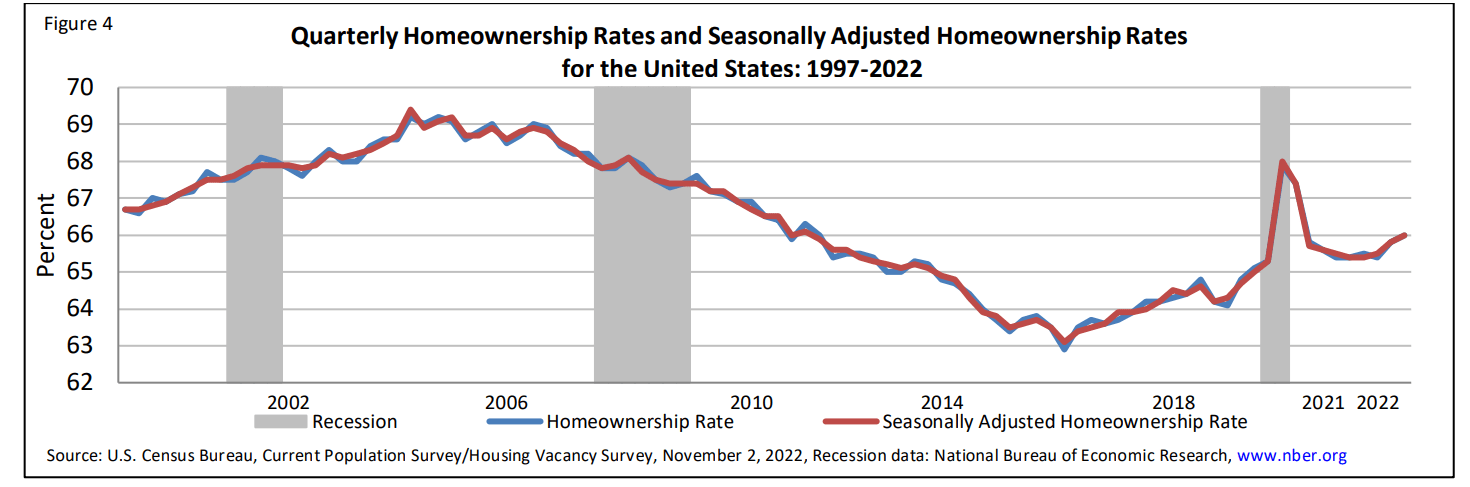

The homeownership rate at 66% has also yet to rebound to levels seen in the late 1990s. This suggests some pent-up demand could have been brewing as well, even among potential homebuyers that have been out of the market.

{kind=link}

Summary

The path of interest rates is difficult to predict, but with the year-end tax loss selling pushing these stocks to the bottom of their 52-week range, you should consider whether you might want a little exposure to the mortgage sector as a contrarian investment. Stocks like Rocket Mortgage, loanDepot, Impac Mortgage, and Angel Oak could benefit greatly from a change in the economic cycle and many economists are predicting a recession is coming which could pause and possibly reverse interest rate hikes. Housing market fundamentals support continued confidence in lending in this area.

For further details see:

Rocket Companies: In 2023, Mortgage Stocks May Be A Contrarian Buy