ROG - Rogers: High Multiples Flat Economic Performance Rated Hold

2023-09-29 23:40:00 ET

Summary

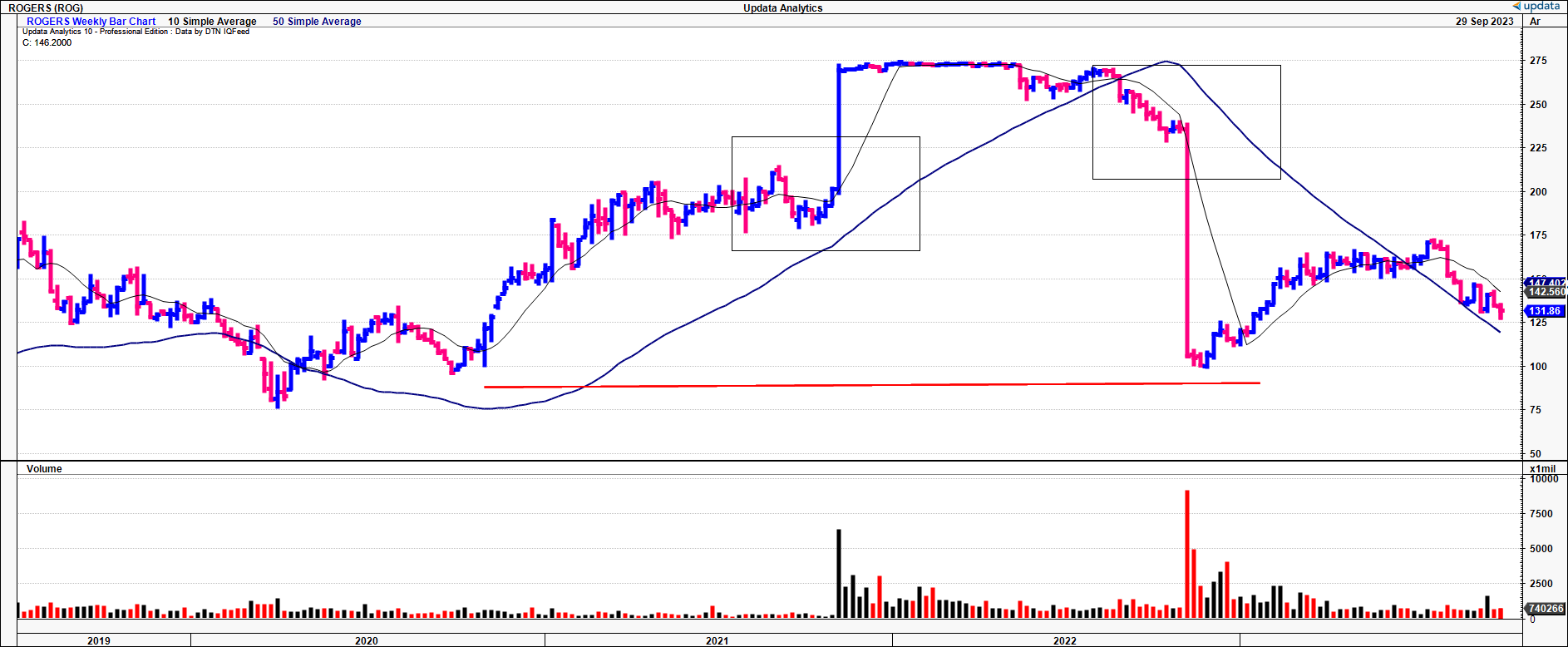

- Shareholders of Rogers Corporation have experienced a difficult period, with the stock price dropping from highs of $275 to $131.

- The planned acquisition by DuPont fell through due to Chinese antitrust approval issues, resulting in a sharp selloff.

- With uncertainty still on the table, and the stock trading at high multiples, I rate ROG a hold.

Investment summary

Shareholders of Rogers Corporation ( ROG ) have endured a difficult period over the last 2 years. In the investment context, the outlook on its share price is still uncertain based on a number of factors.

In short, ROG's stock was dumped from its highs of ~$275 across 2021–'22 to now trade at $131 as I write. It had held that $270 range for around 1 year, until November '22, when DuPont de Nemours (NYSE: DD ) made the decision to abandon its planned $5.2Bn acquisition of the company. This came after months of antitrust review issues with Chinese regulators. After further negotiation, ROG then said it wanted to be a standalone company, affirming that "the strength of Rogers as a standalone business is undeniable".

Specifically, the deal fell apart as the companies couldn't secure Chinese antitrust approval within the specific timeline ending November 1st 2022. DD paid ROG a regulatory termination fee of $162.5mm ($8.70/share) to walk away, after it had originally offered to buy the company for $277 per share.

By February, activist investor Starboard Value revealed that it had (i) acquired a significant stake in ROG and (ii) announced its plans to push for changes within the board. ROG's share price had dropped by ~36% at the time. That wasn't really a large catalyst, as evidenced on the chart. By August, Starboard had reduced its holdings from 1.03mm shares to 774,000 shares. Not a positive implication for the stock's recovery. You can see on the charts the market's violent reactions over the whole time in Figure 1. There was a small recovery at the end of 2022 into 2023, but nothing back to previous highs.

Based on the factors raised in this report today, I rate ROG a hold for now. This is based mainly on valuation grounds, but also on a number of economic factors.

Figure 1.

{kind=link}

Critical facts pattern underlining hold thesis

1. Fundamental catalysts and economic value

- Fundamental factors

The company's most recent quarterly sales were $231mm, down 530bps on Q2 last year, and up from Q4 $210mm in 2020. It pulled this to an operating margin of 12%, after it gained 200bps of gross margin over the 12 months. Management are looking to $240mm in sales next quarter on earnings of $1.25, both at the upper end of range.

Segment wise:

(i). Its advanced electrics ("AES") segment did $130mm of business and was down ~4% YoY. Aerospace + defense sales were strong, a trend that's been consistent across industry in FY'23.

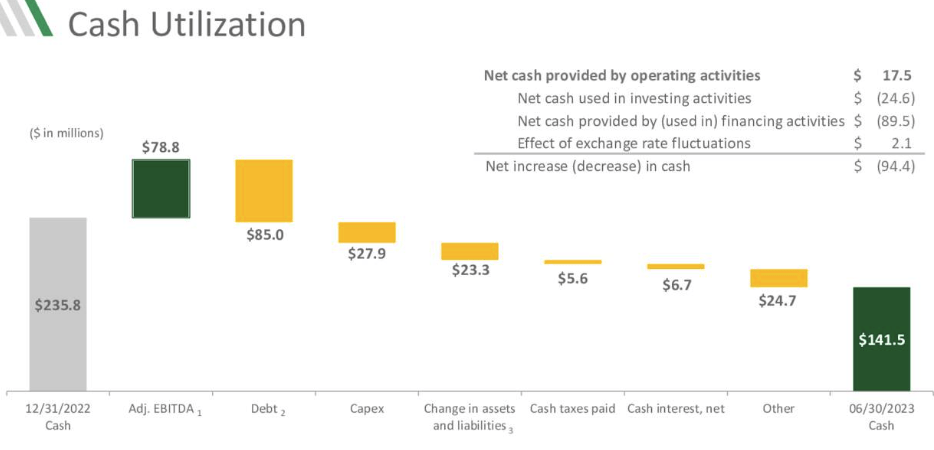

(ii). Elastomeric material revenues were also down ~6.7% YoY to $95.3mm, given a slowdown in ROG's end markets. Critically, this is the 3rd sequential quarter where ROG's key numbers have decreased, and both cash flows and earnings have been lumpy as a result. From Q2 FY'22-'23, the company's cash burn was $94mm, a large portion committed to paying down debt, and $28mm invested into CapEx. It left the 2nd quarter with $141mm in cash.

Figure 2.

Source: ROB Q2 Investor Presentation

{kind=link}

As for the challenges moving forward, management explained on the earnings call what's in sight:

- An overall decline in manufacturing activity in most of its markets.

- Inflation/rates a major factor in this, from production to consumer level.

- Some of its EV customers have " delayed production ramps".

This is a reasonable set of expectations in my view, so it's all about cash flow moving forward. Given the company's tightening set of cash flows in the last few quarters, cash on hand has been tracking lower, whereas NWC working capital requirements have increased from $111.5mm in 2020 to $464mm in Q2. So in my opinion keep a close eye on operating cash flow and the net change in cash each quarter moving forward, as this trend needs to reverse.

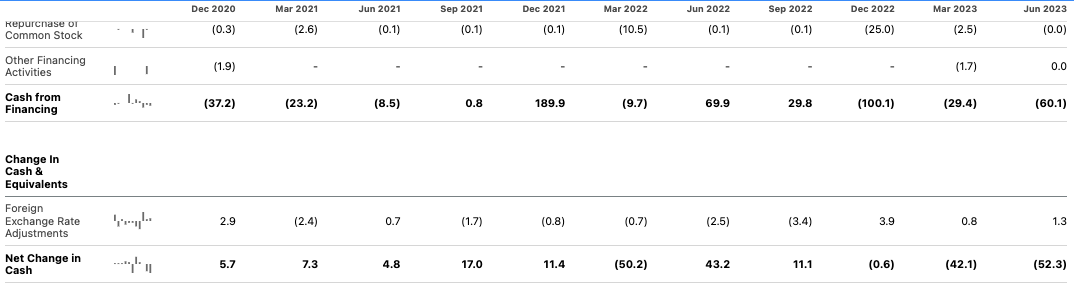

Figure 2(a). ROG change in cash on hand, quarterly, Q4 2020–2023

{kind=link}

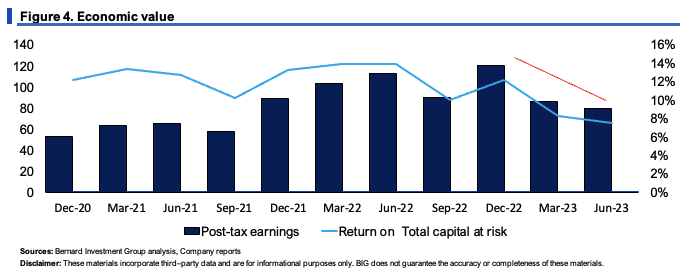

- Economic value

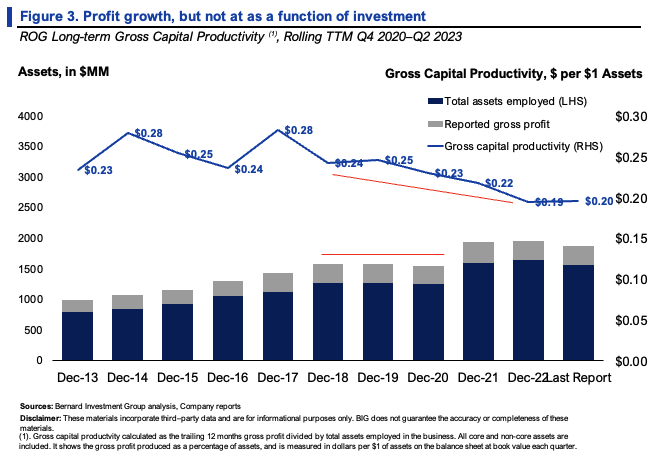

Looking back over the last decade, the company's gross profits have grown at a reasonable rate each year. At the same time, ROG also requires more assets to maintain its competitive position. Despite the reported growth, as a ratio of gross profits to total assets employed, things have been tightening up over the last 6 years. The company has gone from producing $0.24–$0.28 in gross for every $1 of assets employed, to $0.20 on the dollar in the last 12 months.

{kind=link}

In more recent times, two critical factors stand out:

(1). The return on capital invested by the business to support growth and increase its competitive position (economic value).

(2). Where this surplus cash has been deployed.

Figure 4 is split into the two graphs below. The first shows the company's economic value, measured by returns on investment from 2020–'23 on a rolling TTM basis. Here, we'll treat the company as a fellow investor. As you can see, the company had been growing steadily until Q1—Q2 this year. Profits have since tightened as a function of capital required to operate, and this could be a risk to longer-term business growth.

{kind=link}

The second chart of Figure 4 shows ROG's value drivers for the last 3 years. Sales growth has been reasonably high, compounding at ~6% each period over this testing period. Margins have been stable at ~14%.

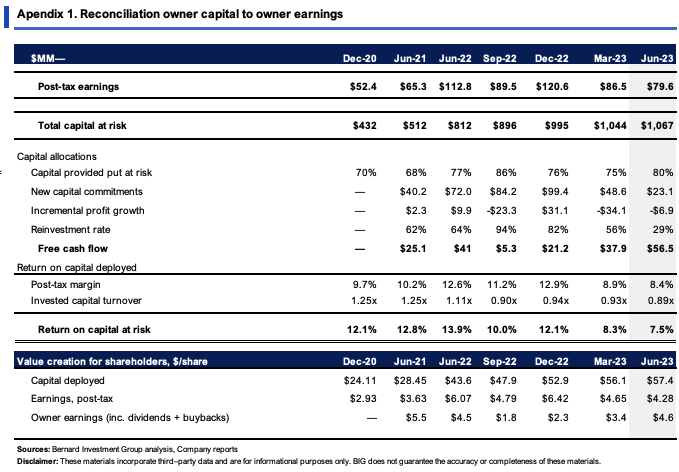

For every $1 of new sales in this time, the company had to invest $0.94 to support the growth, $1.55 when including M&A activity. This is something to consider. A major part of this is because capital turnover is less than 1x sales and post-tax profit margins were 8% last period. Critically, if it continues at this rate, $1 in sales growth will require (i) high reinvestment back in the business, (ii) at a declining rate of return on these investments, reducing the present value of the future cash flows. The full breakdown is observed in Appendix 1.

BIG Insights

Technical factors to consider

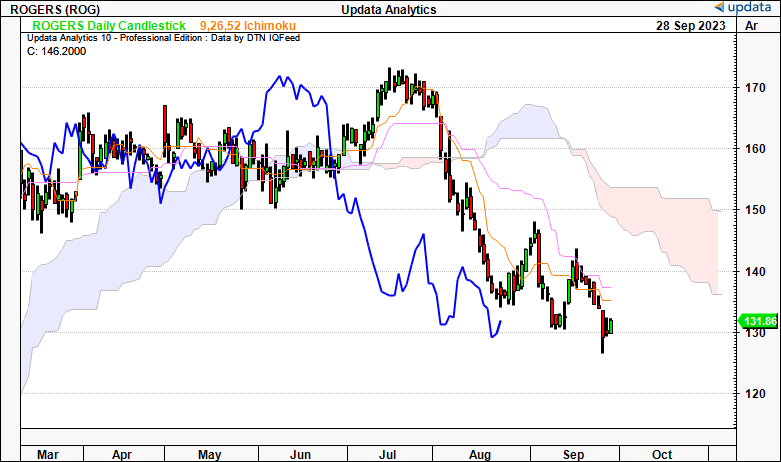

Figures 5 and 6 show a longer-term chart appraisal using daily and weekly cloud charts.

Figure 5. Daily cloud chart

- ROG congested sideways for the good part of 5 months in '23 after it all went down with DD. It then crossed to the downside, after 1) softer earnings, 2) the starboard exit, and 3) broad market weakness. A target $151 by October is the level for the price and lagging line to cross for a bullish view.

- Until then, continues to look for a bottom and uncertain to say where it will find one.

{kind=link}

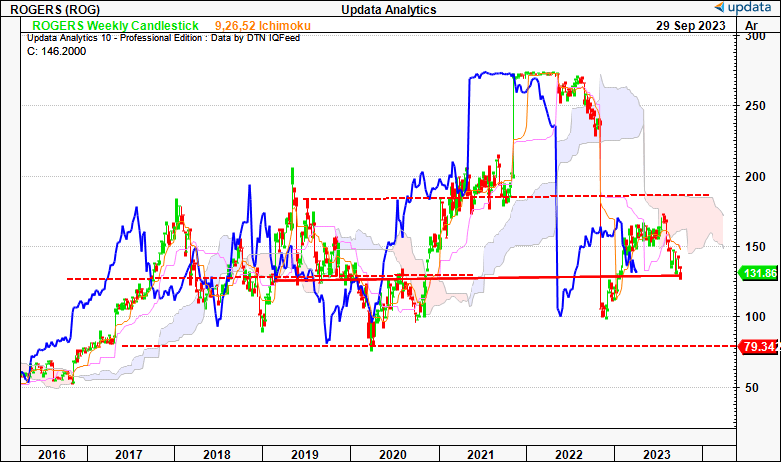

Figure 6. Weekly chart —trading back within very long term range

- Winding back before the three catalysts—1) Covid, 2) the original acquisition announcement, and 3) the termination—ROG is trading back within its longer-term range. The market looks to have been fairly efficient in reorganizing the company's fair value in this regard.

- This has a much wider hurdle to overcome. The level is $183 on this chart by December, and it looks to the coming weeks. The further ROG breaks away from this level to the downside, the greater the effort to curl back up. And we've already discussed a key investor's exit here today.

{kind=link}

Valuation and conclusion

Even with the recent price action, ROG still sells at a premium to the sector. It trades at 31.4x forward earnings and 24x forward EBIT at the time of writing, 44% and 37% premium to peers. It is priced at 2.3x EV/invested capital, and with the trailing ROIC of 7.5%, the market-implied return on capital is 3.2%, indicating the market expects flatter growth moving forward.

Question is, do we believe the market or not. Consider that ROG also sells at ~2x book value at the time of writing, and the company's trailing ROE is 8.4%. I'm not sure I can get there at this multiple. This suggests the market value of its net asset value is worth 2x what is recorded in the books.

To explain it mathematically:

- You'd be paying ~$2.5Bn for a book value that's recorded at $1.25Bn.

- Right now, the trailing ROE is $96.5mm/$1,205 = ~8%.

- Paying the 2x multiple means you are getting an ROE of $96.5mm/2,540 = 4%, halving your return, also aligning with the market's expected returns on capital of ~3.2% from earlier. Definitely something to think about, especially for a positive return in the near term

Figure 7.

Source: Seeking Alpha

With ROG trading at such high multiples still, this is beyond my threshold of what I am willing to pay. 31x forward earnings, 24x EBIT, with a 4% investor ROE, aren't the most appealing sets of numbers. In that vein, I rate ROG a hold on grounds of valuation.

In short, ROG was presented as a potentially attractive special situation earlier this year. Especially when Starboard was on board. It has now trimmed its position, and ROG''s market value looks to have rolled over along with most of the market in September. Analysis of the company's economic value corroborates this view. The firm's capital isn't overly profitable, and asking multiples of 31x forward earnings are too steep for a sensible investor to pay in this instance. Not to mention they are counterproductive to shareholder value. Considering all the factors raised here today, I rate ROG a hold.

{kind=link}

For further details see:

Rogers: High Multiples, Flat Economic Performance, Rated Hold