RCKT - Rocket Pharmaceuticals: Soaring On Pivotal Danon Disease Study Agreement - More Upside Ahead?

2023-09-14 09:40:10 ET

Summary

- Rocket Pharmaceuticals announced yesterday it had reached agreement with the FDA on a potentially pivotal study of in vivo gene therapy candidate RP-A501.

- The drug candidate has faced a long journey to get to this point - now a historic opportunity awaits.

- Data from the study - which could be used to support accelerated approval - will not arrive for at least 15 months.

- Nevertheless, the market's positive response to the news - sending RCKT's share price soaring by >30% - may not have been positive enough.

- Rocket has several other ex-vivo assets showing promise, but if RP-A501 makes it to market - as it has a good chance of doing based on P1 data - Rocket is substantially undervalued today.

Rocket Pharmaceuticals ( RCKT ) stock was soaring yesterday as the company announced alignment with the FDA on its potentially pivotal study of in vivo gene therapy RP-A501, indicated for Danon Disease, which will begin this quarter. The market opportunity may be restricted but the historic opportunity in front of the company is arguably being undervalued by the market, as I suggested back in February. In this note I cover yesterday's highly positive developments in detail, and provide some thoughts around the prospects for further share price growth

Investment Overview - The Value of In Vivo Gene Therapy, Rocket's Initial Success, Followed By Clinical Hold

When I last covered Rocket Pharmaceuticals in a deep dive note for Seeking Alpha back in February, I gave the gene therapy specialist a "Buy" rating based primarily on the promise of the company's exciting in vivo adeno-associated virus (“AAV”) program for Danon disease.

Danon Disease ("DD") is "a multi-organ lysosomal-associated disorder leading to early death due to heart failure" with an estimated patient prevalence of 15k - 30k in the US and EU, according to Rocket's Q223 quarterly report , which goes on to state:

DD is an X-linked dominant, monogenic rare inherited disorder characterized by progressive cardiomyopathy which is almost universally fatal in males even in settings where cardiac transplantation is available.

DD predominantly affects males early in life and is characterized by absence of LAMP2B expression in the heart and other tissues. Preclinical models of DD have demonstrated that AAV-mediated transduction of the heart results in reconstitution of LAMP2B expression and improvement in cardiac function.

Rocket has been conducting a Phase 1 study of RP-A501 in 7 patients. The study actually began in September 2020, and when Rocket released data in December 2020, the results wowed the market - Rocket's stock price leapt from ~$32, to $60 overnight.

The results revealed that "Cardiac LAMP2B protein expression by immunohistochemical staining was greater than 50% of normal LAMP2B in two patients with follow-up data of up to one year," and that:

Males with Danon Disease typically have elevated BNP, transaminases and creatine kinase as a result of skeletal and heart muscle damage. Cardiac dysfunction is often rapidly progressive and severe, with concomitant reductions in cardiac output. RP-A501 demonstrated consistent stabilization or improvements across all of these clinical measures as of the data cutoff.

Gaurav Shah, M.D., Chief Executive Officer and President of Rocket commented that "these early results suggest a path to a potentially transformative option for Danon Disease, and possibly the first viable gene therapy approach for cardiac diseases."

No in vivo gene therapy has ever been approved, but the opportunity to deliver a gene therapy directly into the patient via an injection is thought to be significantly more convenient, and safe, than the ex-vivo approach, which involves a patient undergoing a preconditioning regime similar to chemotherapy to allow cells to be harvested from their body, taken to a lab and engineered, and then reintroduced into the patient.

Despite the risks of the preconditioning, and dangers of a patient's immune system rejecting the engineered cells, leading to potentially fatal complications such as graft vs host disease, several ex-vivo therapies have been approved targeting hematological cancers, but the value the market attaches to an in vivo breakthrough can be evidenced not only by Rocket's share price gains in 2020, but also by the gains made by Intellia Therapeutics ( NTLA ) stock after the company became the first to demonstrate a positive therapeutic effect for a in vivo therapy, in 2021, when its candidate NTLA-2001 had reduced TTR Serum levels in six patients with the disease Transthyretin ((ATTR)) Amyloidosis, Intellia's market cap briefly rose >$10bn.

As covered in my previous note on Rocket, the company's stock price tanked after a patient in the Phase 1 study receiving high-dose RP-A501 suffered progressive heart failure and was forced to undergo a heart transplant. According to Rocket:

This patient had more advanced disease than the four other adult/older adolescent patients who received treatment in the low and high dose cohorts, as evidenced by diminished baseline left ventricle ejection fraction (35%) on echocardiogram and markedly elevated left ventricle filling pressure prior to treatment. The patient’s clinical course was characteristic of DD progression. The patient is doing well post-transplant.

The FDA placed a clinical hold on the Phase 1 study, and although it was lifted in August 2021, Rocket's share price continued to fall, reaching a low of $9 in May 2022 - clearly, the market had lost faith in Rocket's approach, and attached significantly less value to its 3 ex-vivo programs, discussed as follows in the latest quarterly report:

These include programs for Fanconi Anemia (“FA”), a genetic defect in the bone marrow that reduces production of blood cells or promotes the production of faulty blood cells, Leukocyte Adhesion Deficiency-I (“LAD-I”), a genetic disorder that causes the immune system to malfunction, and Pyruvate Kinase Deficiency (“PKD”), a rare red blood cell autosomal recessive disorder that results in chronic non-spherocytic hemolytic anemia.

Rocket Pharma's Resilience Rewarded With FDA Phase 2 Study Nod

Fortunately, despite the safety setback, Rocket did not give up on RP-A501, although management did decide to stop using the higher dose - 1.1e14 gc/kg - and focus exclusively on the low dose - 6.7e13 gc/kg. Further safety measures were also introduced as follows:

exclusion of patients with end-stage heart failure, and a refined immunomodulatory regimen involving transient B- and T-cell mediated inhibition, with emphasis on preventing complement activation, while also enabling lower steroid doses and earlier steroid taper, with all immunosuppressive therapy discontinued 2-3 months following administration of RP-A501.

New efficacy measures were also introduced - New York Heart Association (“NYHA”) Functional Classification - a "gold standard" 4 point scale - Brain natriuretic peptide (“BNP”), a "a key marker of heart failure with prognostic significance in CHF and cardiomyopathies", High sensitivity troponin I - a marker of cardiac injury, Echocardiographic measurements of heart thickness, the patient reported outcome questionnaire Kansas City Cardiovascular Questionnaire (“KCCQ”), histologic examination of endomyocardial biopsies, and LAMP2B gene expression in endomyocardial biopsy samples.

In September last year Rocket presented interim data for the low and high dose cohorts of the Phase 1 study, which importantly revealed "no unexpected and serious drug product-related adverse events or severe adverse events" in either the adult/older adolescent or pediatric low dose cohorts, after 2/3 years.

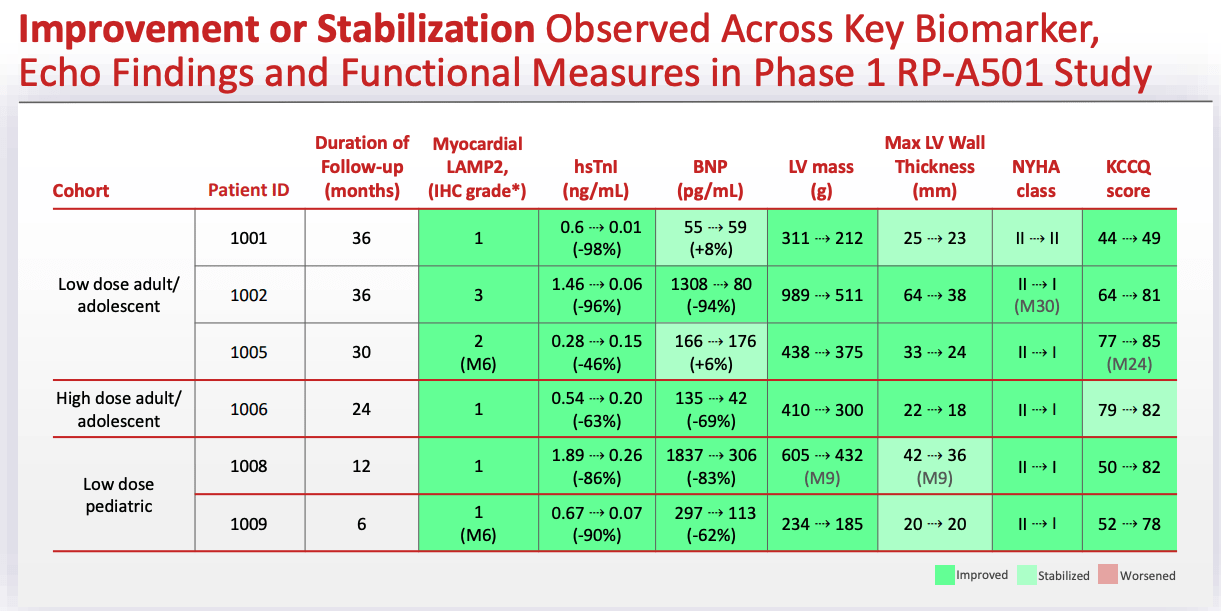

Positive improvements were reported across all of the efficacy measures mentioned above, triggering a slight increase in Rocket's share price, which rose to ~$22, and in January this year, Rocket shared further positive updates. There is a lot of data to consider, but the best summary is arguably provided in the company's September '23 investor presentation, shared below,

Rocket - key findings from P1 study of RP-A501 (investor presentation)

{kind=link}

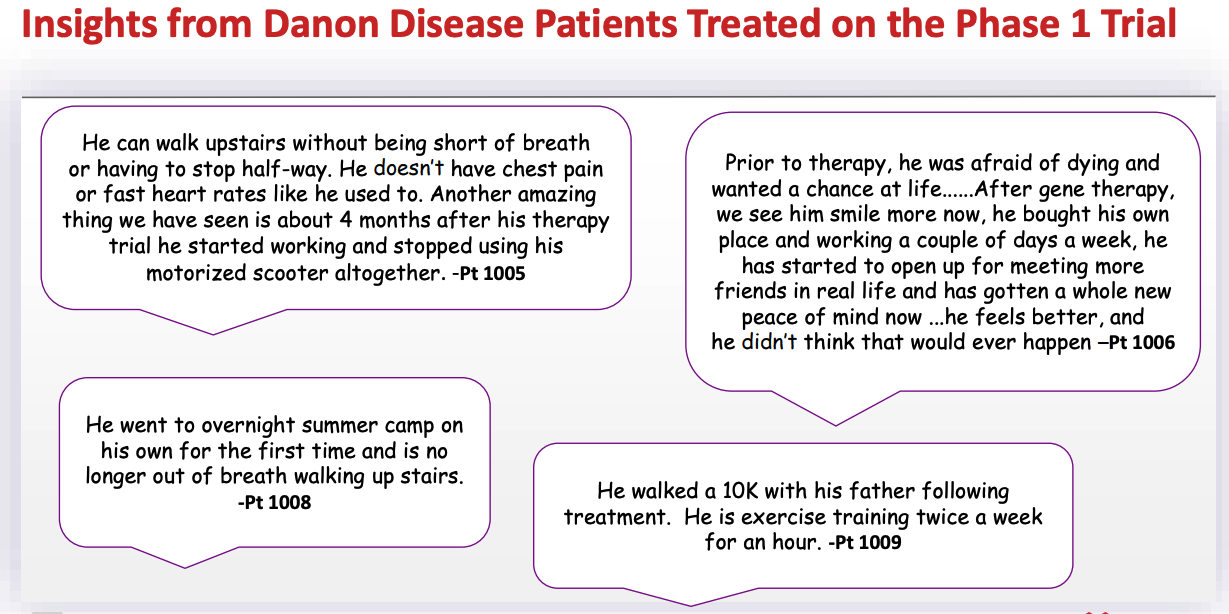

As we can see, the data is almost universally positive, and some personal testimonies from care-givers seem to reinforce the thesis that RP-A501 can have a positive effect on patients.

insights from DD patients (Rocket presentation)

{kind=link}

In June, Rocket shared the news that it had received a Priority Medicines ("PRIME") designation from the European Medicines Agency for RP-A501, and its share achieved an 18-month high price of $18, albeit the gains could also be attributed to progress of its ex-vivo programs, with Phase 2 studies in FA, LAD-I, and PKD all showing positive signs of safety and efficacy.

By the beginning of September, however, the share price had drifted downward to a value of ~$15. While it's not unusual for early stage biotech's share price to drift downward, in Rocket's case, with such a potentially breakthrough therapy in RP-A501, it does seem surprising that the market was selling the company's stock, not buying it.

Validation finally arrived - in part - this week, however, as Rocket announced it had reached "final alignment" with the FDA on a "global Phase 2 pivotal trial of RP-A501 for Danon Disease", and simultaneously completed a stock offering at $16 per share, of 7.8m shares, plus 3.1m pre-funded warrants, to raise a total of ~$175m.

Usually, a stock offering will be met with a fall in the share price, as existing investors' holdings are diluted, but the alignment with the FDA on a potentially pivotal study - i.e. data from the study may be used to support an accelerated approval of its gene therapy, sent the stock price soaring once again, ending trading yesterday priced at $21.2.

The Next Chapter - A 12-Patient Pivotal Study, A Shot At An Historic First In Vivo Therapy Approval

Although shareholders buying Rocket stock will have made only a marginal gain on their investment, after a surprising bear run in August, in my view, there are plenty of grounds for optimism, as Rocket apparently takes the lead in the race for a first approved in-vivo gene therapy.

In a press release , CEO Shah described discussions with the FDA as "highly collaborative", and celebrated the "first-ever regulatory pathway to approval for a genetic treatment for heart disease". The CEO also paid tribute to "our in-house cGMP manufacturing capabilities, which has already provided us with sufficient material for the pivotal study and should support our eventual commercialization efforts.”

The 12 patient study will use a "biomarker-based co-primary endpoint consisting of improvements in LAMP2 protein expression (? Grade 1, as measured by immunohistochemistry), and reductions in left ventricular (LV) mass," with secondary endpoints including change in troponin, natriuretic peptides, KCCQ, and NYHA - in short, markers in which the Phase 1 study has already demonstrated improvements.

Rocket says it will assess co-primary endpoints at 12 months, and that it intends to start the Phase 2 study in Europe this quarter - a 2-patients pediatric study is already underway.

The press release also noted Rocket has received an ICD-10 code from the Centers for Medicaid and Medicare Services ("CMS") - my inference here is that this would set up RP-A501 for reimbursement if approved, i.e., patients would only have to pay out-of-pocket expenses for the drug.

In summary, all things considered, this is an exciting time for Rocket and its investors, and my feeling is that, had it not been for the fundraising, the biotech's stock would be trading substantially higher today. As I noted in my previous post:

Danon disease may be a small market opportunity - Rocket estimates a prevalence of 15k - 30k individuals, with an annual incidence of 800 - 1,200 individuals, but given the high prices of gene therapies, if we consider a scenario where RP-A501 costs $1m for a course of therapy, and treats 1k patients per annum, or where RP-A501 costs $2m, and is used to treat 500 patients - we could be looking at a blockbuster (>$1bn per annum) revenue opportunity.

Revisiting the market opportunity, I would be more inclined to use a list price of ~$500k and increase the patient treatment pool by 2x - after all, the drug is on the accelerated approval path which is used by the FDA when it identifies a strong unmet need amongst the patient population.

When an accelerated approval is granted is usually in response to the rolling submission of data from the pivotal study, so it is possible that if the 12m results are positive enough - and there is reasons to believe they will be - the drug could be a contender for approval before the end of 2024, with a full launch followed by first revenues earned in early 2025.

Drugs given an accelerated approval are usually subject to a post-marketing study, that is required to support the pivotal study data, and ensure that longer-term safety and efficacy goals are met - if the post-marketing study fails, the drug can be withdrawn from the market.

Concluding Thoughts - Prospects of Success, And A Suggested Target Price for RCKT Stock

I can't profess to be a gene therapy insider but even with the dilutive fundraising, I am surprised that Rocket does not generate more excitement in the media, and within the markets, as the company did in 2020, when its share price spiked to >$60, and as Intellia did when its in vivo therapy first showed a positive effect in patients with Transthyretin ((ATTR)) Amyloidosis.

In my last post I cited questions about durability of response, a small patient population, and safety issues around the higher dose as potential reasons why the market is not celebrating the pivotal study news more, and pushing the share price higher.

There is no question that Rocket has more to prove in the clinic - can RP-A501 generate positive biomarker improvements across so many endpoints in a larger, pivotal study, as it did in the Phase 1? With that said, however, there is 2-3 years worth of data from the Phase 1, which goes a long way toward easing safety, durability, and efficacy concerns. The patient feedback is also quite compelling, and the FDA is also clearly buying into this in-vivo therapy.

It's worth noting that at $1.7bn at the time of writing, Rocket enjoys quite a high valuation, and the Danon Disease market opportunity may ultimately fall well short of becoming a blockbuster (>$1bn revenues per annum) one, as creating awareness, securing physician approval, securing sufficient reimbursement, and winning over patients are all significant challenges. On the plus side, following its fundraising Rocket boasts ~$500m of cash - more than enough to fund all of the companies studies, and support a commercial launch of RP-A501, should it come to that.

Nevertheless, the historic achievement of becoming the first to deliver a in vivo gene therapy in heart disease and the validation of Rocket's approach ought to be worth almost as much as the market opportunity itself, and personally, I would regard a market cap valuation of ~$3bn a fairer assessment of what Rocket's business is worth today.

Although I have not covered them in any detail in this post, there are 3 exciting ex-vivo therapies in Rocket's pipeline, 2 of which are moving toward pivotal studies, and have Fast Track, Rare Disease Orphan Drug and regenerative medicine advanced therapy ("RMAT") designations, plus a second heart disease therapy with curative ("one and done") potential, while Rocket is already working on its "next wave" of therapies.

In my experience, even when a biotech has a fairly diverse range of pipeline assets, there is usually one that the market locks onto and guides its share price valuation around, however. If, in Rocket's case, that assets is RP-A501, then personally I would consider that a major positive for shareholders. The ~15-month wait for pivotal Phase 2 data will test the market's patience, and I would not even be surprised if the share price dipped <$20 again before this results arrive.

Longer-term, however, I would double down on my "Buy" recommendation for Rocket stock, based on the fact the market is being myopic about the importance of RP-A501, the market opportunity, and the validation of Rocket's approach.

For further details see:

Rocket Pharmaceuticals: Soaring On Pivotal Danon Disease Study Agreement - More Upside Ahead?