ROK - Rockwell Automation: Turbulence Not Yet Priced In

2023-11-14 22:14:13 ET

Summary

- Rockwell Automation is well-positioned to benefit from long-term trends in factory automation, digitalization, and electrification.

- Near-term risks from slowing industrial growth, China's weakness, and supply chain issues will likely weigh on financial results.

- The current valuation doesn't quite reflect the upcoming slowdown, and investors should wait for a better entry point before buying into the growth story.

Investment Thesis

Rockwell Automation (ROK) is a leading provider of industrial automation equipment, software, and services. The company is well-positioned to benefit from long-term secular trends like factory automation, digitalization, and electrification. Rockwell's large installed base, broad portfolio, and high switching costs provide competitive advantages.

However, near-term risks from slowing industrial growth, China weakness, and lingering supply chain issues will likely weigh on financial results over the next few quarters. Despite the recent sell-off, the stock price still reflects optimistic expectations, trading at ~20x forward P/E. While the long-term outlook remains positive, the current valuation leaves little room for error. Investors should wait for a better entry point before buying into the Rockwell Automation growth story. A Hold rating is appropriate at this time.

Company Overview

Rockwell Automation is one of the largest global suppliers of industrial automation equipment, software, and services. The company was founded in 1903 and is headquartered in Milwaukee, Wisconsin.

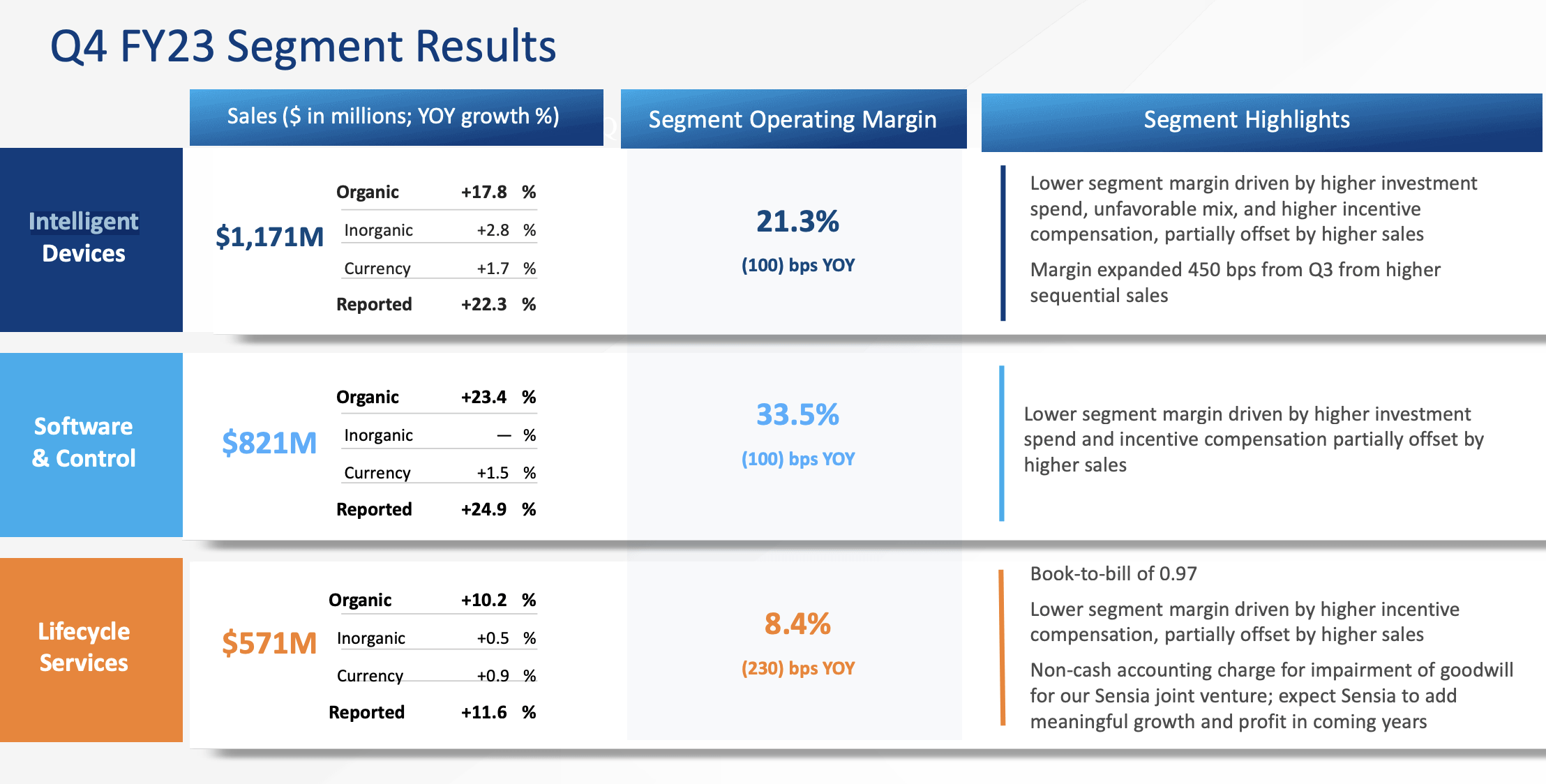

The company functions across three primary segments, each contributing to distinct aspects of its operations. The largest segment, Intelligent Devices, encompasses 45% of its sales and specializes in offering an array of industrial components such as drives, motors, sensors, and more. Within this segment, there are various specialized product lines including drives, motion, advanced material handling, safety, sensing, industrial components, and configured-to-order products.

The Software & Control segment, constituting 32% of the sales, is primarily responsible for providing both hardware and software solutions for control and information management.

The remaining segment, Lifecycle Services, accounting for 23% of sales, focuses on consultation, maintenance, and managed services, ensuring sustained support for their products and systems throughout their life cycles.

{kind=link}

Rockwell's focus markets include discrete manufacturing like automotive and semiconductor, hybrid industries like food & beverage, and process industries like oil & gas.

Competitive Advantages

Rockwell possesses several competitive strengths that solidify its position as a leading industrial automation provider:

- Installed base: The company has had equipment installed globally that requires maintenance, upgrades, and replacement parts. This is capital-intensive to replicate.

- Broad portfolio: Rockwell offers one of the most comprehensive automation solution sets spanning hardware, software, and services. This enables cross-selling and integrated offerings for customers.

- High switching costs: Once a factory is outfitted with Rockwell hardware and software, there are high costs and business disruption risks associated with changing vendors. This customer "lock-in" helps maintain market share.

- Domain expertise: With over 100 years of operating in industrial markets, Rockwell has accumulated specialized knowledge across industries and applications. This domain expertise strengthens customer relationships.

- R&D spending: The company invests over $500 million annually in R&D, focused on differentiating its solutions through emerging technologies like cloud, AI, and digital twin capabilities.

Rockwell's competitive strengths position it well to benefit from long-term growth drivers like factory modernization, industrial internet-of-things adoption, and sustainable manufacturing. However, financial results over the next year face headwinds.

Financial Profile & Recent Results

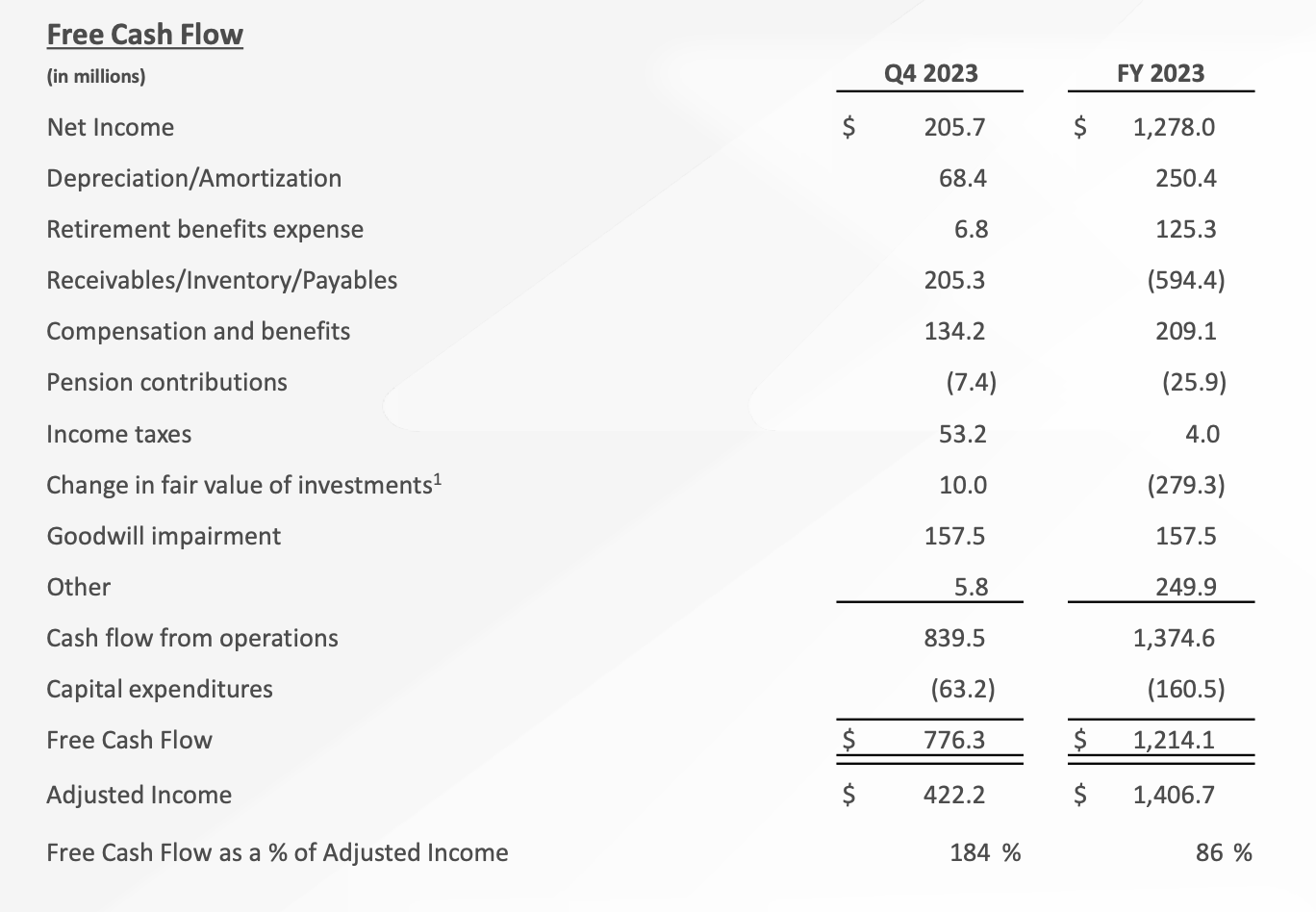

Rockwell maintains a strong balance sheet, providing financial flexibility to invest through business cycles. As of Q4 2023, the company had over $1.07 billion in cash against $2.8 billion in long-term debt. Importantly, Rockwell generates robust cash flow, reporting $1.2 billion of free cash flow in fiscal 2023. The company's net debt to EBITDA leverage ratio stands at a conservative 1.2x. Rockwell also has untapped capacity on its $1.5 billion revolving credit facility if needed.

{kind=link}

The company reported mixed fiscal Q4 2023 results on November 2nd. Sales rose 20.5% driven by easing component shortages, ahead of guidance. Signs of a slowdown were noted by management.

For full-year fiscal 2023, Rockwell posted healthy growth with sales up 17% and adjusted EPS up 28%. The company benefited from strong demand, pricing actions, and operating leverage.

Looking ahead, management issued downbeat guidance for fiscal 2023. They expect organic sales growth of just negative 2% to +4% and adjusted EPS of $12.00-13.50, up only 5% at the midpoint. Ongoing supply chain constraints and weakening demand, especially in China, led management to take a more cautious outlook. CEO Blake Moret mentioned in the Q4 earnings call: "While we saw strong sales growth in China in fiscal year '23, we continue to see high order deferrals and cancellations in China."

The demand slowdown is reflected in Rockwell's backlog, a key indicator of future business conditions. Backlog dropped to $4.1 billion exiting fiscal Q4. Management expects backlog will continue declining through fiscal 2024 as order weakness persists.

To offset demand challenges, Rockwell is pulling cost levers through workforce optimization and structural productivity actions. However, restructuring charges will pressure near-term earnings. Margin expansion may also prove difficult if volume deleverage persists.

Valuation

At ~$261 per share, Rockwell trades at a forward P/E of 20x compared to its 5-year average closer to 21x. The forward P/E premium relative to the broader market reflects expectations for above-average growth.

However, with end-market conditions deteriorating, risks are skewed to the downside. If the industrial economy continues slowing, Rockwell's multiple could contract even further. Bullish investors may point to Rockwell's solid balance sheet and strong cash flow generation as support, which is completely fair.

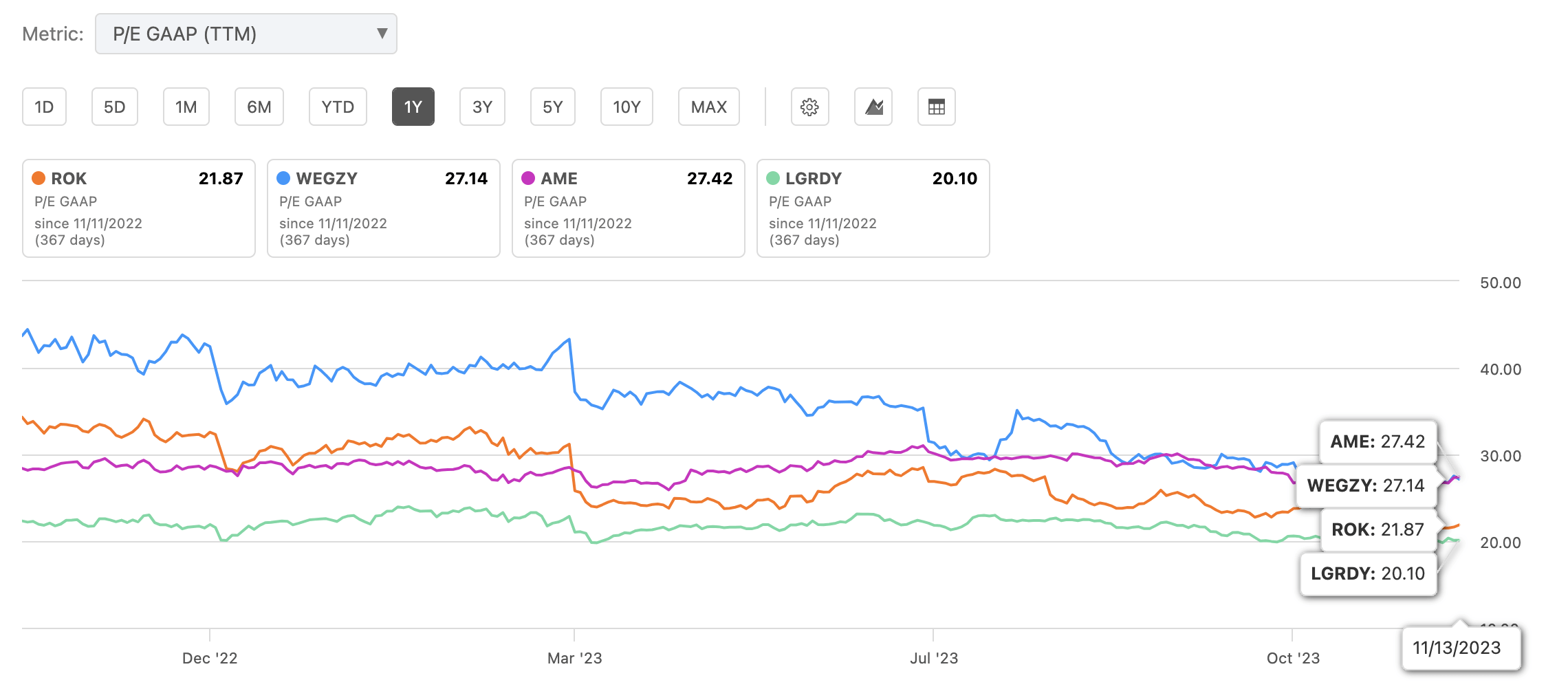

Rockwell also trades at the lower end of its peers on a trailing earnings multiple basis:

{kind=link}

Risks

The biggest near-term risk is that weakening industrial demand persists longer than expected. Lingering supply chain disruptions that constrain revenue growth would also pressure results.

Further order declines or cancellations from customers would likely lead management to take a more defensive posture on costs. This could restrict Rockwell's ability to deliver earnings growth in line with historical trends.

Over the long run, competitive threats remain a risk factor. Rivals like Siemens, ABB, and Schneider Electric are pouring money into industrial software and services to gain share. Pricing pressure or loss of key accounts would impede Rockwell's competitive position.

Macroeconomic risks such as a recession would almost certainly hamper results. Rockwell's automation investments are largely discretionary for customers during downturns.

Conclusion

Rockwell Automation possesses leadership positions in attractive industrial automation markets underpinned by secular growth drivers. The company is competitively advantaged with a broad solutions portfolio, extensive domain expertise, and high customer switching costs.

However, with slowing industrial growth and lingering supply chain disruptions, financial results are likely to disappoint over the next few quarters. The current valuation doesn't leave a lot of room for error and should be concerning especially given that there are clear signs of a slowdown.

Long term, Rockwell should benefit as factory automation adoption increases. But in the near term, exogenous risks are elevated. Waiting for a more compelling entry point seems prudent. The stock earns a Hold rating today.

For further details see:

Rockwell Automation: Turbulence Not Yet Priced In