RCKY - Rocky Brands: Weak Trade Trends And Pressure On Margins

2023-08-12 07:49:07 ET

Summary

- In the 2nd quarter of 2023, the company's revenue decreased by 38.4% YoY, while operating margin decreased to 2.2%.

- Pressure from macro headwinds and high inventory levels at the company's partners led to a 46% YoY decrease in revenue in the wholesale segment.

- I believe that pressure on both revenue growth and operating margin growth will continue in the coming quarters.

- In my opinion, the current valuation level according to the multiples is not extremely low to offset the associated risks.

Introduction

Shares of Rocky Brands (RCKY) have fallen 19% YTD. Despite the fact that the company's shares are relatively cheaply priced by multiples, and management is talking about a gradual normalization of partner companies' inventory levels, I believe that this is still not the best time to go long because, in my opinion, pressure on financial performance will continue in the coming quarters.

Investment thesis

In my personal opinion, in the next quarters of 2023, the company's revenue growth will continue to be under pressure, even if we see a decrease in inflation in the second half of the year, as real consumer incomes will be delayed. Moreover, I believe that a solid decline in revenue in the wholesale segment may have an adverse impact on the level of operating profitability due to a decrease in the scale of the business and the effect of deleverage, since a high share of operating expenses (logistics, rent, wages) is fixed. Also, I don't see any additional growth drivers/catalysts that could drive the company's share price higher.

Company overview

Rocky Brands designs, manufactures and sells clothing and footwear for men and women. The main sales channels are wholesale (72% of revenue) and retail (25% of revenue). The most famous brands of the company: Muck, Servus, XTRATUF, Ranger, Georgia Boot.

2Q 2023 Earnings review

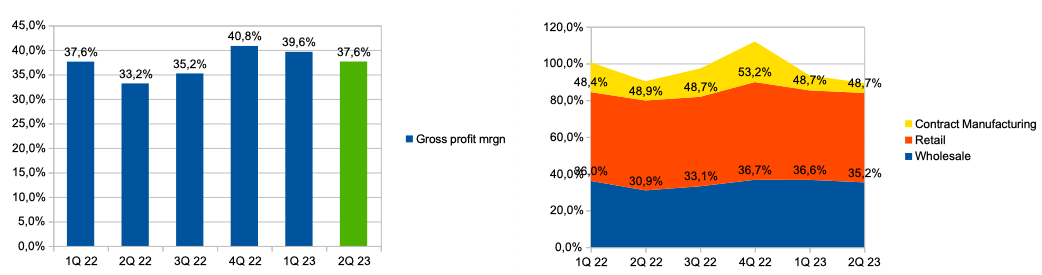

The company's revenue decreased by 38.4% YoY . The largest contribution to the decline in revenue was made by the wholesale segment, where revenue decreased by 46% YoY, while in the retail segment, revenue decreased by 3.6% YoY. The share of revenue attributable to the retail segment increased from 16.1% in Q2 2022 to 25.1% in Q2 2023. You can see the details in the chart below.

Revenue mix (Company's information)

Gross profit margin increased from 33.2% in Q2 2022 to 37.6% in Q2 2023 due to an increase in gross profit margin in the wholesale segment from 30.9% in Q2 2022 to 35.2% in Q2 2023 due to an increase in prices for the company's products. You can see the details in the chart below.

Gross margin & Gross margin by segment (Company's information)

{kind=link}

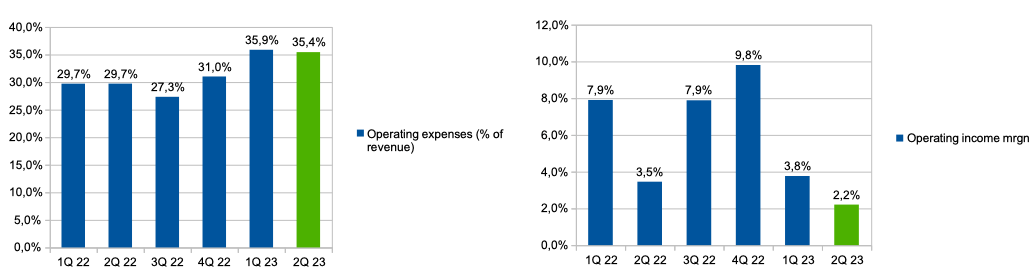

Operating expenses (% of revenue) increased from 29.7% in Q2 2022 to 35.4% in Q2 2023 due to the effect of deleverage. Thus, operating margin decreased from 3.5% in Q2 2022 to 2.2% in Q2 2023. You can see the details in the chart below.

Margin trends (Company's information)

{kind=link}

In addition, the company's management expects the company's revenue in 2023 to be about $470 million, which implies a decrease of 23.6% YoY. On the one hand, the company's expectations imply some improvement in revenue growth in Q3 and Q4 2023, but on the other hand, in my personal opinion, the current trading trends continue to look pessimistic.

My expectations

On the one hand, I like management's comments during the Earnings Call after the release of financial results that the company sees a gradual normalization of demand from partner companies, which should support wholesale revenue. However, on the other hand, I think that despite the fact that trading trends may improve relative to Q2 2023, the overall dynamics are still pessimistic.

Notwithstanding the slow start at-once orders improved month-over-month as the quarter progressed and this trend continued in July, providing a good start to Q3 and leaving us cautiously optimistic that channel inventories are getting properly aligned with demand.

First, I do not expect a quick recovery in consumer clothing spending, even if we see inflation slow in the second half of 2023, as consumers continue to face higher daily spending. In addition, a slowdown in trading trends could result in slower-than-expected destocking at partner companies, which could put pressure on top-line growth.

That said, the return to a more normalized wholesale order pattern will take longer to materialize than we expected on our last earnings call.

Secondly, I believe that the decrease in economies of scale and deleverage will continue to have a negative impact on the operating profitability of the business, since part of the operating costs for production, logistics, rent and wages are fixed.

Risks

Margin: decreased economies of scale, increased marketing costs, and the need to invest in prices to reduce inventory can all result in lower operating margins for a business.

Macro (general risk): high inflation and a decline in real income may lead to a reduction in consumer spending in the discretionary segment, which may have a negative impact on the company's revenue growth dynamics in the future.

Valuation

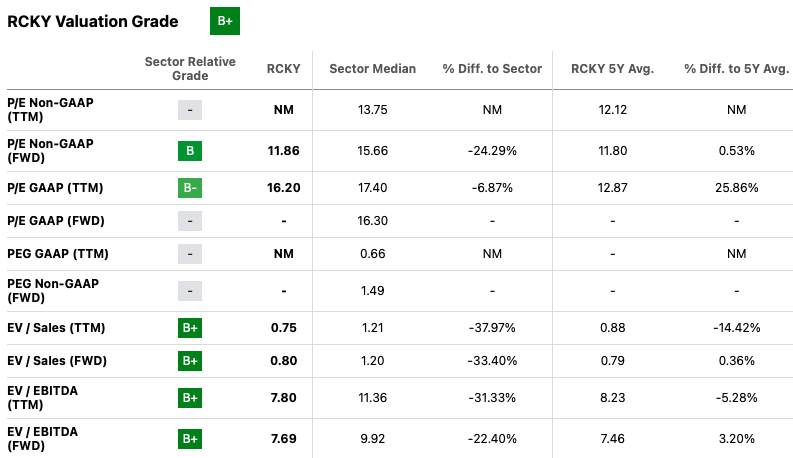

Valuation Grade is B+. On P/E ((FWD)) and EV/EBITDA ((FWD)) multiples, the company trades at 11.9x and 7.7x, respectively, which are 25% and 22% lower than the sector median, respectively. I believe that one should not make a purchase decision based only on a relatively low valuation, because: firstly, the company deserves a discount due to the high rate of decline in revenue, business size and relatively low level of profitability. Secondly, according to P/E ((FWD)) and EV/EBITDA ((FWD)) multiples, the company is still trading above the 5-year average by 1% and 3%, respectively.

{kind=link}

Conclusion

I think that in the coming quarters the company's financial results and share prices will continue to be under pressure, and I do not expect new drivers of growth, such as an increase in business growth or improved profitability. Besides, I don't consider the current valuation level according to multiples to be extremely cheap. I believe that investors should wait for the results for the next quarters before making a decision to buy shares. Thus, my recommendation is Sell.

For further details see:

Rocky Brands: Weak Trade Trends And Pressure On Margins