ROP - Roper Technologies: Incredibly Profitable M&A Strategy That Wins

2023-06-16 06:18:39 ET

Summary

- Roper's strategy is to purchase high-quality, niche businesses with high margins and recurring revenue.

- Roper's current EBITDA-M is 40% and on an upward trajectory due to the development of subscription-based revenue.

- Roper is investing into industries which are fundamentally important to society, creating a non-cyclical operation.

- Technological development is favoring the areas in which Roper is invested, implying healthy growth tailwinds in the coming years.

Investment thesis

We are highly bullish on Roper. The company is on a fantastic trajectory and Management are razor focused on delivering its M&A/SaaS strategy.

Our current investment thesis is:

- Margin improvement is still possible as several businesses transition to a subscription model.

- Industry tailwinds, driven by technological development, should support revenue growth in the coming years.

- Roper's businesses operate as niches within fundamentally important industries, creating a non-cyclical operation.

- Management's execution of M&A continues to deliver and we have full confidence that this will continue to be the case.

Company description

Roper Technologies, Inc. ( ROP ) specializes in the design and development of software and technology-enabled products and solutions. The company offers a wide range of software solutions, including management, diagnostic and laboratory information management, transportation management, and financial analytics software.

Share price

Roper's share price has generated impressive gains over the last decade, returning in excess of 200%. This is a reflection of the company's impressive transition from an industrial business to technology.

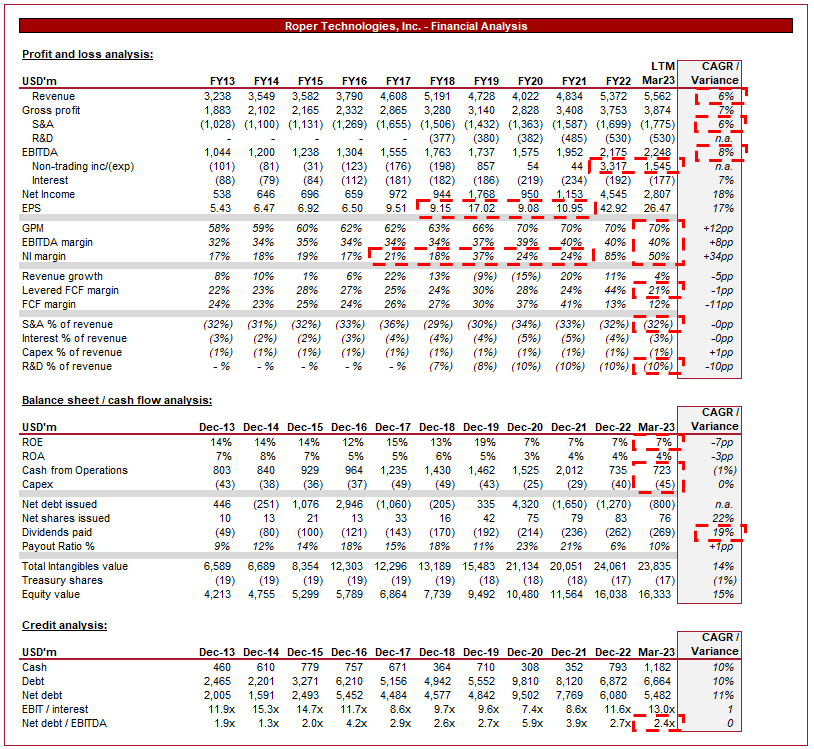

Financial analysis

Roper Financials (Tirk Terminal)

{kind=link}

Presented above is Roper's financial performance for the last decade.

Revenue & Commercial Factors

Roper started as a pump and home appliances maker in the 1890s and was subsequently listed in 1992. At the time, it was referred to as Roper Industrials. Since then, the company has been on a strategic overhaul, transitioning away from Industrials and toward Software. This culminated in the sale of its majority stake in the Industrials business to CD&R .

Roper is now focused on asset-light companies in the software sector, seeking to acquire and develop non-cyclical businesses within niches, creating a defensible position from which to generate lucrative recurring revenues.

The company currently operates in three divisions. Application software, Network Software, and Technology enabled products (Non-software segment). The company is industry agnostic, focusing on its key investment criteria (which we will analyze later).

M&A

Roper's astonishing growth in the last decade has been driven by its M&A strategy. The company targets businesses with:

- Niche operations.

- Highly defensible position with growth potential.

- High margins

- High recurring revenues

- Strong cash flow generation

These are the criteria for a winning strategy. The reason we do not see more businesses attempt a strategy such as this is due to issues with scale, expertise, and integration.

Roper's purchases have generally been in the mid-market, which is the perfect segment due to the lack of competition from the significantly larger Tech majors. This said, the company does face competition from Private Equity, which is likely the reason for the multiples paid.

Further, they are usually technologically advanced, allowing the business to partake in the growth segment of the respective industry while reducing any risk of obsolescence. Additionally, with a technologically-driven approach, these businesses are far more likely to engage in innovation and development, increasing the scope for growth.

One underappreciated factor within Roper's acquisition strategy is the industries the company targets. Despite the niche segments, the majority of the industries the portfolio companies operate within are fundamentally important to society. Just to name a few, Roper operates in the following:

- Construction

- Legal

- Healthcare

- IT

- Insurance

- Shipping

- Foodservices

- Water

- Manufacturing

- Education

- Regulation

None of these industries are discretionary, creating the ultimate non-cyclical portfolio with exposure to economic prosperity. Roper can benefit from reduced downside risk (low churn, high scope for positive pricing) while still enjoying high growth.

Application Software

Application Software (Roper)

Application Software ((AP)) has experienced strong gains in recent quarters, reflecting resilience against economic conditions. This segment has benefited from key acquisitions in recent years such as Vertafore, as well as continued new customer wins.

Deltek (Enterprise software and information solutions for project-based businesses) and Aderant (Global provider of comprehensive business management software for law and other professional services firms) continue to develop their SaaS capabilities, currently focusing on new customer wins and migrating customers. This represents a natural tailwind in the coming years given the scale of these businesses within the division. Further, Deltek continues to expand its relationships with Governments and the private sector, which are generally sectors with sticky demand. Finally, AS continues to benefit from industry tailwinds, with increasing demand for cloud-based services in recent years, driven by mass adoption due to the value proposition.

Network Software

Network Software (Roper)

Network Software ((NS)) is the most lucrative segment within the Roper business, growing equally well to AP. Growth has been driven by core competencies, with portfolio companies increasing ARPU, upselling, and continuing to win new customers.

DAT (Freight matching network, transportation management software, broker logistics software, fleet compliance) and Loadlink (Helps Canadian transportation companies facilitate the critical movement of goods by trucks through the use of its technology) in particular have performed extremely well recently, partially due to the tailwinds in the freight industry in recent years.

Foundry (Designs creative software technologies used to deliver visual effects and 3D content) began transitioning toward a subscription model in 2023, creating scope for increased financial contribution as ARR begins to grow. This should also create margin accretion from the business.

Finally, the healthcare businesses continue to boast strong customer retention, supporting strong ARR. With an aging population in the West, this segment (beyond just NS) represents a key opportunity for Roper long term.

Technology Enabled Products

Technology Enabled (Roper)

Technology Enabled Products ((TEP)) is the only material non-software segment of the business. Despite this, margins are strong, although there has been son dilution in recent quarters.

The segment has struggled with supply chain issues, contributing to increased costs. Portfolio companies have done well to increase prices and optimize where possible. Neptune (Pioneer in the development of Automatic Meter Reading and Advanced Metering Infrastructure technologies for water utilities) and NDI (Provides optical and electromagnetic measurement systems for medical and industrial applications.) continue to lead the pack in performance, reflecting the quality of their solutions. Further, both businesses are benefiting from industry tailwinds. NDI is supported by increased demand for technology-assisted medical treatments, which improve reliability and the provision of complex solutions. Further, Water treatment remains infantile in technological incorporation, representing an opportunity.

Trends

As we previously discussed, Roper is razor focused in identifying globally important industries. Below we will briefly discuss key trends we believe will benefit Roper's portfolio companies (and future acquisitions), with examples of portfolio companies.

The growing availability and collection of large datasets, as well as the desire to extract meaningful insights is driving the demand for advanced analytics capabilities. We are in the midst of a data era, with social media companies valued in the tens of billions for this very reason. Due to this, the demand for actionable insight from raw data is a key issue firms are seeking to address, with AI potentially offering this capability. (Construct Connect, Clinisys)

The increasing adoption of cloud computing is a key trend impacting most industries around the globe. With increased data accumulation and globalization of teams, companies are increasingly seeking cloud solutions to support efficient operations. (iPipeline, Strata)

Automation and technology-supported solutions are becoming important avenues for businesses to explore. This comes as computing power exponentially increases, creating opportunities to optimize operations that otherwise are inferior. (CBORD, NDI)

The healthcare and life sciences sector is experiencing rapid advancements in technological incorporation. The nature of the processes (testing, data analysis, etc) benefits heavily from increased computing capabilities, similar to the data point above. With continued growth in the healthcare industry, we will only see spending on supportive capabilities increase. (Softwriter, SHP)

The Covid-19 pandemic illustrated key weaknesses in the global supply chain while globalization continues to create complexity in operations. We are seeing companies increase investment in their supply chain, seeking optimization, flexibility, visibility, and resilience. This is part of a risk management exercise to reduce the downside potential while maximizing upside. Especially with the current inflationary pressure, businesses are increasingly seeking scope for improvement. (Deltek, iTradeNetwork)

Margins

Roper's margins are highly attractive. The company currently has an EBITDA-M of 40% and a normalized NIM of 20-30% (Currently inflated due to the sale of assets).

We do not need to sell how impressive this is. The margins are a reflection of the niche nature of the companies it acquires, allowing for strong pricing and upselling. Further, as they are predominantly software companies, the margin cost to provide an additional subscription is low.

Roper's normalized FCF is c.25-35% (Currently depressed by a one-off charge), with low cyclicality and sufficient Capex/debt coverage.

Balance sheet

Roper is moderately financed, with an ND/EBITDA ratio of 2.4x. Our view is that a 3x level is a healthy maximum for "the average" business, although the subscription & non-cyclical nature of Roper means it can likely afford more. At this level, the financing of M&A becomes very important. Roper needs to ensure it is financing at a 2.4x multiple or lower ideally, in order to sustain the current level.

Dividend payments have grown at a CAGR of 19%, which is highly impressive. Despite this, the absolute payments are unimpressive (yield of c.1%).

Valuation

Roper valuation (Tikr Terminal)

Roper is currently trading at 28x NTM earnings and 22x NTM EBITDA. This is a premium valuation, especially as many companies have experienced a drawdown in the last year.

This valuation is also a noticeable premium to Roper's historical average, implying its share price is increasing faster than its financial performance.

Our view is that this premium is justified. Throughout the decade, Roper has increased its margins without reducing growth, continuing to pay good prices for fantastic businesses. Said acquisitions are continuing to develop well within the Group, focusing on increasing their ARR and expanding where possible.

Roper benefits highly from valuation arbitrage, purchasing companies for a valuation below its own, realizing immediate gains. This reflects market confidence in its ability to execute the criteria we highlighted above it add value.

Key risks with our thesis

The risks to our current thesis are:

- Roper has begun purchasing larger businesses, which creates greater execution risk. Vertafore, for example, was acquired for over 10% of the company's current market value.

- With current debt levels, we could see M&A activity begin to slow. This would change investor forecasts around growth trajectory.

- Increased competition from Private Equity could force Roper into overpaying for assets or missing out on high-quality businesses.

Final thoughts

We are a big fan of Roper and its strategy. The company has incredible margins and a good growth trajectory. Our expectation is for the current businesses to develop further, continuing to improve margins as subscription-based models are initiated/enhanced. This will be supplemented by greater M&A in the same vein as previously.

For further details see:

Roper Technologies: Incredibly Profitable M&A Strategy That Wins