ROK - Rockwell Automation: The Market Sentiment Is About To Change

2023-09-11 14:06:13 ET

Summary

- Rockwell Automation is a leading provider of electrical equipment in the industrial automation space.

- The company has strong long-term prospects due to the adoption of automation and digitalization systems in manufacturing processes.

- However, short-term headwinds such as supply chain issues and a slowing economy are impacting the company's performance, and its high valuation will become a problem.

Investment Thesis

We have seen and will continue to see the adoption of automation and digitalization systems in manufacturing processes. Combined with plans to ramp up infrastructure spending, the electrical equipment industry is poised to see demand increase in the long term.

Being one of those companies, Rockwell Automation ( ROK ) has good long-term prospects. The market knows this and prices the stock accordingly. On an adjusted P/B basis, it is one of the most expensive stocks in the industry.

However, short-term headwinds started to hit the business, and now the market is getting it. The positive sentiment and “high-growth high-profitability” expectations are about to change. The company might see a reconsideration of its valuation.

That is why Rockwell Automation gets a “Sell” rating. The upside is mostly realized, and this is not the time to be investing in this name.

Introduction

One of the biggest trends we see right now is how fast everything gets digitalized and automated. The human factor is not as big as it was before.

This big transformation can be seen everywhere from how banks operate to how factories are being run. You had to go to a bank branch to send money two decades ago, now there is nearly nothing you cannot do on your phone. You don’t talk to anyone, you just have to press a few buttons. Similarly, you don’t see as many people working in factories anymore, but you see robotic arms that carry, attach, and detach stuff.

There are companies providing the technology behind this big transformation, and even though there is fierce competition, they are achieving huge returns. Some examples would be Emerson Electric ( EMR ), Rockwell Automation, Siemens ( SIEGY ), ABB Ltd. ( ABBNY ), and Schneider Electric ( SBGSF ).

Today, I am going to talk about Rockwell. I will explain how the industry has been booming and might be showing signs of weakness lately. The market has been very optimistic about Rockwell, but the tides might be turning.

Company Description

Rockwell Automation is an industrial automation and digital transformation solutions company with a history dating back to 1903. It is one of the oldest players in the industry.

The term “digital transformation” is a very broad one, but the company’s segments do a good job of showing what exactly Rockwell does. It has three operating segments.

The first and the biggest one is Intelligent Devices. It accounts for 45% of total revenues. Under this segment, Rockwell sells a wide range of motion control and safety devices and other industrial components that allow companies to have automated production processes. These are the robotic arms you see in factories.

The second biggest segment is Software & Control, which offers software and hardware products used to build the automation system. These are also used in system and security infrastructure. The segment accounted for nearly 30% of revenues in fiscal year 2022.

The rest 25% of revenues come from the Lifecycle Services segment. This is where the company offers anything but products: consulting on automation and digital transformation, maintenance services for products sold, and training for clients’ employees.

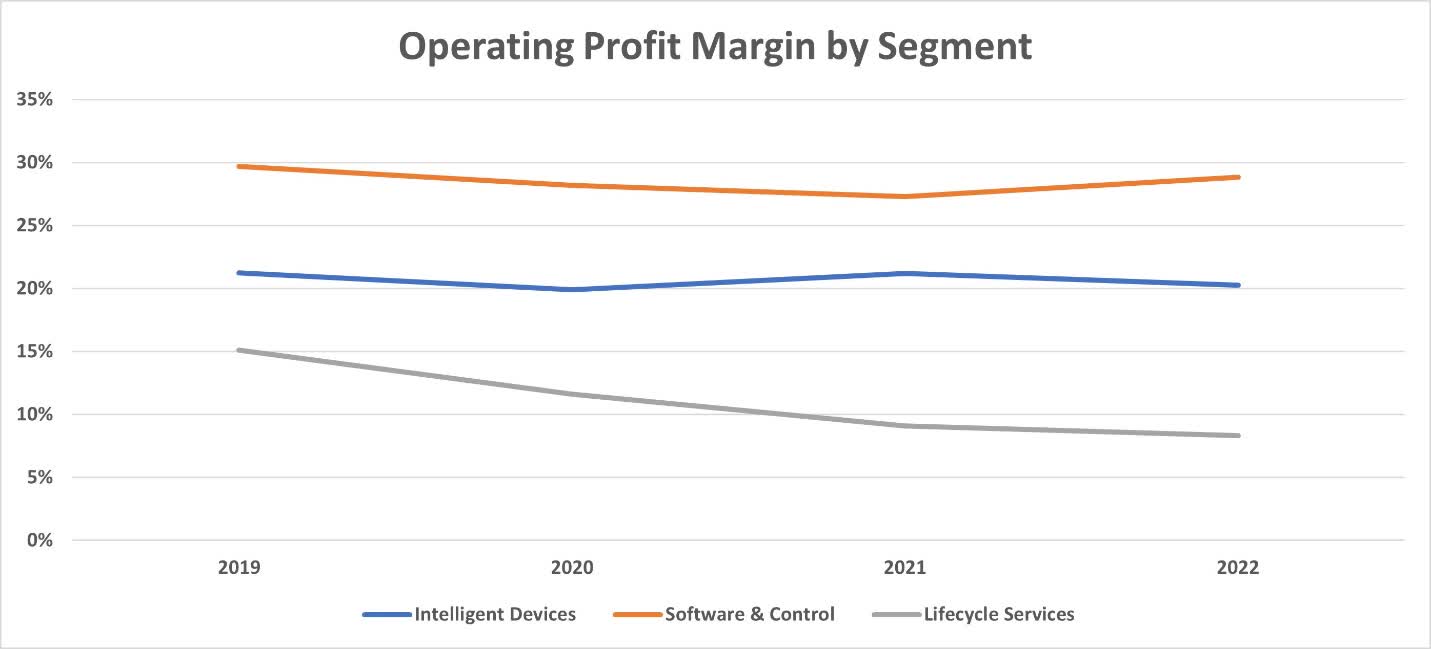

As can be seen below, the highest operating margin business among these is Software & Control. Once the products are sold under Intelligent Devices, customers have to use Rockwell’s software to be able to control them and make them operational. That is how Rockwell makes money.

{kind=link}

These products and services are sold to customers in a wide range of industries including automotive, semiconductor, and warehousing & logistics, life sciences, food & beverage, and oil & gas through independent distributors.

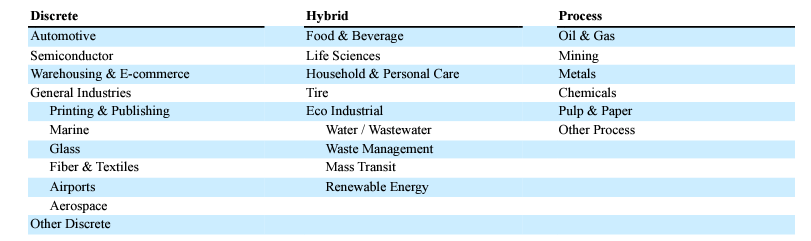

The company categorizes these customers under three titles: Discrete, Hybrid, and Process. Detailed breakdown of industries in these categories is shown below.

{kind=link}

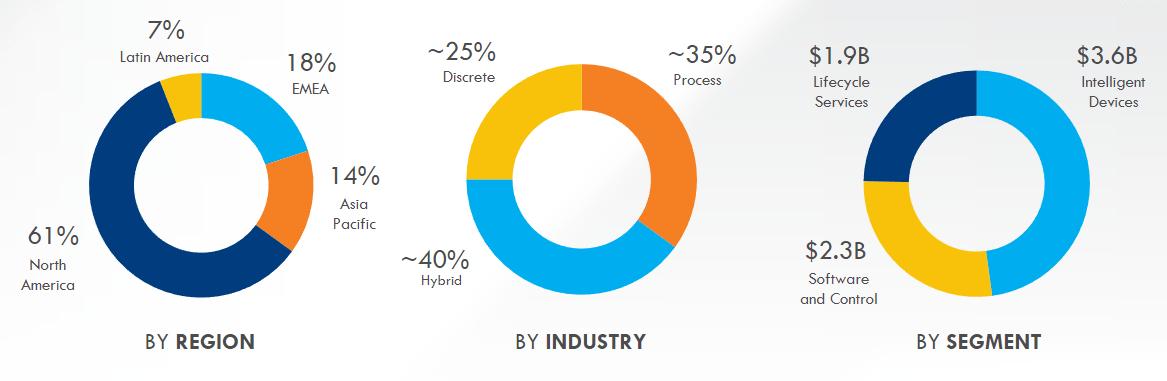

The most recent investor presentation shows that the biggest end market was Hybrid with around 40% of revenues, followed by Process 35% and Discrete (25%). The same presentation reveals that most of the sales were made in North America (61%), followed by EMEA (18%), Asia Pacific (14%), and Latin America (7%).

Investor Presentation - November 2022

{kind=link}

Long-Term Drivers

Rockwell Automation has big competitive advantages that make it able to compete against ones like Siemens, ABB, Schneider Electric, and Emerson Electric. These are all huge firms and very tough to compete against.

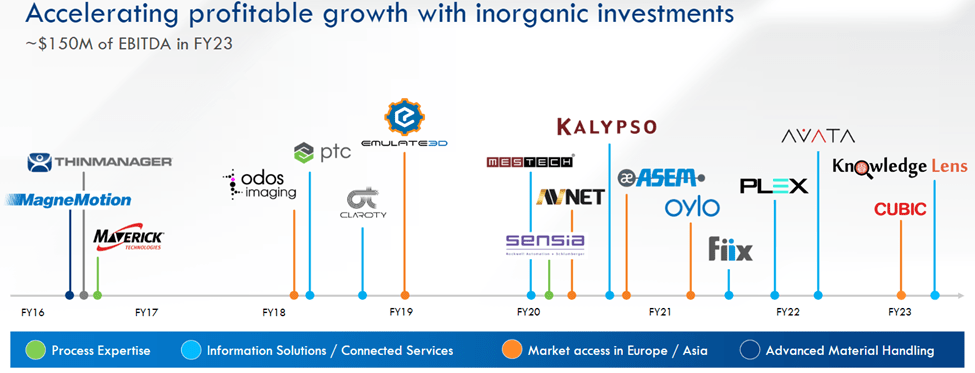

First of all, the company has been focusing on acquisitions to grow its portfolio. It has completed the acquisition of around 15 different companies since 2020. The most recent one the management announced is Clearpath Robotics , a company providing autonomous robotics for industrial applications.

This M&A strategy allows the company to have a wide range of products and turn Rockwell into a one-stop-shop for customers, increasing cross-sell opportunities. Here are the acquisitions the company made since fiscal year 2016:

BofA Global Industrials Conference - March 2023

{kind=link}

Secondly, with 61% of its total revenues coming from North America, Rockwell is poised to benefit from increasing infrastructure spending in the U.S. The Bipartisan Infrastructure Deal came into effect in 2021, and investments in the area have been skyrocketing since. This trend is likely to continue. As companies invest in their manufacturing capacity and infrastructure, they will need Rockwell’s products.

Finally, the company is getting ready to make a big push into the electric vehicle (EV) space. It has partnered with Ford ( F ) to help optimize the manufacturing and recycling of electric vehicles and batteries. It has also partnered with Hyundai ( HYMTF ) for its greenfield megasite in Georgia, U.S. While these may not be incredibly high revenue partnerships, they may be signaling other partnerships to come.

Peer Comparison

We discussed above about how fierce the competition is. The company constantly needs to invest in new partnerships and products to be able to survive. But it’s not easy.

Competitors are huge. In fact, Rockwell is the smallest one in terms of market capitalization among the firms I mentioned. This scale gives advantages to Rockwell’s competitors. So, you may think that the market is going to favor these competitors more than Rockwell and they are going to trade at higher multiples. The situation is completely the opposite.

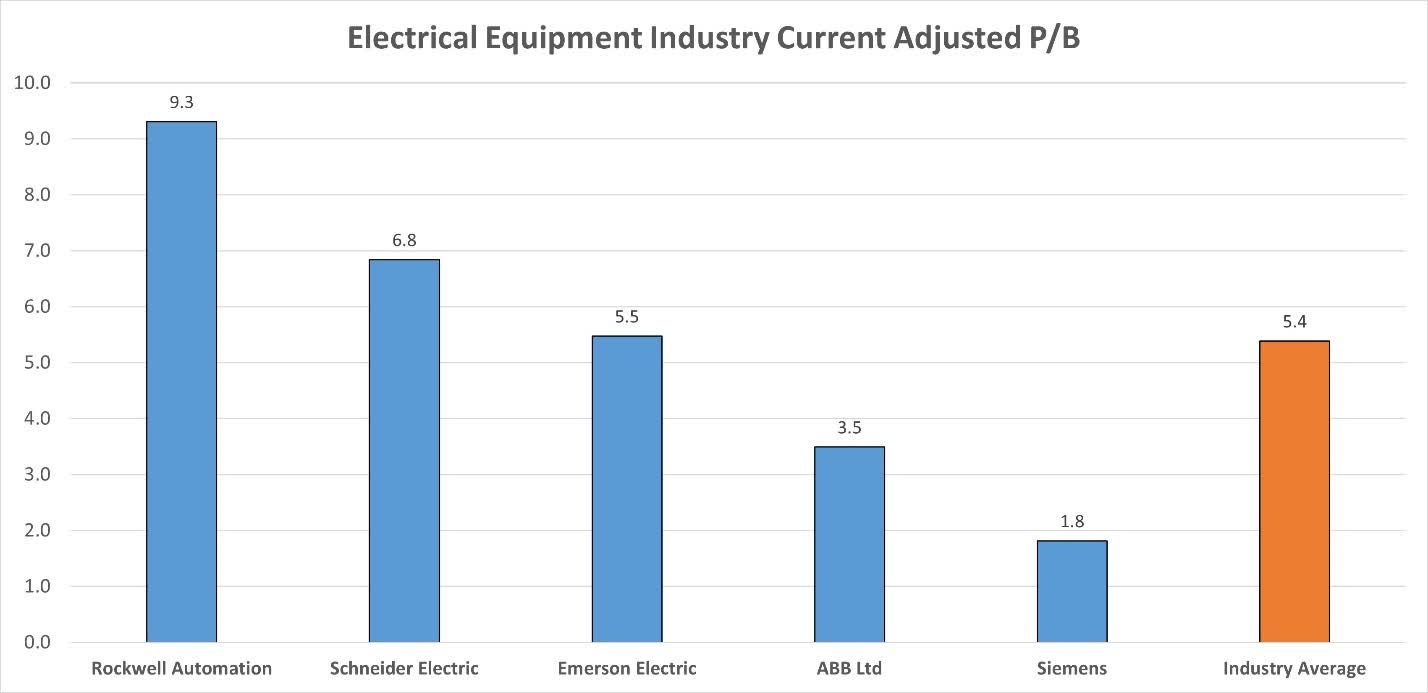

Defining the electrical equipment space as the firms we have discussed in this article, we see that the adjusted P/B of the industry is currently at 5.4x. Emerson Electric is the closest one to this average, trading at a 5.5x adjusted P/B. Rockwell Automation, however, trades at the highest adjusted P/B multiple on this list: 9.3x. See for yourself below…

{kind=link}

The market seems to be aware of the advantage of having high exposure to North America, as it prices the three companies with the highest exposure (in terms of percentage of sales) to the region at higher multiples. However, Rockwell Automation topping this chart seems unjustified and risky from a valuation perspective.

The Market Started To Get It

Rockwell released Q3 2023 earnings on August 1 st . As it’s a company that has seen solid growth since the pandemic, expectations for growth were high. It missed revenue estimates by $100 million and EPS estimates by $0.18. It also cut guidance for both top and bottom line. The updated guidance is for sales to grow at 14%-16% and EPS to be in a range of $11.7 to $12.10. The previous guidance was 16.5% growth for sales and $12.20 for EPS.

Seeing that the company didn’t grow as expected, the market reacted big, and the stock fell more than 7%, the biggest drop in 8 months. After a quick recovery, the stock continues to see pressure from sellers. The stock was also recently downgraded by Barclays . The bank’s analysts think the company is overvalued compared to its peers. This can also be seen above.

This underperformance is not without a reason. Investments in North America continue to be a long-term driver. But in the short term, Rockwell doesn’t really see its benefits. Customers are struggling with big purchases as interest rates are high, and finding capital is costlier. Additionally, there are still unresolved supply chain issues that cause lead times to get extended.

To summarize, the economy continues to slow down, and Rockwell is not enjoying it.

Risks

As this is a sell recommendation, risks related to that will be the company performing much better than expected. There are known challenges the company faces right now: high interest rates affecting customers, a slowing economy, and supply chains being slower and costlier.

These are factors that are tied to the overall macroeconomy. Even if we have a soft landing and the Fed starts to decrease interest rates in time, I don’t see much upside from here. The stock is already priced to benefit from the tailwinds we discussed. But the relative underperformance potential is bigger if things don’t go very smoothly.

The stock can be revisited once these short-term headwinds pass in the next two years. Then there might be a bigger chance of the company’s fundamentals actually showing how much they benefit from the EV adoption and high infrastructure spending in the U.S.

Conclusion

Rockwell Automation is one of the leading electrical equipment providers in the industrial automation space. That market has some strong long-term tailwinds that can push both top and bottom line higher. However, short-term headwinds should not be ignored.

The company started to see the impacts of inefficient supply chains, a slowing economy, and weakening customers. Even though there are incentives for infrastructure investments, customers are not committing to big purchases right now.

The market has been focusing more on long-term trends, but now started to see that the company is struggling after the last recent earnings call. If the market sentiment changes, the company’s high valuation will be a problem. Investors should avoid investing in this stock.

For further details see:

Rockwell Automation: The Market Sentiment Is About To Change