ROK - Rockwell Automation: Strong Market Position But Trading At A Fair Price

2023-11-26 19:45:51 ET

Summary

- Rockwell Automation is a provider of digital transformation and industrial automation solutions with strong revenue growth.

- Government support and the rapid growth of the industrial automation market are driving Rockwell Automation's growth outlook.

- I recommend a hold rating due to the unattractive risk/reward situation.

Investment action

Based on my current outlook and analysis of Rockwell Automation ( ROK ), I recommend a hold rating. Although the expectation of rapid growth of the industrial automation market and the government’s support for infrastructure development are set to drive its growth outlook, the lack of an attractive share price gain pushes me to stay on the sidelines for ROK. I would continue to wait until its share price lowers to a more attractive range or if ROK’s growth outlook and EPS are raised.

Basic Information

ROK is a provider of digital transformation and industrial automation solutions, and it sells its solutions in many locations worldwide. Allen-Bradley, FactoryTalk, and LifecycleIQ Services are some of the brands. Over the last 4 years, ROK has been growing at double-digit rates, and it is accelerating. The opening of economies to lockdowns and border travel restrictions played a part in this growth. All the pent-up demands from these restrictions caused a surge in manufacturing growth, which drives demand for ROK’s automation solution. However, the current macro-outlook is casting shadows on its growth outlook. Even though revenues are growing, operating expenses did not grow and remain stable at an average rate of 23% of revenue. This shows that its business model’s OPEX requirement is neutral. Thus, it can rescale its business size accordingly. Therefore, the shadows cast by an uncertain macro-outlook are not a major concern for me. In addition to these, it managed to reduce its long-term debt from 32% in 2019 to 25.3% for the latest financial year.

Review

ROK reported robust 4Q23 results as its revenue grew by 17.7%. Breaking down by segment, software, and control saw growth of 23.4%, intelligent devices grew 17.8%, and life cycle service grew 10.2%. Improved growth and EBIT in smart devices, software, and control drove the robust performance, offsetting lifecycle services' poor EBIT. The backlog was reported at $4.1 billion. In terms of guidance, ROK has set an EPS projection for FY24, ranging from $12 to $13.50. Furthermore, it guided organic sales growth from negative 2% to positive 4% and sector margins of 21.5%. The adjusted earnings per share for 4Q23 were $3.64.

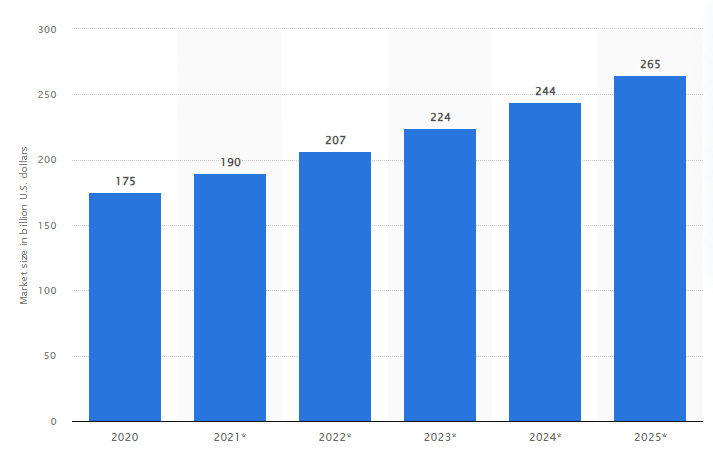

High-quality automation technology plays a big part in the industrial manufacturing process. Industry automation technology aims to improve operational efficiency by accelerating production rates, ensuring efficient use of resources, reducing the supply chain, and ensuring consistency in product quality. Market of industrial automation is at approximately $175 billion in the year 2020. It is forecast to expand at a rate of 9% annually until 2025. Being the market leader in industrial automation, ROK will reap the most benefit from this rising trend to adopt industrial automation.

{kind=link}

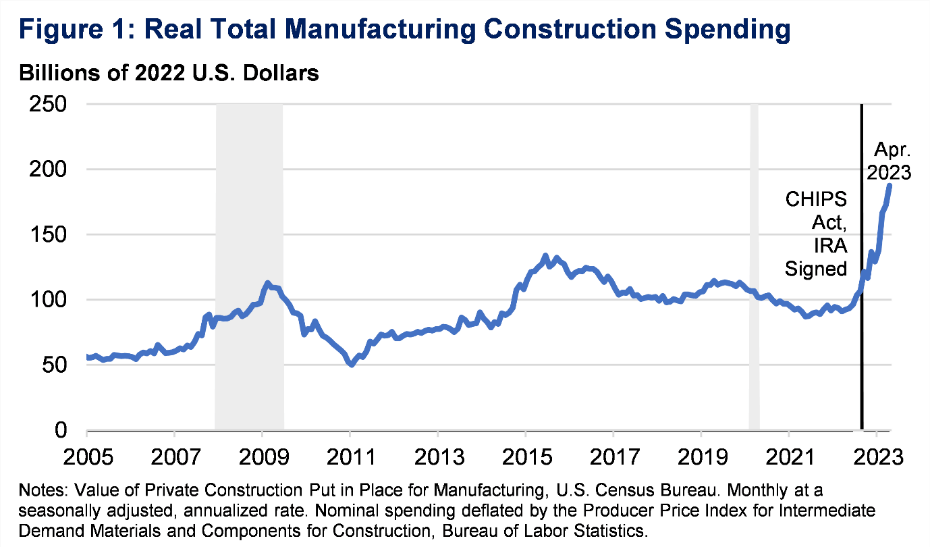

In addition, there is government support in place to propel further demand for the development of infrastructure. The IIJA, IRA, and CHIPS Act's public spending and tax incentives are directed towards the construction of manufacturing facilities. Prior to these government initiatives, total manufacturing construction spending was averaging ~$100 billion. As of April 2023, it had nearly doubled in size. I believe this spending growth would stimulate demand for industrial manufacturing automation and further bolster ROK as the global leader. This government-spending-induced demand is exactly the objective of the support. Its purpose is to boost the overall economy. Being the global leader in industrial automation, I firmly believe this expansion will drive ROK’s revenue growth outlook.

{kind=link}

ROK projected that annual recurring revenue [ARR] would increase by double digits over the long term, rising from over 8% of sales in FY23 to over 9% in FY24. The addition of the FactoryTalk design studio copilot with MSFT brought further enhancements to ROK's industrial software offering. With growing concern about a shortage of workers and an aging population, ROK also brought attention to the need for autonomous production logistics. Management also stated that cyber security is still a major focus for ROK. Hence, in October 2023’s press release, ROK announced that it had signed an agreement to acquire Verve industrial protection. Verve is a cybersecurity software services company that specializes specifically in industrial environments. With ROK being a market leader in industrial automation, I believe this acquisition will make ROK even stronger in the industrial automation segment.

Valuation

I believe ROK will grow at 4% in 2024 and 5% in 2025. This growth expectation is based on management guidance, and I am using the higher end of the range for both revenue and EPS growth guidance. Given its robust 4Q23 results with double-digit growth in all three segments, the importance of automation in the industrial manufacturing process, the expected rapid growth of the industrial automation market, and the US government’s support to push the development of infrastructure, I believe these factors are providing ROK with the tailwind they require to achieve their guided growth. In addition, ROK’s expectation for double digits in ARR further bolstered my belief. Its recent acquisition of Verse provides a compelling point of view.

{kind=link}

ROK is currently trading at 20.65x forward P/E. Its peers are trading at a median of 19.3x. In terms of margins, they are in line. ROK’s EBITDA margin is 2% lower than peers’ medians. ROK’s EBIT margin is 1% higher than peers' medians. Lastly, ROK’s net margin is 1% lower. Overall, I would consider it a close match. In terms of the 2-year growth outlook, ROK’s 5% growth is in line with peers’ medians. With this comparison, I am assigning 19.3x to ROK, and my price target is in line with its current share price. As ROK’s share price has already reached my target price, I recommend a hold rating despite its robust business.

{kind=link}

Risk and final thoughts

One potential upside is a stronger-than-expected increase in industrial production, which could boost ROK's product demand. Another upside is a stronger-than-expected recovery in customer capital spending due to a better macro-outlook, which could benefit ROK's business as it operates in the industrial automation market. The industrial sector's growth is generally correlated to the strength of the economy.

ROK's 4Q23 results highlight its strong market leadership in industrial automation, with strong revenue growth across all segments. This impressive performance, combined with its strategic initiatives like the acquisition of Verve and collaboration with MSFT, really positions itself well as a leader in this rapidly growing industrial automation market. In addition, support from government initiatives further supports its growth trajectory by stimulating manufacturing automation’s overall demand.

For further details see:

Rockwell Automation: Strong Market Position But Trading At A Fair Price