RCI - Rogers Communications: Growth In ARPU And Lower Debt Leverage Ratio Encouraging

2023-11-27 02:03:22 ET

Summary

- Rogers Communications has shown strong growth in revenue and earnings, driven by the acquisition of Shaw Communications.

- The increase in postpaid churn has led to a decline in customer lifetime value.

- That said, higher churn is not unique to Rogers and reflects increased competition across the industry more generally.

- Given continued growth in ARPU, I continue to take a bullish view on Rogers Communications stock.

Investment Thesis: I continue to take a bullish view on Rogers Communications given continued growth in ARPU as well as a reduction in the company's debt leverage ratio.

In a previous article back in July, I made the argument that Rogers Communications ( RCI ) has the capacity for further upside from here, given strong customer lifetime value (LTV) performance, as well as continued earnings growth.

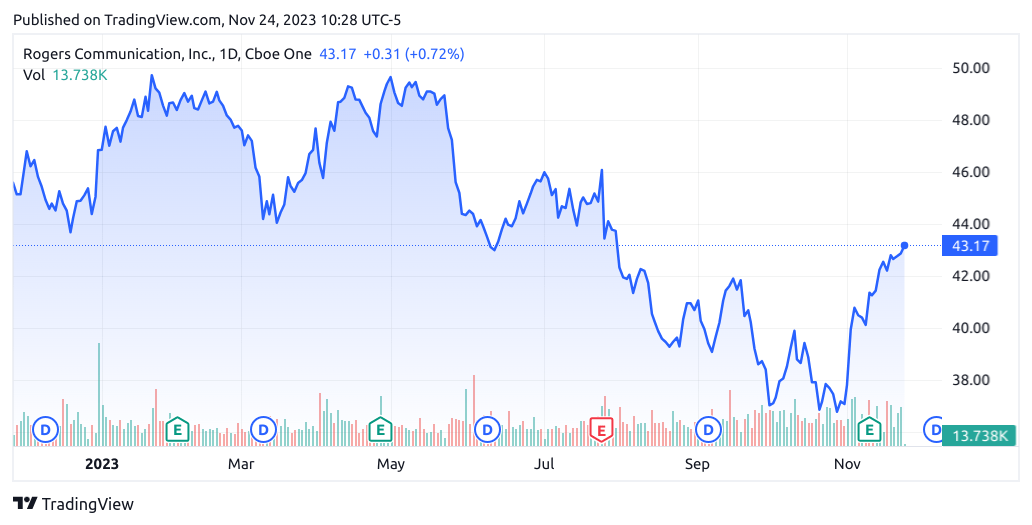

Since then, the stock has descended slightly to a price of $43.17 at the time of writing:

{kind=link}

The purpose of this article is to assess whether Rogers Communications has the ability to see continued growth from here taking recent performance into consideration.

Performance

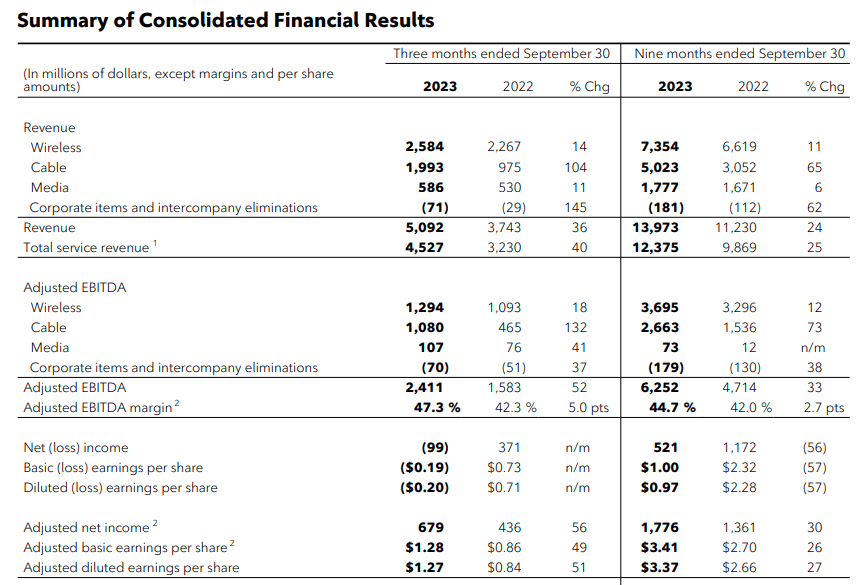

When looking at Q3 2023 earnings results for Rogers Communications (as released on November 9 2023), we can see that both revenue and earnings per share showed strong growth from that of the prior year quarter.

Rogers Communications: 2023 Q3 Earnings Press Release

{kind=link}

However, these results are significantly influenced by the acquisition of Shaw Communications, with cable service revenue seeing an increase of 105% this quarter primarily as a result of the acquisition. Additionally, Rogers Communications saw an increase in its debt leverage ratio to 4.9x on an adjusted basis as a result of the acquisition. However, this is still down from that of 5.1x on an adjusted basis for Q2 2023 , and the company is targeting a ratio of 4.8x by the end of this year.

I had previously made reference to the fact that LTV (or customer lifetime value) for Rogers Communications has shown significant upside over the past few years - indicating that the total revenue an average customer brings in over the lifetime of their contract with Rogers is increasing.

Here is a breakdown of LTV by quarter across the postpaid segment for Rogers Communications. Customer lifetime value across the postpaid segment was calculated as ARPU / postpaid churn rate (%). We can see that LTV has declined in Q3 2023 as compared to the prior year quarter:

LTV calculated by author using ARPU and churn statistics from historical quarterly reports for Rogers Communications. Heatmap generated by author using Python's seaborn visualization library.

The reason for the decline in LTV has been due to higher churn. For instance, ARPU (or average revenue per user) came in at $58.83 for this quarter as compared to $56.82 for Q3 2022. However, churn was 1.08% for this quarter as compared to 0.97% for the prior year quarter. From this standpoint - while growth in revenue has been encouraging - this is being eroded to a degree by a higher rate of churn.

From a balance sheet standpoint, we can see that while long-term debt and total assets have both seen significant increases (in millions of Canadian dollars) resulting from the Shaw acquisition - the long-term debt to total assets ratio itself has remained virtually unchanged - indicating that Rogers Communications has not seen any particular increase in long-term debt in its own right:

| Sep 2022 |

| Sep 2023 |

| Long-term debt |

| 31550 |

| 41345 |

| Total assets |

| 54783 |

| 71778 |

| Long-term debt to total assets ratio |

| 57.59% |

| 57.60% |

Source: Figures sourced from Rogers Communications Q3 2022 and Q3 2023 Press Releases. Long-term debt to total assets ratio calculated by author.

My Perspective and Looking Forward

As regards my take on the above results and the implications for the growth trajectory of the stock going forward, I take the view that while the growth in ARPU that we have been seeing across the Wireless segment has been encouraging - the increase in postpaid churn has been leading to lower LTV - and this could hinder overall revenue growth in the longer-term.

In this regard, I believe that the company needs to demonstrate an ability to reduce churn rates across its postpaid segment going forward - in order to fully capture the value from the growth it has been seeing in ARPU.

With that being said, the increase in churn has not been unique to Rogers, as competitor Bell Canada ( BCE ) has also seen an increase in churn to 1.1% in the most recent quarter as compared to 0.9% in Q3 2022. The company cites greater competitive activity in the market as well as promotional offer intensity as compared to last year as a leading reason behind the increase in churn rates.

Additionally, the company also saw mobile phone blended ARPU down 0.2% to $60.28 from $60.39 in the prior year quarter, which was a reflection of lower overage revenue resulting from customers subscribing to unlimited plans.

In this regard, I take the view that Rogers Communications continues to have the capacity to compete effectively in its marketplace - in spite of higher churn rates which are increasing competition across the industry as a whole at this time.

Risks

In terms of the potential risks to Rogers Communications at this time, increased competition in the marketplace and rising churn may be a concern going forward if we continue to see a decrease in LTV.

However, as has been established - higher churn rates are not unique to Rogers Communications and we have been seeing increased competitive activity across the Canadian telecommunications industry as a whole.

In this regard, I take the view that Rogers has the capacity to bolster LTV in Q1 and Q2 2024 once again in line with traditionally higher seasonal LTV levels as we have seen over the past five years.

Conclusion

To conclude, Rogers Communications has seen significant growth in revenues and earnings resulting from the Shaw acquisition and the fact that the company has been reducing its debt leverage ratio has been quite encouraging. Based on these factors, I continue to take a bullish view on Rogers Communications.

For further details see:

Rogers Communications: Growth In ARPU And Lower Debt Leverage Ratio Encouraging