PLAB - Rogers Corporation: I Bought Did You?

Summary

- My last article on Rogers Corporation was about a look at an undervalued business after a failed M&A. The market pushed the company down to unrealistic levels.

- My stance was "BUY" - and the result, as expected, was market outperformance in a short time.

- What wasn't expected was how short a time it could generate those returns. So, in this article, I am updating my thesis for Rogers for 2023.

Dear readers/followers,

Back when the Rogers Corporation (ROG) deal with DuPont (DD) fell through , the company was not a popular stock to write on. In fact, when I wrote about Rogers, it had been uncovered for several months, despite the fact that I felt that a crash in the share price should have brought more coverage , not less. However, no harm was done. I'm happy to take advantage of under-coverage and provide my spin on things.

In this case, I was happy enough to load up with a 0.4% in Rogers, which I've kept until today. This makes me a very happy investor. Why?

Rogers Corporation Article (Seeking Alpha)

Now, one thing first. You may not feel that when you invest a small amount of money and that rises 27.85% in less than 3 months, this is a great achievement. Let's say you invested $1,000, which is a lot of capital to most of my readers. Even if we annualized those returns, it's hard to get excited with the resulting amount of cash. However, investing is really all about percentages. Many years ago when I started out, and a 27.8% RoR on a 0.4% investment out of my portfolio wasn't much to crow about, I felt similar.

However, I was keen on value investing very early. And I can tell you that in the long term, if you keep compounding and keep following very simple and actionable rules in your investing, you'll eventually come out on top. Today, 0.4% of invested capital is a lot more for me - and so the percentage returns of 27.85% in that short time are impressive as well.

So, even if you just invested $100 into the company, be proud of the RoR you managed here - because the performance is very much repeatable.

Back to Rogers.

Updating on Rogers Corporation

It's no secret that I like to "play" with the market's tendency to overreact on companies and events. I often buy investments after a very bad day, or sell them if they become, as I see it, overvalued during a very good day. I have added to this with my newer approach of allocating 10-15% of my portfolio towards options as well - because volatility lends itself extremely well to selling options.

Market overreaction is your friend, even if like, in this case, Rogers isn't a dividend-paying company that I usually look at. When I looked at it, though, I felt that the upside I saw, especially just normalization, was very much worth it.

Because this company has something that others sometimes don't. Rogers Corporation has consistently outperformed the market, generating solid results on good operations.

ROG IR (ROG IR)

With its two synergistic segments - Advanced Electronic Solutions as well as Elastomeric Material Solutions - Rogers Corporation is in a very good position to be among the market leaders in material sciences.

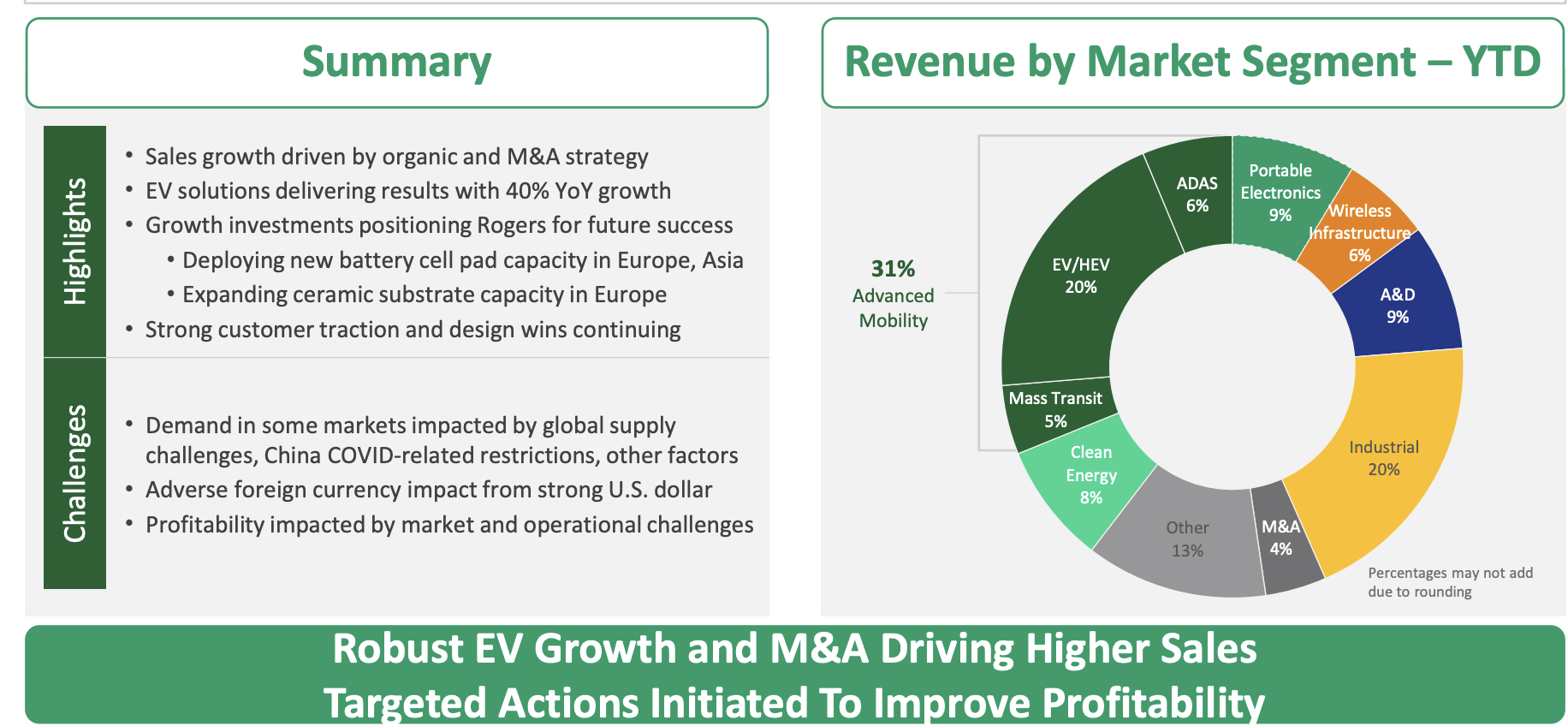

Rogers is a net beneficiary of the ongoing electrification trends and advanced driver assistance system as well as increased use of smartphones and advanced telecommunication systems. In addition, company output/products are being used in general industrial, aerospace and defense, mass transit, clean energy, and connected devices.

This is not some unknown or fading company, but a future necessity for many segments. The company sees the potential to essentially double its sales revenues over a coming 5-year period based on the current EV/HEV and ADAS trends - this is not based on company forecasts, but third-party forecasts outside simple total addressable market ("TAM") models.

Now, the proposed merger was supposed to increase these synergies , but this did not happen - and it's very good for Rogers shareholders that invested after the fact, like me. Because we were able to capitalize on a company with incredible quality at very cheap pricing.

Rogers makes money by researching and designing as well as manufacturing these crucial materials, and they sell to customers in NA and EMEA. The company competes with other engineered materials manufacturers. Generally speaking, there's a very high degree of specialization in these segments, which makes specific peers hard to find. Some that I was able to identify are Photronics ( PLAB ), Corning ( GLW ), and Coherent ( COHR ). While Corning is larger, the company isn't in exactly the same areas either.

So it's a fairly tight peer group - and while Rogers isn't necessarily the absolute market leader here, it's no slouch.

In my original article, I went through a bit in terms of the sales model and how the inventory/cash conversion cycle flows. The disadvantage for Rogers is that they have no control over the cancellation, and penalties for cancellation are difficult to impose, which means that Roger's backlog isn't as indicative of their future sales and cash flows as other companies might be.

But with the way the company is specializing in terms of segments, I expect cancellations to be smaller in number, due to the increasing shift towards electric vehicles ("EVs"), and Roger's role in this shift due to their operational segments.

ROG IR (ROG IR)

Remember, results so far for 2022 have been absolutely solid. Sales in EVHEV, Defense and portable electronics made sure that 2Q22 was positive. We have 3Q22 numbers as well, by the way, and those aren't bad either (as evidenced by how the share price has developed). The company posted YTD9M in December, and these are the results.

{kind=link}

I don't do strong statements often, but I'll do one here - in that if you didn't capitalize on Rogers, you probably made the wrong choice. The valuation the company was trading at did not make sense, even given the headwinds from the failed merger. Rogers has operational excellence in many of its sectors, and even if am personally not a fan of the EV options currently on the market, I can see this market accelerating in the near future. ADAS outlook is superb, with over 230M sensors expected in automobiles in 2026, compared to 142M in 2021. The company is a global business with a very solid manufacturing and research base - globally.

{kind=link}

And after the failed M&A, Rogers is moving forward on its own, doing M&As and new plans for the future. Revenue for 3Q22 is up nearly 6.5%, with 16.9% growth in EMS growth. Gross margins are down somewhat - Rogers isn't immune to FX, mix, or underutilization due to SCM and other headwinds, as well as investments and the like. Operating expenses are up, and from a high level, the trends in terms of earnings don't look perfect at this time. The company is to focus on driving organic growth on the back of strong trends, paying down debt, doing more synergistic M&A's, and returning capital to shareholders in the form of share buybacks. Rogers Corporation has also announced, aside from those buybacks, the potential of even paying a dividend (at least indirectly, in "returning excess cash to shareholders).

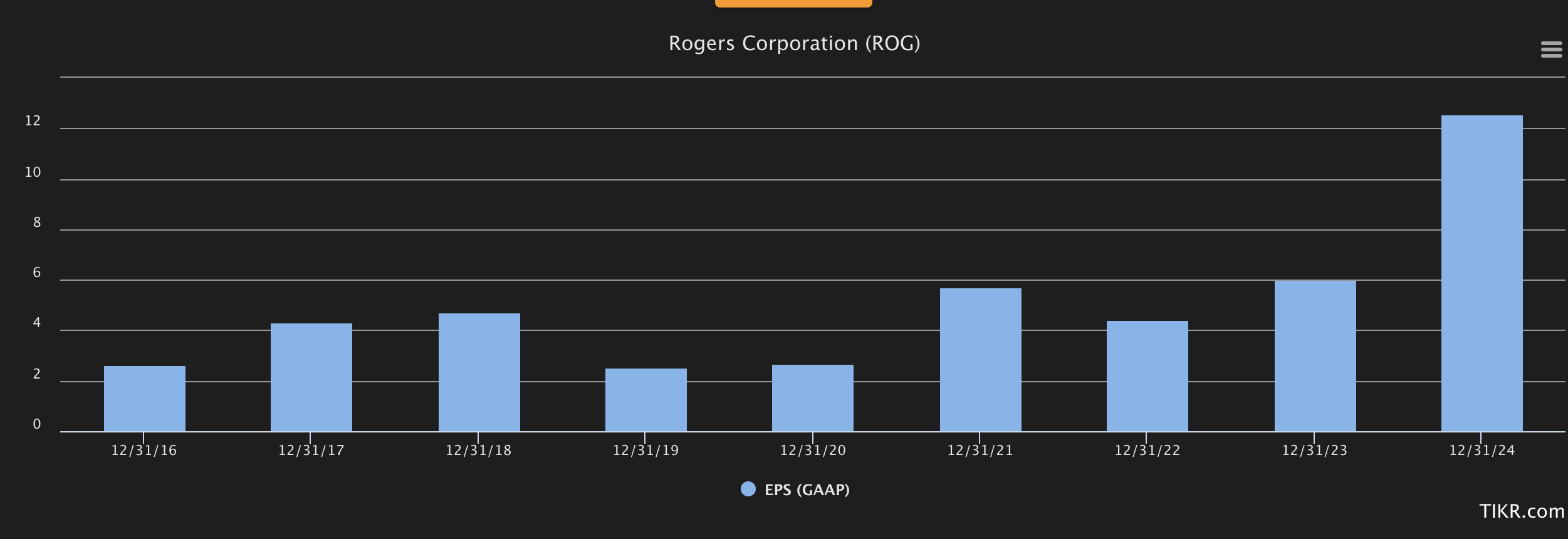

I forecast that operating margins for Rogers will be impaired for some time, as they are in other places and companies - so don't expect these to disappear in the near term.

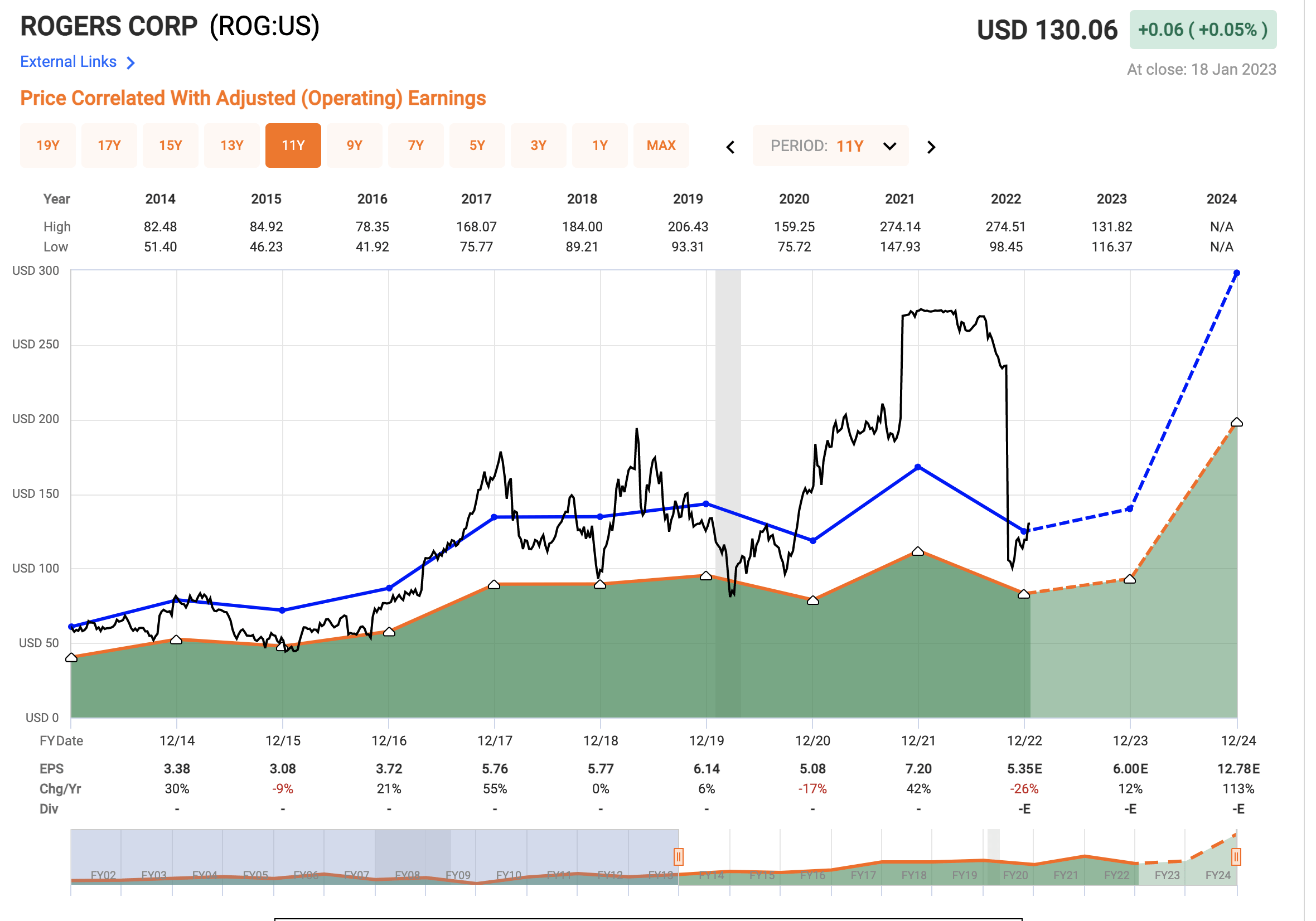

Take a look at the current forecast for GAAP earnings for the company. While we may put into question 2024E, the company's trajectory is not really in question - dipping this year, recovery, and operational efficiencies following.

{kind=link}

With this in mind, let's look at current valuation trends.

Rogers valuation - not a difficult prospect

Rogers Corporation is an exercise in valuation. The company has no dividend, which means that the company is free to reinvest the entirety of its free cash flow into the business, which theoretically should enhance the return on equity for shareholders - like ourselves if we own shares. While 2022 his very likely to be a drop, the same trend can be forecasted here at FactSet.

{kind=link}

You also shouldn't have a hard time seeing why I thought this company was a valuation opportunity only a few months back.

{kind=link}

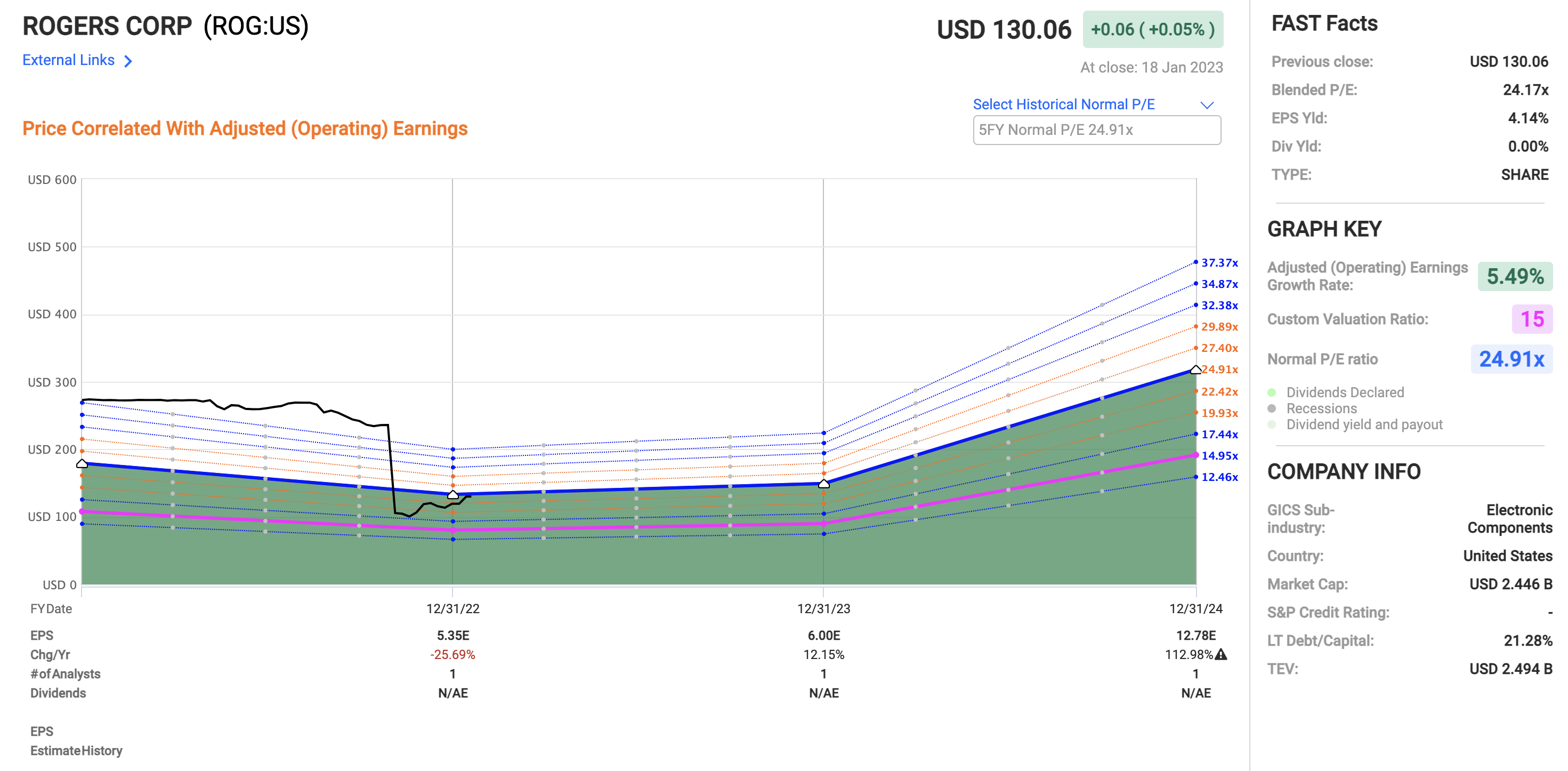

ROG is a textbook volatile stock that typically trades at a very high premium - not undeserved, given its operations, but perhaps undeserved given its recent results, excluding 2021. This premium as you can see is fairly well-established over time. We should view it as fairly reasonable for the growth that this company can deliver, at least potentially. In my last article, I made a case for forecasting the company at around its premium, with the expected RoR even without a dividend, becoming fairly interesting.

You can even begin at a 15x forward P/E, even after the company's recent bout of outperformance, and come to annualized RoR of 22%, or 47% until 2024. That's with a very positive 2024E, but there's some reason to believe that the company will be at least able to post impressive returns for this year, which leads me to forecast the company at least at 15-17% annualized at this point.

Now, I've already made a very decent 20%+ RoR in a very short time. In fact, annualized over the timeframe, my investment in Rogers has generated annualized RoR of 166.76%, which is very nice. At this point, I could step out of the investment - but I don't yet feel that Rogers has really hit its stride. We've only begun to see a normalization of this valuation at this particular time.

Rogers Corporation remains very underfollowed by analysts - both here on Seeking Alpha and outside of SA. There's only one analyst following the company following the merger announcement, and that one still has the price target ("PT") from the merger - meaning at this time, we really can't focus on what analysts say about the company. The last non-merger-impacted PTs call the company a "BUY" with a $277/share PT, which is nonsensical. I don't agree with this PT. To my mind, the company is worth a normalized premium of its 5-year average, or even a normalized 15X P/E. In my last article, I gave Rogers a PT of $150 on a per-share basis.

I'm not moving from this PT at this particular time. $150/share is my long-term target. This incorporates a decent upside for the next 3 years of where the company might go as a stand-alone business.

The latest deal by DD proposed for ROG was too expensive and outsized by half. DuPont shareholders like myself can thank their lucky stars that it didn't actually go through, because 35-45x P/E is not a fair valuation for Rogers corporation. It never was - it's not at this time either, and I can only hope that DD exercises better due diligence in the future when going for deals.

However, for the time being, I'm grateful for the opportunity, because it means that I'm able to generate these sort of returns. I'm not shifting my target, so this is my current thesis.

Thesis

My thesis for Rogers is as follows:

- This is an undervalued play following a failed merger with DuPont, in specialty materials and engineered components/substrates for various attractive end uses and industries. This sort of company typically deserves a premium - and if the company had had size, a credit rating, and yield, it would have deserved more.

- As it stands, I'm willing to give the company a 15x normalized P/E as an introductory price target. This comes to a PT of $150/share.

- I, therefore, start out here with a bit of a speculative "BUY" rating, one that I believe warrants your attention. Still, be aware of the drawbacks of Rogers, because it lacks some things you might want.

Remember, I'm all about :

1. Buying undervalued - even if that undervaluation is slight, and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn't go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them ( italicized ).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

I'm not going to call Rogers Corporation "cheap" any longer, but I do think it's a solid "BUY" here based on it fulfilling 3 out of 5 important criteria here, and being a qualitative, proven business.

I remain LONG the company.

For further details see:

Rogers Corporation: I Bought, Did You?