ROIV - Roivant Sciences: 'Fiercely Economic Actor' With Multiple Catalysts

2023-03-06 14:38:37 ET

Summary

- In its recent past, Roivant has successfully generated a series of satellite companies it calls Vants; it monetized part of its portfolio in 2019.

- More recently, Roivant went public and listed its shares on NASDAQ.

- Roivant's one approved therapy is VTAMA (tapinarof), a topical in treatment of plaque psoriasis.

- Roivant has a sprawling pipeline with multiple potential blockbuster therapies.

- Roivant's financial picture is complicated.

This is my first look at Roivant Sciences ( ROIV ). It has an interesting and productive past, leading to its current situation and future prospects as I discuss in this article.

Formed in 2014 to expedite drug development, Roivant has fathered several productive companies

Where does the "Vant" nomenclature for privately owned Swiss pharma Roivant's satellite companies come from? For those linguistically inclined, the term "Vant" is a tough one. Roivant has latched on to it as a term referencing its 20-odd portfolio companies. In the "about us" tab of its website, Roivant notes:

Roivant has built 20+ portfolio companies (Vants)

One might be inclined to dismiss it as continental foolishness, until one reads:

In 2019, we consummated a $3B upfront strategic transaction with our partners at Sumitomo Pharma, and we have continued to build a broad and differentiated pipeline of drugs and drug candidates...

That is one whopping upfront payment for any company to be notching, much less a company formed only a few years previously. Maybe there is more to these Vants than the nomenclature necessarily implies. In particular, maybe the king of the Vants, Roivant, who retained significant assets, merits serious attention. Ergo this article.

Roivant Sciences has traded erratically since it went public in 05/2021

Back in 05/2021, Roivant Sciences went public in a SPAC transaction valuing the company at $7.3 billion. As I write on 03/04/2023 Roivant has a market cap of ~$6.1 billion.

Initially, its shares traded flat hovering around ~$10.00 often on minor volume under 100,000 shares. When its SPAC closed in early 10/2021 its shares went into a steep skid , trading below $6.00 on several occasions in 10/2021.

The stock soon began a recovery on a positive broker report valuing it at >$20 billion in the long run. Its shares then meandered until 12/2021 when they rallied ~90% following a key patent win.

It turned out to be a case of "easy come, easy go" as Roivant quickly gave back its gains and more, dropping to <$3.00 by 05/2022. It recovered a bit and then was trading <$3.00 again for several sessions in 09/2022. Since its 09/2022 swoon, it has marched up rapidly touching $10.00 on 01/12/2023.

As I write on 03/05/2023 it trades at $8.05.

Roivant's single approved therapy since going public is its VTAMA cream

Roivant's 2019 deal with Sumitomo included a handful of FDA-approved therapies. Its sole recent approval is for its VTAMA (tapinarof) non-steroidal cream approved for topical treatment of plaque psoriasis in adults in 05/2021.

Roivant touts it as the first and only FDA-approved steroid-free topical medication in its class. It also notes it is approved for mild, moderate, and severe psoriasis with no label restrictions on duration of use or body surface. It promptly set a 05/2022 launch date.

Roivant's 02/2023 Overview presentation, (the " Presentation ") slide 4 posits no small ambitions for this VTAMA. It sets outsized revenue goals, anticipating potential blockbuster revenues in psoriasis with additional blockbuster upside potential in atopic dermatitis.

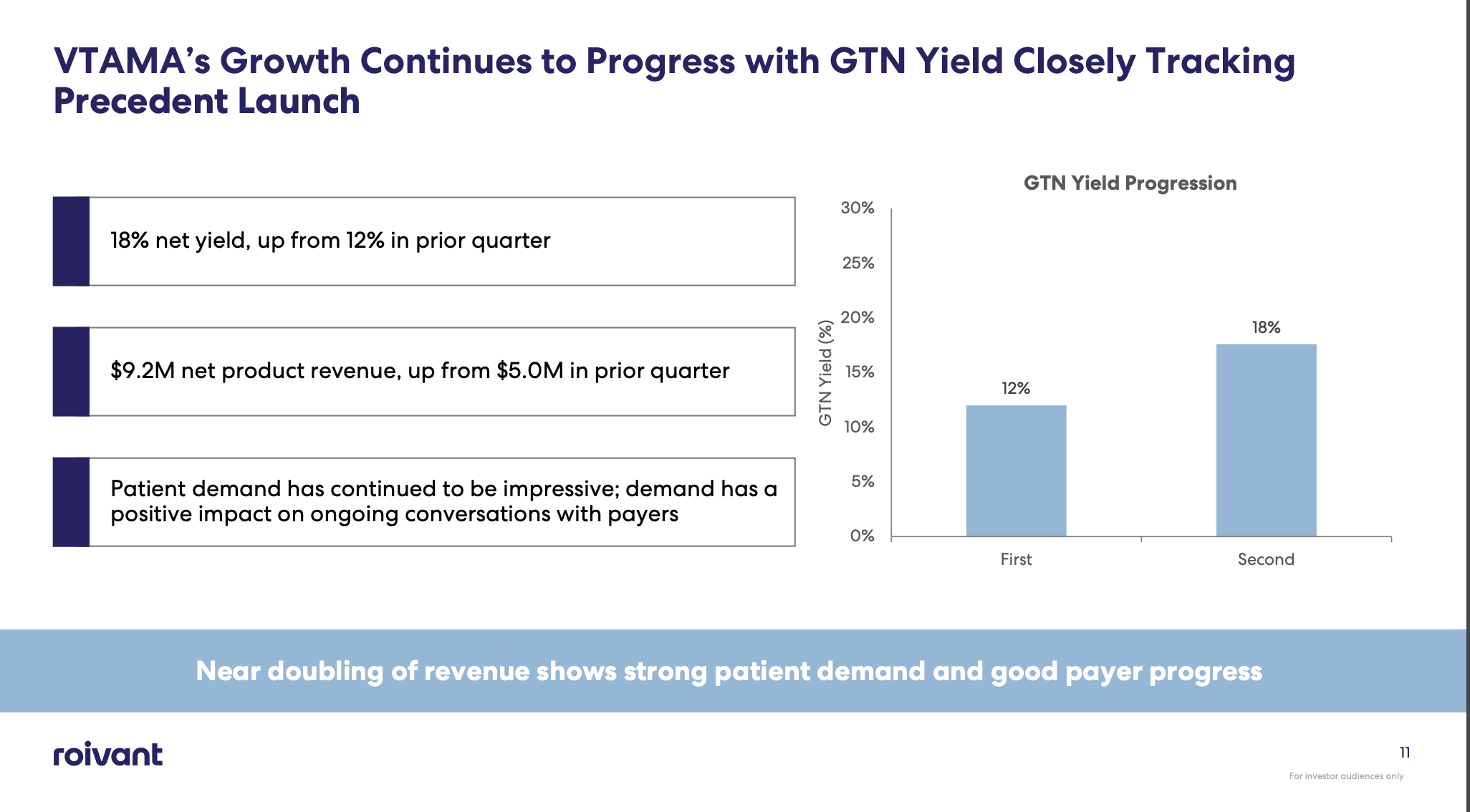

Slide 11 below shows how this will be building from a low base:

{kind=link}

During Roivant's latest 12/31/2022 earnings call (the " Call ") for fiscal Q3, 2022 CEO Gline was positively effusive about VTAMA's launch progress to date. Using terms such as:

- the company is "just incredibly excited for" the commercial launch of VTAMA;

- he was "particularly happy to report" increases in gross to net yield from 12% in our first quarter of launch, up to 18% in the quarter just ended;

- the company was "really happy" with the continued level of patient and physician demand for the product; and

- the company is "really excited" about how that launch is going and "excited" to continue to share updates as we get into the calendar year.

I found this to be a bit of verbal overkill, particularly when initial quarterly revenues were $5 million and $9.2 million. Nonetheless, there are reasons for optimism. Presentation slide 10 shows VTAMA with eight other branded topicals in weekly TRx.

Presentation slides 12 and 13 show it gaining strong payer coverage. It has already achieved coverage for 94 million commercial lives covered (57% of total). It is garnering coverage at parity with or better than topical competitors. It is still in the early days but VTAMA is coming out of the gate strong, with revenues soon to match, or so the company clearly anticipates.

Presentation slide 17 is titled "VTAMA Cream's FDA Label is Differentiated Among Competitors". It features a chart comparing a wide variety of important label differences between VTAMA and 9 competitors, including such well-known therapies as HUMIRA. VTAMA handily bested the lot.

Roivant boasts a top-tier late-stage pipeline

Pipeline, smipeline a cynic might scoff. Pipeline assets are just blue sky; they have a long and tenuous path yet to cross. This is a truism and a dangerous one to forget. However, Roivant claims superior results for its phase 3 trials.

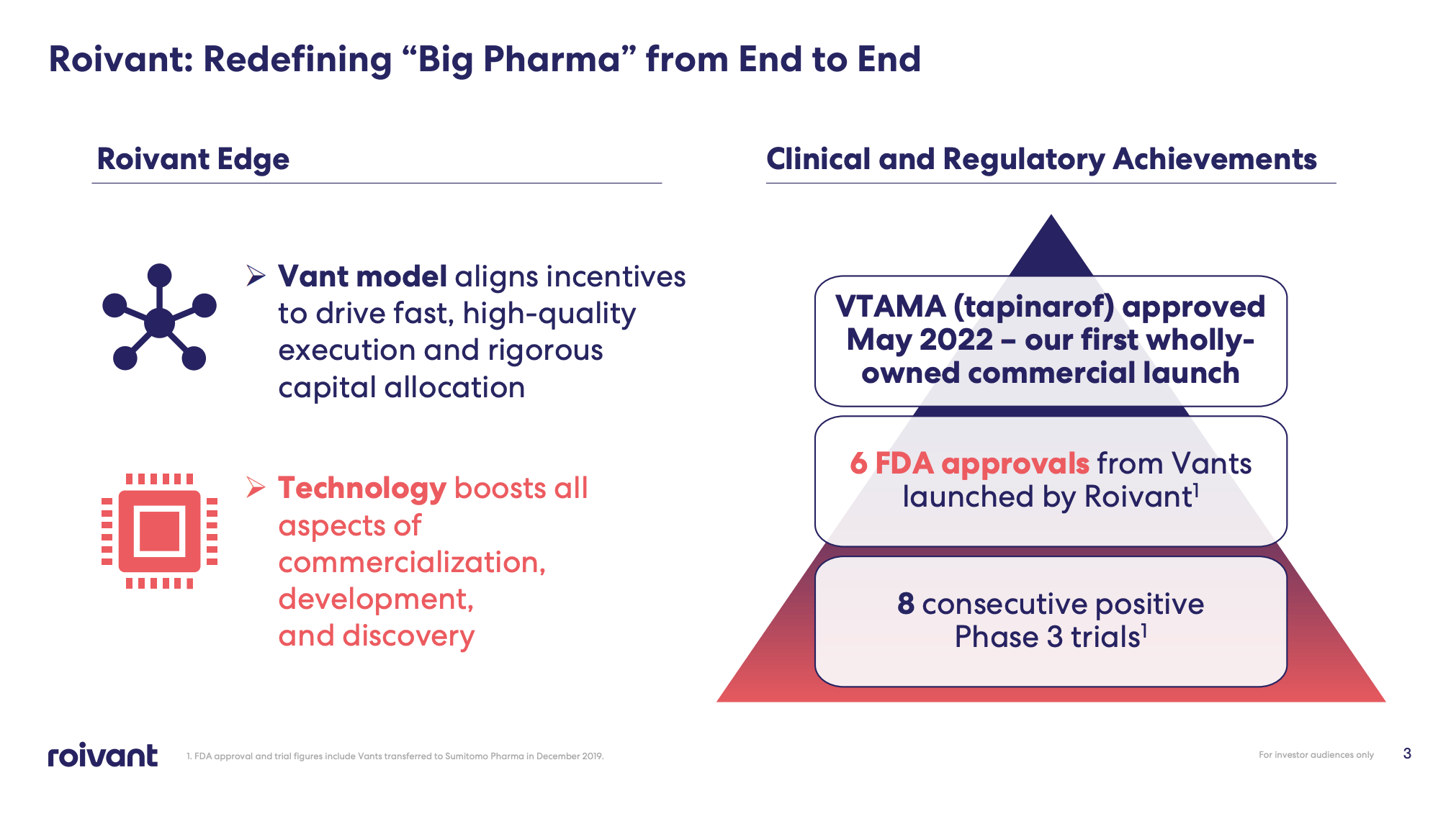

Its Presentation slide 3 below sets out an impressive resume for its molecules:

{kind=link}

Its record of 8 consecutive positive phase 3 trials is particularly attractive. Roivant's Presentation pipeline slide 5 lists four registrational trials, two of which are scheduled to readout yet in 2023. These include its:

- VTAMA phase 3 readouts in atopic dermatitis, a market ~4x the size of psoriasis, in 03 and 05/2023;

- Brepocitinib (TYK2/JAK1) pivotal trial readout in systemic lupus erythematosus (SLE) in 4Q 2023.

Beyond these readouts, which could lead to imminent FDA filings, Roivant's Presentation slide 9 includes a bouquet of upcoming catalysts spread over the next several years.

Roivant maintains a sizeable cash balance, however, it will likely continue its ongoing dilution

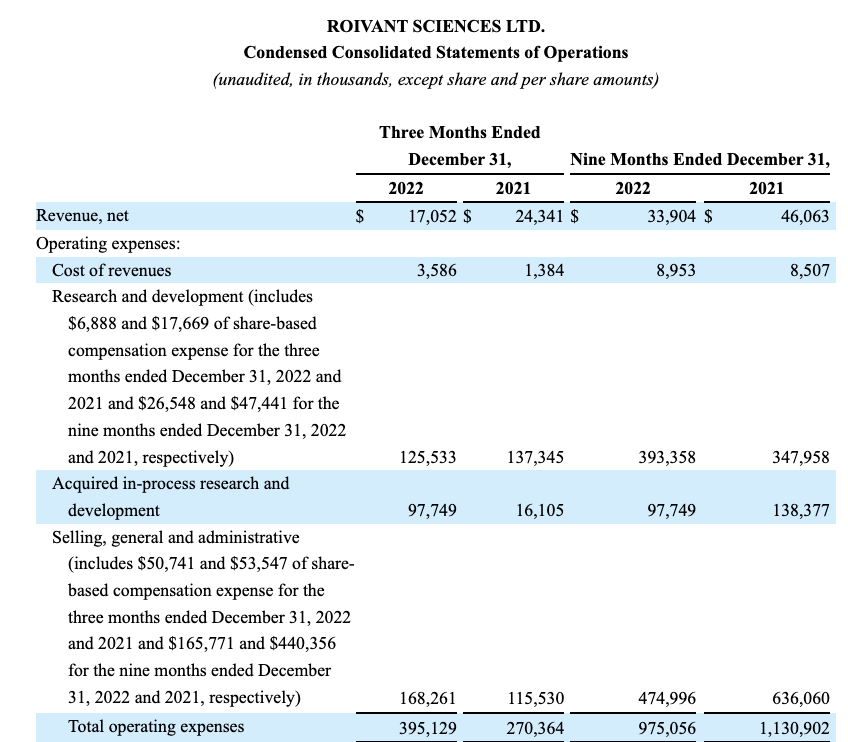

Roivant has an impressive pipeline and operating pedigree as I have discussed. However, it runs an expensive operation as disclosed by the excerpt below from its fiscal Q3, 2022 10- Q :

{kind=link}

When you annualize its total operating expenses for fiscal 2021 they total ~$1.5 billion; for 2022 ~$1.3 billion. Anyway you slice it, Roivant's excellent pipeline and its robust slate of catalysts come with a hefty maintenance price tag.

During the Call, CEO described Roivant's liquidity as follows:

... We ended the quarter with balance sheet cash and cash equivalents of $1.5 billion or about $1.9 billion giving effect to the financing we did two weeks ago, as well as expected to see the proceeds from the sale of the Myovant minority to Sumitomo Pharma, which we expect to complete this quarter.

So look, that gives us, as we've discussed before, cash runway into the second half of 2025. We are producing a tremendous amount of important clinical data during that period across all of... [our key programs]

Yes, it is generating reams of data. However, check out its price chart above with its ever-increasing shares outstanding. I submit that the share count will likely continue to mount.

Conclusion

Roivant is an unusual company. It has a track record of success that gives it nearly the aura of a big pharma. It has lots of component parts and an aggressive CEO who takes a "no holds barred" approach to maximizing value.

In response to a probing analyst question during the Call as to Roivant's approach to monetizing assets, CEO Gline responded:

... we are fiercely economic actors in every way. And so on the one hand, we're very proud of the franchise that we've built and the opportunity for each of these things. And on the other hand, we got the track record that you've observed.

The last thing I'll say is, there is a lot of interest in individual I&I programs and targets out there, obviously. But also as a whole, there are many businesses that may need to expand by multiple opportunities at the same time. And so the franchise, in aggregate, could also present some unique opportunities. And actually, at least one of our past monetization's that you referred, to involved a franchise with multiple programs, and I'd say nothing is off the table.

Nothing is off the table. That could be good, it could be bad. As an investor who wants to invest in a company, not a gunslinger, I am standing back from the king of the Vants.

For further details see:

Roivant Sciences: 'Fiercely Economic Actor' With Multiple Catalysts