RKT - Rocket Companies: To Sell From Buy With At Least 2 Tough Years Ahead

2023-03-27 16:18:33 ET

Summary

- We've learned a lot about mortgage banking and Rocket over the past year. A lot of what we've learned isn't good.

- The next two years should continue to be rough for the business.

- My earnings model gets Rocket to about breakeven both in '23 and '24.

- The stock is selling at nearly 2X book value, expensive for a mortgage banker with a weak earnings outlook.

I wrote my first report on Rocket (RKT) for Seeking Alpha a bit over two years ago, suggesting a Sell at its $17 price at that time. I stayed negative until this past September 30, when I gave it a cautious Buy. The stock was $6.30 then, and I gave a $10 target price. I am now lowering the target price to $7-8 and suggesting that holders take money off the table.

Lessons from the past two years

The past two years have been interesting for Rocket, to say the least. When it went public, the company said this in its first press release, with fun fintech buzzwords in bold:

"Rocket Companies has a proven record of innovation that drives industry disruption …We see tremendous runway to drive long-term profitable growth by increasing market share in the massive and fragmented mortgage industry and leveraging our technology platform to unlock opportunities in our ecosystem .”

I’m restraining my intense desire to make fun of this hype. Instead, here are the facts:

1. Rocket is a mortgage banker, not a tech company. Every company is a tech company today, except maybe for the deli I got lunch from today. Rocket’s results over the past two years have paralleled the mortgage banking cycle. They have not been on a “tremendous runway.”

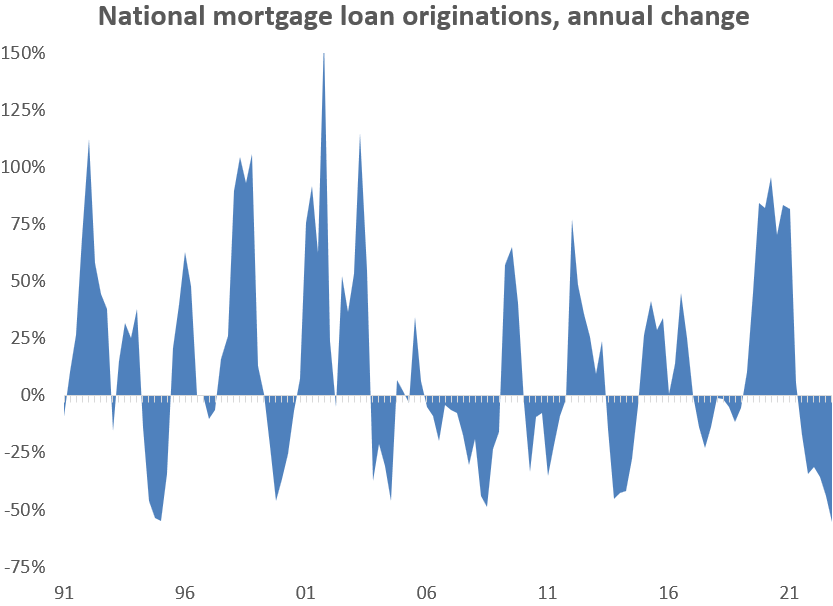

2. Mortgage banking remains wickedly cyclical. Here is the history:

{kind=link}

Fannie Mae

Source: Fannie Mae

Home sales are moderately cyclical with the economy, and mortgage refinancing is wildly cyclical with interest rates. The post-COVID refi boom inevitably ended in today’s mortgage origination world – this quarter’s business volume is 77% below the peak. By the way, interesting that the company went public only two months before the cycle peak.

3. Rocket is unusually refinancing-dependent. For some reason, Rocket does not report its mix of mortgage originations for home purchase and for refi. I’ve followed mortgage banking for over 30 years, and I’ve never seen that. But a regression analysis comparing Rocket's originations against national mortgage purchase and refi data clearly shows that Rocket’s business heavily depends on refinancing. As such, Rocket’s market share of national originations plummeted from its peak of 9½% in Q1 ’21 to 5¼% last quarter.

4. Rocket’s earnings got hurt more than I expected by the downturn. In my first report from March ’21 I said “ That leaves Rocket's EPS well under $2 a share for a long time. ” In my most recent report I said “ I believe that Rocket's normal earnings is about $1.00 a share. That is in the neighborhood of Wall Street's expected '24 EPS of $0.83. ” Well, now the consensus EPS for Rocket as collected by Seeking Alpha is ($0.05) this year and only $0.53 next year. And I argue below that the ’24 consensus estimate could be way high.

Rocket should lose money this year and barely make some next year

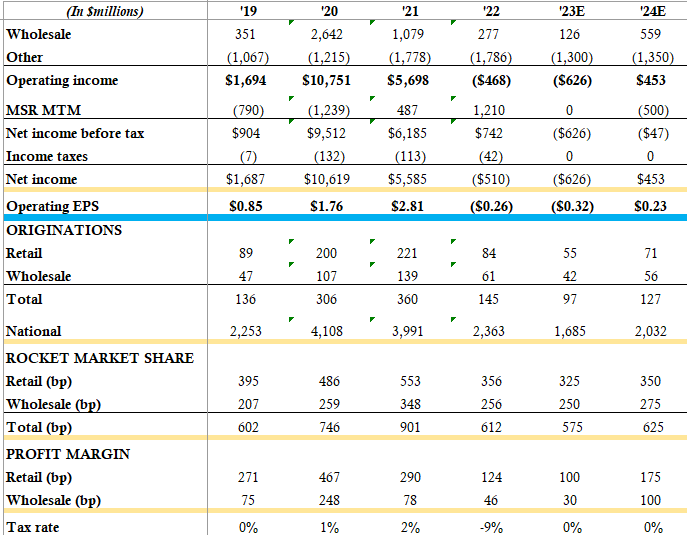

My earnings model has four key line items, per Rocket’s operating earnings reporting:

- Retail includes both Rocket’s direct-to-consumer lending, its ancillary lending services like title insurance, and its income from servicing loans.

- Wholesale means originating loans through mortgage brokers and other consumer lending partners.

- Other is Rocket’s other businesses (all relatively small) and its corporate overhead.

- MSR MTM is a non-cash accounting for changes in the estimate for how much the present value of its loan servicing is worth. I agree with Rocket that it should not be included in operating income.

Here is my model. A discussion of my assumptions follows.

{kind=link}

Rocket financial reports

Sources: Rocket Companies financial reports.

My assumptions - loan originations

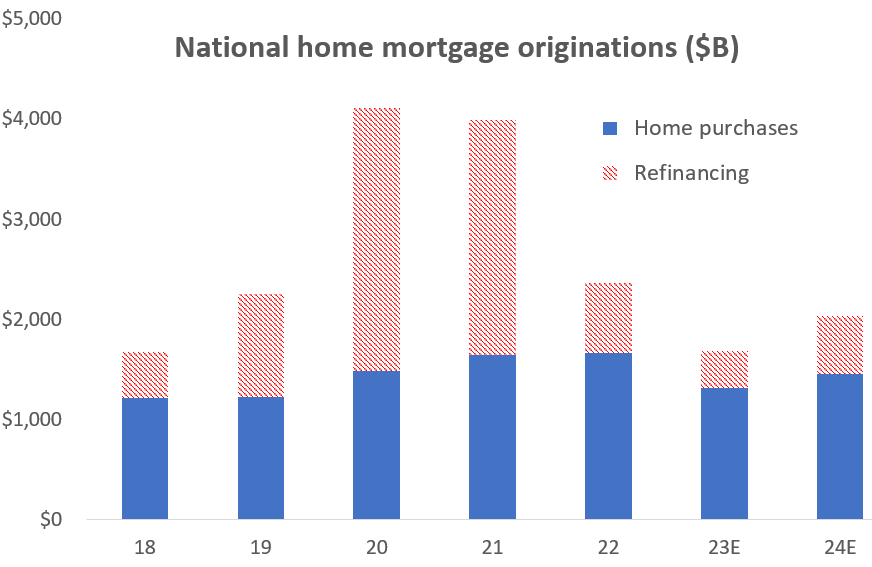

Step 1 is to estimate national originations. I’ll leave that work to Fannie Mae. Here’s the recent history and Fannie’s forecast:

{kind=link}

Fannie Mae

Source: Fannie Mae

We all know why mortgage origination volume dove lower since ’21 – higher mortgage interest rates and, to a far lesser extent, higher home prices. Fannie Mae assumes that mortgage rates will fall to 5% by next year, but origination volume next year should still not reach the 2019 level.

One key reason for the weak forecast is that so many American homeowners have low-rate mortgages that they have very little reason to refinance, and which should even dampen their interest in moving to another home. Essent Mortgage data suggests that about 60% of American homeowners have below 4% mortgages, and at least another 20% have sub-5% mortgages.

Step 2 is market share . I expect Rocket’s share has bottomed out and will gradually rise again. While a lot of excess industry capacity has come out over the past year due to business shutdowns and layoffs, more will certainly occur. Rocket has the financial strength to take advantage of that.

My assumptions – profit margins

Rocket’s profit margins for retail and wholesale loan originations are tough to forecast; they’ve swung sharply, as the historic data in the model shows. My forecast assumes an improvement from Rocket’s (and the industry’s) horrific levels of the second half of last year, but not a return to the pre-COVID 2019 levels.

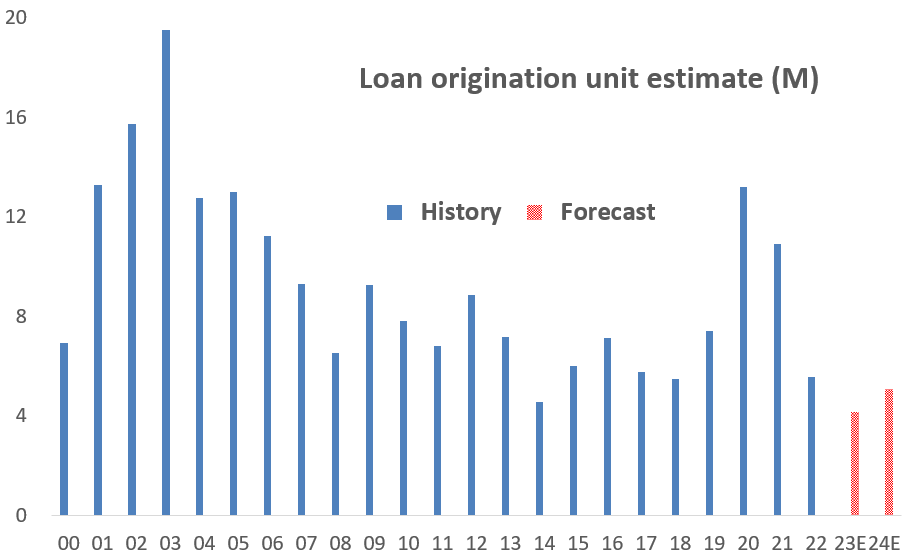

My pessimism is based on the following chart. It assumes that originating a $500,000 mortgage loan or a $200,000 one requires similar manpower. I therefore calculated “unit” mortgage originations, dividing dollar volume of national mortgage originations by the average home price for each year. This chart showing my calculations suggests that ’23 and ’24 unit volume will be among the lowest ever since 2000:

{kind=link}

Fannie Mae and HUD

Sources: Fannie Mae and HUD

This exceptionally weak demand should keep the mortgage banking industry scrambling to reduce capacity for an extended period. Excess supply over demand means lower profit margins.

My assumptions – other

As I said above, this line item includes corporate overhead plus the profit (probably loss) contribution of Rocket’s other businesses, which include an online consumer finance business and used car sales among others. I assume that Rocket will keep cutting expenses through this year before stabilizing next year.

Valuation – The current stock price is optimistic

With no material earnings in sight for at least a few years, how do we get a handle on valuation? For most financials, another good benchmark is book value. Mortgage bankers traditionally sell at around book value. Rocket at present is selling at nearly two times book value. That is quite optimistic considering that we investors will have to wait a while before book value grows again.

If Rocket’s stock price gets back in the $6 range again, I’ll take another look. In the interim, I’d suggest looking elsewhere for capital gains.

How could I be wrong? The bull cases

1. Interest rates could plunge due to a serious recession. Rocket doesn't hold mortgage credit risk, so a sharp recession with a sharply easing Fed will definitely benefit Rocket.

2. Far more cost cutting than I have modelled. Could Rocket return to steady, albeit modest, earnings well before 2025? Maybe.

3. Stories. Rocket was briefly a meme short squeeze story; could happen again I guess. Takeover rumors? Not impossible, although unlikely for a banking industry with its own problems.

For further details see:

Rocket Companies: To Sell From Buy, With At Least 2 Tough Years Ahead