RCKY - Rocky Brands: Quarterly Earnings Surprise Operational Synergies And Cheap

2023-11-16 00:08:19 ET

Summary

- Rocky Brands has potential operational synergies and cost savings opportunities, which could lead to free cash flow growth.

- The company has been selling off brands, which could increase cash or reduce debt.

- Expanding existing brands into new markets could also contribute to net free cash flow growth.

Rocky Brands ( RCKY ) recently announced potential operational synergies and cost savings opportunities, which may bring FCF growth. I would also expect further sales of brands, which may lead to cash increases or debt lowering. The company sold several brands recently. Additionally, further expansion of existing brands into new markets could also bring net FCF growth. I do see risks from changes in consumer preferences and competition, however I think that RCKY trades undervalued.

Rocky Brands

Rocky Brands, the leading designer, manufacturer, and marketer of premium footwear and apparel, operates notable brands such as Rocky, Georgia Boot, and Muck among others. Its focus on quality, comfort, and durability extends to six markets: outdoor, work, service, commercial military, military, and western.

{kind=link}

Its wholesale focus spans brands such as Rocky, Georgia Boot, Muck, and more, distributing to over 10,000 retailers in the US and Canada. Its internal and external sales force targets various accounts, such as Boot Barn and Dick's Sporting Goods, in segments such as outdoor, work, and military.

At the retail level, the company sells directly to consumers through websites, online marketplaces, and own stores. Outdoor gear stores in Ohio provide a product experience, and Lehigh's strategy drives transition to online sales, reducing brick-and-mortar stores.

The company successfully acquired Honeywell's sports and lifestyle footwear business, expanding its portfolio and presence. It reports segmented information and, following the acquisition, adjusted its segment structure to better reflect its approach and performance evaluation. The acquisition included goodwill close to $50 million and total identifiable assets of $215 million. Given the current market capitalization, I would say that there may exist certain undervaluation.

Source: 10-Q

It is a great moment for reviewing the company as recent quarterly earnings were better than expected. The company reported quarterly EPS of close to $1.09, which was better than expected, and revenue of $125 million.

Source: SA

Besides, I believe that the comments made by management in the last quarterly release were overall beneficial. Rocky Brands reported demand improvements, acceleration in at-once orders, and momentum for the year 2024.

Our quarterly performance saw meaningful improvement on a sequential basis as demand for our product improved, resulting in further reduced channel inventory levels and an acceleration in at-once orders from many of our key wholesale partners.

Looking ahead, we believe we are well positioned to improve on recent trends in the fourth quarter and begin 2024 with an improved balance sheet and good momentum across our business. Source: Press Release

Balance Sheet

As of September 30, 2023, the company reported cash and cash equivalents worth $4.24 million, trade receivables of about $97.844 million, inventories of about $194.734 million, and total current assets of about $309.445 million. The total amount of current liabilities was significantly lower than the total amount of current assets, so I believe that liquidity does not seem a problem. With that, in the last three years, the total amount of assets and liabilities decreased, which is not ideal.

With property, plant, and equipment of $53.124 million, goodwill stands at $47.844 million, and total assets were equal to $532.731 million. The asset/liability ratio is larger than one, so I would say that Rocky Brands remains healthy.

Source: 10-Q

I am not really concerned about the list of liabilities, however the total amount of debt is not small. Hence, I believe that studying carefully the total amount of debt and interest rate being paid appears reasonable.

Liabilities include accounts payable of $62.733 million, contract liabilities close to $2.99 million, and current portion of long-term debt of $2.704 million. In addition, long-term debt was equal to $211.19 million, with long-term taxes payable worth $169 million and total liabilities of $315.961 million. It is worth noting that the total amount of debt declined in 2023, 2022, and 2021. In my view, further decreases will most likely bring the interest of investors. At the same time, let’s keep in mind that net income appears to be increasing.

Source: 10-Q

As shown in the table below, Rocky Brands signed debt agreements with rates close to 7%, 5%, 6%, and 8%, but also close to 12%. With these figures in mind, I believe that the WACC in most financial models would range between 6% and 12%.

{kind=link}

Expansion Into New Target Markets With The Same Brands Will Most Likely Bring Net Sales Growth

I believe that the company will most likely seek to drive growth and increase its sales through a series of strategies. This includes expanding into new target markets with existing brands, introducing products with different features and prices. I also expect cross-selling of its brands at similar retailers, expanding its international presence through distributors, and strengthening its e-commerce, taking advantage of online shopping trends. The focus on Lehigh's business and its CustomFit platform seeks to capture opportunities in safety footwear programs.

Pricing Actions That Were Successful In The Past And Further Lower Logistics Costs Could Bring More Gross Margin In The Future

The company noted recent improvements in wholesale gross margin as a result of pricing actions and lower logistics costs. The company commenced to run operations many years ago.

Source: Ycharts

In my view, given the know-how accumulated by the company, economies of scale, and future pricing strategies, we may see further wholesale gross margin improvements.

The increase in Wholesale gross margin as a percentage of net sales was primarily due to the realization of pricing actions taken in the second half of 2022 as well as lower in-bound logistics costs compared to the year ago period. Source: 10-Q

Further Sale Of Assets Could Bring Cash In Hand

The company reported several sales of brands in 2023 and 2022. It appears that the total amount of debt is decreasing as a result of these transactions.

On March 30, 2023, we completed the sale of the Servus brand and related assets to PQ Footwear, LLC and PetroQuim S.R.L. Total consideration for this transaction was approximately $19.0 million, of which $17.3 million was received at closing. The remaining $1.7 million will be paid out in accordance with the purchase agreement. The sale of the Servus brand included the sale of inventory, fixed assets, customer relationships, trade names, and goodwill, all of which related to our Wholesale segment. Source: 10-Q

On September 30, 2022, we completed the sale of the NEOS brand and related assets to certain entities controlled by SureWerx pursuant to terms of an asset purchase agreement dated September 30, 2022. Total consideration for this transaction was approximately $5.8 million, of which $5.5 million was received at closing. Source: 10-Q

In my opinion, if the company continues to deliver successful sales of assets or brands, debt lowers, and revenue growth does not decrease, demand for the stock will most likely increase.

Restructuring Could Bring FCF Margin Growth

I also believe that the operational synergies and cost savings opportunities noted in a recent quarterly release could bring FCF growth. I would expect that investors will most likely notice this commentary, and may accelerate the demand for the stock. As a result, we could see stock price increases.

In September 2023, April 2023, and June 2022, we completed cost savings reviews aimed at operating efficiencies to better position us for profitable growth. We identified a number of operational synergies and cost savings opportunities, including a reduction in workforce. Source: 10-Q

EV/FCF, EV/EBITDA, And Price/Cash Flow Multiples

In the past, Rocky Brands traded at close to 8x and 9x, but also close to 15x FCF. I tried to be very conservative in my financial model. I used multiples of around 4x-8x, however investors may remember that the company traded at more than 9x.

Source: Ycharts

Seeking Alpha offers information about the sector. The sector median EV/EBITDA stands at close to 9x, the price/ cash flow is close to 8.9x, and the price/book is at 1.9x. According to SA, Rocky brands appears undervalued with respect to these multiples.

Source: SA

With The Previous Expectations And Assumptions, I Designed A Conservative Financial Model

My expectations include 2033 net sales of about $2.348 billion, with net sales growth of around 18% and 7% from 2024 to 2033. I also forecast 2033 cost of goods sold of about $1.515 billion, with gross margin of $832 million, and net income of $18 million, with net income / sales of 0.77%.

{kind=link}

With respect to the cash flow statement, I included 2033 depreciation and amortization of about $46 million, with stock compensation expense of about $3 million, and changes in receivables of close to $124 million.

Additionally, with contract receivables of about $2 million, changes in inventories of -$2 million, changes in accounts payable of -$146 million, and changes in contract liabilities of -$4 million, I also obtained 2033 CFO of $107 million and 2033 FCF of $85 million.

Source: CW

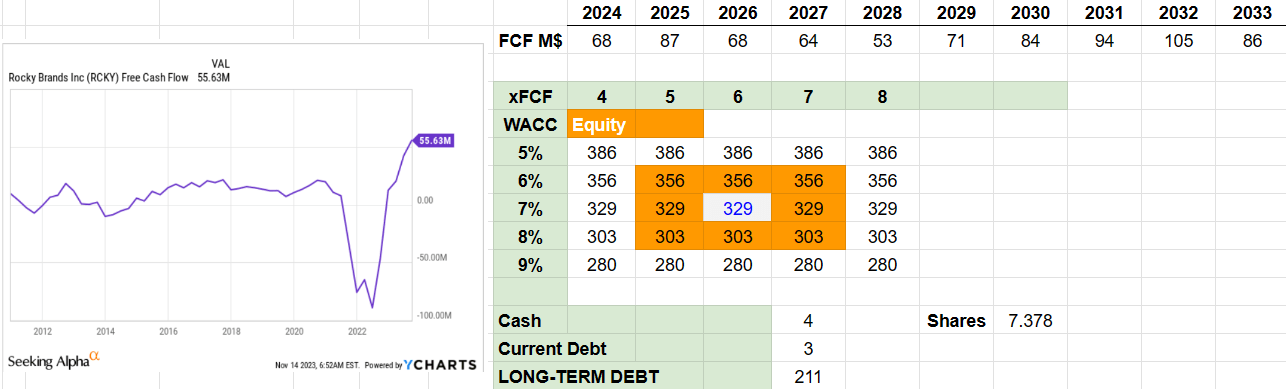

With FCF ranging from $53 million and $105 million from 2024 and 2033, cost of capital of 5%-9%, and EV/FCF of 4x-8x, I obtained an equity valuation close to $280 and $386 million. It is above the current market valuation.

{kind=link}

If we divide by the total amount of shares, the forecast price would stand at about $38-$52 per share with a median price of $44-$45 per share.

Source: CW

Finally, the internal rate of return would stand at close to 7%-15% with a median IRR not far from 11%. Other analysts may obtain different results with other assumptions, however given my results, I believe that most investors would see certain undervaluation.

Source: CW

Competitors

In my opinion, the environment is highly competitive, where factors such as design, quality, comfort, technology, brand recognition, and price are vital. Although the company’s strong brands and long-standing relationships with retailers make it effective, it faces competitors with more resources in finance, distribution, and marketing.

The footwear and clothing industry is changing, influenced by consumer preferences and fashion trends. Its success depends on anticipating and adapting quickly to changes in innovation, design, and trends to maintain consumer acceptance. Failure to do so could negatively impact company’s business and financial results.

Risks

In my opinion, the company's growth strategy is based on expanding its brands into new footwear and clothing markets. However, the success of new products is uncertain, and brands may lose popularity. If they do not anticipate changes in consumer preferences, planned growth and brand image may be affected. Introducing new products requires investment in marketing and development, which can increase operating expenses and affect cash flows. Production challenges and changes in priorities can impact development and manufacturing efficiency. Lack of acceptance of new products could damage profits, image, and competitive position in the long term.

My Opinion

Given the operational synergies and cost savings opportunities noted in a recent quarterly release, Rocky Brands may enter into the radar of new investors. In addition, with a significant amount of know-how accumulated for many years, I believe that further expansion of existing brands into new markets and products could bring net sales growth. Although its strong relationships with retailers and recent acquisitions strengthen its position, competition could also be a challenge. Besides, the company must anticipate changes in consumer preferences to maintain its position, and the debt levels could also be recognized as a risk. With all this being said, I believe that the company could be trading a bit undervalued.

For further details see:

Rocky Brands: Quarterly Earnings Surprise, Operational Synergies, And Cheap