ROP - Roper Technologies: A Good Long-Term Buy

2023-05-09 07:54:13 ET

Summary

- Revenue should benefit from good end-market demand, increasing recurring revenue, and M&A strategy.

- Margin should benefit from operating leverage and improving the business portfolio mix.

- Long-term investors can consider buying the stock.

Investment Thesis

Roper Technologies, Inc. ( ROP ) should benefit from healthy demand in its end markets, driven by secular drivers like digital transformation, an aging population, and water conservation. Additionally, as the company continues to shift customers from on-premise maintenance to cloud services, its recurring revenue base should increase. This along with mergers and acquisitions should help revenue growth.

The company is also poised to benefit from operating leverage and improving its business mix through the acquisition of high-margin businesses. While the company is trading almost in line with its historical valuation based of FY23 P/E, its P/E on FY24 consensus EPS estimates is at a reasonable discount. I believe ROP stock is a good long-term buy at the current levels.

Q1FY23 Earnings

Roper Technologies Inc. reported better-than-expected results for the first quarter of 2023 in the last week of April. On a reported basis, the company's revenue increased by 15% YoY to ~$1.47 billion, which exceeded the consensus estimate of ~$1.45 billion. Organically, revenue grew by 8% YoY. Adjusted EPS increased by 19% YoY to $3.90, beating the consensus EPS estimate of $3.86. The revenue and adjusted EPS growth was driven by good end-market demand and an increase in recurring revenue.

Revenue Analysis and Outlook

In a previous article in February, I expressed a bullish outlook on Roper Technologies Inc., based on its strong base of recurring software revenue, good end-market demand, and a healthy M&A strategy to support revenue growth in the near and long term. Since then, the company has continued to deliver good results, and the stock price has increased by over 7%.

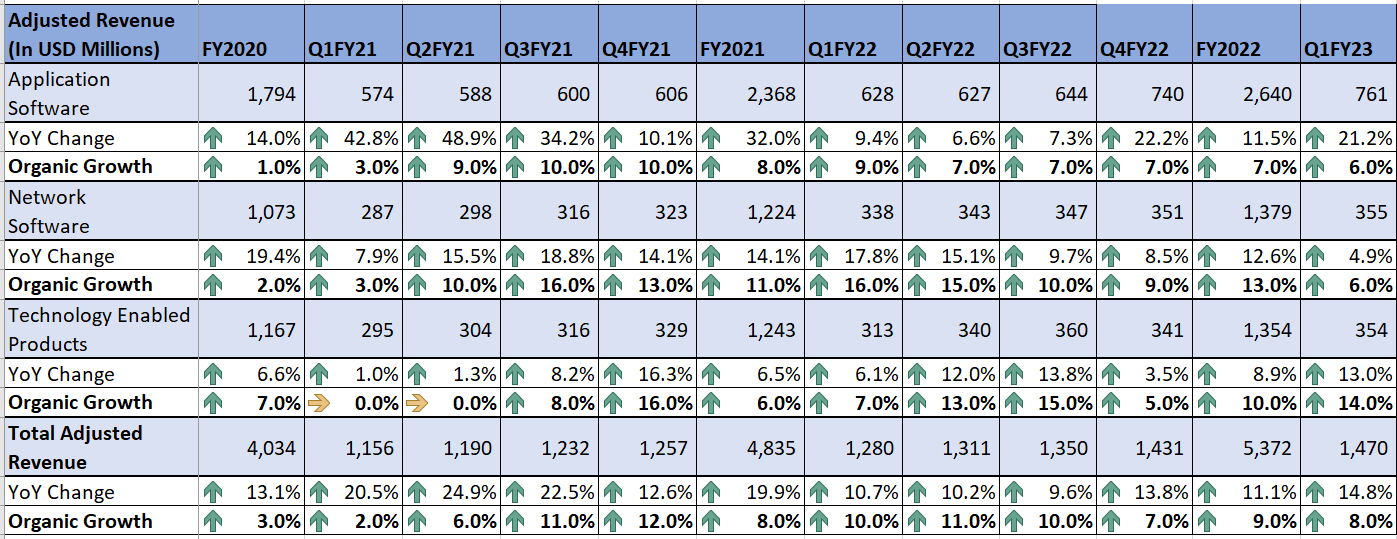

In its first quarter of 2023 earnings report, Roper Technologies continued to exhibit growth momentum. Revenue growth was driven by the contribution of Frontline Education, which was acquired in 2022. Additionally, an increase in recurring revenue resulting from high customer retention and new customer acquisition also boosted top-line growth. As a result, revenue increased by 15% YoY to $1.47 billion. Excluding an 8 percentage point benefit from acquisitions and a 1 percentage point FX headwind, revenue increased by 8% YoY on an organic basis.

ROP's Historical Revenue (Company Data, GS Analytics Research)

{kind=link}

Looking ahead, I believe ROP is well-positioned to deliver strong revenue growth in the years to come. The company should benefit from secular trends driving end-market demand, a growing recurring revenue base, and its successful M&A strategy.

The company's strategic shift towards non-cyclical businesses with a high level of recurring revenue base has helped to accelerate end-market demand over the past few years. I expect this trend to continue as the world moves towards greater digital transformation and automation. ROP should benefit from this secular trend due to its focus on delivering mission-critical software solutions to specific industries that solve a particular problem (e.g. automation) in that industry. This makes customers dependent on ROP's products for their day-to-day operations.

In my previous article , I talked about various efforts the company is taking to up-sell and cross-sell its customer base from on-premise to cloud through expanding its Software-as-a-Service ((SAAS)) offerings in its Application Software segment. It launched a couple of new software solutions in Q4, Tax Fixed Assets, and Nuke products, which should help the company in increasing its Annual Recurring Revenue ((ARR)). Additionally, during Investor Day in March 2023, the company commented that it is further advancing its Vertafore offering through the migration of its solutions to Amazon Web Services (AWS). Vertafore is a cloud-based software providing solutions to the property and casualty insurance industry and helps them manage their distribution channel including agency management, compliance, licensing, workflow, and data solutions. This migration should further enhance end-user experience and help in boosting ARR.

Moreover, the company's end markets remain healthy. In particular, Roper's medical and water products are benefiting from secular demand trends. The population is aging at a much faster rate than in the past. The older population requires more medical treatments which is boosting demand for ROP's medical products. Similarly, the growing need for the conservation of water is increasing demand for water management products. So, I expect end-market demand to remain healthy due to these secular demand trends, and the resiliency of its end markets (healthcare, legal, education, government contracting, utilities, and food), should help ROP weather tough economic times. This should also help offset the slowdown in ROP's freight-matching business DAT (due to the softening of the U.S. freight market).

Finally, ROP's successful M&A strategy should continue to drive long-term growth by expanding its footprint in niche markets. The company's focus on acquiring businesses with high margins and high levels of recurring revenue is helping it gain market share in its respective niche markets. ROP's strong cash flow generation and net leverage ratio of 2.4x exiting Q1 should allow it to pursue further bolt-on M&A opportunities.

Overall, I am optimistic about ROP's revenue growth prospects moving forward. Management's guidance of north of 12% reported revenue growth with 6% to 7% organic revenue growth in 2023 appears achievable given the good end-market outlook, M&As, and an increase in recurring revenue.

Margin Analysis and Outlook

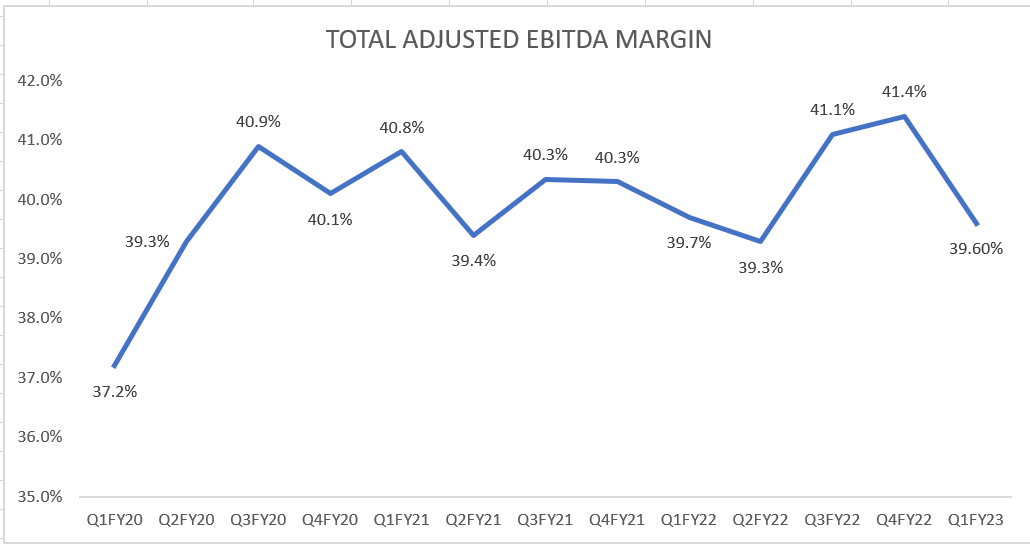

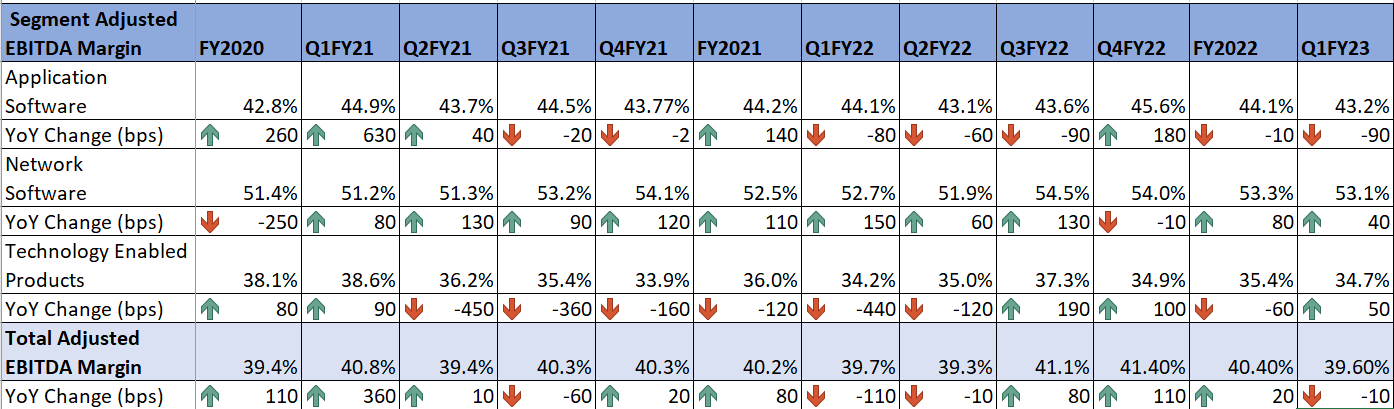

Roper successfully offset the impact of supply chain challenges and inflationary headwinds in the second half of 2022 through operating leverage from higher sales. However, in the first quarter of 2023, the company faced additional costs associated with ramping up implementation capacity in the Application Software segment. This more than offset the operating leverage and resulted in a 10 basis points year-over-year decline in the adjusted EBITDA margin to 39.6%.

ROP's Historical Adjusted EBITDA Margin (Company Data, GS Analytics Research) ROP's Segment-wise Historical Adjusted EBITDA Margin (Company Data, GS Analytics Research)

{kind=link}

{kind=link}

Looking forward, while the additional costs associated with ramping up implementation capacity in the Application Software segment are expected to impact the second quarter margins as well, I expect margins to expand in the second half of 2023 as these ramp-up costs wind down. Moreover, ROP's transition from a cyclical and project-oriented business to a less cyclical and more recurring revenue mix, combined with its asset-light business model, has been a key driver of margin expansion. As the company continues to acquire businesses with high margins and high levels of recurring revenue, it should be able to further improve its business portfolio and drive margin growth. Additionally, margins should benefit from operating leverage through increasing revenue. Therefore, I remain optimistic about ROP's margin growth prospects in the coming years.

Valuation and Conclusion

Currently, ROP is trading at a P/E of 28.13x FY23 consensus EPS estimate of $16.29 and a P/E of 25.68x FY24 consensus EPS estimate of $17.84. The company's historical 5-year average forward P/E is 28.51x. While the company's P/E multiple on the current year earnings is almost in line with historical averages, it P/E multiple of FY24 consensus EPS estimates is at a reasonable discount. I believe investors with long term horizon can consider ROP stock. With the company's growth strategy to transition towards a less cyclical and recurring revenue business portfolio showing promising results, and the secular demand trends supporting the end markets, ROP is expected to weather recessionary pressure. Therefore, I continue to have a buy rating on the stock.

For further details see:

Roper Technologies: A Good Long-Term Buy