ROP - Roper Technologies: Impressive Transformation Yet Fully Valued

2023-03-14 11:13:12 ET

Summary

- What's in a name? Eight years ago Roper Industries changed its name to Roper Technologies to reflect its transformation to a diversified technology company.

- Fast forward to today, and you'll find that 75% of the business is software, having undergone an aggressive portfolio restructuring.

- Is the market fully valuing Roper's transformation? We do a deep dive into the business to determine if it warrants a place in your portfolio.

Investment Thesis

Roper Technologies ( ROP ) is a truly intriguing company with a storied history. Roper Technologies used to be called Roper Industries , and while that one word change might not seem like much, it is evident of an entire transformation that the company has undergone over the last decade. Roper has slowly been transforming itself from a stodgy, capital-intensive industrial business into a technology-focused enterprise comprised of leading, vertical software companies in niche categories.

This transformation has helped fuel growth and margin expansion. However, this hasn't gone unnoticed by the market. Roper Technologies has outperformed the S&P ( SPY ) on a 6 month, 1 year, and 5 year basis. Currently sitting around $420, the stock is down roughly 16% from its 2021 high of $500, however it's had a nice bounce from the October 2022 lows of $360.

We outline Roper Technologies' transformation in the article below, and analyze it for its investment potential as a potential position in our dividend growth portfolio. We conclude that while it is an extremely high quality company with a terrific business model, the current macro-economic uncertainty and rich valuation are making us wait on the sidelines until we reach a more attractive entry point.

Company Background

Roper has come a long way since its industrial beginnings in 1890. Founded by George D. Roper, the company initially sold home appliances, stoves, and pumps. For approximately 60 years, the company went by the name George D. Roper. In 1957, it sold its stove business, and changed its name to the Roper Pump Company. The company continued primarily selling pumps and acquired various business along the way, and changed its name again in 1981 to Roper Industries. In 1992, Roper Industries went public and continued to operate as an industrial company selling pumps, valves, and fluid-testing equipment. Things remained that way until 2001, when Brian Jellison took over as CEO.

Engineering a Transformation

Brian Jellison, a former executive of General Electric ( GE ) and Ingersoll Rand ( IR ), became Roper's CEO in November 2001. At that time, Roper Industries' market cap was around $1 billion. Today, it's hovering around $45 billion. Now, Jellison could have continued to stay the course on Roper's traditional path, fighting for market share in pumps and valves, and picking up adjacent businesses along the way.

Instead, Jellison had the vision and the audacity to turn that approach on its head. Instead of the typical industrial holding company approach, Jellison replaced that with an operating model approach. The vision was to acquire leading businesses with high margins and strong cash flows and allow them to operate in a decentralized business model, enabling the previous owners to maintain their existing culture and identity and run the company as they see fit. And that is exactly what Jellison did during his tenure; constantly executing on that strategy by taking cash flows from an acquired business and acquiring more new business that throw off more strong cash flows. Rinse and repeat.

After Jellison's unfortunate passing in 2018 due to illness, Neil Hunn took over as CEO. Hunn has been with Roper Technologies for nearly 12 years and worked under Jellison as Executive VP and COO, so he has seen the transformation under the leadership of Jellison first hand, and has continued that same approach to this day.

Roper Industries becomes Roper Technologies

Taken from page 1 on Roper's latest investor presentation , their strategy can be summed up in one sentence:

We compound cash flow by acquiring and growing niche, leading technology businesses.

Roper's appetite for high-margin, cash flowing businesses in niche categories led them to start acquiring companies outside of their traditional industrial heritage. In 2012, Roper acquired Sunquest Information Systems, which was a maker of laboratory and diagnostic software. The pace of M&A accelerated soon thereafter with acquisitions of Aderant, rf IDEAS, and CliniSys catapulting Roper into the markets of legal software, RFID technology, and life sciences, respectively.

Perhaps most notable, in 2015 Roper Industries announced a name change to Roper Technologies reflecting its evolution as a diversified technology company. Brian Jellison stated:

The Roper Technologies name reflects our existing family of high-performing businesses and also points to a future of great opportunities.

Jellison kept true to that promise by continuing to acquire and grow leading businesses over the following years, primarily in the vertical software markets. We would encourage our readers to take a few minutes and parse through the various companies that Roper has added to its portfolio . A quick look shows various types of businesses: campus solution software (CBORD), software for contractors (ConstructConnect), healthcare analytics (Strata), supply chain software (IntelliTrans), and creative visual effect software (Foundry), just to name a few.

At first glance, you would think that these are completely disparate, unrelated businesses, and you wouldn't be wrong. But the common thread that ties all of these together - and the reason they all thrive under the Roper corporate umbrella - is that these are niche categories that have minimal competition. Moats are strong and margins are high. A large software outfit like Oracle ( ORCL ), Microsoft ( MSFT ), or Salesforce ( CRM ) is not going to go after these smaller markets. It just isn't worth their time, R&D dollars, or marketing spend. One (whimsical) way to look at it, is that the Oracles of the world are too busy mending their nets and casting them overboard trying to catch as much cod as they can, while these niche software players are sharpening their knives to pry open their next oyster as they deep sea dive for pearls. There's just no comparison.

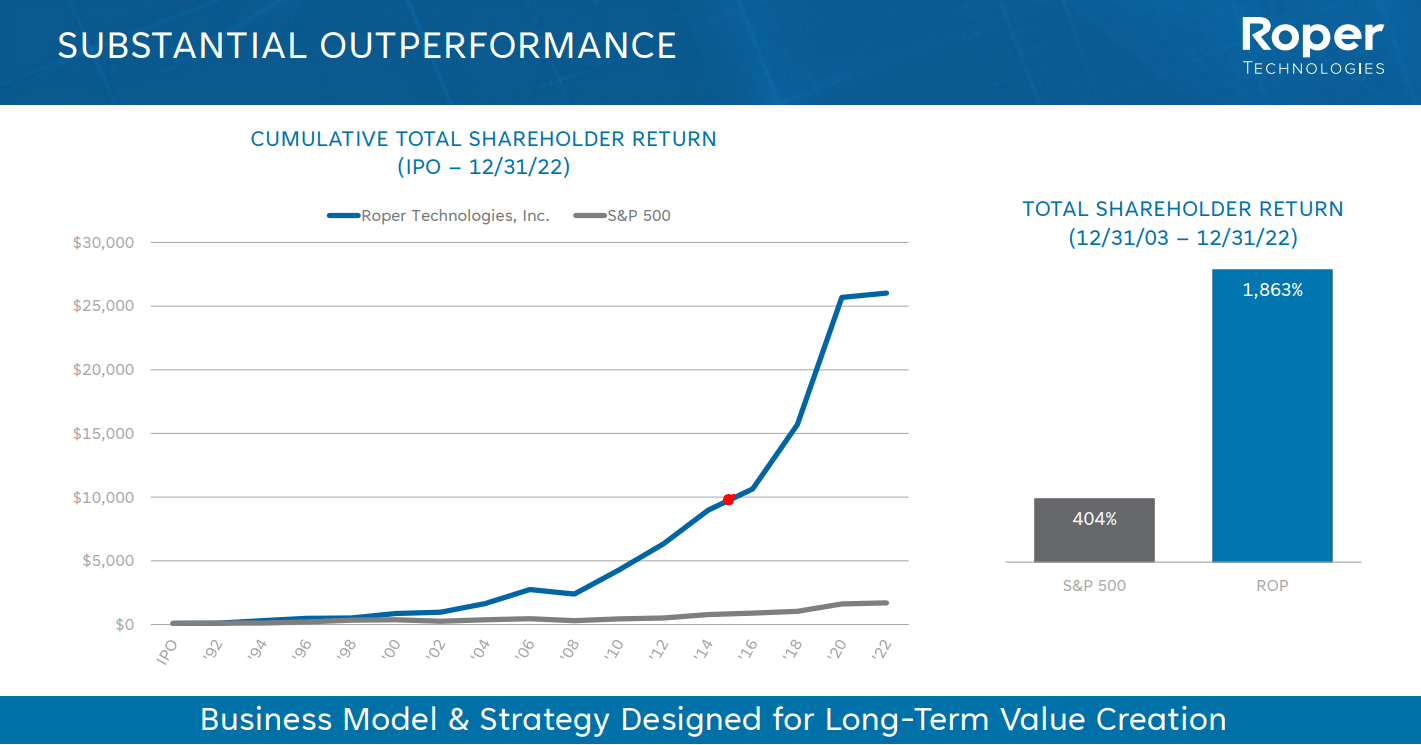

In fact, since Roper became "Roper Technologies" in 2015, their stock growth has gone exponential, as evidenced in this chart below. We don't think that's a coincidence.

Roper Investor Presentation, Feb 2023

{kind=link}

During last month's earnings call (Q4 2022), newly appointed CFO Jason Conley made a very insightful remark that likely went missed by most investors, stating:

I've been blessed to help guide and execute our evolution from Roper Industries to Roper Technologies, which has been underpinned by our North Star belief that cash is the best measure of performance. And as we enter 2023, our best years are ahead of us. We have a family of market-leading businesses with durable growth drivers and terrific free cash flow margins.

There's a lot to unpack in that short paragraph, but this is just one more example of the overall consistency in Roper's business philosophy. Having a "North Star" belief of generating strong free cash flow margins is exemplary of a high quality business. Investors are realizing that times are changing, and Roper provides a welcome contrast to other technology firms that are borderline profitable focusing solely on how many active users they have during a given month.

Vertafore & Frontline Acquisitions

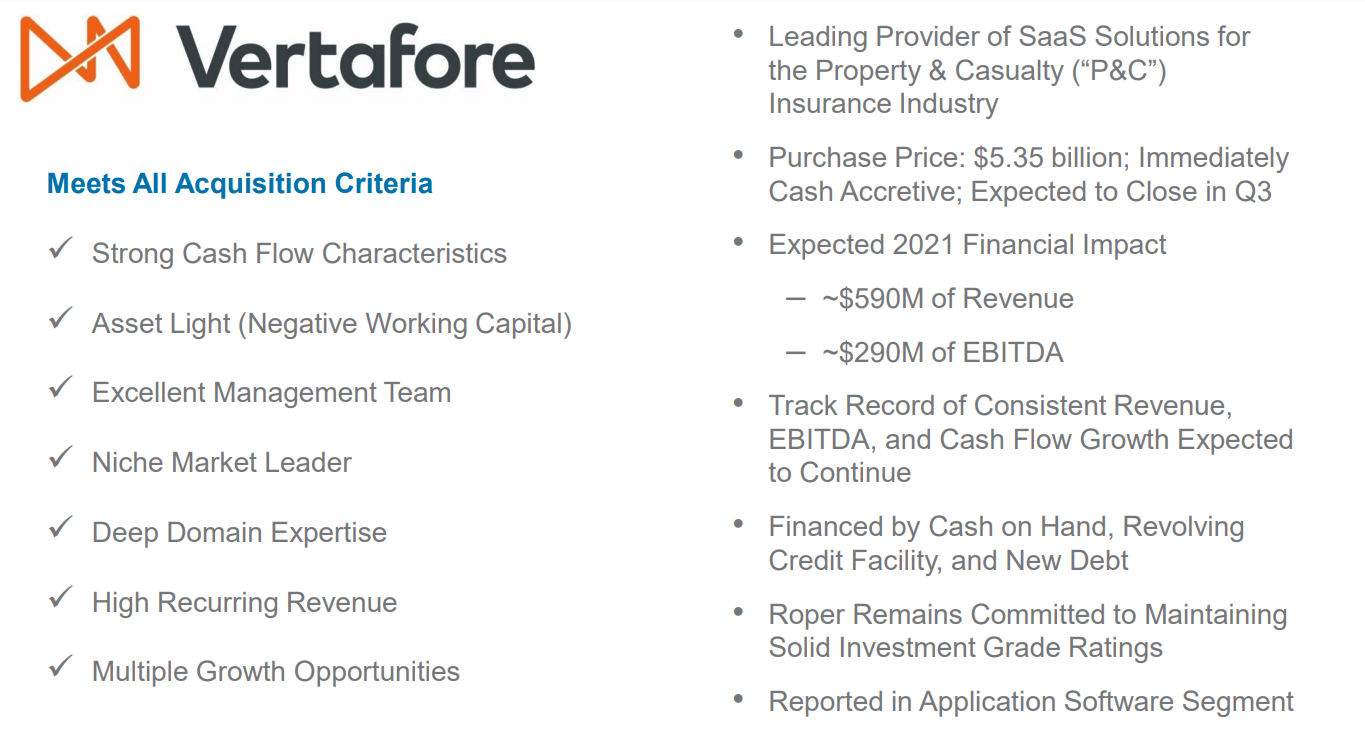

Up until 2020, Roper Technologies has usually paid a couple hundred million dollars for acquiring companies, seldom exceeding $1 billion except for a few cases with Deltek, PowerPlan, and iPipeline. However, in mid-August 2020, Roper made a cornerstone acquisition with Vertafore, a leading property and casualty insurance software business for $5.4 billion. This was larger than its five previous acquisitions combined, and signaled to the market that Roper Technologies was serious about the "technologies" part of its name. We took a look at some historical stock charts and it turns out that the market was not too keen on this acquisition, with Roper falling about 10% in the month following this announcement, versus the S&P remaining roughly flat.

Despite the larger-than-usual purchase price, we can see from Roper's presentation that this met all their criteria for an attractive acquisition target: strong cash flows, asset light business, high recurring revenue, niche market leader, and providing strong growth opportunities, among others.

Vertafore Acquisition Presentation, Aug 2020

{kind=link}

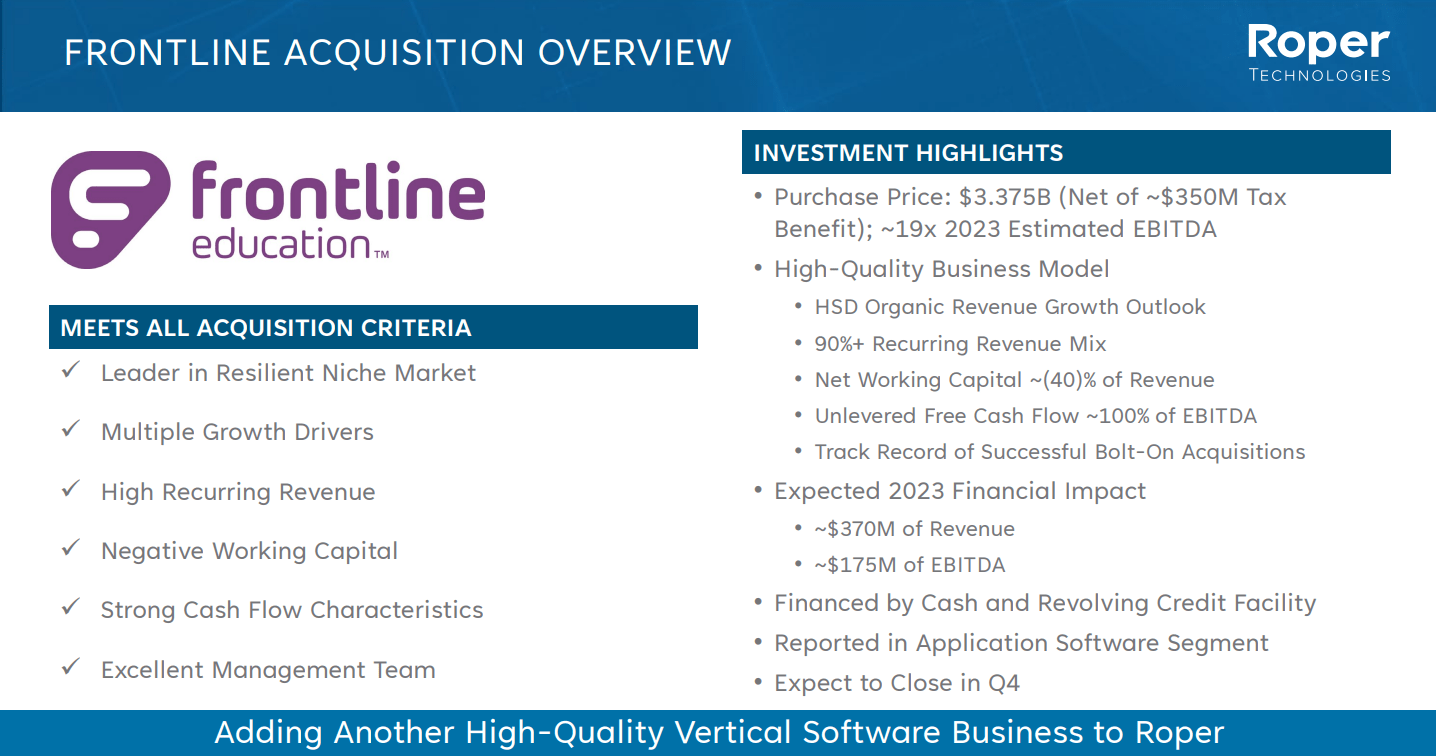

And then, just last August, Roper again made waves by announcing a $3.4 billion purchase of Frontline Education, a leading software provider of solutions for K-12. In their earnings call that month, they once again highlighted the rationale for acquiring Frontline, and it lined up to be nearly verbatim to their criteria when they acquired Vertafore, two years earlier.

Roper Conference Call Presentation, Aug 2022

{kind=link}

Even though Frontline and Vertafore are in two completely separate industries, Roper recognizes that they carry the same characteristics of strong cash flow, leaders in niche markets, growth potential, and high switching costs.

That last item regarding high switching costs is crucial: once a customer implements a software and trains their staff, there is a strong reluctance to switch to a different provider. Fighting status quo and the law of inertia is like fighting gravity. Sometimes you can do it, but only after enormous amounts of time, energy, and cost. Therefore, with a leading provider of software the likes that Roper acquires, most customers will be complacent to continue subscribing to it, whether it's for educators, contractors, healthcare workers, or insurance agents.

To reiterate, Roper's business model isn't to go in and drastically change the way these companies operate and create revolutionary synergies across its subsidiaries. Rather, its decentralized model allows these companies to continue operating as they have been, with the financial backing of Roper's compounding cash flow machine quietly at work in the background. This is just a testament to the vision that Brian Jellison laid out for the company a decade ago, and is the blue print that Neil Hunn has followed since then.

Strong Fundamentals

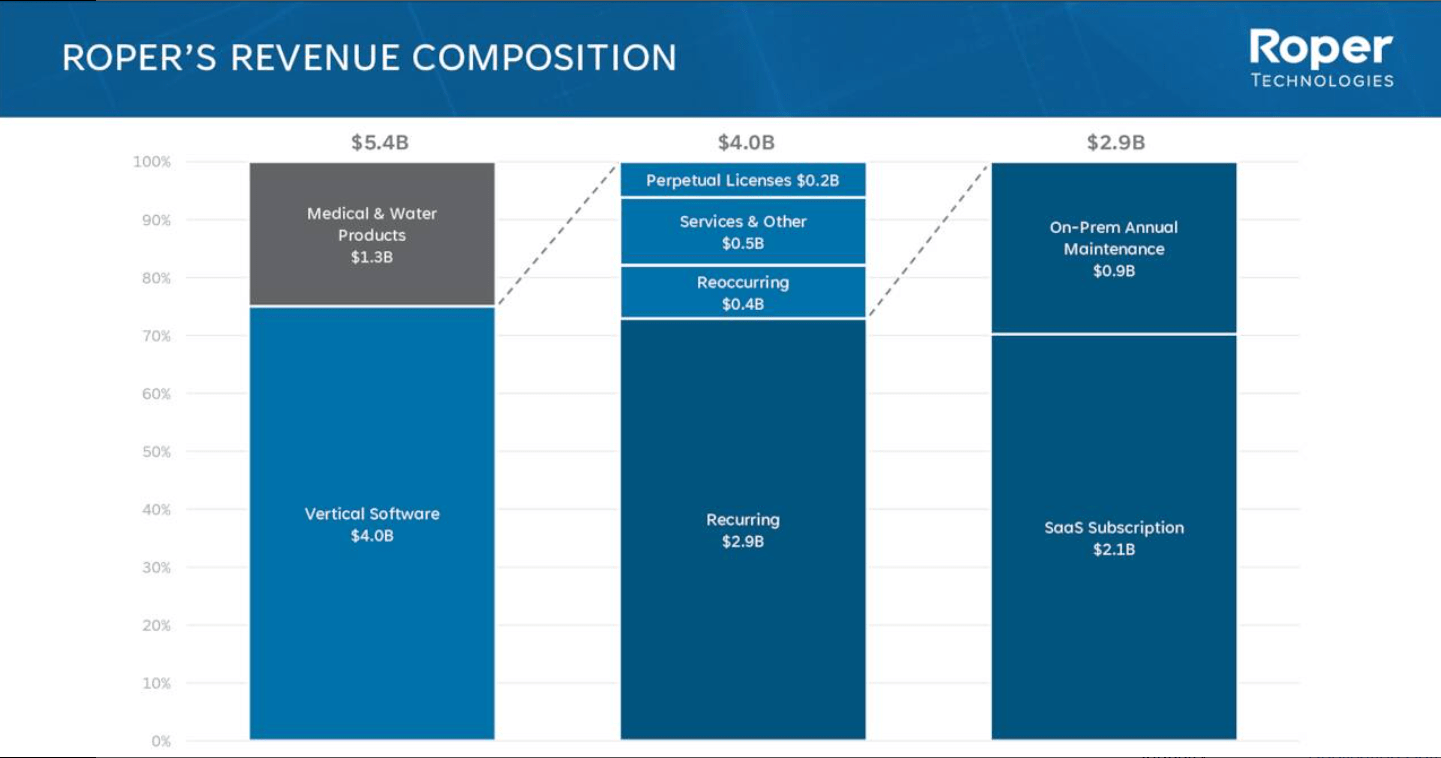

Roper's aforementioned transformation has resulted in a full 75% of revenue coming from its portfolio of vertical software solutions, with the remaining 25% coming from medical and water-related products. While the medical and water-related segment is not driven by recurring software revenue, these are still pretty attractive and resilient markets in their own right, in light of macroeconomic uncertainty these days. For instance, Roper owns the Neptune brand of water meters, which are installed in more than 72 million households.

Roper Investor Presentation, Feb 2023

{kind=link}

History of Margin Expansion

With 75% of Roper's revenue coming from software, roughly 70% of this amount is recurring revenue in the form of SaaS subscriptions and annual maintenance. As Roper has acquired these software businesses and continued to divest an increasing amount of its legacy industrial business, it has transitioned from a capex, project-based business model to a more asset-light, recurring growth model sporting higher margins.

As investors, one of the key metrics we look at for any potential investment is the history of margin expansion (or contraction). This is crucial because higher margins translate to a company retaining more of each dollar that it earns which is correlated to strong levels of free cash flow. This, in turn, can be used by the company to reinvest in the business, acquire companies, and reward shareholders.

Looking at Roper's gross margins, these have gradually expanded over the years with gross margins at 59% in 2014, rising to 62% in 2016, jumping to 67% in 2019, and subsequently growing to 70% in 2021 and 2022. This isn't all that unexpected from a serial acquirer of high quality vertical software, but quite impressive nonetheless.

Dividend History

Roper Technologies' dividend does not stand out when compared to the pack of other dividend and dividend-growth stocks. Its yield is currently standing at a paltry 0.65%. However, what investors may not realize is that Roper is a dividend aristocrat, having raised its dividend for 30 consecutive years.

Despite its dividend growth track record, Roper is somewhat a victim of its own success. Its stock price has continued to appreciate so much over the years that its dividend has remained on the lower side. Long term investors that have been in this name are no doubt quite pleased with its performance and are likely sitting on a relatively higher yield on cost. If you had purchased stock in Roper Industries ten years ago, the stock price was around $120 and the annual dividend was $0.66 for a dividend yield at that time of roughly 0.55% - not too far off what it is today. However, if you have continued to sit on those same shares over the last decade, your yield-on-cost would be 2.3% - still not high yield by any means, but pretty decent for a high quality company with years of growth and compounding returns ahead of it. Roper won't be making it into a retiree's high yield income portfolio any time soon, but that's because Roper is primed for capital appreciation. This might be an investment for someone in their 20s, 30s, or 40s to take a closer look at and perhaps tuck away in their portfolio for the next 10-20 years.

On a related note, we don't want to chase yield for yield's sake. There are a ton of lousy businesses out there yielding 5%+ that we wouldn't think about touching. There are also a ton of terrific businesses out there that barely yield anything. When you make an investment, you need to know exactly how it fits into your portfolio and what purpose it serves there. Our general portfolio is a growth and income approach, and by not focusing solely on yield, this has led us to some great, but low yielding, investments such as Visa ( V ), Costco ( COST ), and Nvidia ( NVDA ).

Valuation and Target Price

So now that we've had a chance to look under the hood of Roper a bit, and understand its business, operating model, fundamentals, and growth prospects, we need to see if this would make a worthwhile addition to our portfolio. And if so, at what price we'd be willing to pay. We would also like to remind investors that every investment also comes with its own sort of cost - opportunity cost. Every dollar you put into one investment means that those dollars cannot be invested into something else.

When we look at Roper Technologies, we'll screen it with a lens looking at it as a technology company versus its traditional industrial roots. Roper's model of decentralized vertical software companies doesn't really fit the mold of most peer groups, but we think we've identified some comparable companies to pit Roper against: Constellation Software ( CNSWF ) - a Canadian software conglomerate that has a similar acquisitive nature and operating model to Roper; Guidewire Software ( GWRE ) - a mid-cap vertical software company in the property and casualty insurance space (likely competing directly with Roper's Vertafore), and Blackbaud ( BLKB ) - a small-cap vertical software provider selling to K-12, healthcare, and non-profit organizations (similar target markets as Roper's Frontline, CBORD, CliniSys, and Strata).

In the chart below, we size up these companies looking at valuation and growth metrics.

| Market Cap |

| P/E |

| Forward P/E |

| P/S |

| PEG |

| Gross Margin |

| Roper Technologies |

| $45B |

| 45 |

| 26 |

| 8.3 |

| 3.7 |

| 70% |

| Constellation Software |

| $35B |

| 72 |

| N/A |

| 6 |

| 1.6 |

| 36% |

| Guidewire Software, Inc. |

| $6B |

| N/A |

| N/A |

| 6.5 |

| N/A |

| 43% |

| Blackbaud |

| $3B |

| 21 |

| 16 |

| 3.5 |

| 1.5 |

| 53% |

A bit of a mixed bag here. Roper Technologies definitely comes out head and shoulders above the group on gross margins, but its valuation leaves us wanting more. It turns out that Guidewire is not profitable yet, so any earnings-related metrics turns out to be non-applicable. And we were actually quite surprised by Blackbaud. This is a name that hasn't come across our radar yet, but their valuation metrics were the most attractive here, and they also sport some strong gross margins. They unfortunately don't pay a dividend, but this intrigues us enough that this could be a company we take a closer look at later on.

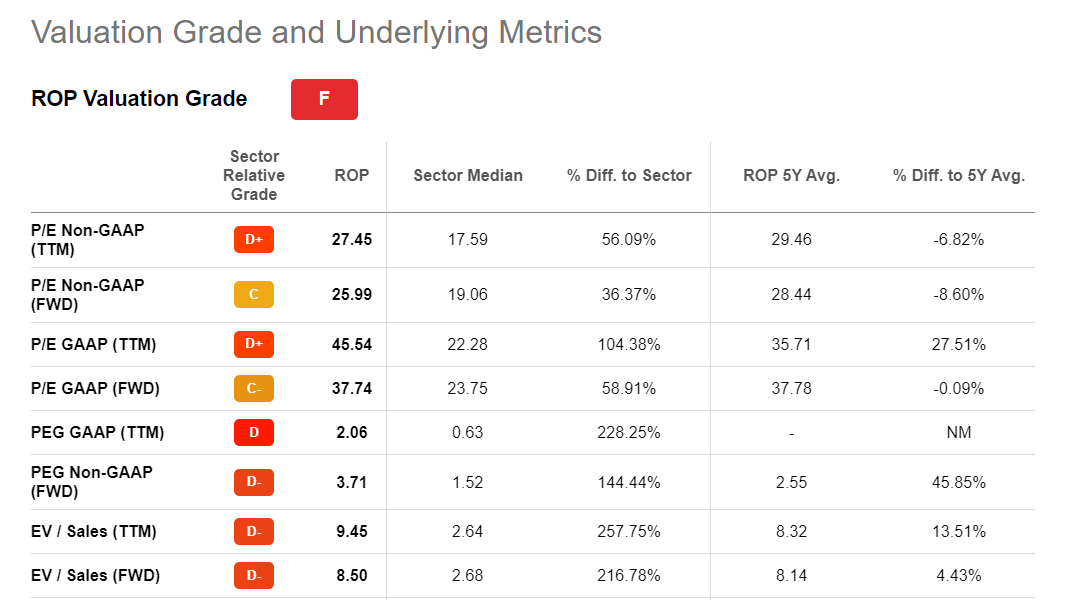

While we like Roper as a business, we're struggling with their valuations. We like the PEG ratio to be under 2 (and under 1 is even better), and prefer the Price-to-Sales ratio to be around 3 or 4, or ideally even less. Seeking Alpha seems to agree and gives Roper's valuation score an F:

{kind=link}

We definitely don't mind paying up a bit for a high quality company, but Roper seems to have gotten ahead of itself in terms of paying for growth at a reasonable price. We'd like to see their forward P/E get closer to the sector median of 19, which would imply a price of $300. The last time Roper traded this low was in the depths of March 2020 during the COVID-crash. In fact, that month Roper actually traded down to around $250 before sharply bouncing back. We recognize that, barring a major recession, it might be a stretch for Roper to trade back down to those levels, so we think a fair price would be somewhere around the $350 level. This isn't too far off from where it traded this past October during the lows of 2022. $350 is a 17% retracement from current levels, so for the time being, we'll wait on the sidelines to see if rate-induced macroeconomic uncertainty helps to anchor Roper's stock price closer to these levels.

Risks

Roper Technologies is a cash compounding machine. They have dozens of businesses that are throwing off cash today and getting redeployed into larger sized acquisitions (namely Vertafore and Frontline). However, a key risk is that in order for Roper to move the needle for revenue and margin growth, it will need to make larger-sized acquisitions.

There isn't too much acquisition-related integration risk, because Roper's modus operandi is to keep each acquired business running as it has, with leadership, culture, and decision-making capabilities intact. However, as an acquisitive company, there are several critical risks that stem from this type of business model:

- Dilution risk - If Roper decides to issues shares to fund a large acquisition, current shareholders are diluted.

- Interest rate risk - If Roper decides to fund a large acquisition through debt/corporate bond instruments, current high rates could eat through cash flows in order to service interest payments.

- Shareholder returns risk - Funding future acquisitions may result in a shift in the company's shareholder returns policy, which may decrease share buybacks and/or lead to lackluster dividend growth.

- Execution risk - with any acquisition, Roper must ensure it will continue strong execution and contribute to high growth rates and margins. Given Roper's history of M&A, this isn't too much of a concern. However, the stakes will be raised as Roper feels the need to acquire larger businesses over the coming years.

Take Away

Frankly, we like Roper Technologies a lot. We are quite impressed with its transformation over the last decade and subsequent margin expansion. Its name change eight years ago is indicative of this transformation which has served it well. We have no doubt that Roper will continue to execute on its "North Star" strategy of acquiring market-leading, niche businesses and continue to be a compounding cash machine. We are also a big fan of their dividend growth history, despite the currently low yield.

The main qualm that we have is with its valuation. Price-to-Earnings, PEG, and Price-to-Sales ratios all need to come down to a more reasonable range. Unfortunately (for potential investors), the market seems to have fully priced in Roper's transformation along with some optimistic assumptions for future growth. While we are fine paying a slight premium for a high-quality business such as this, there is just too much of a gap in what we think is fair value. $350 seems to be a more reasonable level, and we would likely initiate a starter position around those levels.

As always, thanks for reading. We hope you enjoyed this article! Feel free to let us know your thoughts in the comments section.

For further details see:

Roper Technologies: Impressive Transformation, Yet Fully Valued