RCI.B:CC - Rogers Communications: Earnings Growth Encouraging But Concerns Remain

2023-03-09 05:10:15 ET

Summary

- Rogers Communications still faces uncertainty with respect to the Shaw merger.

- While earnings growth has been encouraging, RCI stock still seems expensive on this basis.

- I continue to expect modest growth in the short to medium term.

Investment Thesis

I take the view that growth will remain lacklustre until the eventual outcome on the Rogers-Shaw merger becomes more clear and earnings growth starts to rebound towards pre-pandemic levels.

In a previous article back in November, I made the argument that Rogers Communications ( RCI ) is unlikely to see a great deal of upside in the short to medium-term as a result of continued uncertainty over the Shaw acquisition as well as modest performance with respect to churn rates and ARPU (average revenue per user).

The stock has climbed by just under 3% since my last article.

{kind=link}

The purpose of this article is to assess whether Rogers Communications could expect renewed upside going forward on the basis of most recent quarterly performance.

Performance

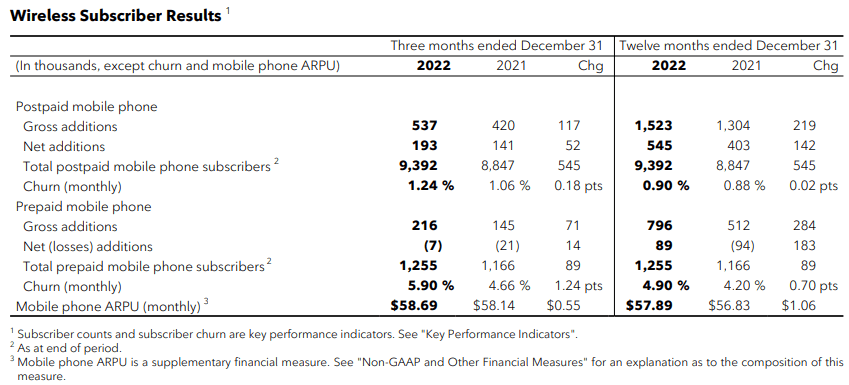

With regards to recent quarterly performance , we can see that while mobile phone ARPU is up by $1.06 on a twelve-month basis - churn on a postpaid basis is up slightly from 0.88% to 0.90% over the same period, with a higher jump of 4.20% to 4.90% on a prepaid basis.

Rogers Communications: Fourth Quarter and Full-Year 2022 Results

{kind=link}

With respect to the latter - higher churn rates mean that a higher proportion of customers are choosing to cease using services from Rogers. While prepaid churn is up significantly as compared to postpaid - I do not see this as a big concern given that postpaid mobile phone subscribers make up the majority of mobile phone customers for Rogers outright.

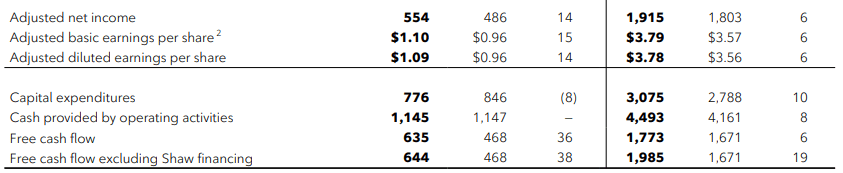

Moreover, the company's growth in free cash flow continues to remain impressive. We can see that while capital expenditures in the most recent quarter were up by $776 million with a significant increase in network infrastructure as compared to the five-year average - free cash flow was also up by 36% over the same period, with a 6% increase on a 12-month basis as compared to last year:

Rogers Communications: Fourth Quarter and Full-Year 2022 Results

{kind=link}

The deadline for the merger between Rogers and Shaw Communications ( SJR ) has been extended for a fourth time until March 31 for final approval. With the deal having come under significant scrutiny from regulatory authorities, Rogers and Quebecor ( OTCPK:QBCRF ) have been considering lowering roaming rates for Freedom Mobile customers who roam on the Rogers network - with a view to avoiding the appearance of anti-competitiveness in this regard and ultimately allow the merger to proceed.

Roaming has traditionally been a significant revenue generator for mobile phone companies. With this revenue stream having come under pressure during the pandemic to lower levels of international travel as well as regulatory changes mandating that customers have the right to have their handset unlocked free of charge - a further reduction of rates is likely to place further pressure on this segment.

From this standpoint, continued uncertainty over the merger has continued and Rogers has already had to make significant compromises to gain approval for the deal.

Looking Forward

Going forward, while continued uncertainty remains over the Rogers-Shaw merger, Rogers has shown resilient performance in terms of growth in revenues, earnings and free cash flow.

The main risks that I see to Rogers Communications at this time include further delays on a merger decision - potentially impacting investor confidence in the stock. While recent quarterly results have been encouraging - inflationary pressures as well as potentially lower roaming charges to allay merger concerns surrounding anti-competitiveness could place downward pressure on revenues.

ycharts.com

Additionally, we can see that while earnings (on a normalized diluted basis) have seen seeing a steady recovery since 2020 - the company's P/E ratio still remains significantly above levels seen before this period - indicating that the stock might still remain overpriced compared to the pre-pandemic period.

Conclusion

To conclude, Rogers Communications has shown resilient growth in earnings and cash flow. However, I take the view that growth will still remain lacklustre until the eventual outcome on the Rogers-Shaw merger becomes more clear and earnings growth starts to rebound towards pre-pandemic levels.

For further details see:

Rogers Communications: Earnings Growth Encouraging, But Concerns Remain